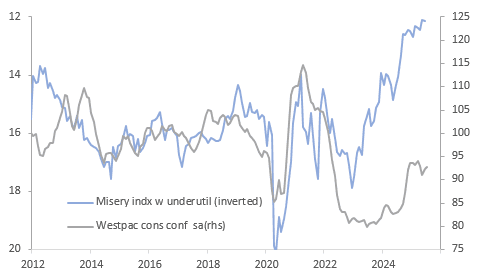

AUSTRALIA: “Misery Index” Suggest Consumer Confidence Should Have Improved More

RBA Deputy Governor Hauser talked today about how consumer confidence has not improved as much as the “misery index”, combination of inflation and unemployment, implied. He wondered if this was due to a “scarring effect” from high inflation driving real disposable incomes lower in recent years, but noted that the RBA has been unable to model it suggesting that there may be “something special now compared with the past”.

- Post-Covid, the misery index peaked at 11.7% in December 2022 with the unemployment rate at only 3.5% but headline inflation at 7.8%. It has come down to 6.2% in June 2025 with the unemployment rate only 0.8pp higher but headline inflation 5.7pp lower.

- Westpac consumer confidence began to improve mid-2023, following the misery index by six months. The pickup though stalled at the start of this year, even before US tariffs were announced and despite 50bp of RBA easing. In July it printed at 92.9 down slightly from December’s 93.7. The misery index improved 0.3pp since end-2024.

Australia consumer confidence vs misery index

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUD Crosses - AUD Bounces Overnight

So much for the huge Month-end and Quarter-end selling in US Stocks as the dip finds demand once more and new highs are seen. CFTC data out for last week shows both Asset Managers and Leveraged Funds added to their AUD short positions, given how poorly the USD is trading one would expect most of these shorts are being expressed in the crosses where the has AUD traded poorly particularly against the EUR and GBP. Should AUD/USD begin to build momentum higher through 0.6600 even these crosses will start to be challenged.

- EUR/AUD - Overnight range 1.7894 - 1.7964, Asia is currently trading around 1.7930. The pair again found some supply back towards the 1.8000 area overnight, it has had a good run higher but how the AUD/USD trades through 0.6550/0.6600 will be key. First support seen back towards the 1.7800 area, a break above 1.8000 and the move could extend higher.

- GBP/AUD - Overnight range 2.0848 - 2.0991, Asia is trading around 2.0895. This pair continues to meet supply towards the multiple tops above 2.1000. A sustained break above 2.1050 is needed to see the move higher regain momentum, like EUR/AUD though a more positive risk backdrop and the AUD/USD potentially breaking higher could potentially see this pair back off and move towards the lower end of its 2.0500 -2.1050 range.

- AUD/JPY - Overnight range 94.00 - 94.89, Asia is trading around 94.40. Choppy price action as the pair establishes a range between 92.00 - 96.00. Should risk build on this move, focus could turn back to the 96.00 area.

- AUD/NZD - Overnight range 1.0762 - 1.0798, the cross is dealing in Asia around 1.0790. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some direction.

