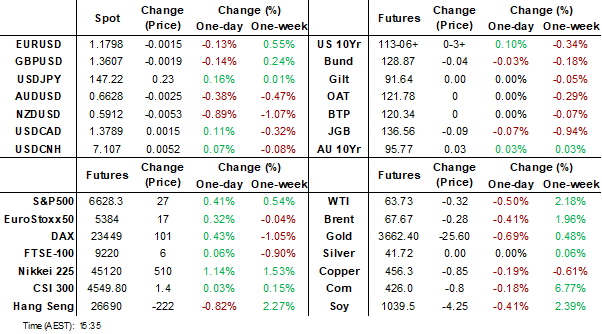

MNI EUROPEAN MARKETS ANALYSIS: USD Rises, BoE In Focus Later

- NZ has been in focus, with a sharp move lower in NZD and local yields, after Q2 GDP fell 0.9%q/q (well below market and RBNZ forecasts). RBNZ dated OIS pricing is 9-15bps softer across meetings versus yesterday’s close.

- Australia’s monthly labour market data are volatile and August seemed to unwind July’s moves. Looking through this, annual employment growth was its lowest since the pandemic but the unemployment rate held steady at 4.2%. The AUD has weakened, although is still up against NZD.

- US Tsy yields have edged lower, but the USD is higher, particularly against some of the Asian currencies. China tech equities continue to rally.

- Later the August US lead index, September Philly Fed and jobless claims print. The BoE is expected to leave rates unchanged at 4% and the ECB’s Lagarde, Buch, de Guindos and Schnabel speak.

MARKETS

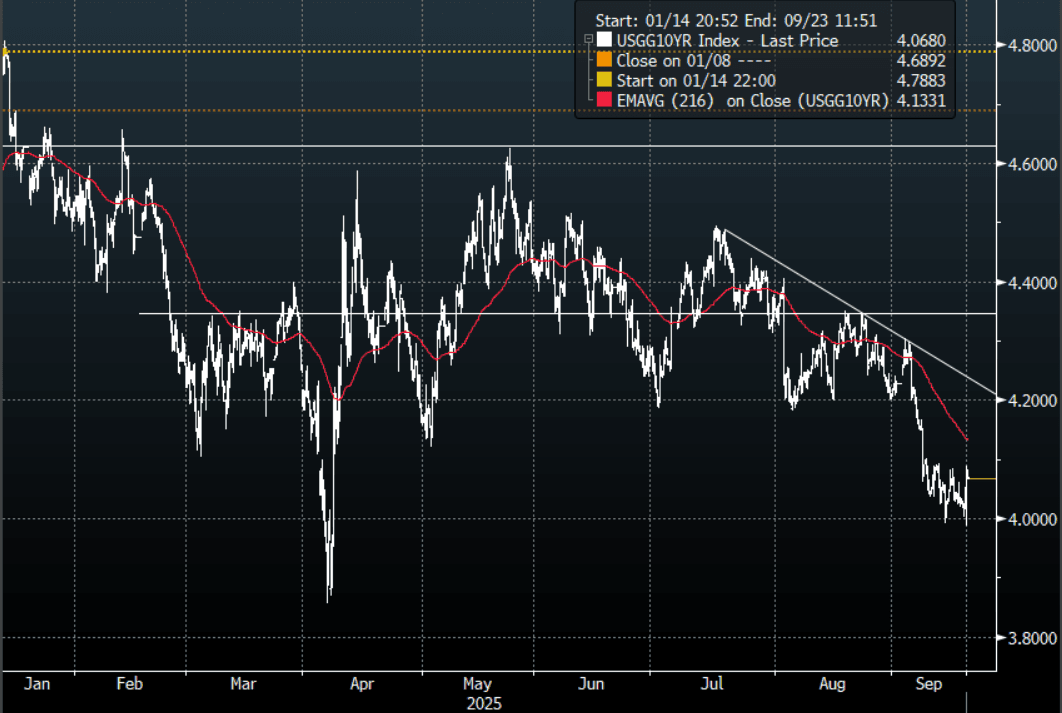

US TSYS: Asia Wrap - Yields Edge Lower

The TYZ5 range has been 113-00 to 113-07 during the Asia-Pacific session. It last changed hands at 113-06+, up 0-02 from the previous close.

- The US 2-year yield has edged lower trading 3.536%, down 0.02 from its close.

- The US 10-year yield has edged lower trading around 4.068%, down 0.02 from its close.

- (Bloomberg) -- The Federal Reserve’s first interest rate cut since December to shield the jobs market collides with a revision higher for its economic growth and inflation forecasts, leaving the central bank ever-more data dependent.

- RenMac on X: “We have two sided risks which means there is no risk free path.” The next two meetings should be priced closer to a coin flip for rate cuts.”

- Jim Bianco on X: “This meeting was a mess. One member of the FOMC thinks the Fed is going to HIKE rates this year. One (Stephen Miran) thinks it is going to cut 1.25% this year (5 cuts over two meetings). Add to this is Powell using the term "Risk Management" to describe this cut. If this is the case now, then the Fed cannot also be data dependent. Both cannot be true at the same time.”

- Data/Events: Initial Jobless Claims, Philadelphia Fed Business Outlook, Leading Index, Net Long-term TIC Flows

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

BOJ: MNI BoJ Preview - Sep 2025: Maintain Cautious Stance On Hikes

EXECUTIVE SUMMARY

- The Bank of Japan is expected to keep policy unchanged in September, with future decisions hinging on October’s Tankan survey and branch managers’ meeting, which will clarify corporate sentiment and investment trends.

- External risks, particularly the impact of U.S. tariffs and potential weakness in U.S. labour markets, are now the central concern, limiting the urgency for near-term rate hikes despite inflation hovering near 3%.

- Political uncertainty following Prime Minister Ishiba’s resignation complicates the outlook, with leading candidates and opposition parties generally favouring fiscal stimulus and accommodative monetary policy.

- Analysts are split: some see the BoJ at risk of falling behind the curve, while others argue the next meaningful opportunity for a hike could be as late as 2026, depending heavily on wage momentum and inflation sustainability.

- Governor Ueda’s cautious communication style is expected to reinforce market perceptions of dovishness, emphasising flexibility and conditionality rather than committing to a specific tightening timeline.

