MNI EUROPEAN MARKETS ANALYSIS: Yen Up Post BoJ

- The BoJ held rates as expected, but two board members were in favour of a hike. The central bank also outlined plans to dispose of its ETFs and J-REIT holdings. Yen has firmed, while JGB futures are down sharply.

- The USD is mostly firmer elsewhere, holding onto Thursday's gains. US Tsy yields have edged higher.

- Equity trends are mixed, with Japan markets down, but away from session lows. Oil is slightly weaker.

- Looking ahead, we have the BoJ press conference from Governor Ueda. UK and Canadian retail sales are also due.

MARKETS

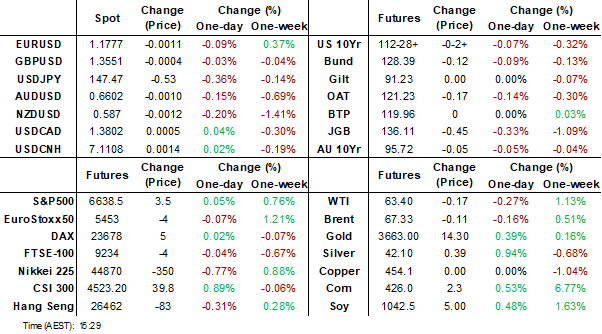

The TYZ5 range has been 112-27+ to 112-31+ during the Asia-Pacific session. It last changed hands at 112-28, down 0-03+ from the previous close.

- The US 2-year yield is trading around 3.563%.

- The US 10-year yield is trading around 4.122%, up 0.02 from its close.

- 10-Year Yields could not extend below 4.00% and have bounced as the Fed could not meet the markets very dovish expectations. The first buy-zone is now back towards the 4.15%/4.20% area where I suspect demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- Bloomberg - “Long Bonds Are a Buy as Contagion Fears Ease, TS Lombard Says. The bearish sentiment that has made global longer-maturity sovereign bonds among the worst-performing fixed-income assets this year may be about to wane, making the securities a buy.”

- Lance Roberts on X: “Goldman Sachs expected path for future rate cuts. One at every meeting this year, and two next year. But absolutely no chance of recession? - h/t @ISABELNET_SA”

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

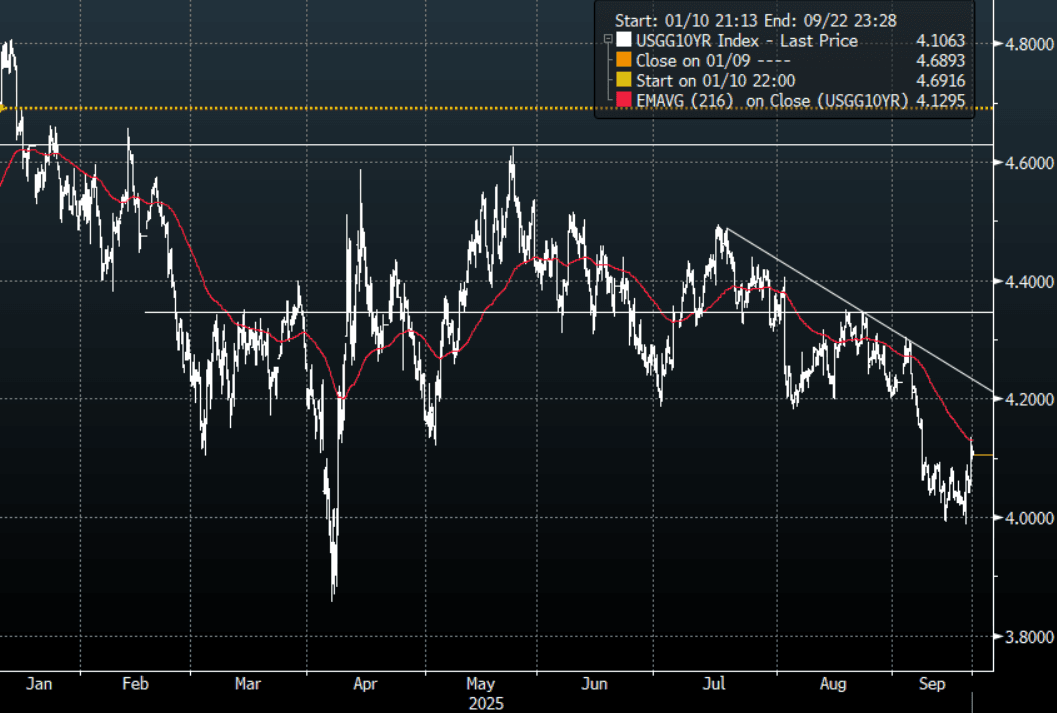

STIR: $-Bloc Little Changed Over Past Week, Except For NZ

Interest rate expectations across the $-bloc showed little net change over the past week, except in New Zealand, which was sharply lower (-19bps).

- In the US, the Fed resumed its easing cycle with the first cut of the year on September 17, of 25bp to a range of 4.00-4.25%. That decision was expected, but the lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference. Despite a lower rate path signalled in the new Dot Plot, a seeming lack of clarity on delivering those future rate cuts saw an early dovish market reaction subsequently reverse.

- The Bank of Canada also resumed easing on September 17 after a 3-meeting hold, with a 25bp rate cut to an overnight rate of 2.50%. There was limited market reaction on net to the decision and press conference, with the BOC as expected keeping the door open to further easing as soon as the next meeting in October, but falling short of any firm guidance to that effect.