Fig 1: GBP/AUD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

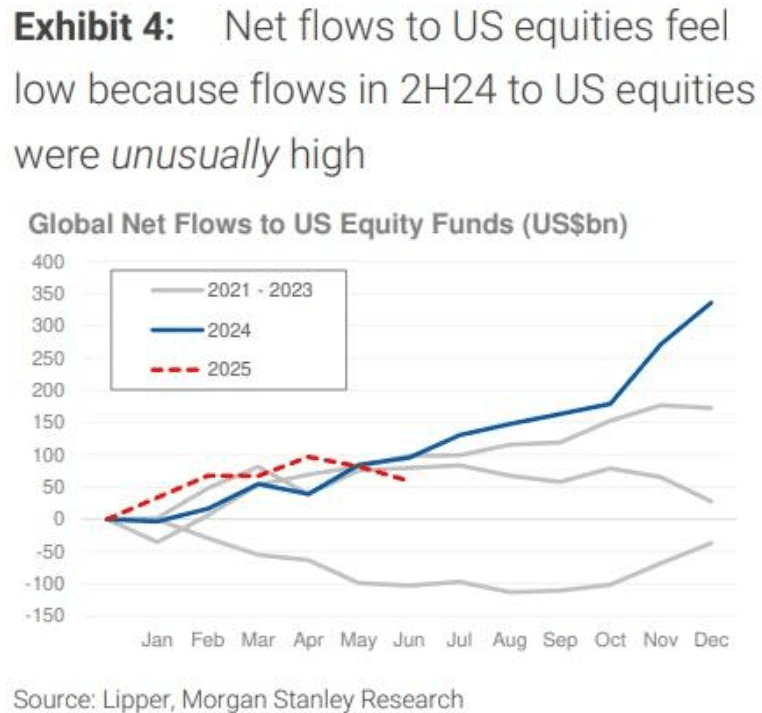

US STOCKS: Make New Highs Even With Month-End Selling

The ESU5 overnight range was 6224.25 - 6265.50, Asia is currently trading around 6255. So much for the huge Month-end and Quarter-end selling as the dip finds demand once more and new highs are seen. This morning has seen US futures open pretty flat in our session ESU5 +0.02%, NQU5 +0.02%.

- Andreas Steno Larsen on X: "US exceptionalism is back in equity markets but NOT in FX markets”

- Lance Roberts on X: ”One of the great narratives of late has been that investors are fleeing US assets. Weekly data suggests this is hardly the case in both stocks and bonds where net fund flows remain positive just at a slower pace than 2024” See Graph below.

- “Conerns from Deepseek to Tariffs are now just a distant memory as stocks crank out new highs. But with markets heading back into more exuberant levels, a risk of short-term pullback increases.”

- Zerohedge on X: “Hedge Funds Buy Stocks For 8th Straight Week: Pile Into Financials, Dump Energy.”

- The market has been caught underweight and with momentum type funds(CTA’s) adding through all-time highs these reluctant PM’s are being forced to return to the market.

- Short-term this does look a little overdone but dips should find demand, first support is back towards the 6100 area.