- Full preview here:

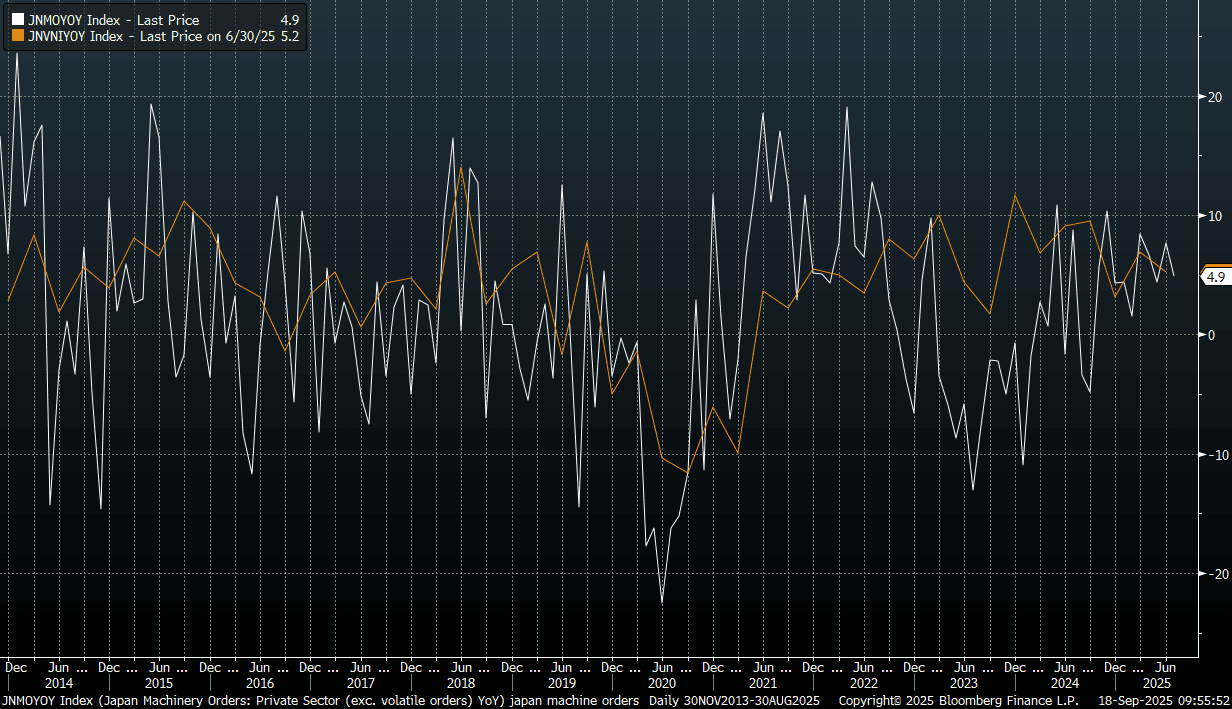

JAPAN DATA: July Core Machine Orders Below Forecasts, Y/Y Momentum Holding Up

Japan July core machine orders printed below forecasts. We fell 4.6%m/m in July against a -1.5% forecast (and after a 3.0% rise in June). In y/y terms we rose 4.9%, against a 5.2% forecast and 7.6% gain in June. The chart below shows core machine orders against capex for Japan, both in y/y terms. We are off recent highs, but the July machine orders update is not pointing to sharp weakening in y/y momentum.

- In terms of the detail, government/public machine orders were up 21.3%m/m, but this segment is very volatile. Manufacturing and non-manufacturing both recorded rises in the month, but this was likely due to volatile components, which are excluded from the core machine headline outcome.

Fig 1: Japan Core Machine Orders & Capex Y/Y

Source: Bloomberg Finance L.P./MNI

JGBS: Long-End Rallies Ahead Of BoJ Policy Decision, Natl CPI Tomorrow Too

JGB futures are weaker and near session lows, -13 compared to settlement levels.

- Cash US tsys are 2-3bps richer in today's Asia-Pac session after yesterday's post-FOMC sell-off. Focus turns to Thursday's weekly claims.

- Cash JGBs are little changed across benchmarks out to the 10-year but 2-4bps richer beyond. The benchmark 10-year yield is 0.4bp higher at 1.603% versus the cycle high of 1.6490%.

- Swap rates have twist-flattened, with rates 2bps higher to 2bps lower. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see National CPI and Weekly Investment Flow data alongside the BoJ Policy Decision.

- The Bank of Japan is expected to keep policy unchanged in September, with future decisions hinging on October's Tankan survey and branch managers' meeting, which will clarify corporate sentiment and investment trends.

- External risks, particularly the impact of U.S. tariffs and potential weakness in U.S. labour markets, are now the central concern, limiting the urgency for near-term rate hikes despite inflation hovering near 3%.

- Political uncertainty following Prime Minister Ishiba's resignation complicates the outlook, with leading candidates and opposition parties generally favouring fiscal stimulus and accommodative monetary policy. Full MNI BoJ Preview here:

AUSSIE BONDS: Modestly Richer After Employment Data

ACGBs (YM +2.0 & XM +1.5) are slightly richer after the August jobs data missed expectations.

- Australia’s monthly labour market data are volatile and August seemed to unwind July’s moves. Looking through this, annual employment growth was its lowest since the pandemic but the unemployment rate held steady at 4.2% and underemployment continued to trend down to its lowest since 1991. RBA Governor Bullock focused on the Q2 average unemployment rate, given the data’s volatility and that is likely to remain the case. September prints on 16 October.

- Cash US tsys are 2-3bps richer in today's Asia-Pac session after yesterday's post-FOMC sell-off. Focus turns to Thursday's weekly claims.

- Cash ACGBs are 2bps richer on the day, 2-3bps richer after the data. The AU-US 10-year yield differential is at +14bps.

- Swap rates are 3bps lower post-data.

- The bills strip is +2 to +4 across contracts, with a flattening bias.

- RBA-dated OIS pricing is softer across meetings after the data. A 25bp rate cut in September is given a 10% probability, with a cumulative 30bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$1000mn of the 1.00% 21 December 2030 bond.

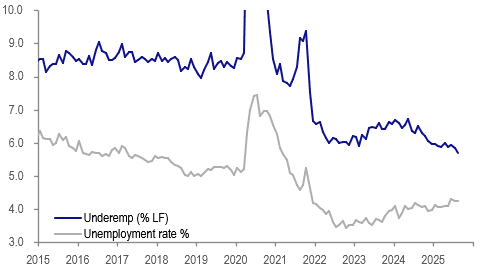

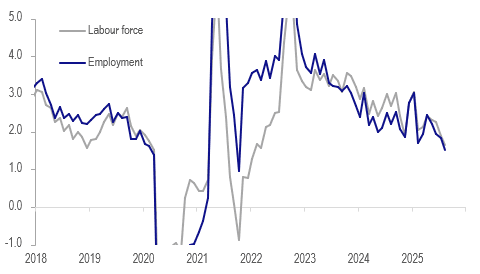

AUSTRALIA DATA: Jobs Volatile, Underemployment Very Low

Australia’s monthly labour market data are volatile and August seemed to unwind July’s moves. Looking through this, annual employment growth was its lowest since the pandemic but the unemployment rate held steady at 4.2% and underemployment continued to trend down to its lowest since 1991. RBA Governor Bullock focussed on the Q2 average unemployment rate given the data’s volatility and that is likely to remain the case. September prints on 16 October.

