JAPAN DATA: IP Growth Exceeds Forecasts, Autos Nudges Higher Despite Tariffs

Japan June industrial production (IP) growth was better than forecast. We rose 1.7%m/m, against a -0.8% forecast and May slip of 0.1%. The y/y outcome printed at +4.0%y/y, versus 1.3% forecast and -2.4% for May. The y/y outcome was the strongest pace since May 2023. The June retail sales print was also better than forecast, up 1.0%m/m versus 0.5% forecast, which left us at +2.0%y/y, against a 1.8% forecast and 1.9% prior (which was revised down from the originally reported 2.2%).

- For IP, strength in production was for capital goods and construction. Consumer related production was negative in the month. In y/y terms capital goods production posted a healthy rise, +9.0%.

- Ex transport capital goods IP growth was -0.2%, but autos still managed a modest rise of 0.1%, despite tariff headwinds from the US.

- This is likely to be seen as a resilient result in the face the tariff threat, particularly as Japan managed to negotiate a lower reciprocal tariff rate (of 15%).

- On the retail side, most categories saw positive m/m outcomes, except for fuel and department stores. Y/Y total retail spend remains off recent highs and is around mid range for the past few years.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JAPAN DATA: Q2 Tankan Surprises On The Upside, Capex Outlook Firmer

