MNI EUROPEAN MARKETS ANALYSIS:South Korea Gets 15% Tariff Rate

- Fallout from the hawkish Fed hold on Wednesday was evident in terms of some higher USD/Asia FX pairs today. G10 FX performed better. AUD and NZD were aided by a surge in US equity futures following better Meta/Microsoft earnings news. USD/JPY is lower, with the BoJ raising its inflation forecast but seemingly not in a hurry for further rate hikes given a still uncertain outlook.

- US Tsy yields edged down slightly, while South Korea secured a 15% reciprocal tariff deal with the US (similar to Japan's outcome)

- China official PMIs softened more than expected for July, while Australia retail sales posted a solid June bounce.

- Later US June PCE spending/prices, July Challenger job cuts, Q2 employment cost index, jobless claims and MNI July Chicago PMI are released. Also, July France/Germany CPI and June euro area unemployment print.

MARKETS

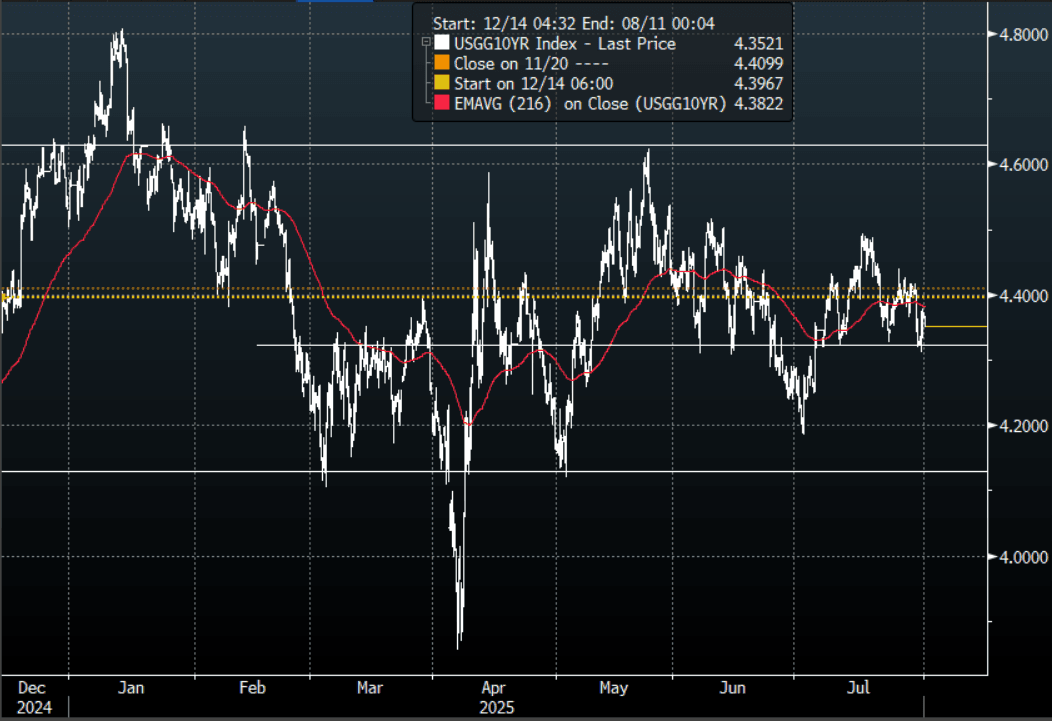

The TYU5 range has been 110-31 to 111-04+ during the Asia-Pacific session. It last changed hands at 111-03+, up 0-03 from the previous close.

- The US 2-year yield has shifted lower trading around 3.92.4%, down 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.352%, down 0.01 from its close.

- The 10-year yield has again held the support around its pivot within the wider range 4.10% - 4.65%, decent supply was seen around the 4.30/35% area once more. This would need to clear above the 4.45% area to potentially regain upward momentum now.

- Nick Timiraos on X: ”September’s Fed decision hinges on data clarity. If the recent muddle persists, that “could make it very tough—if it’s not bad enough to make it a slam dunk to cut, and it is not good enough to declare victory,” says Rich Clarida.”

- “Powell gives the Heisman stiff-arm to any attempt to get pinned down on September. Responding to a leading hypothetical on what would generate a rate cut in September: "I'm not going to say that, no. We're just going to need to see the data. It could go in many different directions." "We're going to make a judgment based on all of the data and based on the balance-of-risks analysis."

- Data/Events: Challenger Job Cuts, Personal Income, PCE, ECI, Initial Jobless Claims, MNI Chicago PMI

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Bonds Unwind Initial Post-BoJ Cheapening, Lab Mkt Data Tomorrow

JGB futures are little changed, -2 compared to settlement levels, after reversing initial weakness seen after the release of the BoJ Policy Decision.

- The BoJ held rates steady at 0.50%, as widely expected. The decision by the board was also unanimous. The central bank nudged down the degree of uncertainty surrounding the outlook. It noted: "it remains highly uncertain how trade and other policies in each jurisdiction will evolve and how overseas economic activity and

prices will react to them." In the previous statement, these uncertainties were judged 'extremely' high. - On balance, the statement brings us marginally closer to a further rate hike, given the central bank's degree of uncertainty was slightly softened. Still, the BoJ seems unlikely to act in the near term (the next policy meeting is on Sep 19, followed by Oct 30). It has time to assess key macro trends and obtain greater clarity around the outlook (i.e. move away from high uncertainty around the trade/external outlook).

- Cash JGBs are little changed across benchmarks out to the 20-year and 1-2bps cheaper beyond. The benchmark 10-year yield is 0.1bp higher at 1.562% versus the cycle high of 1.616%.

- Swap rates are flat to 1bp lower.

- Tomorrow, the local calendar will see Jobless Rate and Job-To-Applicant Ratio data.

BOJ: On Hold As Expected, Uncertainty Around Outlook Still High

The BoJ held rates steady at 0.50%, as widely expected. The decision by the board was also unanimous. The central bank nudged down the degree of uncertainty surrounding the outlook. It noted: "it remains highly uncertain how trade and other policies in each jurisdiction will evolve and how overseas economic activity and

prices will react to them." In the previous statement, these uncertainties were judged 'extremely' high.

