OIL: Benchmarks Edging Lower, But Still Up For The Week

Oil benchmarks are down a touch in the first part of Friday dealings. We were last just under $67.35/bbl for Brent, while WTI was close to $63.35/bbl. Moves lower at this stage are not beyond 0.20%, but continue the downside momentum seen in recent sessions. Both benchmarks are still up for the week though, for WTI are are still +1.2% higher, while Brent is +0.55% firmer.

- Focus remains on US President Trump's calls for nations to stop buying Russian oil to help end the conflict in Ukraine. Via BBG: "Trump said the conflict would end “if the price of oil comes down,” and repeated calls for countries to stop buying fuel from the OPEC+ member." Ukraine strikes on Russian energy infrastructure is the other focus point.

- On the EU side, it is considering the phasing out of all Russian LNG imports earlier than the end of 2027, which was the EU’s initial plan. Its focus is turning to Russian LNG, given that many EU countries are reluctant to hit India and China with tariffs for purchases of Russian oil.

- Meanwhile, the market is weighing the pledged rise in OPEC+ output against the bloc’s spare capacity to follow through on production hikes, coupled with Chinese storage buying.

- The trend condition in WTI futures is still bearish, with initial support at $61.29, the Aug 13 low and the bear trigger, followed by $57.71, the May 30 low. Initial resistance to watch is $66.03, the Sep 2 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBNZ: MPC Speakers Coming Up

The RBNZ 25bp rate cut 25bp today was accompanied by updated staff forecasts and a press conference held by acting Governor Hawkesby. There will be further appearances by MPC members following this decision.

- August 20: Governor Hawkesby gives interview on Newstalk ZB at 1700 NZST.

- August 21: Governor Hawkesby is interviewed on Radio NZ at 0600 NZST, Newstalk ZB at 0730 and CNBC TV at 1130.

- August 22: Forecasting Manager Williams speaks at the SIFA conference at 1345 on the August policy statement.

- August 29: Chief economist Conway speaks to the Macro Group at 1230.

- September 5: Chief economist Conway moderates a panel on monetary-fiscal interaction in policymaking at the RBA annual research conference.

- September 10: Chief economist Conway speaks at Auckland Chamber of Commerce lunch 1230-1400.

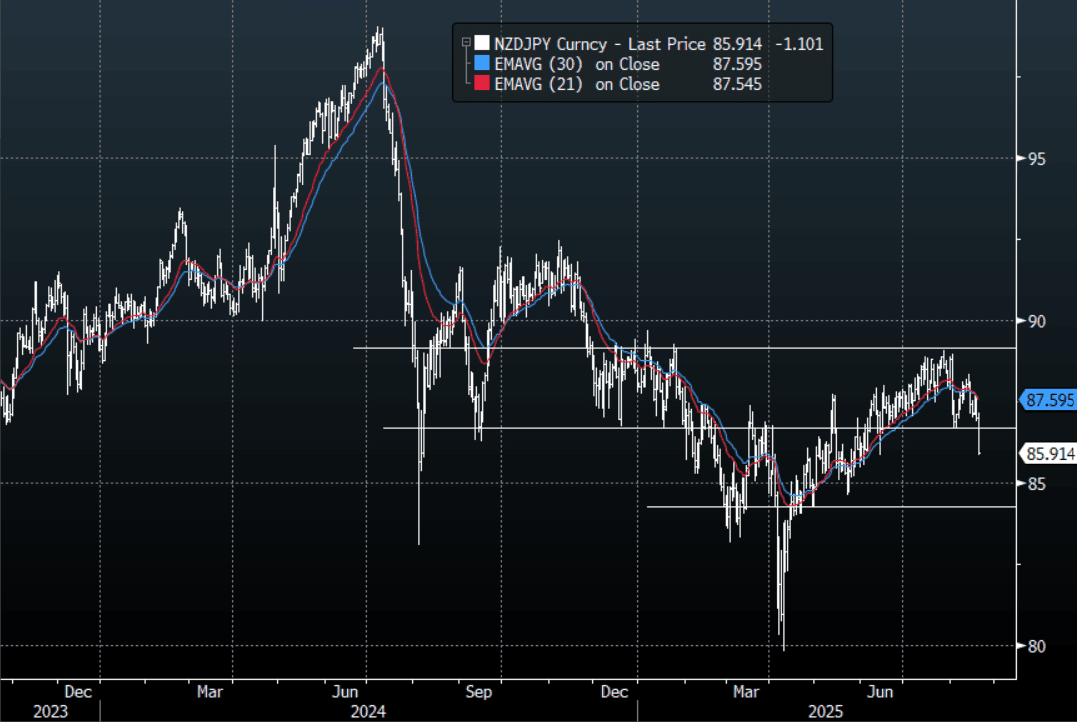

FOREX: Yen Crosses - Turn Lower With Risk, NZD/JPY Breaks Lower On Dovish RBNZ

US equities saw some profit-taking heading into Jackson Hole led by big Tech, this saw risk sensitive pairs like the JPY crosses trade heavy. This morning US futures have extended their move lower, ESU5 -0.30%, NQU5 -0.45%. The JPY crosses momentum higher looks to have stalled for now and should risk continue to correct this could see these crosses turn with it. NZD/JPY was given an extra nudge with the help of a dovish RBNZ.

- EUR/JPY - Overnight range 171.70 - 172.70, Asia is trading around 171.60. This pair’s move higher looks to have stalled for now as risk seems to be correcting lower. The risk is a move back to 170.00 which for the bulls needs to hold.

- GBP/JPY - Overnight 198.83 - 199.86, Asia trades around 198.80. This pair has again failed to break back above 200.00. With risk being pared back into Jackson Hole the JPY crosses have all slipped lower. First support back towards the 197.50 pivot within the wider 195-200 range.

- NZD/JPY - Overnight range 86.90 - 87.59, Asia is currently dealing 85.90. The pair has broken through its support around 86.50 on the back of a dovish RBNZ. This a powerful move lower and if sustained should now see bounces met with supply, especially if risk continues to retrace.

- CNH/JPY - Overnight range 20.5149 - 20.5820, Asia is currently trading around 20.5100. This pair has drifted lower but still above its pivotal 20.30/20.40 support. A sustained break back below 2.3000 is needed to turn momentum lower again, until then it looks comfortable in a 20.4000-20.8000 range.

Fig 1 : NZD/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBNZ: OCR Path “Signals” Further Easing

The pace of NZ’s economic recovery appears to have disappointed the MPC with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2 with two members voting for a 50bp reduction. The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signalling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- The revised OCR path implies another 43bp of easing by year end with 16bp in Q1 2026. This suggests that the last two meetings of 2025 on October 8 and November 26 are both “live” with around an even possibility of another one in February 2026. However, the MPC was clear that it remains highly data dependent.

- Headline inflation was revised higher over H2 2025 and H1 2026 and is forecast at 2.2% in Q4 2026 with it not returning to the 2% mid-point of the target band until H1 2027. It is now expected to be at the top of the band in Q3 2025.

- Rates were cut by 25bp as upside and downside risks were seen as “broadly balanced”, financial conditions continue to ease due to previous cuts and the OCR would signal the MPC’s easing bias.

- The case for a 50bp cut included “declining inflationary pressure and significant spare capacity”, global uncertainty could have “self-reinforcing” effects on domestic demand, a larger cut would send a clearer signal and excess capacity would put downward pressure on inflation.

- Arguments to hold rates were discussed which included global uncertainty had eased since May, the full effect of previous easing was yet to be felt, July data “suggest some improvements” and inflation is close to the top of the band and near-term expectations are rising. One member supported this view.