Australia unemployment vs underemployment rates %

Source: MNI - Market News/ABS

- Employment fell 5.4k in August after rising 26.5k driven by a 40.9k drop in full-time jobs (FT) following July’s +63.6k. Part-time (PT) rose 35.6k after falling 37.2k and the 3-month average at 12.9k is outperforming FT’s -5.1k. Annual growth is at 1.5% y/y, the lowest since 2021, with FT up 1.3% y/y and PT +1.9%.

- Again there are tentative signs of a switch away from FT jobs to PT, which was also reflected in hours worked with FT down 0.9% m/m but up 0.8% y/y but PT up 1.8% m/m & 2.1% y/y. More data is needed though to confirm this.

- The participation rate eased to 66.8% from 67% with the labour force falling 6k in August despite a 38k increase in the working-age population. Thus the number of unemployed fell 0.9k keeping the unemployment rate steady at 4.2%. The Q3 average is in line with Q2’s.

- The decline in the labour force and participation rate suggest that the soft jobs print may reflect fewer skilled candidates in August.

Australia employment vs labour force y/y%

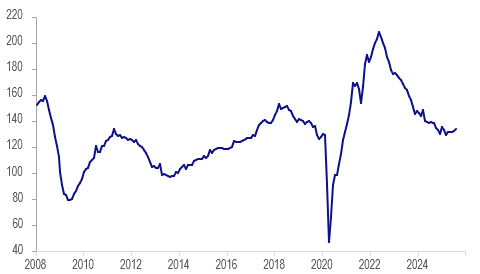

AUSTRALIA DATA: Q3 Data Show Stabilisation, Underemployment Still Trending Down

While the headline employment and unemployment rate numbers get most of the attention, the RBA looks deeper and monitors underemployment, youth unemployment, hours worked, vacancies, the quit rate and labour shortage measures closely. Governor Bullock was also clear that given the data’s volatility, it focuses on the quarterly averages. While August employment and hours were disappointing, other variables signalled that the labour market remains solid.

- The underemployment rate continued to trend lower falling 0.1pp in August to 5.7%, the lowest since 1991. The Q3 average to date is down 0.1pp to 5.8%. The 2024 average was 6.4%. Q3 average of the unemployment rate was in line with Q2 at 4.2%.

- Q3 employment is up 0.2% q/q to date, a slowdown from Q2’s +0.6% q/q but in line with Q1’s +0.3% q/q.

- The youth unemployment rate was stable at 9.7% in August but the Q3 average is 0.1pp higher than Q2. It is of interest as it can lead the broader labour market.

Australia unemployment rate 15-24 years %

- Hours worked fell 0.4% m/m in August driven by a 0.9% drop in full-time (FT). Q3 is down with both FT and PT down 0.1% q/q.

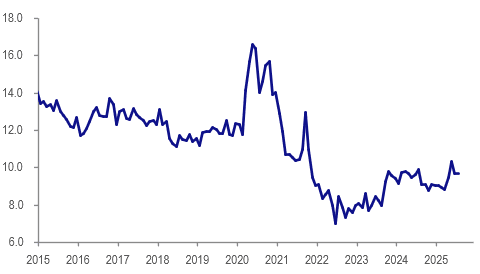

- SEEK new job ads rose for the second straight month in August to be down 3.4% y/y with 3-month momentum picking up to its fastest in just over 3 years. Internet vacancies to unemployed stabilised in July.

Australia SEEK new job ads 2013=100

Source: MNI - Market News/SEEK

BONDS: Market Ponders A 50bp Cut After Weak Q2 GDP

NZGBs closed showing a massive bull-steepener, with benchmark yields 4-12bps lower.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. With two votes for a 50bp cut in August, the risk of a larger move before year-end is material.

- Statistics NZ reported that 10 out of 16 industries contracted in Q2 with manufacturing the largest falling 3.5% q/q. Construction was down 1.8% q/q with the sector continuing to struggle.

- GFCF fell 1.1% q/q, the seventh quarterly decline in the last 2 years, with residential building down 1.9% q/q and other assets -0.9% q/q. GFCF is down 3.2% y/y after -3.4% in Q1.

- Today’s weekly supply saw solid demand, with cover ratios ranging from 3.22x (May-34) to 3.41x (May-30).

- Swap rates closed 5-11bps lower.

- RBNZ dated OIS pricing closed sharply softer across meetings. 33bps of easing is priced for October, with a cumulative 57bps by November 2025.

- Tomorrow, the local calendar will see trade balance data.

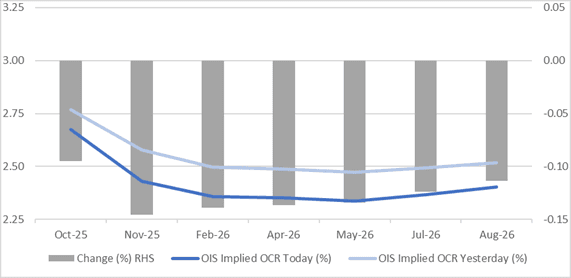

STIR: RBNZ-Dated OIS Shunts Softer After Weak GDP Print

Following today's weak Q2 GDP print, RBNZ dated OIS pricing is 9-15bps softer across meetings versus yesterday’s close.

- 33bps of easing is priced for October, with a cumulative 57bps by November 2025.

Figure 1: RBNZ Dated OIS Current vs. Yesterday (%)

Source: Bloomberg Finance LP / MNI

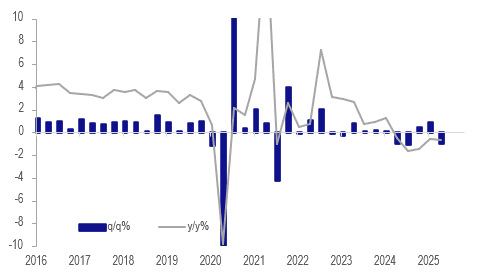

NEW ZEALAND: Very Weak Growth Increases Chance Of Larger Rate Cut

Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. With two votes for a 50bp cut in August, the risk of a larger move before year end is material.