- On inflation the central bank noted, "The projected year-on-year rate of increase in the CPI (all items less fresh food) for fiscal 2025 is higher, mainly due to the effects of the rise in food prices. The projected rates of increase in this CPI for fiscal 2026 and 2027 are more or less unchanged." The current fiscal year projection was raised to 2.7% from 2.2%, while for 2027 it was nudged up to 2.0% from 1.9%.

- On growth: "Japan's economic growth is likely to moderate, as trade and other policies in each jurisdiction lead to a slowdown in overseas economies and to a decline in domestic corporate profits and other factors, although factors such as accommodative financial conditions are expected to provide support." It added: "Comparing the projections with those presented in the previous Outlook for Economic Activity and Prices (Outlook Report), the projected real GDP growth rates are more or less unchanged." Current financial year growth is forecast at 0.6%, while for 2027 it is forecast at 1.0%.

- Risks to growth are skewed to the downside, while inflation risks are generally balanced the BoJ noted.

- The BoJ maintained its policy outlook: "WILL CONTINUE TO RAISE POLICY RATE IF ECONOMY, PRICES MOVE IN LINE WITH FORECAST, IN ACCORDANCE WITH IMPROVEMENTS IN ECONOMY, PRICES" - (Rtrs).

- On balance, the statement brings us marginally closer to a further rate hike, given the central bank's degree of uncertainty was slightly softened. Still, the BoJ seems unlikely to act in the near term (the next policy meeting is on Sep 19, followed by Oct 30). It has time to assess key macro trends and obtain greater clarity around the outlook (i.e. move away from high uncertainty around the trade/external outlook).

JAPAN DATA: Local Investors Sell Offshore Debt, But Recent Trends Still Positive

Offshore flows for Japan bond and equity markets were mixed last week. Local investors sold offshore bonds for the first time since early June. Since mid June we have had cumulative buying for this segment of over ¥5.6trln, including the modest outflow last week. Hence the trend still remains positive for Japan purchases of offshore debt. Global bond returns are off early July cycle highs but remain well up for the year. Local investors bought overseas equities for the second straight week, but the cumulative trend over recent months remains negative.

- In terms of inbound flows, offshore investors continued to buy local stocks. Indeed, since the start of April we have only had one week of outflows for this segment. Cumulative buying of Japan stocks over this period is nearly ¥10trln.

- Offshore investors sold local bonds last week, marking the third in the last four weeks we have seen net selling. Cumulative buying is still modestly positive for the past two months.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending July 25 | Prior Week |

| Foreign Buying Japan Stocks | 743.3 | 571.9 |

| Foreign Buying Japan Bonds | -184.6 | -990.7 |

| Japan Buying Foreign Bonds | -331.6 | 1643.8 |

| Japan Buying Foreign Stocks | 206.3 | 333.6 |

Source: Bloomberg Finance L.P./MNI

JAPAN DATA: IP Growth Exceeds Forecasts, Autos Nudges Higher Despite Tariffs

Japan June industrial production (IP) growth was better than forecast. We rose 1.7%m/m, against a -0.8% forecast and May slip of 0.1%. The y/y outcome printed at +4.0%y/y, versus 1.3% forecast and -2.4% for May. The y/y outcome was the strongest pace since May 2023. The June retail sales print was also better than forecast, up 1.0%m/m versus 0.5% forecast, which left us at +2.0%y/y, against a 1.8% forecast and 1.9% prior (which was revised down from the originally reported 2.2%).

- For IP, strength in production was for capital goods and construction. Consumer related production was negative in the month. In y/y terms capital goods production posted a healthy rise, +9.0%.

- Ex transport capital goods IP growth was -0.2%, but autos still managed a modest rise of 0.1%, despite tariff headwinds from the US.

- This is likely to be seen as a resilient result in the face the tariff threat, particularly as Japan managed to negotiate a lower reciprocal tariff rate (of 15%).

- On the retail side, most categories saw positive m/m outcomes, except for fuel and department stores. Y/Y total retail spend remains off recent highs and is around mid range for the past few years.

AUSSIE BONDS: Modestly Cheaper, Narrow Ranges Despite Upbeat Data

ACGBs (YM -4.5 & XM -2.5) remain weaker after trading in narrow ranges.

- Q2 retail sales volumes were stronger-than-expected, rising 0.3% q/q after 0.1%, the fourth consecutive rise bringing annual growth to 1.5%, the highest in almost three years. RBA Deputy Governor Hauser noted today that consumption growth has not recovered as expected, given the pickup in real disposable income growth and low unemployment.

- The number of building approvals rose sharply in June, driven by the volatile multi-dwelling component. They were up 11.9% m/m after a downwardly-revised +2.2% in May, with private houses down 2.0% m/m but non-houses jumped 33.1% m/m.

- Cash US tsys are ~2bps richer in today’s Asia-Pac session after yesterday’s post-FOMC sell-off.

- Cash ACGBs are 1-3bps cheaper with the AU-US 10-year yield differential at-8bps.

- The bills strip is weaker, with pricing -3 to -5.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in August is given a 97% probability, with a cumulative 60bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Tomorrow, the local calendar will see Cotality Home Values, S&P Global PMI Mfg and PPI data.

- The AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond tomorrow.

AUSTRALIA DATA: Retail Sales Improve In Q2

- Q2 retail sales volumes were stronger-than-expected rising 0.3% q/q after 0.1%, while June values rose 1.2% m/m after an upwardly-revised 0.5% (see press release here).

- June building approvals jumped 11.9% m/m after 2.2% due to the volatile multi-dwelling component as private houses fell 2% m/m.

- Export prices fell 4.5% q/q in Q2, more than expected, while import prices were down 0.8% after +2.1% and +3.3% respectively.

- RBA’s measure of private credit rose 0.6% m/m & 6.8% in June, in line with May.

RBA: Economy Developing As Expected, May Be “Scarring Effect” On Consumers

Deputy Governor Hauser’s comments at the Barrenjoey economic forum suggest that the RBA currently views the economy as evolving as expected. He noted that Q2 trimmed mean inflation and unemployment prints were in line with projections. The Q2 CPI data was “very welcome”. In May, there was 50bp of H2 easing assumed in the outlook.

- The Board is debating about how much momentum the economy has and in this context he noted that consumption growth has been underwhelming despite real income growth and low unemployment. The misery index suggests that consumer confidence should have improved more than it has which could be because of a “scarring effect” from recently falling real incomes, but that is difficult to model and may reflect “something special now”.