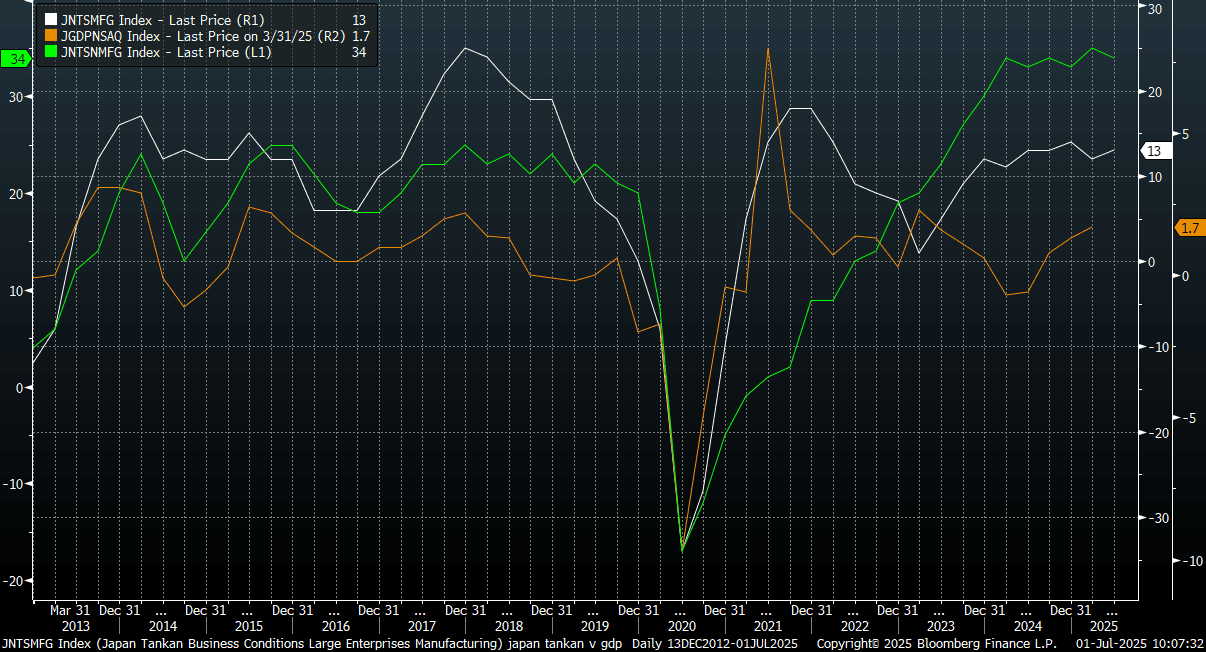

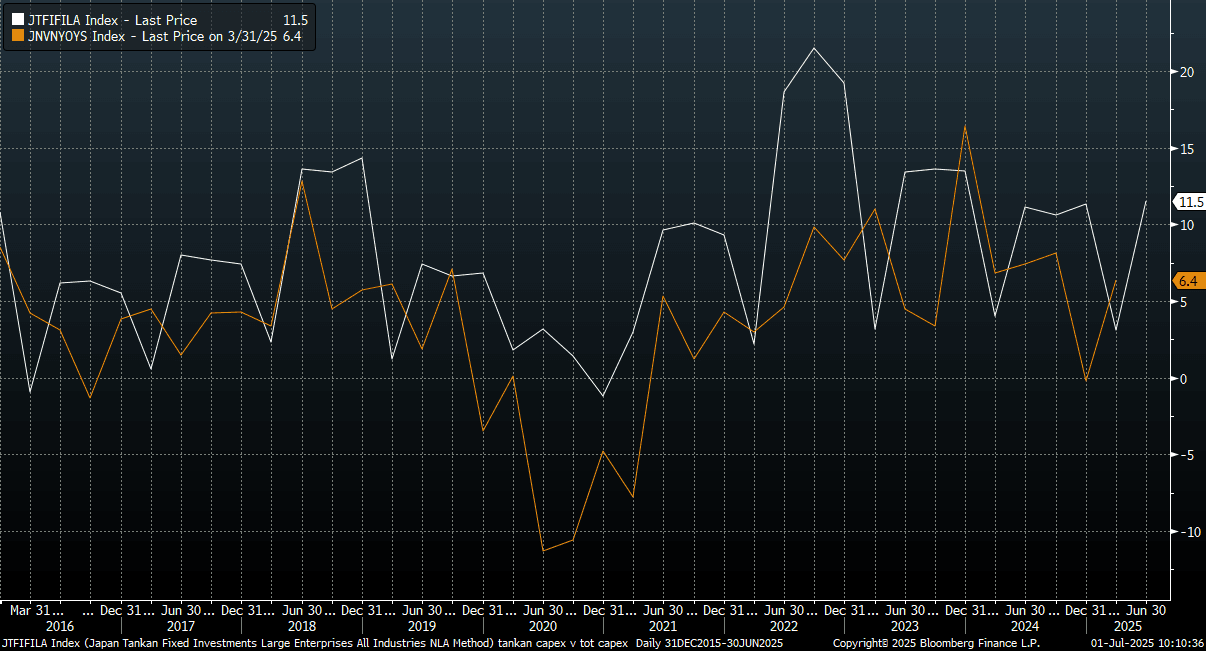

The Q2 Tankan survey delivered some positive upside surprises. The large manufacturing index rose to 13, versus 10 forecast and 12 prior. The outlook for this segment was also better than forecast, printing at 12 (9 was forecast and 12 was the Q1 outcome). The all industry capex estimate was also stronger than expected, coming in at 11.5%, versus 10.0% forecast (3.1% was the prior outcome). For large non-manufacturing firms, the results were slightly less positive, with headline index at 34, in line with forecast, while prior was 35. The outlook printed at 27, below the expected 29 outcome (28 was recorded in Q1).

- For smaller firms, manufacturing sentiment levels remained below levels recorded for non-manufacturing firms. Both sectors saw outcomes close to forecasts, 1 for small manufacturing firms, 15 for non-manufacturing firms.

- The first chart below plots the headline large manufacturing and non-manufacturing indices versus y/y Japan GDP growth, which is the orange line on the chart. In the face of external headwinds, particularly in terms of the tariff threat, today's results point to a resilient backdrop. Both Tankan measures for large firms are just off recent highs.

- The second chart below plots the capex estimate from the Tankan survey the white line on the chart) against the capital investment, which is only out for Q1. This is pointing to a firmer capex backdrop for Q2, which again will please the authorities in the face of external headwinds.

Fig 1: Q2 Tankan Survey Results Paint Resilient Backdrop

Source: Bloomberg Finance L.P./MNI

Fig 1: Q2 Tankan Capex Estimate & Capex Y/Y

Source: Bloomberg Finance L.P./MNI

US TSYS: Cash Open

TYU5 is trading 112-02, down 0-02 from its close.

- The US 2-year yield opens around 3.72%, unchanged from its close.

- The US 10-year yield opens around 4.23%, almost unchanged from from its close.

- MNI Interview - Atlanta Federal Reserve President Raphael Bostic told an MNI Connect event Monday the potential for tariffs to create inflation pressure into next year means going slow on cutting interest rates with one this year and three in 2026, expressing a broader caution until there's clarity around U.S. fiscal policy and global conflicts.

- “Goldman said the first rate cut may come in September, sooner than it had forecast.”(BBG)

- (Bloomberg) - Treasury Secretary Scott Bessent’s indication that his department is less keen on borrowing at longer tenors opens up the door to more bill issuance. That’s a sentiment echoed by President Donald Trump in comments last week, although his notion of only issuing debt of less than nine months’ maturity is highly unlikely to happen.

- The 10-year yield has accelerated through its support, this should clear the way for a move lower with the 4.10% area the first target. 10-year yields should now find demand on any bounce back to the 4.35/40% area.

- Data/Events: S&P Global US Man PMI, Wards Total Vehicle Sale, ISM Manufacturing, Construction Spending, JOLTS, Dallas Fed Services Activity

MNI: MNI BOJ JUNE TANKAN LARGE MFG INDEX +13; MAR 12; MEDIAN 9

- MNI BOJ JUNE TANKAN LARGE MFG INDEX +13; MAR 12; MEDIAN 9

- BOJ SEPT TANKAN LARGE MFG INDEX FORECAST AT +12

- BOJ TANKAN LARGE NON-MFG INDEX +34; MAR 35; MEDIAN 34

- BOJ SEPT TANKAN LARGE NON-MFG INDEX SEEN AT 27