ASIA STOCKS: Japan Stocks Down Post Hawkish BoJ Hold, Mixed Trends Elsewhere

The main focus as Friday's Asia Pac session has unfolded has been Japan equity market weakness. This follows the BoJ hawkish hold earlier. We had rates held steady at 0.50%, but two board members voted in favor of rates moving up by 25bps. This, along with BoJ outlining plans for disposing of its ETF and J-REIT holdings, have been a clear negative for Japan stocks (USD/JPY is also down, potentially weighing on exporter related stocks).

- At the time of writing, the NKY 225 was off close to 1.2% (away from session lows). The Topix was down around 0.70%. The central bank will start selling its ETFS and J-REITS holdings, (albeit once it makes the necessary operational preparations). ETFS will be sold at a pace of about 330bn per year. J-REITS at about 5bn per year. They will be selling them to the market in amounts broadly equivalent to sales of stocks previously purchased from financial institutions. BBG noted: "The BOJ has around 70 trillion yen in ETFs (market value, not book)." So at face value it will take considerable time to shrink this part of its balance sheet. The BOJ did note that the future pace of sales may be modified.

- Bank stocks were one of the few bright spots, likely in response to higher JGB yields (BoJ hike odds are higher for Oct), the Topix bank index up around 0.55%.

- Elsewhere, Hong Kong's HSI is up at touch, while the CSI 300 is up 0.33%, but the Shanghai Composite is around flat in terms of mainland trends.

- The Kospi and Taiex are both down, although losses are less than 1% at this stage. This is despite surge in the US SOX index in Thursdays trade. Both markets are still close to fresh cycle highs though.

- In Australia, the stock market index is up 0.70%, aided by bank shares and health care stocks.

- In South East Asia, trends are mixed - Malaysia, Thailand and Indonesia are little changed, while the Philippines are up 0.60%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Mostly Cheaper With A Steeper Curve

JGB futures are little changed, -3 compared to settlement levels.

- Japan Export Growth Negative, Lagging Other Parts Of Asia : Japan July export and import outcomes were fairly close to market expectations, but the trade balances were slightly weaker. Exports fell -2.6%y/y (-2.1% forecast and -0.5% prior), while imports were -7.5%y/y, (-10.0% forecast and 0.3% prior). The trade deficit was -117.5bn, against a 198.5bn forecast.

- Japan Core Machine Orders Above Forecasts, Suggesting Resilient Capex : Japan June core machine orders were better than forecast. We rose 3.0%m/m, versus -0.5% forecast and -0.6% prior. The y/y print was 7.6%, against a 4.7% forecast and 4.4% prior. Today's machine orders print continues to paint a resilient capex picture for Japan's economy.

- US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 0.5bp lower (7-year) to 3bps higher (40-year). The benchmark 10-year yield is 0.4bp higher at 1.606% versus the cycle high of 1.616%.

- Swap rates are flat to 1-2bps higher, with a steepening bias.

- Tomorrow, the local calendar will see Weekly International Investment Flows, S&P Global PMIs (P) and Machine Tool Orders alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