- A pickup in consumption growth in other countries as well as Australia’s positive real income growth is positive for the spending outlook. But if productivity growth stays weak, consumption could still disappoint.

- Unemployment remains historically low and firms are saying that while it is easier to find staff it still takes time and they have to pay the right rate. But there are signs that the labour market is rebalancing.

- His favourite charts have the cone around the base case for a variable, which in the case of the unemployment rate was very wide. So, it is easy to be surprised by unemployment but if it were to rise sharply, then the Board would have to react.

- In terms of tariffs, Hauser noted that the impact was less severe than feared as the worst duties and retaliation haven’t happened and as such the rise in the effective global tariff has been modest. Also, the global economy may be more resilient with frontloading/diverting of shipments but should be careful as the impact could be seen over the longer-term.

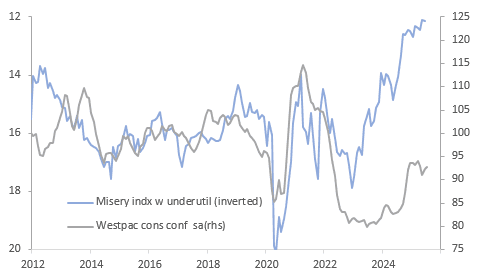

AUSTRALIA: “Misery Index” Suggest Consumer Confidence Should Have Improved More

RBA Deputy Governor Hauser talked today about how consumer confidence has not improved as much as the “misery index”, combination of inflation and unemployment, implied. He wondered if this was due to a “scarring effect” from high inflation driving real disposable incomes lower in recent years, but noted that the RBA has been unable to model it suggesting that there may be “something special now compared with the past”.

- Post-Covid, the misery index peaked at 11.7% in December 2022 with the unemployment rate at only 3.5% but headline inflation at 7.8%. It has come down to 6.2% in June 2025 with the unemployment rate only 0.8pp higher but headline inflation 5.7pp lower.

- Westpac consumer confidence began to improve mid-2023, following the misery index by six months. The pickup though stalled at the start of this year, even before US tariffs were announced and despite 50bp of RBA easing. In July it printed at 92.9 down slightly from December’s 93.7. The misery index improved 0.3pp since end-2024.

Australia consumer confidence vs misery index

Source: MNI - Market News/LSEG

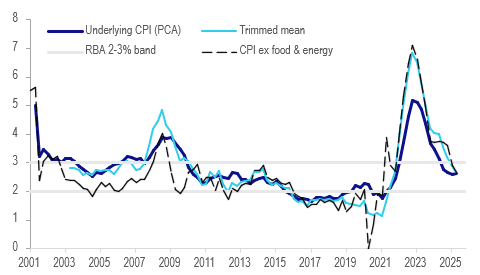

AUSTRALIA: Core Inflation Measures Converging As Moderate Towards Mid-Point

The Q2 trimmed mean measure of inflation moderated further towards the RBA’s target mid-point of 2.5%. It printed at 2.7% with the 2q/2q average annualised at 2.6%. Our PCA measure of underlying inflation came in at 2.6% for the second straight quarter, very close to the band mid-point. The downtrend in core inflation as well as market services inflation now within the 2-3% band should reassure the RBA that inflation is sustainably within target and result in a 25bp cut on August 12.

- There are different ways of measuring underlying inflation – trimmed mean, excluding volatile items such as food and energy, the median. We have another version using principal components analysis (PCA) based on Bank of Canada research. They are all now within the RBA’s 2-3% band.

- PCA is useful for when there are a large number of variables, as it finds common patterns that explain most of the variance in the data. In this case, it extracts the common movement in prices and thus creates a measure that reflects underlying developments in inflation and not sector-specific shocks.

- The chart below shows PCA CPI against other inflation measures. It is less volatile, with a standard deviation below that of the trimmed mean. After running ahead of the trimmed mean from 2019 until mid-2021, the two have converged around 2.6-2.7% along with other underlying measures of inflation. The gap was as wide as 1.5pp in Q4 2022.

Australia underlying inflation y/y %

Source: MNI - Market News/ABS/LSEG

- The share of CPI components rising more than 3% in Q2 was slightly higher than in Q1 at 36.8% after 35.6%. However, this is below the historical average and low compared to 2022-2024. Little change to the share and unchanged PCA core inflation may be signalling a stabilisation.

- The median CPI moderated 0.1pp to 2.1% y/y in Q2, it has been within the RBA’s band for the last 5 quarters.

BONDS: NZGBS: Closed Mid-Range But Outperformed US Tsys

NZGBs closed mid-range, with yields flat.

- After the negative post-FOMC lead-in from US tsys, NZGBs opened weaker but reversed direction as US tsys rallied ~2bps in today’s Asia-Pac session.

- NZGBs outperformed US tsys on the day, with the NZ-US 10-year yield differential 4bps lower at +16bps.

- Today’s weekly supply drew a powerful bid tone, with cover ratios of 3.72x (May-34) to 4.90x (May-30).

- “Housing and personal consumer lending from registered banks grew to NZ$381.59 billion in June from NZ$379.91 billion in the previous month. Such lending from non-bank lending institutions was broadly flat in the month at NZ$12.09 billion, compared with NZ$12.05 billion in the prior month.” (MTN via BBG)

- Swap rates closed 1-2bps higher, with the 2s10s curve marginally flatter.

- RBNZ dated OIS pricing closed little changed across meetings. 20bps of easing is priced for August, with a cumulative 34bps by November 2025.

- Tomorrow, the local calendar will see ANZ July consumer confidence and June building permits data.

FOREX: USD Gets A Boost From A Hawkish Powell

The BBDXY has had a range of 1217.30 - 1219.06 in the Asia-Pac session, it is currently trading around 1218, -0.05%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking has been seen. Monday’s US-EU trade deal was seen as a big loss for the European Union and this has provided the USD bounce with further tailwinds. A hawkish tone from Powell has added to the USD’s tailwinds and to the shorts woes. A sustained move back above the 1220 area would begin to really pressure the shorts in the short-term, but offer better levels for the market to re-enter shorts possibly back towards the 1240/50 area. The market will now be looking towards NFP on Friday.