NZ GDP y/y% production

- Statistics NZ reported that 10 out of 16 industries contracted in Q2 with manufacturing the largest falling 3.5% q/q. Construction was down 1.8% q/q with the sector continuing to struggle.

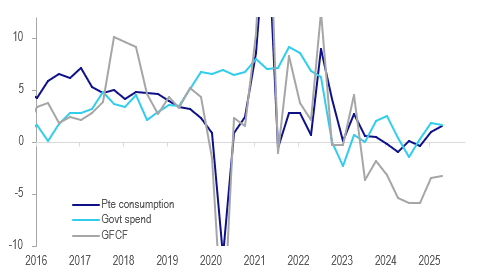

- Private and government consumption were the only positives in the expenditure measure of GDP rising 0.4% q/q and 0.1% q/q respectively. Household spending is gradually recovering with higher durables & non-durables, Q2 the third consecutive increase and the annual rate up to 1.5% from 1.0% and -1.0% a year ago.

- GFCF fell 1.1% q/q, the seventh quarterly decline in the last 2 years, with residential building down 1.9% q/q and other assets -0.9% q/q. GFCF is down 3.2% y/y after -3.4% in Q1.

- Goods & services exports fell 1.2% q/q to be up 0.7% y/y (Q1 3.6%) with goods down 2.6% q/q, driven by dairy & meat, and services -1.1% q/q. Imports rose 0.6% q/q driven by a 4.2% q/q increase in services.

NZ domestic demand y/y%

Source: MNI - Market News/LSEG

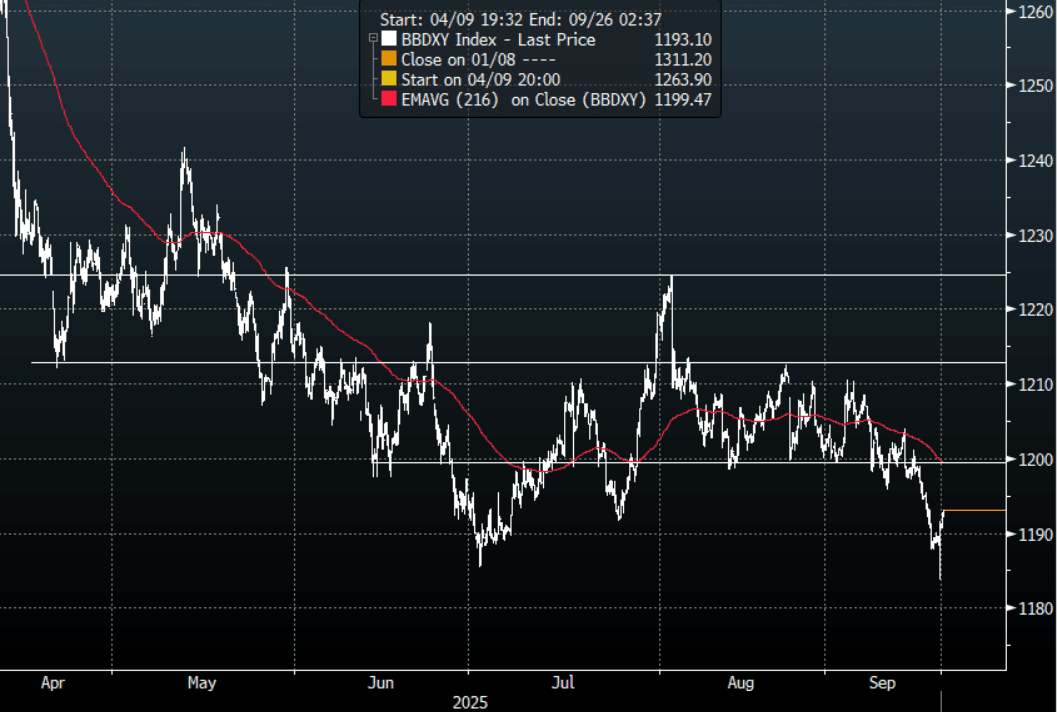

FOREX: Asia FX Wrap - The USD Gets A Reprieve, For How Long ?

The BBDXY has had a range of 1190.63 - 1192.71 in the Asia-Pac session; it is currently trading around 1193, +0.20%. The USD bounced as the Fed could not reach the levels of dovishness the market had been pricing in. How far can this market retrace, I suspect sellers would be all over a bounce back toward 1200 initially. A break below 1180 has been put off for now, but it feels like we will have another look down there at some point.

- EUR/USD - Asian range 1.1808 - 1.1829, Asia is currently trading 1.1800. The pair is is consolidating above 1.1800 after the USD failed to break lower. Should this level be sustained the first target is 1.2000 then the focus moves to the 1.2200/2300 area.

- GBP/USD - Asian range 1.3610 - 1.3635, Asia is currently dealing around 1.3610. The pair is probing the top-end of its recent 1.3350-1.3650 range after a false break overnight, price action suggests it may be looking to break these highs and reassert its momentum higher. A sustained break above 1.3650 will initially target the year's highs just below 1.3800, through here it would open a move back to the 1.4200/1.4300 area.

- USD/CNH - Asian range 7.0934 - 7.1087, the USD/CNY fix printed 7.1085, Asia is currently dealing around 7.1050. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.50%, Gold $3656, US 10-Year 4.066%, BBDXY 1193, Crude Oil $63.81

- Data/Events : EZ Current Account & Construction Output MoM, Italy Current Account Balance