- In New Zealand, both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ's August OCR path. With two votes for a 50bp cut in August, the risk of a larger move before year-end is material.

- Looking ahead, the next key regional event is the RBA’s Policy Decision on September 30, with market pricing giving a 25bp cut at this meeting a probability of 7%.

- Looking ahead to December 2025, current market-implied policy rates cumulative expected easing are as follows: US (FOMC): 3.64%, -49bps; Canada (BOC): 2.33%, -17bps; Australia (RBA): 3.30%, -30bps; and New Zealand (RBNZ): 2.40%, -60bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

BOJ: On Hold, But 2 Dissents, BoJ Outlines Plans To Sell ETF/J-REIT Holdings

As expected, the BOJ left rates on hold at 0.50%. Still, this was held by a vote of 7-2 by the board. The two dissenters were board members Takata and Tamura, who both were in favor of raising the policy rate to 0.75%.

- This was the first time we had dissent under Ueda's watch. Takata noted that the inflation target had more or less been achieved, while Tamura indicated that rates should be set closer to neutral. In this sense today's decision may be eyed as a hawkish hold, although we will wait to see what Governor Ueda says later at the press conference.

- On the economy and inflation, the language used by the BOJ didn't suggest a lot had changed around the outlook. Underlying inflation was described as stagnate due to slowing economic but expected to gradually accelerate. The growth outlook was described in a similar fashion. Capex is rising moderately, while consumption has been resilient. Inflation expectations have also risen modestly. It retains the bias to raise rates.

- The other focus point from the meeting was that the central bank will start selling its ETFS and J-REITS, (albeit once it makes the necessary operational preparations). ETFS will be sold at a pace of about ¥330bn per year (this is book value, market value is ¥620bn per BBG). J-REITS at about ¥5bn per year. They will be selling them to the market in amounts broadly equivalent to sales of stocks previously purchased from financial institutions.

- BBG noted: "The BOJ has around 70 trillion yen in ETFs (market value, not book)." So at face value it will take some take considerable time to shrink this part of its balance sheet. The BOJ did note that the future pace of sales may be modified.

- The market reaction has been hawkish, with the 2 dissenting votes a factor. USD/JPY is down around 0.50% to 147.25/30, while JGB futures are down, likewise for local stocks.

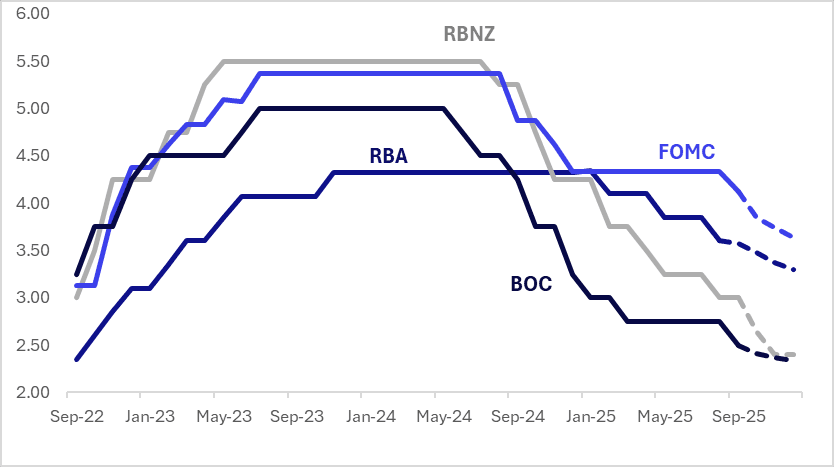

JAPAN DATA: Aug Inflation Close To Forecasts, Core- Ex Fresh Food/Energy, Sticky

Japan August national inflation was close to market forecasts. The headline rose 2.7%y/y, 2.8% was forecast (prior 3.1%). The core ex fresh food measure was up 2.7%y/y, in line with market expectations (prior was also 3.1%). The ex fresh food, energy measure was 3.3%y/y, also in line with forecast and down a touch on the 3.4% July outcome.

- In terms of the m/m outcome, headline was up 0.1%, ex fresh food was flat, while ex fresh food and energy rose 0.3%m/m. Goods prices were up 0.1%m/m while services rose 0.2%, although often the service print gets revised. In July it was originally reported that services were up 0.1%m/m, but the outcome is now back to flat.

- The main drop in the month came from the 4.2% decline in utility prices (as energy subsidies impacted). Clothing, down -0.7%m/m (the fourth straight decline) was the other soft point. Elsewhere though most categories were close to July outcomes or higher. Notably entertainment was up 1.8%m/m, after a 0.8% July gain. Fresh food rose 3.3%m/m as well, after a period of extended falls.

- In y/y terms, we didn't see strong shifts relative to July, outside of utilities dropping to -4.0%y/y (from -0.2%). Services prices were up 1.5% for the third month in a row.

- We have the BoJ meeting later today. No change is expected. Today's inflation update is unlikely to shift thinking dramatically in terms of the broader BoJ inflation outlook.

Fig 1: Japan CPI Trends Y/Y - Core Ex Fresh, Energy Still Sticky Above 3%

Source: Bloomberg Finance L.P./MNI

JAPAN DATA: Offshore Investors Sell Local Equities, Outbound Flows To Bonds

In the week ending Sep 12, Japan outbound and inbound investment flows were mixed. In terms of inbound flows we saw sharp net selling of local equities by offshore investors. This marked net outflows in this segment in 3 out of the last 4 weeks. Japan equities have performed quite strongly through Sep to date, but recall we have seen offshore investors build up a strong net inflow position into Japan stocks since April of this year. Hence last week's outflow may be reflective of some rebalancing. Offshore investors bought local bonds in decent size, more than offsetting the prior week's outflow. The cumulative sum of net flows into this segment is still close to flat in recent months though.