- EUR/USD - Asian range 1.1404 - 1.1438, Asia is currently trading 1.1425. The pair saw some heavy selling putting in a top towards 1.1800 for now. The price looked a little stretched in the short term, and with the USD making a recovery the EUR is set for a correction of sorts. It broke the first support around the 1.1550 area and is now testing the more important 1.1300/1.1400 area, where I would expect demand first up.

- GBP/USD - Asian range 1.3234 - 1.3263, Asia is currently dealing around 1.3260. This pair looks like it is now breaking lower indicating a deeper correction. Support seen now back towards 1.3100/1.3200 and look for supply now on bounces back towards 1.3500.

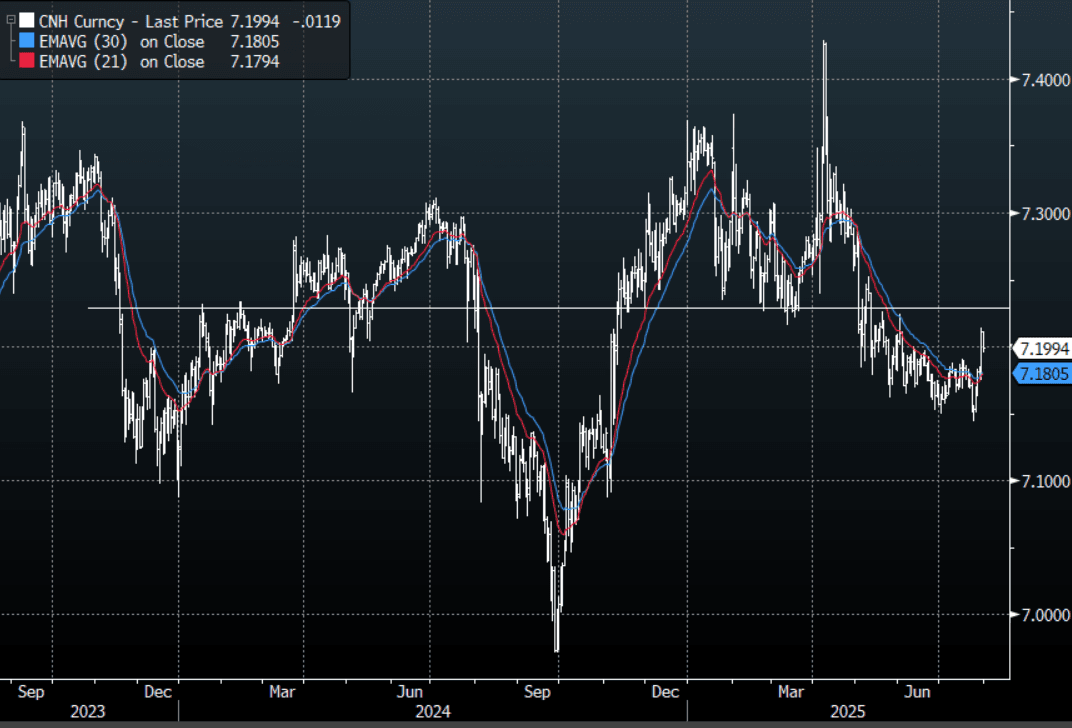

- USD/CNH - Asian range 7.1959 - 7.2113, the USD/CNY fix printed 7.1494, Asia is currently dealing around 7.2000. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.97%, Gold $3296, US 10-Year 4.354%, BBDXY 1217, Crude Oil $69.87

- Data/Events : Germany Import Prices/Unemployment & CPI, France CPI & PPI, Italy unemployment & CPI, EZ Unemployment

Fig 1: USD/CNH Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

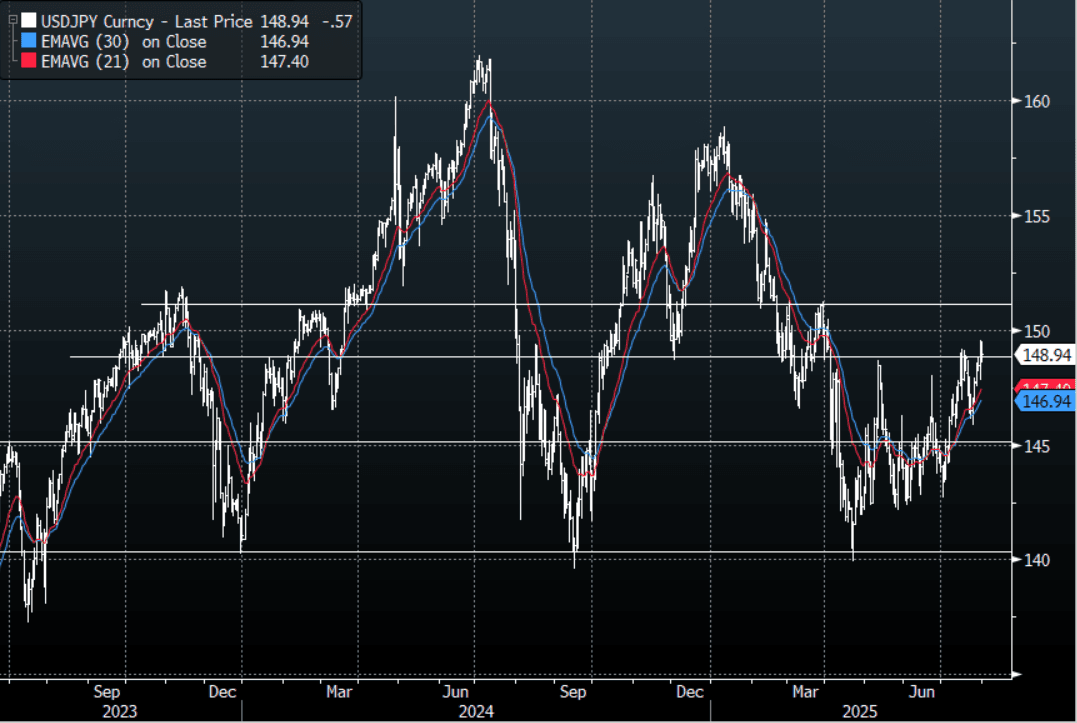

JPY: Asia Wrap - BOJ Raises Inflation Forecast To Help JPY

The Asia-Pac USD/JPY range has been 148.59 - 149.51, Asia is currently trading around 148.80, -0.45%. USD/JPY drifted lower into the BOJ and then took another leg as inflation forecasts were raised. The pair caught between a hawkish Powell and a hawkish BOJ. How the USD trades going into the NFP print tomorrow will probably dictate short-term moves. First support back towards 146/147 and on the topside the pivotal 151/152 area remains key.