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

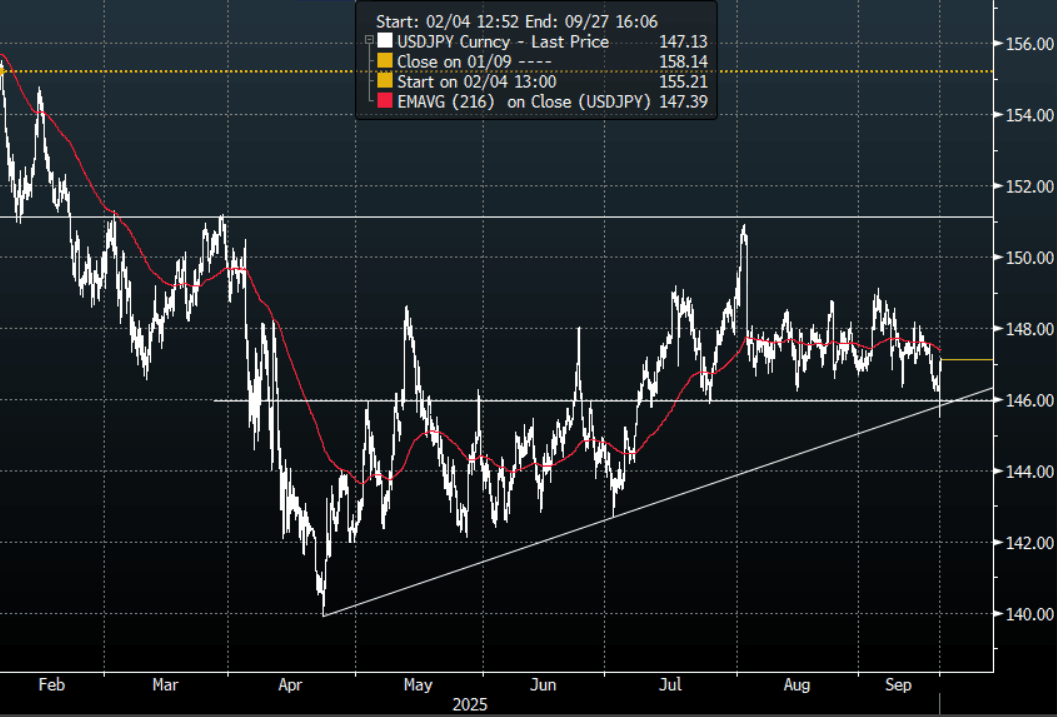

JPY: Asia Wrap - USD/JPY Consolidates Around 147.00 After False Break Lower

The USD/JPY range has been 146.77 - 147.15 in the Asia-Pac session, it is currently trading around 147.10, +0.10%. USD/JPY tried and failed to break lower as the USD bounced when the FOMC could not deliver on the markets level of dovishness priced in. The price is now back towards the middle of its recent 146-149 range, and we need a convincing break on either side to see a clearer direction again. A move back below 145/146 is needed to potentially start seeing the short Yen positions being flushed out. Just the BOJ left this week to potentially be that catalyst ?

- MNI AU - July Core Machine Orders Below Forecasts, Y/Y Momentum Holding Up: Japan July core machine orders printed below forecasts. We fell 4.6%m/m in July against a -1.5% forecast (and after a 3.0% rise in June). In y/y terms we rose 4.9%, against a 5.2% forecast and 7.6% gain in June. We are off recent highs, but the July machine orders update is not pointing to sharp weakening in y/y momentum.

- Nikkei Asia via BBG - “The Bank of Japan is expected to hold interest rates steady at its monetary policy meeting this week, Nikkei has learned, as the central bank continues to mull the effects of U.S. tariffs on wages, business investment and the domestic economy.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($600m), 146.00($820m), 148.00($539m). Upcoming Close Strikes : 145.00($1.92b Sept 19), 146.40($897m Sept 19) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs again as they look to rebuild their position +87239( Last +78427), leveraged funds reduced their short position perhaps losing confidence the support will continue to hold -49591(Last -66914).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

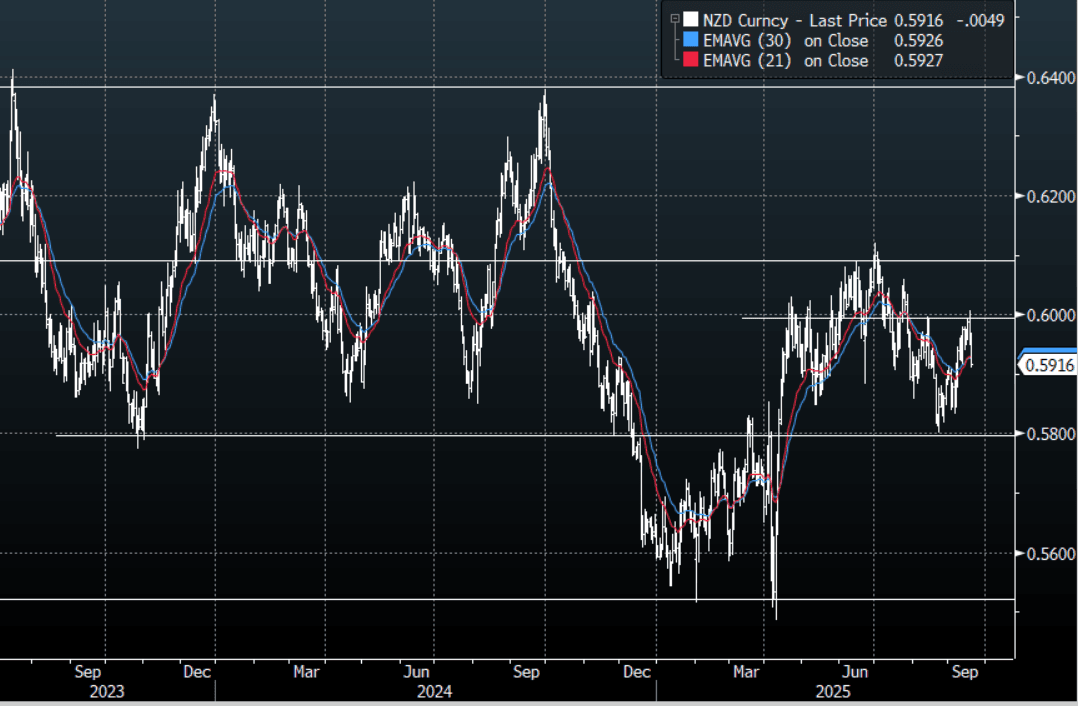

NZD: Asia Wrap - Very Weak GDP Sees NZD Underperform Across The Board

The NZD/USD had a range of 0.5911 - 0.5968 in the Asia-Pac session, going into the London open trading around 0.5920, -0.80%. The very weak GDP data this morning points to a poor backdrop for growth and increases the chance of larger rate cuts. The NZD rejected the 0.6000 area and looks set to potentially move lower now, I suspect some demand will reemerge back towards the 0.5900 area first up, through here and the pivotal 0.5800 support looms. The trend against the USD is a little harder to predict but the NZD underperformance in the crosses is beginning to gain real momentum.

- MNI AU - NZ Q2 GDP, Very Weak Growth Increases Chance Of Larger Rate Cut: Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. With two votes for a 50bp cut in August, the risk of a larger move before year end is material.