- In terms of Japan outbound flows, we saw good net buying of offshore bonds (marking the third straight week of flows into this segment). This fits with the on-going rise in global bond returns (led by rising US Tsys, although this trend has paused post the US FOMC).

- Outbound flows to global equities stayed positive, but were very modest.

Table 1: Japan Offshore Weekly Investment Flows

| Billion Yen | Week ending Sep 12 | Prior Week |

| Foreign Buying Japan Stocks | -2034.0 | 108.6 |

| Foreign Buying Japan Bonds | 1188.6 | -604.8 |

| Japan Buying Foreign Bonds | 1478.5 | 208.0 |

| Japan Buying Foreign Stocks | 29.7 | 891.1 |

Source: Bloomberg Finance L.P./MNI

JGBS: Market Cheaper After BoJ Policy Announcement

JGB futures are sharply weaker, -46 compared to settlement levels, after the BoJ Policy Decision.

- The BoJ kept its overnight call rate unchanged at 0.50% in a 7–2 vote, marking the first time under Governor Ueda that two board members dissented, with Takata and Tamura proposing to raise the short-term rate target to 0.75%.

- The central bank also unveiled plans to offload its ETF and J-REIT holdings, with annual sales set at roughly ¥330 billion for ETFs and ¥5 billion for J-REITs, proportionate to their share in the BoJ’s portfolio. The pace of sales may be adjusted in future meetings depending on market conditions and experience.

- In its economic assessment, the BoJ noted that Japan’s economy is recovering moderately, with exports and output flat, capital expenditure on a modest upward trend, and consumption resilient. Inflation expectations have risen moderately, though underlying inflation is expected to stagnate in the near term before gradually accelerating.

- The central bank warned that global trade policies may slow Japan’s growth temporarily, but anticipated a later re-acceleration.

- Takata argued that the price target was more or less achieved, while Tamura suggested rates should be set closer to neutral.

- Cash JGBs are cheaper after the decision, with the curve twist-flattening further. Benchmark yields are 4bps higher (5-year) to 1bp lower (40-year).

- The swap rates are 2bps higher to 1bp lower. Swap spreads are mixed.

AUSSIE BONDS: Cheaper Ahead Of Next Week's RBA Gov. Testimony & CPI Data

ACGBs (YM -5.0 & XM -6.0) are cheaper and at/near session cheaps on a data-light day.

- Cash US tsys are flat to 2bps cheaper, with a steepening bias, in today’s Asia-Pac session.

- Cash ACGBs are 5-6bps cheaper with the AU-US 10-year yield differential at +13bps.

- The bills strip bear-steepened, with pricing -2 to -6.

- MNI POLICY: RBA Sees Risk That NAIRU Slightly Lower Than 4.5%. Internal analysis of recent economic data suggests the non-accelerating inflation rate of unemployment (NAIRU) may be 10-20 basis points below the Reserve Bank of Australia's 4.5% estimate, which is based on model outputs likely distorted by the pandemic years, MNI understands. Former staffers have called on the RBA to revise its NAIRU estimate lower for some time.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in September is given a 7% probability, with a cumulative 29bps of easing priced by year-end.

- On Monday, the local calendar will see RBA Governor Bullock appearing before the House of Representatives Standing Committee on Economics. August CPI data is due on Wednesday.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 3.00% 21 November 2033 bond on Wednesday and A$900mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Post-GDP Rally Extends, Light Calendar Next Week

NZGBs closed 3-4bps richer, extending yesterday’s post-Q2 GDP rally. Benchmark yields are 7-18bps lower than pre-data levels, with the 2/10 curve steeper.

- NZGBs outperformance versus the $-bloc continued, with the NZ-US and NZ-AU 10-year yield differentials 8bps tighter on the day.

- Swap rates closed 2-4bps lower, with the 2s10s curve steeper.

- Bloomberg - "RBNZ Nowcast Estimate of New Zealand GDP Shows 3q Expansion. RBNZ updates its Kiwi-GDP nowcast estimate for 3q GDP growth, on its website. Shows GDP expanding 0.6% q/q. Gauge has picked up steadily since showing 0.2% growth in early July. NOTE: 2q nowcast estimated a 0.2% contraction, but eventual result was a 0.9% downturn."

- RBNZ dated OIS pricing closed 1-5bps softer across meetings. 33bps of easing is priced for October, with a cumulative 59bps by November 2025.

- The local calendar is empty next week apart from ANZ Consumer Confidence on Friday.

FOREX: Asia FX Wrap - How Far Can The USD Pull Back ?

The BBDXY has had a range of 1195.00 - 1197.03 in the Asia-Pac session; it is currently trading around 1195, -0.05%. The USD’s bounce extended overnight with the Fed not being able to reach the levels of dovishness the market had been pricing in. How far can this market retrace, I suspect sellers would be all over a bounce back toward the 1200/1210 area initially. A break below 1180 has been put off for now, but it feels like it's just a question of time before we have another look down there.

- EUR/USD - Asian range 1.1770 - 1.1793, Asia is currently trading 1.1775. The pair rejected the move above 1.1900 and quickly retraced. The pair will be looking for dips back towards 1.1700 to find support to build a base from which to move higher again.