- "BOJ Keeps rates unchanged, raises FY2025 inflation forecast to 2.7% from 2.2%" - BBG

- (Bloomberg) - “The BOJ’s hold decision looks at least as hawkish as the Fed’s, meaning that traders should start seriously considering September’s meeting as a live one for a Japanese rate hike.”

- JAPAN DATA Local Investors Sell Offshore Debt, But Recent Trends Still Positive: Offshore flows for Japan bond and equity markets were mixed last week. Local investors sold offshore bonds for the first time since early June. Since mid June we have had cumulative buying for this segment of over 5.6trln, including the modest outflow last week. Hence the trend still remains positive for Japan purchases of offshore debt. Local investors bought overseas equities for the second straight week, but the cumulative trend over recent months remains negative.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($971m).Upcoming Close Strikes : 147.00($1.52b Aug 1), 146.00($1.43b Aug 1) - BBG.

CFTC data shows Asset managers surprisingly added slightly to their JPY longs +72326( Last +71610), while leveraged funds have slightly reduced their newly built short JPY position -11571(Last -12606).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

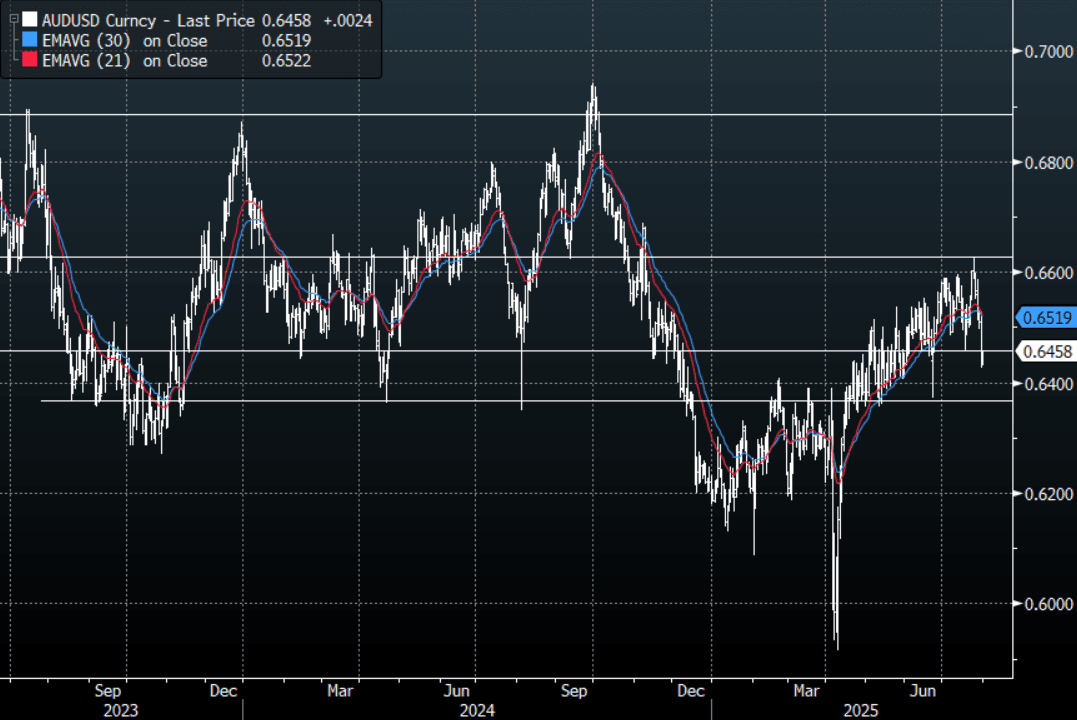

AUD: Asia Wrap - AUD/USD Gets A Boost From Retail and US Tech

The AUD/USD has had a range of 0.6433 - 0.6460 in the Asia- Pac session, it is currently trading around 0.6460, +0.40%. A stellar earning report from Metta and Microsoft saw US stocks surge back into the close. This morning has seen US futures take another leg higher as the market digests the late earnings reports as well a trade deal with South Korea, ESU5 +0.95%, NQU5 +1.35%. Upward momentum now looks to be clearly breaking down and the pivotal support back towards 0.6350 will now be key to hold the bears in check. A better retail print added to the tailwinds, lets see how far the AUD can bounce while stocks keep moving higher.

- AUSTRALIA DATA: Discounting Boosts Q2 Spending But Still Down Per Person. Q2 retail sales volumes were stronger-than-expected, rising 0.3% q/q after 0.1%, the fourth consecutive rise bringing annual growth to 1.5%, the highest in almost three years. RBA Deputy Governor Hauser noted today that consumption growth has not recovered as expected given the pickup in real disposable income growth and low unemployment. The ABS noted that per capita volumes fell again signalling that spending remains soft.

- AUSTRALIA: “Misery Index” Suggest Consumer Confidence Should Have Improved More. RBA Deputy Governor Hauser talked today about how consumer confidence has not improved as much as the “misery index”, combination of inflation and unemployment, implied. He wondered if this was due to a “scarring effect” from high inflation driving real disposable incomes lower in recent years, but noted that the RBA has been unable to model it suggesting that there may be “something special now compared with the past”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD1.38b), 0.6500(AUD710m), 0.6465(AUD1.01b). Upcoming Close Strikes : 0.6600(AUD847m Aug 5), 0.6550(AUD831m Aug 5) - BBG

- AUD/JPY - Asia-Pac range 95.87 - 96.28, Asia is trading around 96.15. The pair could not hold above 97.00 on Monday and drifted lower overnight into the FOMC, but has not really bounced back as would be expected considering the move higher in stocks. The support between 95.00 - 96.00 held very well last week and the pair is looking to regain its momentum for a move higher but this price action does not look great. A close back below 95.00 would be problematic for bulls.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

