PRECIOUS METALS: Gold - Price Action Shows Momentum Stalling

The range overnight for gold was $3,628.07 - $3,673.06, Asia is currently trading around 3645.00, +0.05%. Gold has drifted lower for a third day after stalling around $3,700/oz. The market is having to recalibrate its dovishness after the FOMC, this and a reprieve for the USD are both contributing to the exhaustive price action. After such a powerful move higher after breaking the $3450/3500 area a retracement could actually be healthy, I suspect buyers will be around on dips back towards the $3500/$3550/oz area initially.

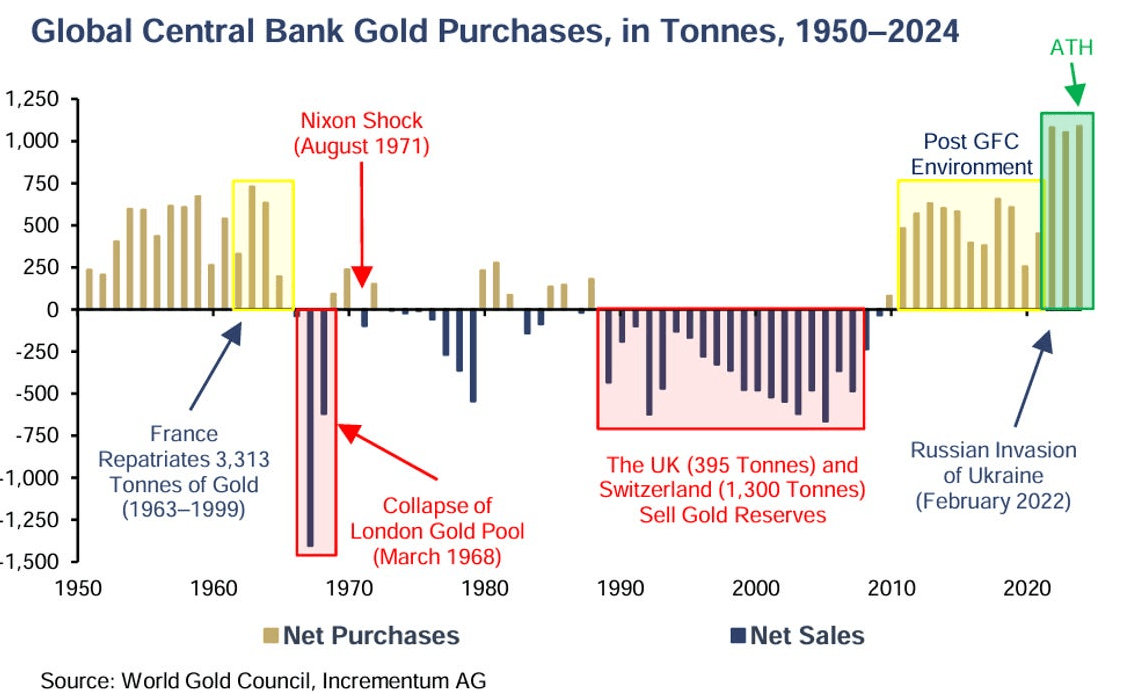

- The Market NZZ - “Central banks are likely to continue buying gold to diversify their dollar reserves. Since the US capital market is unmatched in breadth and depth, and no other currency can match it, gold is increasingly being chosen. This shift began with the freezing of Russian foreign exchange reserves in 2022. Since then, emerging market central banks in particular have acquired more than 1,000 tons of gold annually, a new record (see green box in the chart).”

- Real Vision on X: "Gold is no longer following the old rules — liquidity is now in control. Since 2022, financial conditions—not real rates—have become the key driver of gold’s price action.”

- Augur Infinity on X: “The YTD performance of gold is the best since 1979.”

Fig 1 : Central Bank Gold Purchases

Source: MNI - Market News/The Market NZZ/World Gold Council

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBNZ: OCR Path “Signals” Further Easing

The pace of NZ’s economic recovery appears to have disappointed the MPC with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2 with two members voting for a 50bp reduction. The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signalling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- The revised OCR path implies another 43bp of easing by year end with 16bp in Q1 2026. This suggests that the last two meetings of 2025 on October 8 and November 26 are both “live” with around an even possibility of another one in February 2026. However, the MPC was clear that it remains highly data dependent.

- Headline inflation was revised higher over H2 2025 and H1 2026 and is forecast at 2.2% in Q4 2026 with it not returning to the 2% mid-point of the target band until H1 2027. It is now expected to be at the top of the band in Q3 2025.