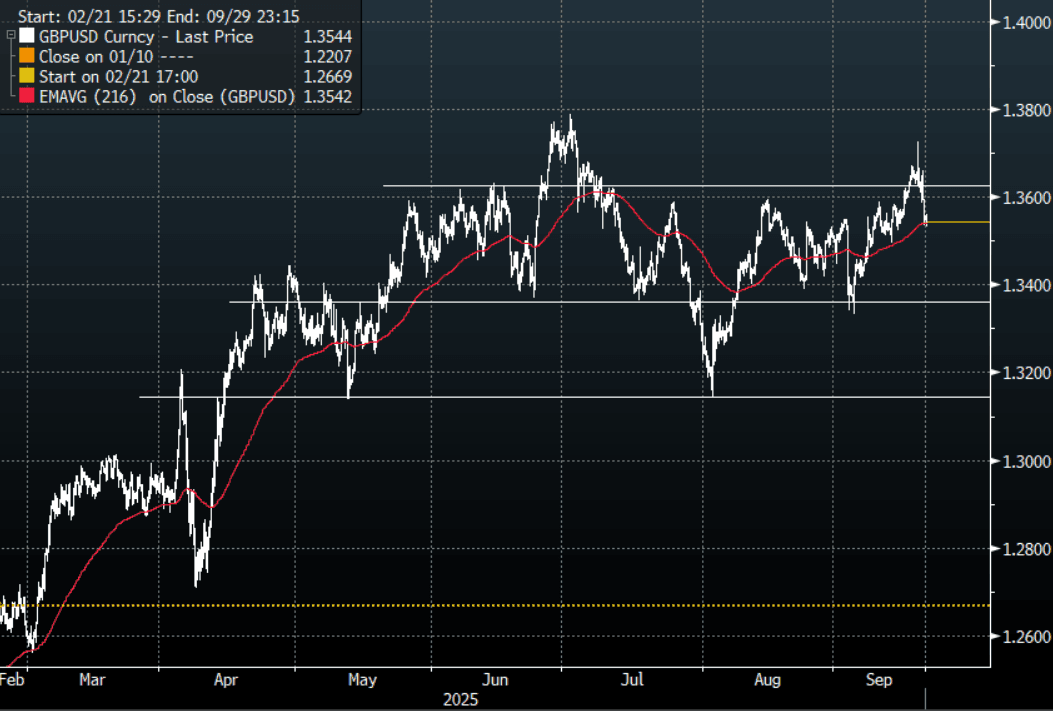

- GBP/USD - Asian range 1.3531 - 1.3559, Asia is currently dealing around 1.3545. The pair rejected the break higher and has moved back into the middle of its recent range. Dips back towards the 1.3500 area should initially find some support.

- USD/CNH - Asian range 7.1059 - 7.1157, the USD/CNY fix printed 7.1128, Asia is currently dealing around 7.1100. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.05%, Gold $3660, US 10-Year 4.12%, BBDXY 1196, Crude Oil $63.35

- Data/Events : EZ Bloomberg Sept. Eurozone Economic Survey, Italy Bloomberg Sept. Italy Economic Survey, France PPI/Business Confidence/Manufacturing Confidence, Germany Bloomberg Sept. Germany Economic Survey, Spain Bloomberg Sept. Spain Economic Survey

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

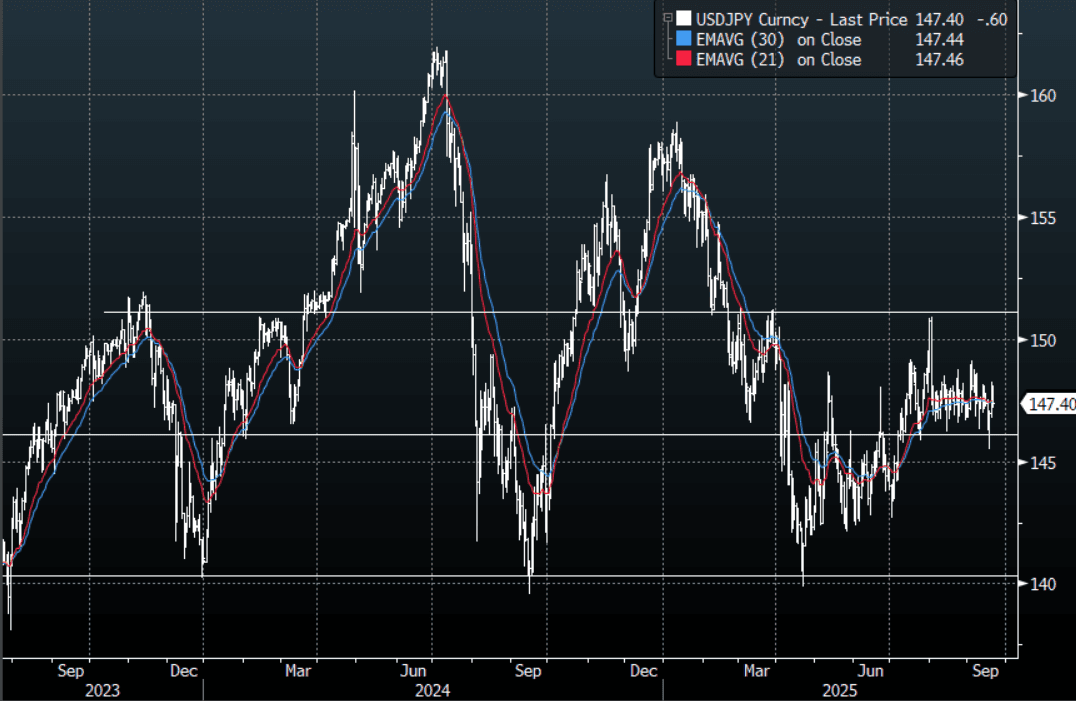

JPY: USD/JPY - Moves Lower As BOJ Has 2 Dissenters, Press Conference Next

The USD/JPY range has been 147.20 - 148.11 in the Asia-Pac session, it is currently trading around 147.40, -0.40%. USD/JPY stalled above 148.00 heading into the BOJ, 2 dissenters then saw the pair extend the move lower. The price is still in the middle of its recent 146-149 range, and we need a convincing break on either side to see some clearer direction again. The USD/JPY bears will be hoping that Governor Ueda provides a clearer path of when rate hikes could potentially begin, based on past performance I wouldn't be holding my breath.