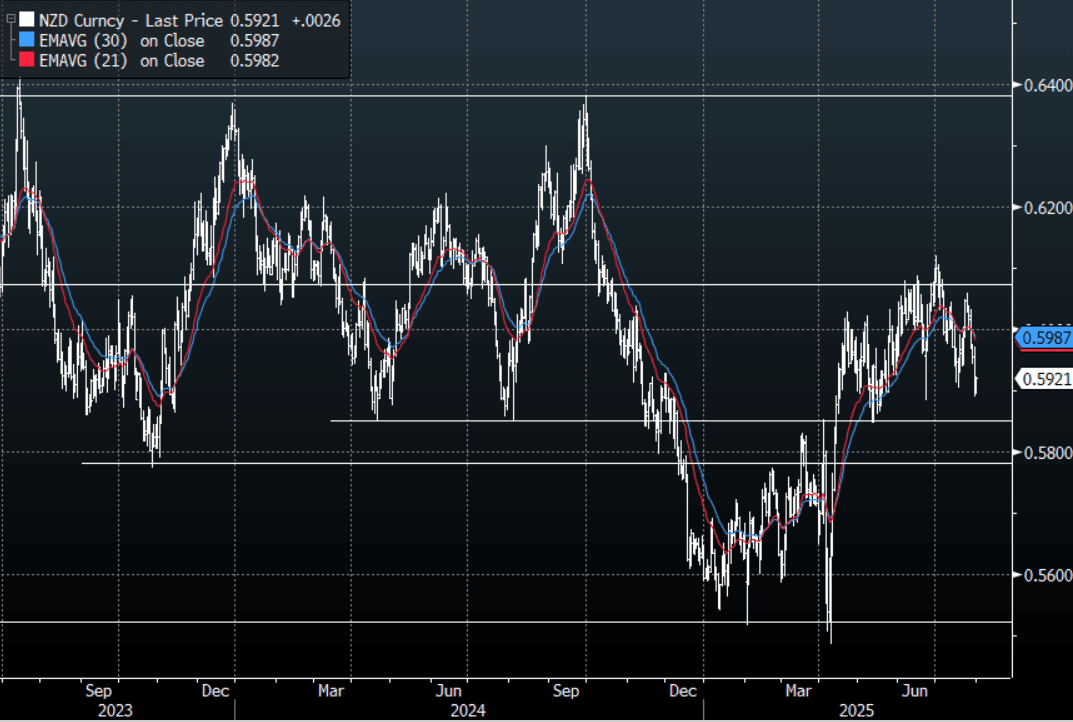

NZD: Asia Wrap - NZD/USD Gets Relief From US Tech Earnings

The NZD/USD had a range of 0.5894 - 0.5917 in the Asia-Pac session, going into the London open trading around 0.5915, +0.37%. The pair broke through 0.5950 and traded very poorly overnight with momentum lower being added by Powell’s hawkish tone. The support towards 0.5800/50 will now become pivotal, a sustained close back below there would start to look very bearish. Strong Tech Earnings has seen risk open better bid, this could provide the NZD/USD with some respite in our session to slow the recent slide, E-Minis +0.95%, NQU5 - +1.35%.

- Bloomberg - “Meta surged after a stronger-than-expected third-quarter revenue forecast signaled its core advertising business is still growing quickly enough to support aggressive AI spending. Microsoft also jumped as sales from its Azure cloud-computing unit grew 39%, faster than analysts anticipated.”

- CHINA Official PMIs Continue to Moderate: China's National PMIs continued to moderate in July. Ongoing weakness in domestic consumption and volatility in exports is exacerbating the concerns. Despite this, at China's Politburo on Wednesday, the nation's economic strength was saluted. That came after the country registered a record trade surplus in the first half of the year on soaring shipments to southeast Asia and stabilizing exports to the US.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5965(NZD504m). Upcoming Close Strikes : none. - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +5034(Last +8192), the Leveraged community added slightly to their shorts last week -7328(Last -6744).

AUD/NZD range for the session has been 1.0905 - 1.0924, currently trading 1.0915. The Cross continues to trade sideways as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Outperforms, Softer Trends Elsewhere

Asian equities are mostly weaker, outside of Japan market gains. This comes despite a much better US futures backdrop, although this is largely focused on the tech side, following late positive earnings/outlook news from both Meta and Microsoft in the US on Wednesday. Nasdaq futures were last up +1.35%, while Eminis were around +0.95% higher.

- Japan markets are seeing the Topix up close to 0.80%, while the NKY 225 is around 0.90% higher. Some positive spillover from US futures moves may be in play, while earlier the BoJ held rates steady, as widely expected. The level of uncertainty surrounding the trade outlook was described as high, but this was down from the previous meeting's description of 'extremely high'.

- The Taiex is also tracking slightly firmer, last up around 0.25%. The Kospi is struggling though, down close to 0.45%. This comes despite a positive trade deal outcome, at least at face value, with the US, where the reciprocal tariff rate will be 15%.

- China and Hong Kong markets are both down a little over 1% at the lunch time break. In Wednesday US trade the Golden Dragon index continued to decline, down a further 1.82% (marking the fifth straight session decline). Earlier data showed slightly softer than expected official PMI reads for China in terms of July. Manufacturing remains in contraction territory.

- In South East Asia, markets are weaker, although losses are not beyond 1% at this stage. Thailand and Malaysia await tariff level announcements from the US. US President Trump has doubled down on criticism of Indian tariffs and their business with Russia. Benchmark Indian markets are off a little over 0.60%.

ASIA STOCKS: Tech Related Inflows Dominate, Indian July Outflows Over $2bn

Yesterday saw positive inflow momentum for tech related plays in terms of South Korea and Taiwan. Taiwan's net inflow yesterday nearly offset the prior day's outflow. Month to date Taiwan inflows are just short of $8bn. South Korea's month to date net inflows are just over $4.2bn. Given global tech equity trends, with Nasdaq futures outperforming strongly in the first part of trade today following better Meta and Microsoft earnings results, we could see continued focus on the AI/tech related space from a flow standpoint.

- Earlier Samsung's earnings result were below expectations, with the chip segment notably missing. Still, the recent chip deal with Tesla may help turn conditions around in this space. South Korea has also managed to negotiate a 15% reciprocal tariff deal with the US, similar to Japan's outcome. The Kospi is up around 0.25% in the first part of trade today.

- Elsewhere, Indian outflows continued, bringing month to date outflows to over $2bn. Trade deal uncertainty with the US continues as trump threatened a 25% tariff due to India's own barriers and purchases of Russian oil (negotiations continue though).

- Trends in South East Asia saw outflows. Indonesia will sell outflows this month, while Thailand is looking at inflows of close to $500mn.

