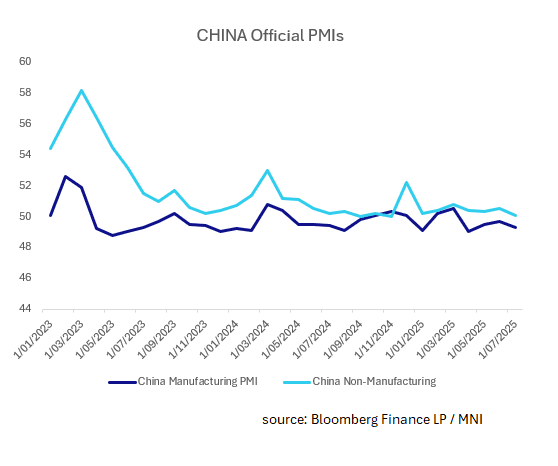

CHINA: Official PMIs Continue to Moderate

Jul-31 01:43

- China's National PMIs continued to moderate in July.

- In China, the two main Purchasing Managers' Indices (PMIs) are the National Bureau of Statistics (NBS) PMI and the S&P Global (formerly the Caixin PMI) . The NBS PMI focuses on larger, state-owned enterprises, while the Caixin PMI emphasizes smaller and privately owned businesses.

- The PMI Manufacturing moderated to 49.3 against a market estimate of 49.7 and prior of 49.7. New orders and the employment component declined from last month, driven mainly by the impact from the larger businesses.

- China' Non-manufacturing PMI was 50.1 (estimate 50.2) bringing the Composite to 50.2.

- Ongoing weakness in domestic consumption and volatility in exports is exacerbating the concerns.

- Despite this, at China’s Politburo on Wednesday, the nation’s economic strength was saluted. That came after the country registered a record trade surplus in the first half of the year on soaring shipments to southeast Asia and stabilizing exports to the US.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: BBDXY - The Move Lower Is Gaining Momentum

Jul-01 01:28

The BBDXY range overnight was 1190.00 - 1195.39, Asia is currently trading around 1188. The BBDXY again found solid supply towards the 1195.00 area overnight and then capitulated lower. This has followed through into the Asian session as the USD opens on the backfoot, -0.20%. This move seems to be gaining momentum now and rallies should now find eager sellers, first resistance is back towards 1200.

- (Bloomberg) - In a US stock market at record highs, it’s the fall of the dollar that’s telling about the diminished appeal of US assets in global portfolios.

- Luke Gromen on X: “Do not miss the forest for the trees - the political infighting is a symptom of something critical: It is dawning on policymakers their only options are crush Entitlements, crush Rates (aka deval the USD & re-accel inflation), crush Defense, &/or crush USTs relative to NGDP.”

- Andreas Steno Larsen on X: “Could Trumps push to get a new chair weaken the USD another 20%? Judging from historical comparisons from other countries it is now a feasible setup.”