- Bloomberg - Language of dissenters: “Takata Hajime considered that there had been a shift away from the deflationary norm and the price stability target had been more or less achieved. Tamura Naoki considered that, with risks to prices becoming more skewed to the upside, the Bank should set the policy interest rate a little closer to the neutral rate. They proposed that the Bank set the guideline for money market operations as follows: the Bank would encourage the uncollateralized overnight call rate to remain at around 0.75 percent.”

- MNI BRIEF: Japan Aug Core CPI Rises 2.7% Vs. July 3.1%. Japan’s annual core consumer inflation slowed to 2.7% y/y in August from 3.1% in July, the Ministry of Internal Affairs and Communications said Friday, as lower energy and food prices excluding perishables weighed on the index. The reading stayed above the Bank of Japan’s 2% target for the 41st straight month but fell below 3% for the first time since November 2024.

- "JAPAN RULING PARTY LAWMAKER TAKAICHI TO PROPOSE INCOME TAX CUT AND CASH PAYOUT TO HOUSEHOLDS, IN CAMPAIGN PLEDGE FOR RULING PARTY LEADERSHIP RACE, TAKAICHI TO CALL FOR GRADUALLY LOWERING RATIO OF GOVT DEBT TO GDP IN CAMPAIGN PLEDGE -NIKKEI" RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($600m), 146.00($820m), 148.00($539m). Upcoming Close Strikes : 145.00($1.92b Sept 19), 146.40($897m Sept 19) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

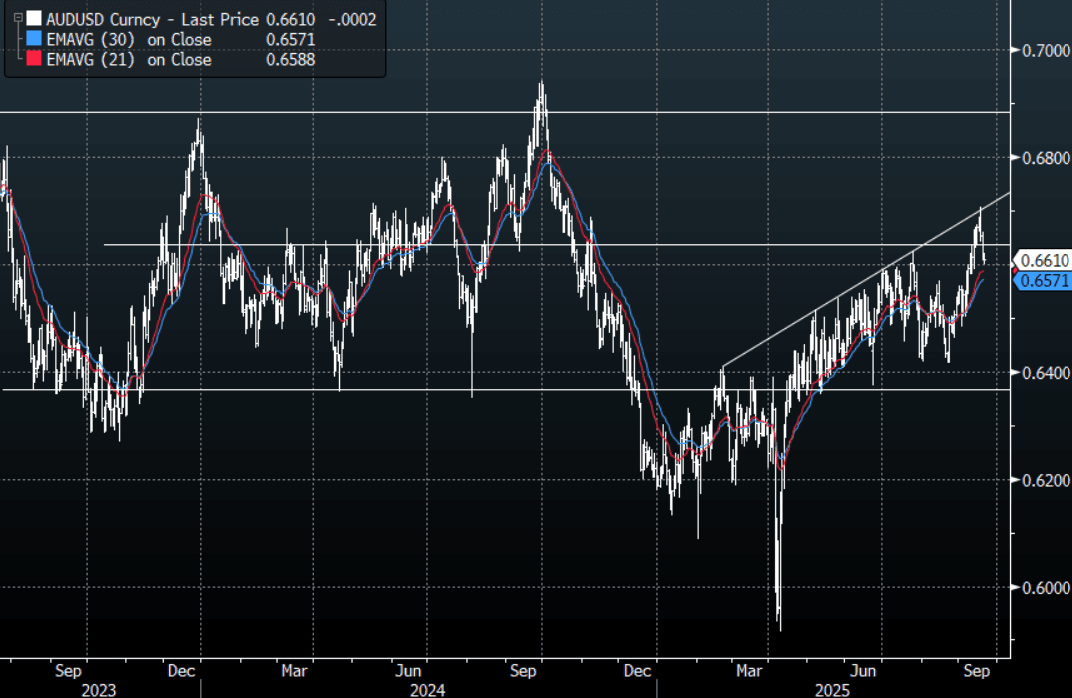

AUD/USD - Consolidates Above 0.6600

The AUD/USD has had a range of 0.6600 - 0.6620 in the Asia- Pac session, it is currently trading around 0.6610, -0.02%. US stocks, just another day and another all-time high, nothing stops this train. The USD retracement extended overnight, though time will tell how long the reprieve lasts. The AUD/USD should still see dips supported for now with the first buy-zone back towards the 0.6550 area.

- Bloomberg - “‘Hedge America’ Trade Fuels Global Rush Into Short-Dollar Wagers. Global investors are buying US stocks and bonds while also buying derivatives to protect those investments against declines in the dollar. The hedging activity is expected to weigh on the dollar, with some banks anticipating it will struggle to rebound from its slide, and estimates suggesting the wave of fresh dollar hedging could ultimately tally about $1 trillion.”