- Bloomberg - Westpac Sees Kiwi Falling to 58 US Cents on Deep RBNZ Rate Cuts. Westpac now expects RBNZ to cut by 50bps at its Oct. meeting and another 25bps in November to bring the official cash rate to 2.25%. They entered a short NZD/USD position “targeting 0.5800 or lower". "The USD leg has already priced in an aggressive easing cycle, and there is no top-tier US data until GDP”.

- “ASB BANK NOW SEES RBNZ CUTTING CASH RATE TO 2.5% IN OCTOBER, NOW SEES RBNZ CUTTING CASH RATE TO 2.25% BY YEAR END" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5935(NZD737m). Upcoming Close Strikes : 0.6020(NZD 374m Sept 22) - BBG

- AUD/NZD range for the session has been 1.1143 - 1.1241, currently trading 1.1210. The Cross is breaking above the multiple highs around the 1.1200 area and is looking to accelerate higher on the back of some very poor Q2 GDP data. Dips should now continue to be supported as the move higher begins to gather pace.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

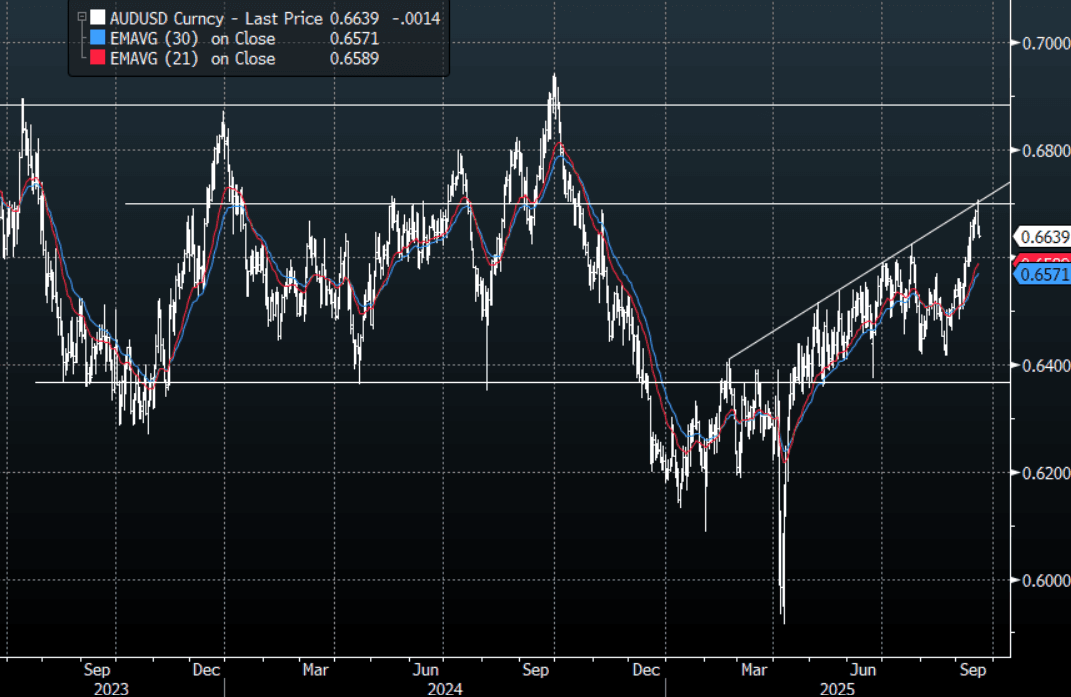

AUD: Asia Wrap - AUD/USD Extends Retracement On Employment Data

The AUD/USD has had a range of 0.6634 - 0.6659 in the Asia- Pac session, it is currently trading around 0.6640, -0.23%. The AUD pulled back overnight and this morning's unexpected drop in employment has seen the move extend lower, retracing some of its recent gains. The AUD move higher failed towards 0.6700 as the USD found some relief. Do we see a further short-term retracement in the USD, if so I suspect the reprieve is temporary. The price action in the AUD/USD suggests dips will be supported for now with the first buy-zone back towards the 0.6550 area. A retest of the 0.6700 area at some point seems to be a question of timing.

- MNI AU - Jobs Volatile, Underemployment Very Low: Australia’s monthly labour market data are volatile and August seemed to unwind July’s moves. Looking through this, annual employment growth was its lowest since the pandemic but the unemployment rate held steady at 4.2% and underemployment continued to trend down to its lowest since 1991. RBA Governor Bullock focussed on the Q2 average unemployment rate given the data’s volatility and that is likely to remain the case. September prints on 16 October.

- MNI AU - Q3 Data Show Stabilisation, Underemployment Still Trending Down: While the headline employment and unemployment rate numbers get most of the attention, the RBA looks deeper and monitors underemployment, youth unemployment, hours worked, vacancies, the quit rate and labour shortage measures closely. Governor Bullock was also clear that given the data’s volatility, it focuses on the quarterly averages. While August employment and hours were disappointing, other variables signalled that the labour market remains solid.

- " AUSTRALIA PM ALBANESE: ANNOUNCES A$5 BILLION NET ZERO FUND IN THE NATIONAL RECONSTRUCTION FUND, A$2 BILLION FOR THE CLEAN ENERGY FINANCE CORPORATION TO CONTINUE TO DRIVE DOWNWARDS PRESSURE ON ELECTRICITY PRICES" RTRS

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD1.13b), 0.6650(AUD774m). Upcoming Close Strikes : 0.6650(AUD906m Sept 23), 0.6750(AUD1.16b Sept 19) - BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Global Tech Rally Benefits Asia

The global tech rally continues to support key markets in Asia with the Hang Seng Tech and the KOSDAQ up strongly. Chip related stocks were strong in Hong Kong following a regulatory ban on Nvidia, boosted expectations for growth for Chinese tech companies.

- The Hang Seng is down marginally by -0.18% whilst the CSI 300 is up +0.32%, Shanghai up +0.45% and Shenzhen up +0.70%.

- The NIKKEI is up +1.3% today, hitting new all time highs of 45,383.

- The KOSPI is up +1.13% to also reach a new high of 3,450.

- The FTSE Malay KLCI is down -0.81%, taking back all of yesterday's gains.

- The Jakarta Comp roared with the unexpected BI rate cut and is up at new all time highs of 8,046.

- The NIFTY 50 has opened Thursday strongly up +0.33% and has produced positive gains for the 17 of 19 last trading days.

