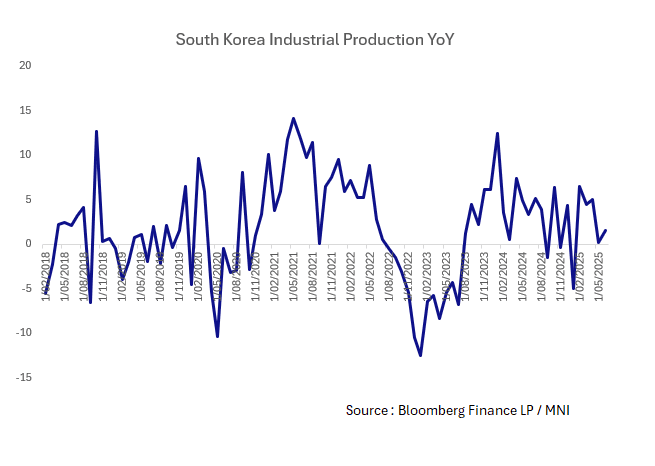

SOUTH KOREA: Industrial Production Up on Chip Demand

Jul-30 23:06

- After the revised date showed contraction in May, South Korea's June Industrial Production rebounded to +1.6%, but missed estimates.

- Industrial output rose 1.6% MoM (estimate +2.5%) versus revised -3.3% in May

- The recovery comes as exports rose +9.2% in June, despite the tariff threat still looming over the Korean economy.

- The demand for Korea's semi-conductor chips continues to buffet the economy, as chip exports jumped over 11% YoY in June offsetting the impact on the auto sector which is the most exposed to tariff risk.

- The miss versus expectations reflects the uncertainty that remains due to the trade war.

- The US President has threatened up to 25% tariffs on Korean goods. June's Industrial Production result quite likely reflects the need of exporters to ship product ahead of finalization of tariffs.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Richer With US Tsys, Trump Criticises Powell Again

Jun-30 23:02

In local morning trade, NZGBs are 2-3bps richer after US tsys finished near NY session bests, 3-6bps richer with a flatter curve.

- The moves come amid President Trump stepping up his criticism of Fed Chair Powell and his ‘entire board’ over the level of US interest rates.

- The Q2 NZIER business confidence survey showed improvement, but underlying activity remained weak. NZIER noted: "A net 27 percent of firms expect an improvement in general economic conditions over the coming months on a seasonally adjusted basis, which was a further lift from the net 23 percent in the March quarter."

- On inflation/costs: "Cost and pricing indicators suggest an easing in inflation pressures in the June quarter. The easing of capacity pressures is reflected in the continued dominance of firms reporting a lack of sales as the primary constraint on their business, as opposed to those reporting finding labour as the primary constraint."

- Swap rates are 1-2bps lower.

- RBNZ dated OIS pricing is slightly softer across meetings. 4bps of easing is priced for July, with a cumulative 33bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 2.75% May-51 bond.

MNI: UK JUN BRC SHOP PRICES +0.3% M/M, +0.4% Y/Y

Jun-30 23:01

- MNI: UK JUN BRC SHOP PRICES +0.3% M/M, +0.4% Y/Y

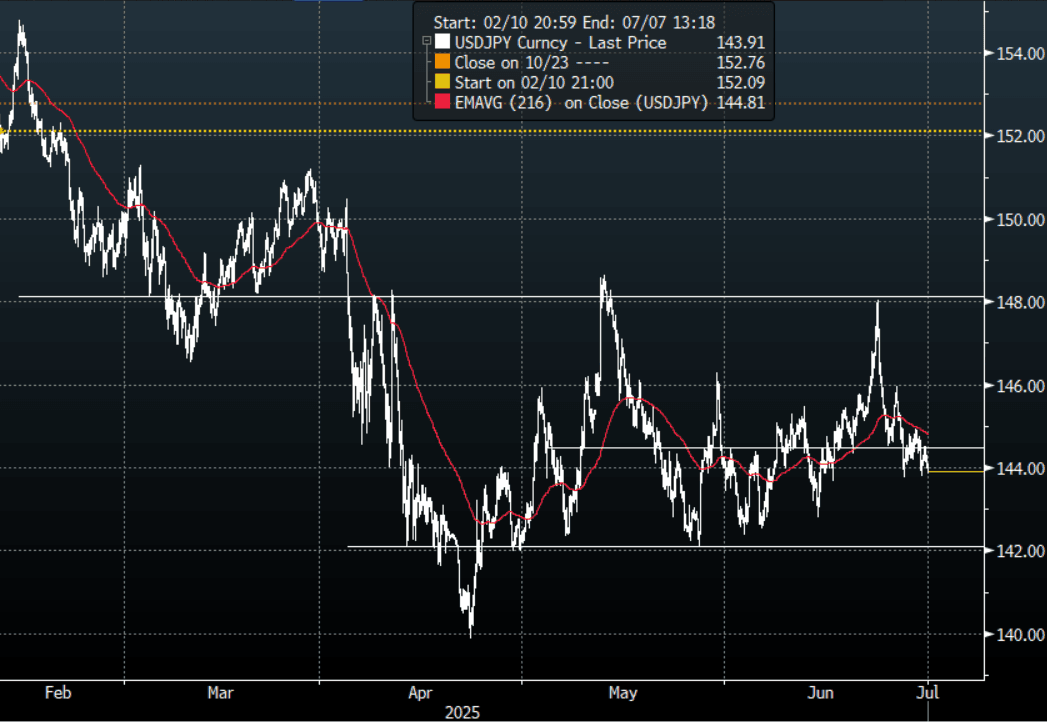

JPY: USD/JPY - Finding Support Around 144.00 For Now

Jun-30 22:52

The overnight range was 143.78 - 144.51, Asia is currently trading around 143.90. USD/JPY continues to find demand sub 144.00 for now, the price action does stand out with the USD looking like it's in freefall, and US yields extending their move lower. For the moment no clear direction in the middle of its wider 142.00 - 148.00 range with a bias to selling rallies.

- Bloomberg - “Trump threatened more penalties against Japan over what he said was the country’s unwillingness to accept US rice, with Kevin Hassett saying talks aren’t over.”

- (Bloomberg) - “The 25% sectoral tariff on automobiles - a key sector for Japan - remains a sticking point in trade talks with the US as Prime Minister Shigeru Ishiba's team continues to push hard for concessions. But factories are humming. Stocks are rising. The levy may not be the drag on growth the Bank of Japan had feared. Behind it all, a still-weak yen, for now, is doing its job - keeping production lines running.”

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY is looking for a fresh catalyst in the middle of its 142.00 - 148.00 range, while the USD continues to move lower this should see sellers on any bounce for now.

- CFTC data shows Asset managers paring back their JPY longs very slightly +93003, while leveraged funds added to their longs again trying to rebuild their position +15935.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($1.02b), 143.50(559m).Upcoming Close Strikes : 140.00($1.11b July3), 139.75($1.05b July 3).

- Data/Event : Tankan, S&P Global Japan PMI Mfg, Consumer Confidence Index

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P