- MNI POLICY: RBA Sees Risk That NAIRU Slightly Lower Than 4.5%. Internal analysis of recent economic data suggests the non-accelerating inflation rate of unemployment (NAIRU) may be 10-20 basis points below the Reserve Bank of Australia’s 4.5% estimate, which is based on model outputs likely distorted by the pandemic years, MNI understands. Former staffers have called on the RBA to revise its NAIRU estimate lower for some time.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD857m), 0.6750(AUD1.17b). Upcoming Close Strikes : 0.6525(AUD705m Sept 22), 0.6650(AUD906m Sept 23), 0.6720(AUD791m Sept 24) - BBG

- AUD/JPY - Asia-Pac range 97.32 - 97.97, Asia is trading around 97.40.The pair has stalled towards 98.50, dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

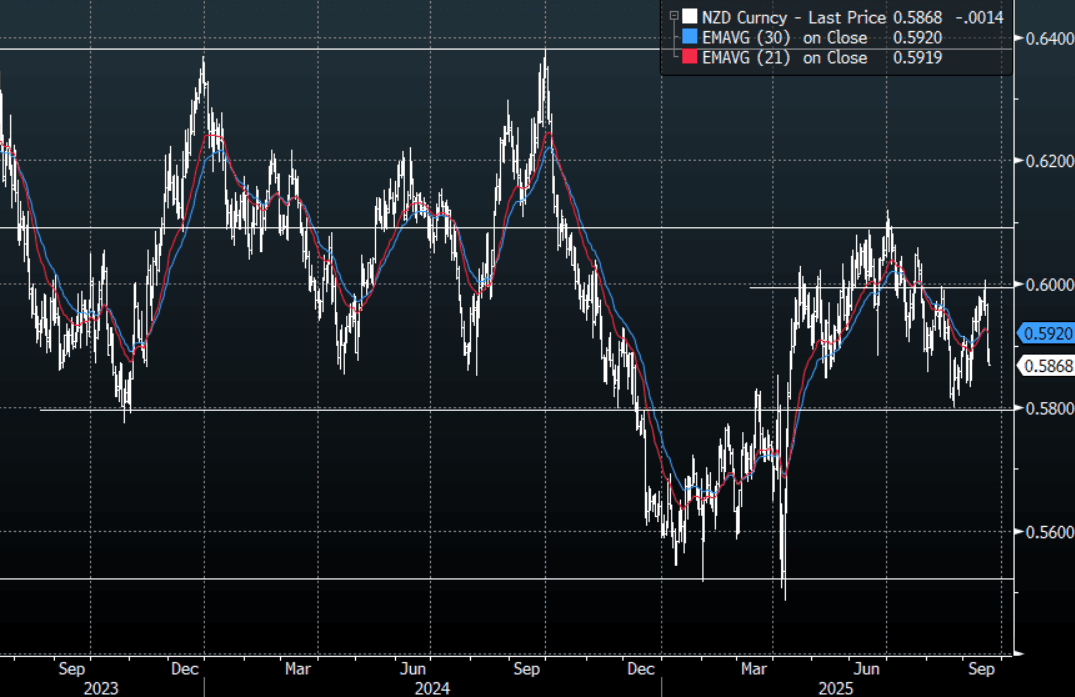

NZD: Asia Wrap - NZD/USD Trades Heavy Below 0.5900

The NZD/USD had a range of 0.5868 - 0.5892 in the Asia-Pac session, going into the London open trading around 0.5870, -0.22%. US stocks, just another day and another all-time high, nothing stops this train. The USD retracement extended, though time will tell how long the reprieve lasts. The NZD underperformance got a real nudge from the poor GDP data. While the USD continues to pullback the NZD/USD is a great vehicle to express that but when the USD sellers return the NZD underperformance will once again be best expressed in the crosses. The 0.5800 is important support, a sustained break through there would turn the focus back towards the 0.5500 lows.

- Bloomberg - “RBNZ Nowcast Estimate of New Zealand GDP Shows 3q Expansion. RBNZ updates its Kiwi-GDP nowcast estimate for 3q GDP growth, on its website. Shows GDP expanding 0.6% q/q. Gauge has picked up steadily since showing 0.2% growth in early July. NOTE: 2q nowcast estimated a 0.2% contraction, but eventual result was a 0.9% downturn.”

- “NZ Aug. Trade Deficit Widens to NZ$1.185b. New Zealand's trade deficit widened to NZ$1.185b in August from revised -NZ$716m in July, according to Statistics New Zealand. Exports fell to NZ$5.94b from revised NZ$6.56b in July. Imports fell to NZ$7.12b from revised NZ$7.27b in July.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6020(NZD 374m Sept 22), 0.5900(NZD372m Sept24) - BBG

- AUD/NZD range for the session has been 1.1230 - 1.1249, currently trading 1.1240. The Cross has broken above the multiple highs towards the 1.1200 area and is looking to accelerate higher on the back of some very poor Q2 GDP data. Dips should now continue to be supported as the market turns its focus towards the 1.1400/1.1500 area.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Stocks Down Post Hawkish BoJ Hold, Mixed Trends Elsewhere

The main focus as Friday's Asia Pac session has unfolded has been Japan equity market weakness. This follows the BoJ hawkish hold earlier. We had rates held steady at 0.50%, but two board members voted in favor of rates moving up by 25bps. This, along with BoJ outlining plans for disposing of its ETF and J-REIT holdings, have been a clear negative for Japan stocks (USD/JPY is also down, potentially weighing on exporter related stocks).