Fig 1: Global Net Flows To US Equity Funds

Source: MNI/@LanceRoberts/Morgan Stanley Research

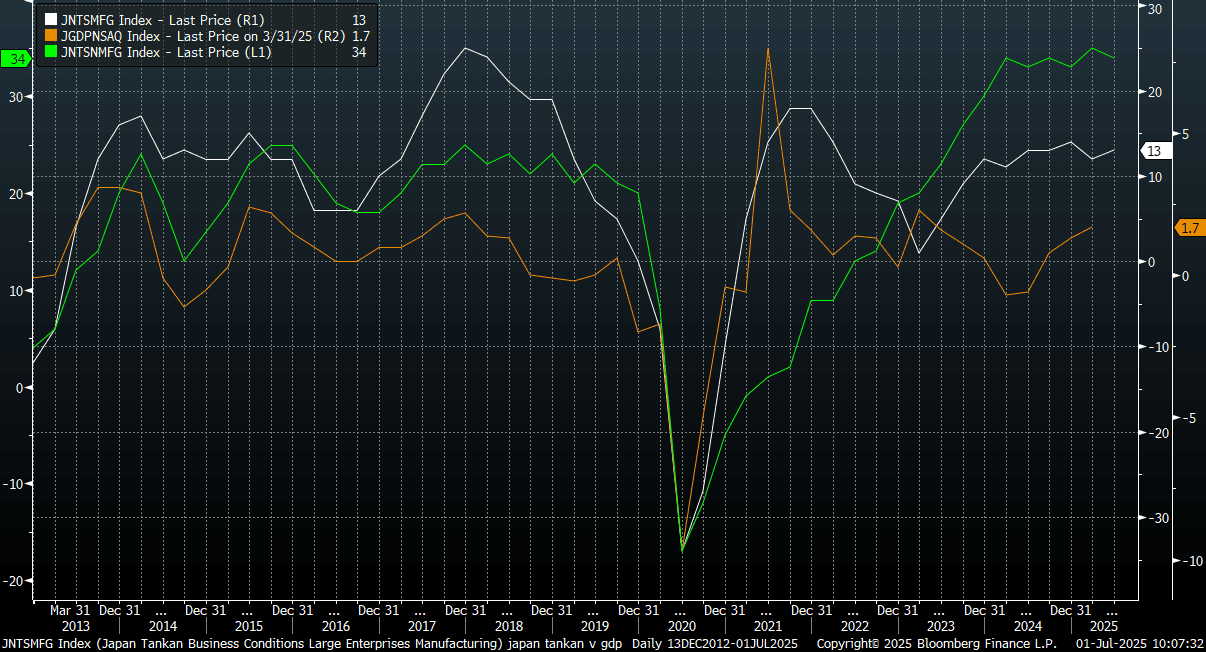

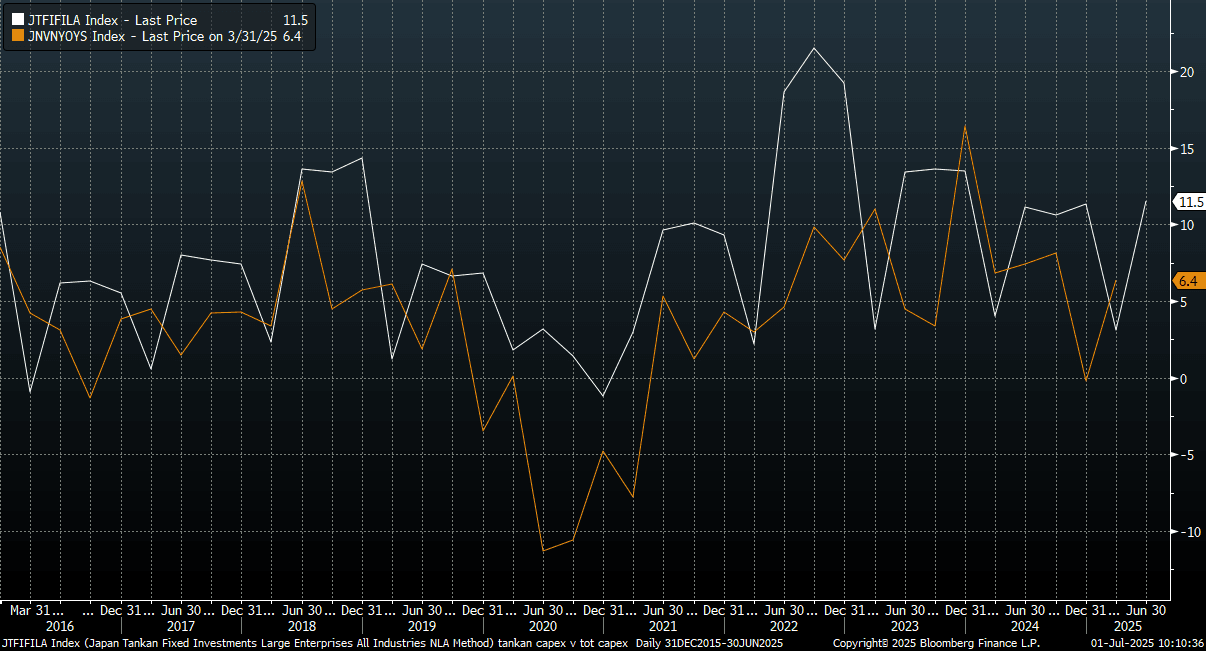

JAPAN DATA: Q2 Tankan Surprises On The Upside, Capex Outlook Firmer

The Q2 Tankan survey delivered some positive upside surprises. The large manufacturing index rose to 13, versus 10 forecast and 12 prior. The outlook for this segment was also better than forecast, printing at 12 (9 was forecast and 12 was the Q1 outcome). The all industry capex estimate was also stronger than expected, coming in at 11.5%, versus 10.0% forecast (3.1% was the prior outcome). For large non-manufacturing firms, the results were slightly less positive, with headline index at 34, in line with forecast, while prior was 35. The outlook printed at 27, below the expected 29 outcome (28 was recorded in Q1).

- For smaller firms, manufacturing sentiment levels remained below levels recorded for non-manufacturing firms. Both sectors saw outcomes close to forecasts, 1 for small manufacturing firms, 15 for non-manufacturing firms.

- The first chart below plots the headline large manufacturing and non-manufacturing indices versus y/y Japan GDP growth, which is the orange line on the chart. In the face of external headwinds, particularly in terms of the tariff threat, today's results point to a resilient backdrop. Both Tankan measures for large firms are just off recent highs.

- The second chart below plots the capex estimate from the Tankan survey the white line on the chart) against the capital investment, which is only out for Q1. This is pointing to a firmer capex backdrop for Q2, which again will please the authorities in the face of external headwinds.

Fig 1: Q2 Tankan Survey Results Paint Resilient Backdrop

Source: Bloomberg Finance L.P./MNI

Fig 1: Q2 Tankan Capex Estimate & Capex Y/Y

Source: Bloomberg Finance L.P./MNI