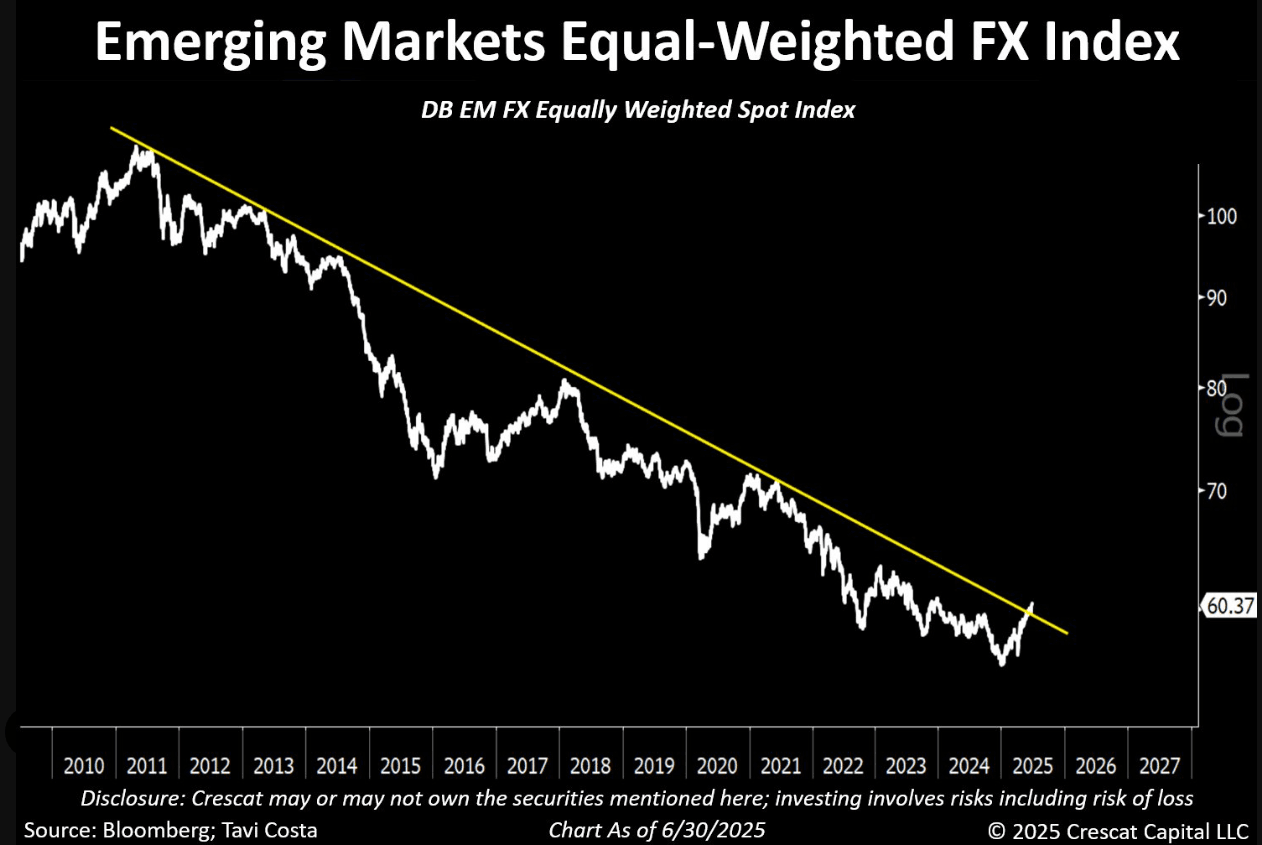

- Otavio Costa on X: “Fascinating move. You can tell a secular decline in the dollar is likely underway when emerging market currencies begin breaking key resistance levels. Dollar downturns tend to be long-lasting and broad-based, typically fueling rallies in metals, other commodities, and foreign currencies. The last time we saw this kind of shift was in the 1970s and again in the early 2000s. We have probably triggered another one of these cycles, in my view.” See Graph Below

- The BBDXY has broken convincingly now below 1200, this close could prove to be significant and points to the potential start of another leg lower, first target 1150 and then beyond.

- There is a broad consensus that the USD is set to embark on a decent move lower as the world reduces its exposure to the US and repatriates a lot of these flows.

Fig 1: EMFX Chart

Source: MNI/@TaviCosta/Bloomberg

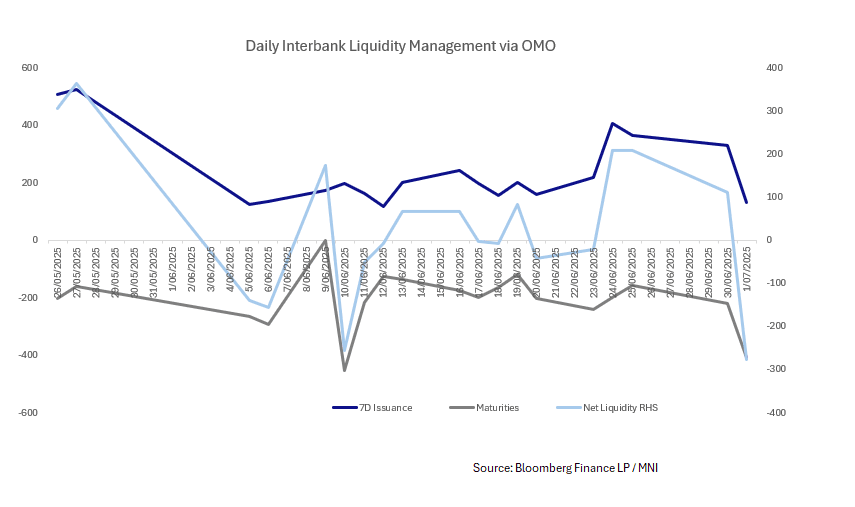

CHINA: Central Bank Withdraws CNY275.5bn via OMO

Jul-01 01:24

- The PBOC issued CNY131bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY406.5 bn

- Net liquidity injection CNY275.5 bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.41%, from prior close of 1.91%.

- The China overnight interbank repo rate is at 1.36%, from the prior close of 1.90%.

- The China 7-day interbank repo rate is at 1.60%, from the prior close of 2.30%.

JGBS: Futures Weaker After Tankan Delivers Upside Surprise

Jul-01 01:23

In Tokyo morning trade, JGB futures are weaker, -2 compared to settlement levels, after reversing the overnight session’s modest gains.

- The Q2 Tankan survey delivered some positive upside surprises. The large manufacturing index rose to 13, versus 10 forecast and 12 prior. The outlook for this segment was also better than forecast, printing at 12 (9 was forecast and 12 was the Q1 outcome). The all industry capex estimate was also stronger than expected, coming in at 11.5%, versus 10.0% forecast (3.1% was the prior outcome). For large non-manufacturing firms, the results were slightly less positive, with headline index at 34, in line with forecast, while prior was 35. The outlook printed at 27, below the expected 29 outcome (28 was recorded in Q1).

- President Donald Trump threatened to impose a fresh tariff level on Japan, citing the country's unwillingness to accept US rice exports, despite Japan's massive rice shortage. (per BBG)

- Cash US tsys are modestly richer, with a flattening bias, in today’s Asia-Pac session after yesterday’s bull-flattener.

- Cash JGBs are modestly cheaper across benchmarks. The benchmark 10-year yield is unchanged at 1.432% ahead of today’s supply

- Swap rates are flat to 1bp higher. Swap spreads are mixed.