Table 1: Asian Market Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 449 | 2040 | -5156 |

| Taiwan (USDmn) | 541 | 827 | 1856 |

| India (USDmn)* | -425 | -1891 | -10286 |

| Indonesia (USDmn) | -39 | -65 | -3672 |

| Thailand (USDmn)* | -8 | 138 | -1854 |

| Malaysia (USDmn) | -8 | -93 | -2929 |

| Philippines (USDmn) | -1 | -8 | -627 |

| Total (USDmn) | 509 | 948 | -22668 |

| * Data Up To July 29 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Slightly Lower, Watching Developments Against Russian Crude Buyers

Oil prices are only slightly lower today holding onto the significant gains made this week in the face of US President Trump’s threats against Russia and those who buy its fossil fuels. WTI reached a high of $70.41/bbl early in the APAC session but has trended lower since to be down 0.2% to $69.87. Brent is 0.3% lower at $73.05/bbl after a peak of $73.53. The USD index is down 0.2%.

- More US trade deals have been announced with India to face 25% tariffs plus an unspecified “penalty” for buying Russian oil and weapons, Brazil 50% for policies that threaten US security, while South Korea’s will be 15% in line with Japan and the EU. President Trump said today that India’s 25% was too high and so that doesn’t seem the final rate.

- With India to currently be penalised for buying Russian oil, the market is nervous that US restrictions particularly on third parties could materially impact global supplies. OPEC meets on August 3 to decide its production target for September and while another increase is widely expected, it has limited capacity to make up for any loss of Russian output.

- The US also increased restrictions on Iran targeting the shipping network and companies of Hossein Shamkhani. The EU sanctioned his business interests last week. His vessels are said to transport goods and oil from Russia and Iran around the world.

- Later US June PCE spending/prices, July Challenger job cuts, Q2 employment cost index, jobless claims and MNI July Chicago PMI are released. Also, July France/Germany CPI and June euro area unemployment print.

Gold Higher Today With Attention On US Data & Trade Deals

After falling 1.6% on Wednesday, gold is up 0.7% to $3296.7/oz today as it finds support from two FOMC members voting for a July rate cut and some punitive trade measures from the US against India and Brazil. It reached a high of $3298.61 earlier. US Treasury yields and the US dollar are lower today (BBDXY USD -0.1%) which will also be supporting the rally in bullion.

- More US trade deals have been announced with India to face 25% tariffs plus an unspecified “penalty” for buying Russian oil and weapons, Brazil 50% for policies that threaten US security, while South Korea’s will be 15% in line with Japan and the EU. President Trump said today that India’s 25% was too high and so that doesn’t seem the final rate.

- Trade deals will continue to be a focus with the clear possibility that negotiations will continue past the August 1 deadline. Today’s US PCE prices and Friday’s July payrolls will also be monitored closely.

- Silver is up 0.3% to $37.24, close to the intraday high which followed a low of $36.979.

- Equities are mixed with the S&P e-mini up 0.9% and Nikkei +0.9% but Hang Seng down 1.1% and KOSPI -0.7%. Oil prices are down with WTI -0.2% to $69.89/bbl. Copper has continued sinking and is -20.5%.

- Later US June PCE spending/prices, July Challenger job cuts, Q2 employment cost index, jobless claims and MNI July Chicago PMI are released. Also, July France/Germany CPI and June euro area unemployment print.

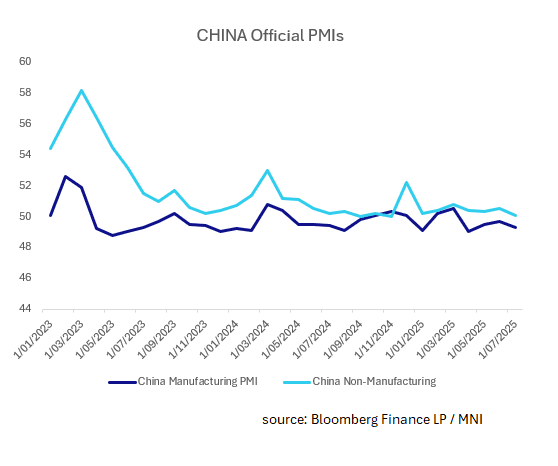

CHINA: Official PMIs Continue to Moderate

- China's National PMIs continued to moderate in July.

- In China, the two main Purchasing Managers' Indices (PMIs) are the National Bureau of Statistics (NBS) PMI and the S&P Global (formerly the Caixin PMI) . The NBS PMI focuses on larger, state-owned enterprises, while the Caixin PMI emphasizes smaller and privately owned businesses.

- The PMI Manufacturing moderated to 49.3 against a market estimate of 49.7 and prior of 49.7. New orders and the employment component declined from last month, driven mainly by the impact from the larger businesses.

- China' Non-manufacturing PMI was 50.1 (estimate 50.2) bringing the Composite to 50.2.

- Ongoing weakness in domestic consumption and volatility in exports is exacerbating the concerns.

- Despite this, at China’s Politburo on Wednesday, the nation’s economic strength was saluted. That came after the country registered a record trade surplus in the first half of the year on soaring shipments to southeast Asia and stabilizing exports to the US.

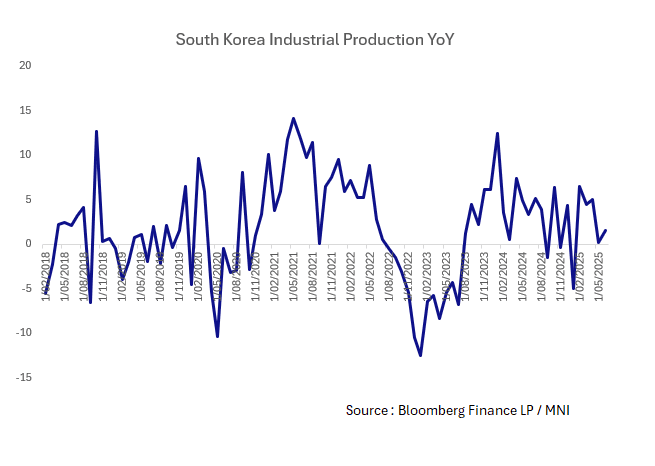

SOUTH KOREA: Industrial Production Up on Chip Demand

- After the revised date showed contraction in May, South Korea's June Industrial Production rebounded to +1.6%, but missed estimates.