- At the time of writing, the NKY 225 was off close to 1.2% (away from session lows). The Topix was down around 0.70%. The central bank will start selling its ETFS and J-REITS holdings, (albeit once it makes the necessary operational preparations). ETFS will be sold at a pace of about 330bn per year. J-REITS at about 5bn per year. They will be selling them to the market in amounts broadly equivalent to sales of stocks previously purchased from financial institutions. BBG noted: "The BOJ has around 70 trillion yen in ETFs (market value, not book)." So at face value it will take considerable time to shrink this part of its balance sheet. The BOJ did note that the future pace of sales may be modified.

- Bank stocks were one of the few bright spots, likely in response to higher JGB yields (BoJ hike odds are higher for Oct), the Topix bank index up around 0.55%.

- Elsewhere, Hong Kong's HSI is up at touch, while the CSI 300 is up 0.33%, but the Shanghai Composite is around flat in terms of mainland trends.

- The Kospi and Taiex are both down, although losses are less than 1% at this stage. This is despite surge in the US SOX index in Thursdays trade. Both markets are still close to fresh cycle highs though.

- In Australia, the stock market index is up 0.70%, aided by bank shares and health care stocks.

- In South East Asia, trends are mixed - Malaysia, Thailand and Indonesia are little changed, while the Philippines are up 0.60%.

ASIA STOCKS: Tech Related Inflows Rebound, Thailand Sees Outflows

Inflow momentum turned positive once again for South Korean and Taiwan markets yesterday. Taiwan was the best performer, as its onshore equity market closed at a fresh record high (up +1.30%). Tech/AI sentiment remains buoyant, with the SOX index up a further 3.60% in Thursday US trade. Via BBG: "Information technology was the best-performing sector, with Intel notching its best day since 1987 as Nvidia announced a $5 billion investment and said the two will co-develop chips for PCs and data centers." Positive spill over to Taiwan stocks today may aid further inflow momentum. Sep to date inflows are now at +$8.7bn, which is a fresh cycle high.

- For South Korea, such trends should also aid the inflow backdrop, although it can have a lower beta compared to Taiwan with respect to such moves.

- Elsewhere, India saw modest outflows on Wednesday, leaving the 5-day sum of net inflows in negative territory.

- Yesterday saw notable outflows from Thailand. At just over $100mn this was the largest net outflow day since end of August. The local equity index fell yesterday, the SET back under 1300. The new government is looking to step up efforts to curb FX outperformance and it is mindful around further portfolio inflow risks (from an FX standpoint).

- Indonesia saw modest outflows, while the 5-day sum was close to flat.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 244 | 2556 | -907 |

| Taiwan (USDmn) | 473 | 2347 | 8841 |

| India (USDmn)* | -32 | -154 | -15292 |

| Indonesia (USDmn) | -22 | 8 | -3718 |

| Thailand (USDmn) | -101 | -83 | -2611 |

| Malaysia (USDmn) | -15 | 124 | -3669 |

| Philippines (USDmn) | -1 | 7 | -725 |

| Total (USDmn) | 547 | 4806 | -18080 |

| * Data Up To Sep 17 |

Source: Bloomberg Finance L.P./MNI

OIL: Benchmarks Edging Lower, But Still Up For The Week

Oil benchmarks are down a touch in the first part of Friday dealings. We were last just under $67.35/bbl for Brent, while WTI was close to $63.35/bbl. Moves lower at this stage are not beyond 0.20%, but continue the downside momentum seen in recent sessions. Both benchmarks are still up for the week though, for WTI are are still +1.2% higher, while Brent is +0.55% firmer.

- Focus remains on US President Trump's calls for nations to stop buying Russian oil to help end the conflict in Ukraine. Via BBG: "Trump said the conflict would end “if the price of oil comes down,” and repeated calls for countries to stop buying fuel from the OPEC+ member." Ukraine strikes on Russian energy infrastructure is the other focus point.

- On the EU side, it is considering the phasing out of all Russian LNG imports earlier than the end of 2027, which was the EU’s initial plan. Its focus is turning to Russian LNG, given that many EU countries are reluctant to hit India and China with tariffs for purchases of Russian oil.

- Meanwhile, the market is weighing the pledged rise in OPEC+ output against the bloc’s spare capacity to follow through on production hikes, coupled with Chinese storage buying.

- The trend condition in WTI futures is still bearish, with initial support at $61.29, the Aug 13 low and the bear trigger, followed by $57.71, the May 30 low. Initial resistance to watch is $66.03, the Sep 2 high.