ASIA STOCKS: South Korea & Taiwan See Modest Outflows, Malaysian Inflows Firmer

Yesterday saw modest outflow pressures from both South Korea and Taiwan. This followed a generally strong period of prior inflow momentum, so some slowing was not surprising, particularly given the Fed risks due later on Wednesday. For Wednesday trade, both onshore equity markets also pulled back from recent highs. The overnight tone was softer US equity trends, including in the tech space, but losses were modest. US futures are also up in early dealings today, led by the tech side. In early Thursday dealings the Kospi is up around 0.50%. Both the South Korean and Taiwan markets return solid 5-day rolling sum momentum.

- Elsewhere, India enjoyed better inflow momentum on Tuesday, helping drive a better 5-day sum backdrop. Part of the focus will remain on US-India trade talks and whether warm ties between PM Modi and US President Trump can help lower tensions.

- Indonesia saw modest outflows yesterday, despite the JCI moving higher (above 8000) in the aftermath of the surprise BI cut.

- Malaysian markets returned and with local markets rising, we saw some catch up from a offshore flow standpoint.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -144 | 2481 | -1151 |

| Taiwan (USDmn) | -45 | 3066 | 8368 |

| India (USDmn)* | 187 | 388 | -15260 |

| Indonesia (USDmn) | -9 | 18 | -3696 |

| Thailand (USDmn) | -6 | 65 | -2510 |

| Malaysia (USDmn) | 83 | 164 | -3669 |

| Philippines (USDmn) | 12 | 11 | -724 |

| Total (USDmn) | 79 | 6193 | -18642 |

| * Data Up To Sep 16 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Trending Lower As Energy Demand In Focus

Oil prices have continued to trend lower after falling close to a percent on Wednesday driven by the Fed’s cautious tone especially in regards to downside risks to the labour market. The US dollar has also continued trending higher (BBDXY +0.2%) during today’s APAC trading impacting dollar-denominated crude. WTI is down 0.5% to $63.75/bbl off the intraday low of $63.56. It reached $64.14 early in the session. Brent is 0.3% lower at $67.73/bbl after falling to $67.50.

- The Fed’s warning of risks to the labour market added to market concerns regarding the strength of energy demand given the increase in US tariffs this year and the IEA’s forecast of a record oil surplus in 2026. The 25bp Fed cut was widely expected and so the outlook for future meetings will be monitored closely.

- Geopolitical risks stemming from Ukrainian attacks on Russian refining and export facilities as well as increased sanctions on Russia and those who buy its fossil fuels persist.

- Later the August US lead index, September Philly Fed and jobless claims print. The BoE is expected to leave rates unchanged at 4% and the ECB’s Lagarde, Buch, de Guindos and Schnabel speak.

Gold Holds Losses As USD Strengthens

The US dollar continued trending higher (BBDXY +0.2%) during today’s APAC trading, thus gold prices are moderately lower. They are down 0.1% to $3655/oz off the intraday low of $3651.98 which followed a peak of $3672.06. The downside has been limited by slightly lower Treasury yields.

- The Fed cut rates as expected due to a weaker labour market and Chair Powell’s comments were cautious. He said that “there’s no risk-free path now” and that while 10 FOMC members indicated two or more rate cuts by year end, 9 had fewer and so the committee is “in a meeting by meeting situation”. While Powell noted upside risks to inflation, he said that the impact from higher tariffs had been less than expected to date.

- The administration’s new FOMC appointment Miran voted for a 50bp cut adding to fears for the Fed’s independence.

- Silver has continued falling today after Wednesday’s 2.1% drop. It is currently down 0.7% to $41.38 after a low of $41.309.

- Equities are mixed with the S&P e-mini up 0.5% and CSI 300 +0.3% but Hang Seng down 0.2% and ASX -0.6%. Oil prices are lower with WTI -0.4% to $63.80/bbl. Copper is down 0.4%.

- Later the August US lead index, September Philly Fed and jobless claims print. The BoE is expected to leave rates unchanged at 4% and the ECB’s Lagarde, Buch, de Guindos and Schnabel speak.

INDONESIA: BI Cuts In “Joint Effort” To Boost Growth

Bank Indonesia (BI) unexpectedly cut rates 25bp to 4.75%, the third consecutive monthly easing, which is unusual. It is especially surprising given it has intervened to defend the rupiah in the last few weeks due to political instability and previously emphasised the importance of FX and financial stability. President Prabowo has a growth target of 8% (Q2 GDP grew at 5.1% y/y) and BI may also be shifting more towards supporting the economy.

- BI’s accompanying statement added the phrase “joint efforts to stimulate economic growth”, which suggests that it may be supporting government policy.

- It has left its growth forecast unchanged for 2025 at “above the midpoint of the 4.6-5.4% range”. It does expect H2 2025 to improve due to the “strengthening policy synergy between Bank Indonesia and the Government”.

- BI will continue watching economic and price developments for opportunities to ease further assuming IDR stability. It will continue its macroprudential policies to boost lending, which it has been doing for some time.

- It noted that “economic growth in Indonesia must be increased in line with economic capacity” suggesting that it believes there is a negative output gap. It observes that consumption in Q3 is “restrained” given lower sentiment driven by a weaker labour market.

- It also mentioned that capex needs to be supported by “accelerating the realisation of various government priority programs”, which is an addition to the statement.

- USDIDR reached a peak of 16440 on Wednesday but finished down 0.1% at 16430. It peaked at 16498 following the replacement of Finance Minister Indrawati. With the Fed also cutting rates 25bp on Wednesday, the US-Indonesian rate differential held steady but at an 18 month low.

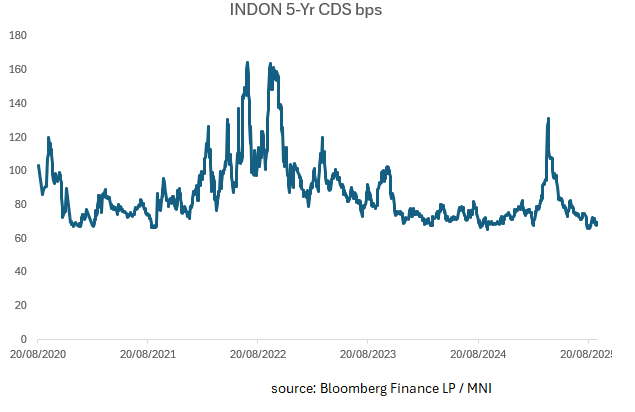

INDONESIA: Case for Further CDS Tightening Seems Limited

- The performance of the INDON 5-Yr CDS since April has been remarkable, tightening from the wides of +131bps to a low of +66bps in August.

- With the new FinMin seemingly underwriting the President's ambitious growth targets, we highlighted recently that the options available are walking away from the deficit cap of 3% and or lower rates.