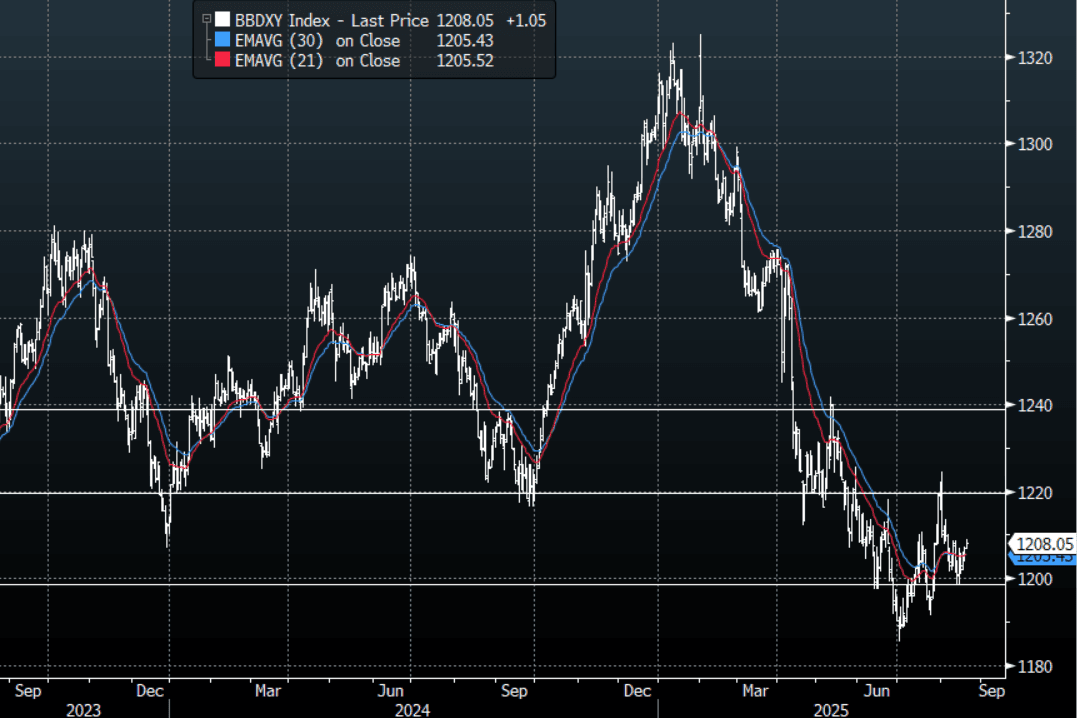

FOREX: Asia FX Wrap - The USD Bid Remains Steady Heading Into Jackson Hole

The BBDXY has had a range of 1206.79 - 1208.95 in the Asia-Pac session, it is currently trading around 1208, +0.10%. The USD continues to see profit-taking as the market pares back some risk as we head into Jackson Hole at the end of the week. Depending on the contents of Powell's speech this could change very quickly but the BBDXY looks to be putting in a third higher low which would be a worrying sign to the bears that we could be putting in a short-term base. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows, but risk is more likely skewed to the USD shorts continuing to be reduced into Powell's speech.

- EUR/USD - Asian range 1.1622 - 1.1651, Asia is currently trading 1.1635. The market is trading sideways in a 1.1600-1.1750 range heading into Jackson Hole. The pair is unlikely to extend too far as the market awaits Powell's speech.

- GBP/USD - Asian range 1.3462 - 1.3493, Asia is currently dealing around 1.3475. Having broken back above its pivot look for dips to again be supported, with risk retracing the pair is probing its first support seen towards 1.3400.

- USD/CNH - Asian range 7.1868-7.1931, the USD/CNY fix printed 7.1384, Asia is currently dealing around 7.1890. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.30%, Gold $3320, US 10-Year 4.31%, BBDXY 1208, Crude Oil $62.41

- Data/Events : EZ CPI, Germany PPI

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Holding Richer After RBNZ's Forward Guidance

ACGBs (YM +4.5 & XM +3.5) are richer but off session bests.

- The local market has benefited from positive spillover from a strong post-RBNZ rally in NZGBs.

- The RBNZ cut the OCR by 25bps to 3.0%, as expected (4-2 vote; some favoured a 50bp cut), with forward guidance that saw the OCR averaging 2.71% in 4Q 2025, 2.56% in 2Q 2026, and 2.59% in 3Q 2026 (down from May's trough forecast of 2.9%). It indicated scope for further rate cuts if inflation pressures ease; forecasts imply a good chance of two more 25bp cuts.

- Cash US tsys are little changed in today's Asia-Pac session after modest gains.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at -2bps.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in September is given a 30probability, with a cumulative 37bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will see S&P Global PMIs (P) and Consumer Inflation Expectation data.

- The AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Friday.