PRECIOUS METALS: Gold - Price Action Shows Momentum Stalling

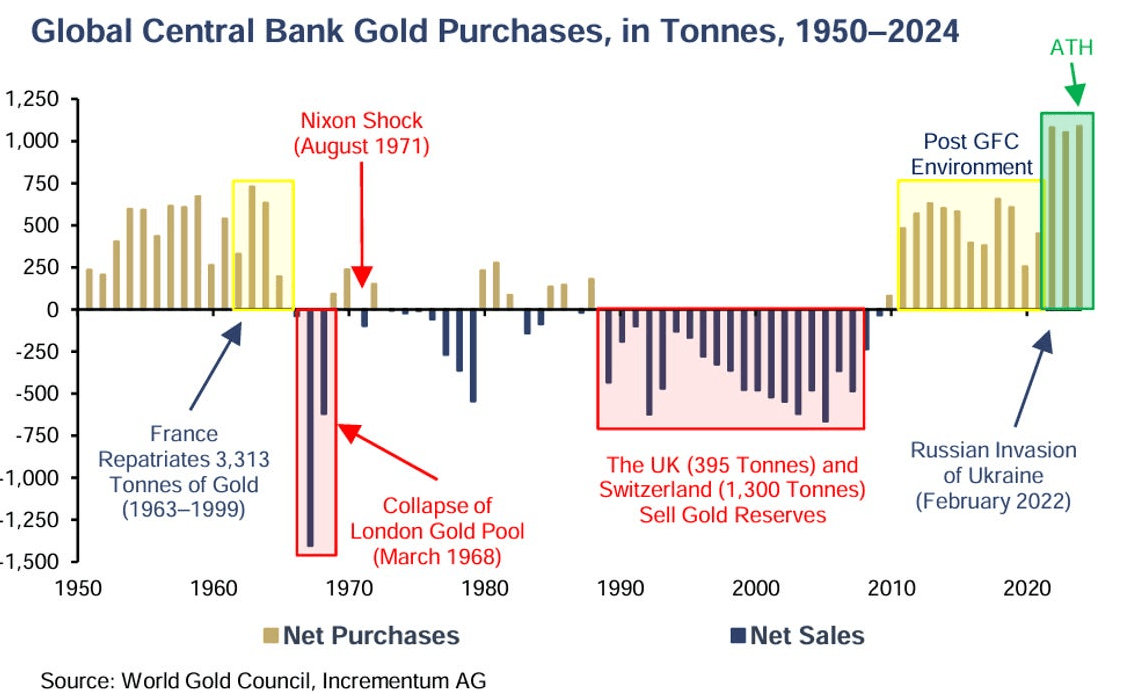

The range overnight for gold was $3,628.07 - $3,673.06, Asia is currently trading around 3645.00, +0.05%. Gold has drifted lower for a third day after stalling around $3,700/oz. The market is having to recalibrate its dovishness after the FOMC, this and a reprieve for the USD are both contributing to the exhaustive price action. After such a powerful move higher after breaking the $3450/3500 area a retracement could actually be healthy, I suspect buyers will be around on dips back towards the $3500/$3550/oz area initially.

- The Market NZZ - “Central banks are likely to continue buying gold to diversify their dollar reserves. Since the US capital market is unmatched in breadth and depth, and no other currency can match it, gold is increasingly being chosen. This shift began with the freezing of Russian foreign exchange reserves in 2022. Since then, emerging market central banks in particular have acquired more than 1,000 tons of gold annually, a new record (see green box in the chart).”

- Real Vision on X: "Gold is no longer following the old rules — liquidity is now in control. Since 2022, financial conditions—not real rates—have become the key driver of gold’s price action.”

- Augur Infinity on X: “The YTD performance of gold is the best since 1979.”

Fig 1 : Central Bank Gold Purchases

Source: MNI - Market News/The Market NZZ/World Gold Council

ASIA FX: Stronger Yen Doesn't Aid Region, IDR & THB Down For The Week

The bias around USD/Asia pairs is higher in the first part of Friday dealings. The firmer US yield backdrop from Thursday, most notably with the 10yr real yield moving back up to 1.73%, is supporting broader dollar sentiment. Regional equity sentiment is mixed, with aggregate shifts less than 1% at this stage. We did see some USD/Asia pairs pull back in line with USD/JPY (post the hawkish BoJ hold), but follow through has been limited.

- USD/CNH was last around 7.1100, against earlier highs of 7.1157. Focus is on the upcoming phone call between US President Trump and China President XI (scheduled for 9am ET US). It's expected to center around the future of Tiktok but the market will also be eyeing for any broader trade related sentiment that emerges from the call. Both onshore and offshore yuan spot sit up modestly for the week.

- USD/KRW is back at 1395 in latest dealings, up around 0.50% from end Thursday levels. This is quite the rebound given we got to 1375.65 on Wednesday. The pair hasn't been above 1400 so far in Sep. Dovish rhetoric from the BoK coupled with the US yield rebound have been won headwinds. For the week though we are little changed.

- TWD has done better than KRW amid the firmer global tech equity tone (which has helped keep inflows into local stocks firm). Spot USD/TWD was last near 30.135, still near week to date lows just under 30.00. TWD is up close to 0.30% so far this week, the best performer in EM Asia FX. As expected the CBC held steady on Thursday.

- THB sits off around 0.50% so far this week, the second worst performer in EM Asia FX (with IDR the worse). USD/THB was last around 31.85/90, just short of week to date highs (31.965). A short while ago a series of headlines crossed. The BoT noted it had acted on the baht and would continue to monitor it closely (looking to avoid excessive moves). It added that the baht was stronger than what was implied by underlying fundamentals but that it hadn't seen any unusual speculation (per RTRS). The central bank also reiterated that the baht had been discussed with the Thailand FinMin.

- USD/IDR is up close to 1.2% so far this week, as the pair consolidates its break above 16500, which puts us to fresh highs back to May of this year. BI's surprise rate cut shows a clear shift to drive growth, with financial stability now seemingly less important. The pair was last at 16565.

- Other pairs have seen little change over the past week, USD/PHP is holding above 57.00, but within recent ranges. USD/MYR is back above 4.2000, unable to sustain the recent break lower.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 19/09/2025 | 0600/0700 | *** | Public Sector Finances | |

| 19/09/2025 | 0600/0700 | *** | Retail Sales | |

| 19/09/2025 | 0600/0800 | ** | PPI | |

| 19/09/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1830/1430 | San Francisco Fed's Mary Daly |