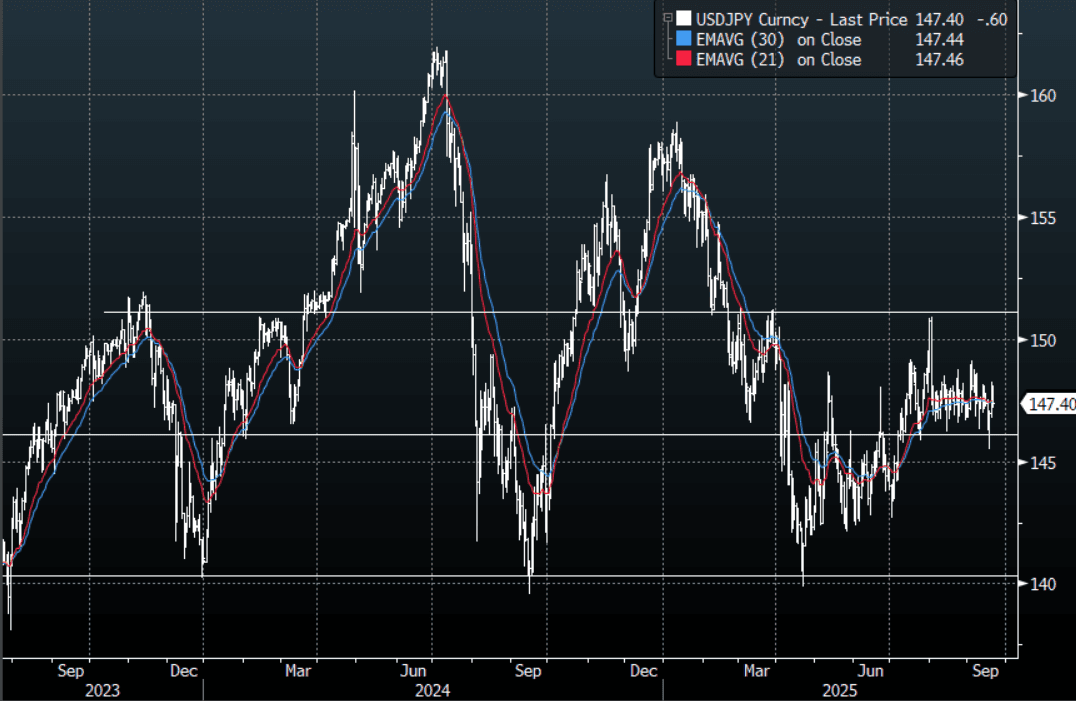

JPY: USD/JPY - Moves Lower As BOJ Has 2 Dissenters, Press Conference Next

The USD/JPY range has been 147.20 - 148.11 in the Asia-Pac session, it is currently trading around 147.40, -0.40%. USD/JPY stalled above 148.00 heading into the BOJ, 2 dissenters then saw the pair extend the move lower. The price is still in the middle of its recent 146-149 range, and we need a convincing break on either side to see some clearer direction again. The USD/JPY bears will be hoping that Governor Ueda provides a clearer path of when rate hikes could potentially begin, based on past performance I wouldn't be holding my breath.

- Bloomberg - Language of dissenters: “Takata Hajime considered that there had been a shift away from the deflationary norm and the price stability target had been more or less achieved. Tamura Naoki considered that, with risks to prices becoming more skewed to the upside, the Bank should set the policy interest rate a little closer to the neutral rate. They proposed that the Bank set the guideline for money market operations as follows: the Bank would encourage the uncollateralized overnight call rate to remain at around 0.75 percent.”

- MNI BRIEF: Japan Aug Core CPI Rises 2.7% Vs. July 3.1%. Japan’s annual core consumer inflation slowed to 2.7% y/y in August from 3.1% in July, the Ministry of Internal Affairs and Communications said Friday, as lower energy and food prices excluding perishables weighed on the index. The reading stayed above the Bank of Japan’s 2% target for the 41st straight month but fell below 3% for the first time since November 2024.

- "JAPAN RULING PARTY LAWMAKER TAKAICHI TO PROPOSE INCOME TAX CUT AND CASH PAYOUT TO HOUSEHOLDS, IN CAMPAIGN PLEDGE FOR RULING PARTY LEADERSHIP RACE, TAKAICHI TO CALL FOR GRADUALLY LOWERING RATIO OF GOVT DEBT TO GDP IN CAMPAIGN PLEDGE -NIKKEI" RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($600m), 146.00($820m), 148.00($539m). Upcoming Close Strikes : 145.00($1.92b Sept 19), 146.40($897m Sept 19) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Holding Richer After RBNZ's Forward Guidance

ACGBs (YM +4.5 & XM +3.5) are richer but off session bests.

- The local market has benefited from positive spillover from a strong post-RBNZ rally in NZGBs.

- The RBNZ cut the OCR by 25bps to 3.0%, as expected (4-2 vote; some favoured a 50bp cut), with forward guidance that saw the OCR averaging 2.71% in 4Q 2025, 2.56% in 2Q 2026, and 2.59% in 3Q 2026 (down from May's trough forecast of 2.9%). It indicated scope for further rate cuts if inflation pressures ease; forecasts imply a good chance of two more 25bp cuts.

- Cash US tsys are little changed in today's Asia-Pac session after modest gains.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at -2bps.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in September is given a 30probability, with a cumulative 37bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will see S&P Global PMIs (P) and Consumer Inflation Expectation data.