- Rates were cut by 25bp as upside and downside risks were seen as “broadly balanced”, financial conditions continue to ease due to previous cuts and the OCR would signal the MPC’s easing bias.

- The case for a 50bp cut included “declining inflationary pressure and significant spare capacity”, global uncertainty could have “self-reinforcing” effects on domestic demand, a larger cut would send a clearer signal and excess capacity would put downward pressure on inflation.

- Arguments to hold rates were discussed which included global uncertainty had eased since May, the full effect of previous easing was yet to be felt, July data “suggest some improvements” and inflation is close to the top of the band and near-term expectations are rising. One member supported this view.

BONDS: NZGBs: Gap Richer After RBNZ Gives Dovish Guidance

NZGBs gap 9-12bps richer after the RBNZ cut the OCR by 25bps to 3.0%, as expected (4–2 vote; some favoured a 50bp cut).

- Forward guidance sees the OCR averaging 2.71% in 4Q 2025, 2.56% in 2Q 2026, and 2.59% in 3Q 2026 (down from May’s trough forecast of 2.9%). Indicates scope for further rate cuts if inflation pressures ease; forecasts imply a good chance of two more 25bp cuts.

- GDP seen contracting 0.3% q/q in 2Q 2025 but growing 0.3% q/q in 3Q 2025. Risks to the outlook remain both to the upside and downside.

- Bottom line: RBNZ delivered a widely expected rate cut to 3%, signalled a lower future OCR path, and left the door open for further easing if inflation moderates. Markets responded with a weaker NZD and higher local equities.

- Swap rates are 9-12bps lower after the decision.

- RBNZ dated OIS pricing has shunted softer for meetings beyond August. Pricing is 14-18bps softer out to July 2026. 31bps of cumulative easing is priced by November 2025.

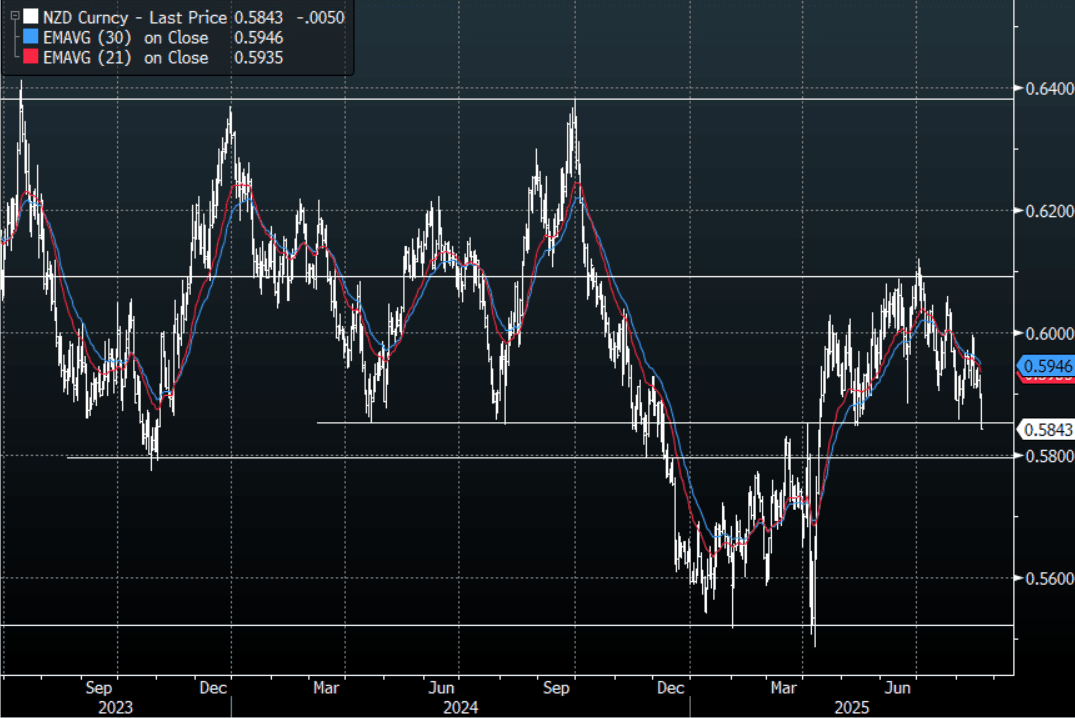

NZD: NZD/USD - Probing Pivotal Support After The RBNZ

With policy makers signaling there is scope to lower borrowing costs further if inflation pressure ease the NZD/USD has quickly moved lower and is now testing some pivotal support. Is this enough for the NZD to break lower and reignite the momentum lower ? Together with a market that is paring back USD shorts into Jackson Hole it does leave the NZD vulnerable.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P