BONDS: NZGBS: Post-GDP Rally Extends, Light Calendar Next Week

NZGBs closed 3-4bps richer, extending yesterday’s post-Q2 GDP rally. Benchmark yields are 7-18bps lower than pre-data levels, with the 2/10 curve steeper.

- NZGBs outperformance versus the $-bloc continued, with the NZ-US and NZ-AU 10-year yield differentials 8bps tighter on the day.

- Swap rates closed 2-4bps lower, with the 2s10s curve steeper.

- Bloomberg - "RBNZ Nowcast Estimate of New Zealand GDP Shows 3q Expansion. RBNZ updates its Kiwi-GDP nowcast estimate for 3q GDP growth, on its website. Shows GDP expanding 0.6% q/q. Gauge has picked up steadily since showing 0.2% growth in early July. NOTE: 2q nowcast estimated a 0.2% contraction, but eventual result was a 0.9% downturn."

- RBNZ dated OIS pricing closed 1-5bps softer across meetings. 33bps of easing is priced for October, with a cumulative 59bps by November 2025.

- The local calendar is empty next week apart from ANZ Consumer Confidence on Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Mostly Cheaper With A Steeper Curve

JGB futures are little changed, -3 compared to settlement levels.

- Japan Export Growth Negative, Lagging Other Parts Of Asia : Japan July export and import outcomes were fairly close to market expectations, but the trade balances were slightly weaker. Exports fell -2.6%y/y (-2.1% forecast and -0.5% prior), while imports were -7.5%y/y, (-10.0% forecast and 0.3% prior). The trade deficit was -117.5bn, against a 198.5bn forecast.

- Japan Core Machine Orders Above Forecasts, Suggesting Resilient Capex : Japan June core machine orders were better than forecast. We rose 3.0%m/m, versus -0.5% forecast and -0.6% prior. The y/y print was 7.6%, against a 4.7% forecast and 4.4% prior. Today's machine orders print continues to paint a resilient capex picture for Japan's economy.

- US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 0.5bp lower (7-year) to 3bps higher (40-year). The benchmark 10-year yield is 0.4bp higher at 1.606% versus the cycle high of 1.616%.

- Swap rates are flat to 1-2bps higher, with a steepening bias.

- Tomorrow, the local calendar will see Weekly International Investment Flows, S&P Global PMIs (P) and Machine Tool Orders alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

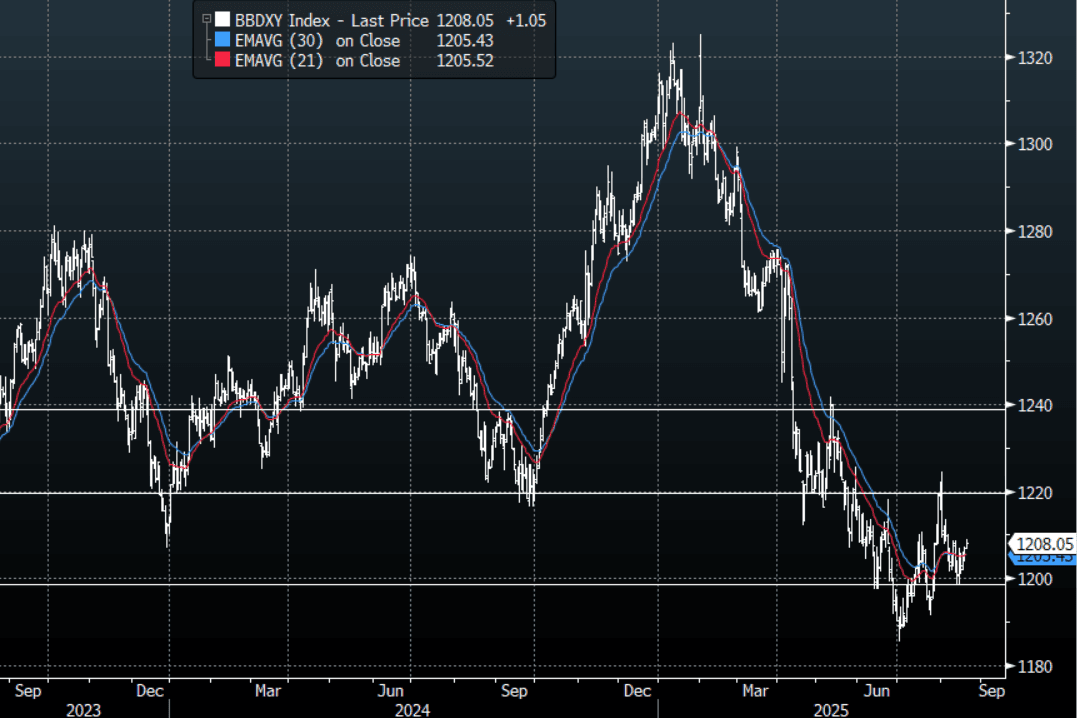

FOREX: Asia FX Wrap - The USD Bid Remains Steady Heading Into Jackson Hole

The BBDXY has had a range of 1206.79 - 1208.95 in the Asia-Pac session, it is currently trading around 1208, +0.10%. The USD continues to see profit-taking as the market pares back some risk as we head into Jackson Hole at the end of the week. Depending on the contents of Powell's speech this could change very quickly but the BBDXY looks to be putting in a third higher low which would be a worrying sign to the bears that we could be putting in a short-term base. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows, but risk is more likely skewed to the USD shorts continuing to be reduced into Powell's speech.

- EUR/USD - Asian range 1.1622 - 1.1651, Asia is currently trading 1.1635. The market is trading sideways in a 1.1600-1.1750 range heading into Jackson Hole. The pair is unlikely to extend too far as the market awaits Powell's speech.

- GBP/USD - Asian range 1.3462 - 1.3493, Asia is currently dealing around 1.3475. Having broken back above its pivot look for dips to again be supported, with risk retracing the pair is probing its first support seen towards 1.3400.

- USD/CNH - Asian range 7.1868-7.1931, the USD/CNY fix printed 7.1384, Asia is currently dealing around 7.1890. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.30%, Gold $3320, US 10-Year 4.31%, BBDXY 1208, Crude Oil $62.41

- Data/Events : EZ CPI, Germany PPI

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Holding Richer After RBNZ's Forward Guidance

ACGBs (YM +4.5 & XM +3.5) are richer but off session bests.

- The local market has benefited from positive spillover from a strong post-RBNZ rally in NZGBs.

- The RBNZ cut the OCR by 25bps to 3.0%, as expected (4-2 vote; some favoured a 50bp cut), with forward guidance that saw the OCR averaging 2.71% in 4Q 2025, 2.56% in 2Q 2026, and 2.59% in 3Q 2026 (down from May's trough forecast of 2.9%). It indicated scope for further rate cuts if inflation pressures ease; forecasts imply a good chance of two more 25bp cuts.

- Cash US tsys are little changed in today's Asia-Pac session after modest gains.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at -2bps.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in September is given a 30probability, with a cumulative 37bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will see S&P Global PMIs (P) and Consumer Inflation Expectation data.

- The AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Friday.