- The AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Friday.

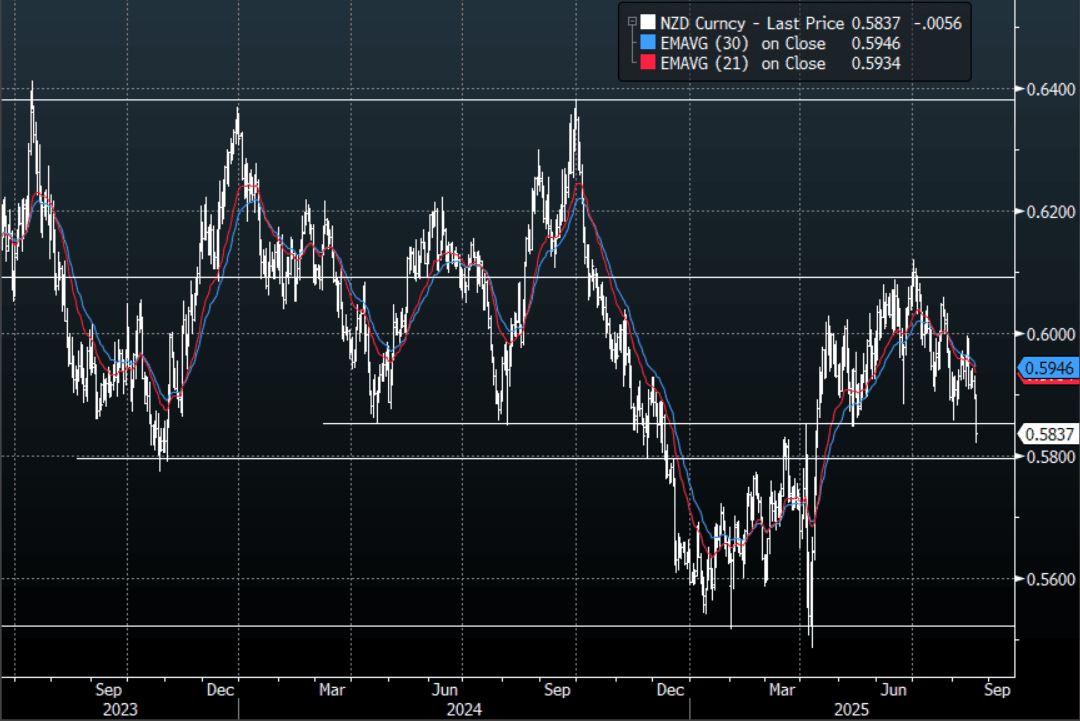

NZD: Asia Wrap - NZD/USD Probing Pivotal Support On A Dovish RBNZ Cut

The NZD/USD had a range of 0.5821-0.5900 in the Asia-Pac session, going into the London open trading around 0.5935, -0.95%. A dovish RBNZ that contemplated a cut of 50bps saw NZD/USD break lower and is now probing some pivotal support around the 0.5800/0.5850 area. Some of the crosses have broken some key levels AUD/NZD above 1.1000 & NZD/JPY below 86.50. Risk has extended its move lower this morning, E-minis -0.30%, NQU5 -0.45% adding to the weight in the NZD.

- RBNZ: OCR Path “Signals” Further Easing. The pace of NZ’s economic recovery appears to have disappointed the MPC with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2 with two members voting for a 50bp reduction. The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signaling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- "RBNZ GOV HAWKESBY: NEXT TWO MEETINGS ARE LIVE, NO DECISIONS HAVE BEEN MADE, OCR PROJECTION TROUGHS AROUND 2.5%, CONSISTENT WITH FURTHER CUTS” - [RTRS]

- "RBNZ GOV HAWKESBY: NEVER HAD A 4 TO 2 VOTE BEFORE, RANGE OF VIEWS AROUND THE RISKS TO OUTLOOK, MPC DEBATED RISKS AROUND MORE AGGRESSIVE CUT - [RTRS]"

- Whole Milk Prices Edge Higher At Latest Auction : Overnight the whole milk powder auction (held around 2 times per month) saw average prices rise 0.3% to $4036. Whole milk powder prices are up from recent lows but still around 7.7% off 2025 highs (albeit presenting a supportive backdrop for NZ's terms of trade).

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5925(NZD400m), 0.5950(NZD320m). Upcoming Close Strikes : 0.5980(NZD660m Aug 21). - BBG

- AUD/NZD range for the session has been 1.0939 - 1.1064, currently trading 1.1035. The dovish RBNZ has seen the Cross surge higher breaking back above 1.100 convincingly. This move should now see dips supported as it looks to build momentum to push higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: RBNZ Forward Guidance Sparks Massive Rally

NZGBs closed 10-16bps richer, with a steeper 2/10 curve, after today’s RBNZ policy decision.

- The pace of NZ’s economic recovery appears to have disappointed the MPC, with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2, with two members voting for a 50bp reduction.

- The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signalling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- The revised OCR path implies another 43bp of easing by year end with 16bp in Q1 2026.

- Swap rates closed 11-18bps lower, with a steeper 2s10s curve.

- RBNZ dated OIS pricing closed 14-23bps softer for meetings beyond August. 35bps of cumulative easing is priced by November 2025.

- Tomorrow, Governor Hawkesby will appear before a parliamentary committee to talk about the latest Monetary Policy Statement.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.