- Industrial output rose 1.6% MoM (estimate +2.5%) versus revised -3.3% in May

- The recovery comes as exports rose +9.2% in June, despite the tariff threat still looming over the Korean economy.

- The demand for Korea's semi-conductor chips continues to buffet the economy, as chip exports jumped over 11% YoY in June offsetting the impact on the auto sector which is the most exposed to tariff risk.

- The miss versus expectations reflects the uncertainty that remains due to the trade war.

- The US President has threatened up to 25% tariffs on Korean goods. June's Industrial Production result quite likely reflects the need of exporters to ship product ahead of finalization of tariffs.

INDIA: Country Wrap : 25% US Tariffs to Come

- US President Donald Trump's decision to slap India with a 25% tariff and additional punitive duties for trade with Russia will shave off some economic growth, but a weaker rupee may extend some support. Key sectors, including textiles, pharmaceuticals, electronics, agri-products, and machinery, are expected to feel the brunt. The recent weakness in the Indian rupee, if sustained, could cushion the impact by making Indian products more competitive (source NDTV)

- After announcing a 25 per cent tariff and penalties for purchasing oil from Russia , US President Donald Trump said on Wednesday (local time) that Washington is continuing trade negotiations with New Delhi. He emphasized that India is one of the countries imposing high tariffs on the United States. (source MINT)

- The NIFTY 50 is giving back the last two days of gains this morning with falls of -0.65%.

- The Rupee continues to struggle, lower today by -0.10% and -1.4% over the last 5 trading days.

- Bonds are steady with the 10-year at 6.375%

INDONESIA: Country Wrap: Government Focuses on Key Trade Agreements

- The government’s multi-billion dollar ambition to move the production value chain across dozens of commodities will turn Indonesia into a powerful country, according to Energy Minister. Indonesia aims to process its abundant resources at home and turn them into higher-valued exports. For instance, the resource-rich country intends to turn its unprocessed nickel ores into stainless steel or even batteries to make more money in international trade. (source Jakarta Globe)

- The Indonesian government is accelerating the finalization of key trade agreements to reduce tariffs and broaden export market access, amid looming import duties from the United States. Secretary of the Coordinating Ministry for Economic Affairs confirmed the efforts during the Bisnis Indonesia Mid-year Challenges 2025 event this week. The United States is planning to implement a 19 percent import tariff on most Indonesian goods, reduced from a 32 percent rate announced in April. Certain goods such as processed nickel and coffee beans may qualify for lower rates. The US was Indonesia’s second-largest export market in 2024, accounting for 9.3 percent of total exports, or USD 28.18 billion. (source Business Indonesia)

- The Jakarta Composite has seen two consecutive days of falls for the first time in four weeks. After yesterday's close lower by -0.89%, it is lower today by -0.33% in what appears to be profit taking given rises of 8% for July.

- The Rupiah is one of the bigger fallers in the region today down -0.38% to 16,466 and is 1.40% weaker month to date.

- The bond market is weak with yields higher by +2.5-4.5bps across the curve, with the curve flattening. The 10year is at 6.58%

ASIA FX: USD Firmer Against Most SEA FX, CNH & KRW Outperform

Some South East Asian currencies have weakened noticeably in the first part of Thursday trade. PHP is the weakest performer, down around 1.3% in spot terms so far today. THB has lost ground, so too has MYR, INR and IDR. For INR and IDR intervention efforts have likely curbed USD upside. In North East Asia, CNH and KRW have outperformed, while TWD has lost ground.

- Spot USD/PHP has surged, the pair getting close to 58.38, last near 58.34, 1.3% weaker versus the USD so far today. Sensitivity to a hawkish Fed hold on Wednesday, coupled with month end dynamics look to be weighing on the Peso. Earlier 2025 highs around the 58.70/75 region are the likely next upside target.

- USD/IDR is up 0.40%, last close to 16460, eyeing a 16500 test. Similar dynamics could be in play, although headlines crossed earlier that the BI was intervening to curb rupiah losses.

- USD/INR opened higher, getting too 87.74, but sits back at 87.55/60 in latest dealings. We aren't too far away from a 88.00 test. INR is under pressure amid trump tariff threats, with earlier remarks from the US President suggesting a positive trade deal was unlikely to be announced in the near term (although it is likely both sides are still talking).

- USD/MYR is above 4.2500, while USD/SGD is lower, last near 1.2940, taking its cue from the better G10 tone seen against the USD. USD/THB is firmer, last near 32.70. Both Malaysia and Thailand are awaiting tariff/trade details from the US.

- USD/CNH is back under 7.2000, aided by the modest rise in the USD/CNY fixing (with the error term taking the bulk of Wednesday's USD gains). We did see softer PMI outcomes, but these didn't impact sentiment.

- USD/KRW is back under 1390, with the 15% trade deal outcome a positive in the broader context of Asian reciprocal tariff levels. USD/TWD is continuing to push higher, the pair now above 29.90. Like some parts of SEA, Taiwan is awaiting tariff/trade details from the US.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 31/07/2025 | 0600/0800 | ** | Import/Export Prices | |

| 31/07/2025 | 0630/0830 | ** | Retail Sales | |

| 31/07/2025 | 0645/0845 | *** | HICP (p) | |

| 31/07/2025 | 0645/0845 | ** | PPI | |

| 31/07/2025 | 0755/0955 | ** | Unemployment | |

| 31/07/2025 | 0800/1000 | *** | Bavaria CPI | |

| 31/07/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 31/07/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 31/07/2025 | 0900/1100 | ** | Unemployment | |

| 31/07/2025 | 0900/1100 | *** | HICP (p) | |

| 31/07/2025 | 1000/1200 | ** | PPI | |

| 31/07/2025 | 1200/1400 | *** | HICP (p) | |

| 31/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 31/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 31/07/2025 | 1230/0830 | * | Payroll employment | |

| 31/07/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/07/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/07/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/07/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 31/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 31/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 01/08/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 2330/0830 | * | Labor Force Survey | |

| 01/08/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/08/2025 | 0130/1130 | * | Producer price index q/q | |

| 01/08/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 01/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0800/1000 | * | Retail Sales | |

| 01/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/08/2025 | 0900/1100 | *** | HICP (p) | |

| 01/08/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/08/2025 | 1230/0830 | *** | Employment Report | |

| 01/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) |