- The new FinMin has already made some policy adjustments withdrawing US$12bn equivalent from the Central Bank and distributing to the state owned banks with instructions to lend. he FinMin has indicated that the new Sovereign Wealth Fund Danantara will be used increasingly to help achieve the growth targets.

- However, it seems unlikely that Danantara and increased lending alone will supersize growth. Government spending must rise, which creates risk of challenging the deficit cap (3% of GDP).

- Central Bank rates may need to be cut yet at this point, the Bank Indonesia remains ' independent '. Yet the idea of independence may now be in question following the BI's surprise cut in rates overnight. Only 2 of 38 forecasts on BBG suggested a cut with the main Indonesian banks in the no change camp, as were we.

- So soon after the surprising change of the FinMin for the BI to cut in the face of limited need, especially when their currency is the worst performer in the region. The BI appears to be shifting from a strong emphasis on financial stability to a much more pro-growth bias/outlook.

- With 5-Yr CDS near tights, the potential for rallying from here seems limited.

SOUTH KOREA: Country Wrap: BOK Has Room to Focus on Domestic Factors

Market Summary: The KOSPI is up +1.13% to also reach a new high of 3,450 as the Won fell heavily by -0.64% to 1,385.30 and the yield curve steepened. The KTB 10-Yr is at 2.82%

- The ruling Democratic Party of Korea (DPK) is seeking to accelerate its push for “mutual growth” whereby banks and other financial services companies will bear greater social responsibility in the form of cash contributions and financial assistance packages, market watchers said Wednesday. (source Korea Times)

- The Federal Reserve's latest interest rate cut has created more room for the Bank of Korea (BOK) to focus its monetary policy more on domestic factors, the central bank said Thursday. BOK Deputy Gov. Park Jong-woo made the assessment while presiding over a market situation meeting earlier in the day, after the Fed lowered its benchmark rate by a quarter percentage point, its first rate cut this year, flagging slower job growth. (source Korea Times)

CHINA: Country Wrap: SOEs Performing Well

Market Summary: The Hang Seng is down marginally by -0.18% whilst the CSI 300 is up +0.32%, Shanghai up +0.45% and Shenzhen up +0.70%. The Yuan Reference Rate at 7.1085 Per USD; Estimate 7.1101 and bonds are steady with the CGB 10-Yr at 1.78%.

- China climbed one spot this year to enter the top 10 of the World Intellectual Property Organization's Global Innovation Index for the first time, reflecting the government’s strong emphasis on and support for intellectual property, according to a report released on Sept. 15. (source Yicai)

- China's centrally administered state-owned enterprises (SOEs) have achieved robust growth in both total assets and profits during the 14th Five-Year Plan period (2021-2025), according to the state assets regulator on Wednesday. (source Xinhua)

ASIA FX: USD Higher Against SEA, IDR Lower Post BI Cut, THB Down As Well

In SEA FX, the USD is biased higher in the first part of Thursday trade. US nominal Tsy yields have dipped slightly, but this follows late Wednesday gains (as Fed Chair Powell's comments around confidence in the economy drove moves, after the earlier FOMC 25bps cut). Note the US 10yr real yield ended Wednesday around 1.68%, so not making fresh lows, which has likely provided some dollar support against SEA FX.

- Outside of these broader US developments focus has been on local news flow. In Indonesia fallout is evident from yesterday's surprise BI cut. It appears that the central bank has become more focused on growth than FX developments with it saying its “decision is consistent with joint efforts to stimulate economic growth”. Spot USD/IDR has risen above 16500 (up +0.50%), which has been a firm resistance point since May of this year. No sign of BI intervention headlines yet, but this will be a watch point for markets.

- USD/THB is rising as well, last at 31.80/85, up around 0.35%. Recent highs rest at 31.965, whilst the 20-day EMA is around 32.03, while the 50-day EMA (which we have been above since April) is back at 32.285. Headlines crossed a short while ago - "THAI BAHT IS LIKELY TO RISE FURTHER DUE TO CAPITAL INFLOWS INTO BONDS AND STOCKS - INCOMING DEPUTY FINMIN and "*THAI NOMINATED FIN MIN EKNITI: PREPARES MEASURES TO MANAGE BAHT" - BBG. The incoming FinMin also stated that discussions have been held with the BoT. It remains to be seen what measures are announced, but for the moment it is providing caution on chasing USD/THB lower.

- USD/PHP has risen back above 57.00, off around 0.30% in PHP terms. We remain within recent ranges. From the central bank: "*BSP'S ABENOJA: WE MAY BE NEAR THE APPROPRIATE INTEREST RATES" - BBG.

- USD/MYR is also higher, but at 4.1960, remains sub the 4.2000 level. USD/GSD is back around 1.2800, which was a support zone recently, so may now act as a resistance point.

ASIA FX: USD Biased Higher, USD/KRW The Standout, Modest Moves Elsewhere

In North East Asia FX, the bias has also been for firmer dollar levels, although outside of USD/KRW, gains have been fairly modest.

- USD/CNH has been supported ahead of the 7.1000 level. The USD/CNY fix rose and the fixing error was only just negative (hence no bias for a meaningfully stronger yuan). Still we haven't gotten back above 7.1100 either. Onshore equities continue to rally. The CSI 300 up a further 0.20%. A modest gain, but underlying tech trends remain quite strong. China's move away from Nvidia chips is buoying sentiment in this space.

- Spot USD/KRW has push back above 1385, up around 0.50%, while the 1 month NDF has lost 0.35% in won terms. This fits with broader USD gains, particularly in the G10 space, where the likes of AUD and NZD have lost ground on poor local data outcomes. Local South Korean equities have risen, up over 1.2%, but this hasn't aided FX sentiment. The wedge between USD/KRW spot and the US-SK 1y1y rate differential has closed somewhat. This differential fell to lows around +51bps at the start of the month but is now around +61bps.

- Spot USD/TWD is higher, holding above 30.05, but this is less than a 0.1% gain at for the USD this stage. Local equities are up over 1%, while we also have the CBC decision later, which is expected to see policy rates left on hold at 2.00%.

- USD/HKD is down slightly, last around 7.7750. Headlines equities are weaker, but the tech sub index is still rallying, with potential inflows into this space aiding HKD sentiment.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 18/09/2025 | 0710/0910 | ECB Lagarde Video Message at Women Leadership Summit | ||

| 18/09/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 18/09/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/09/2025 | 0800/1000 | ECB de Guindos at MNI Connect Event | ||

| 18/09/2025 | 0900/1100 | ** | EZ Construction Output | |

| 18/09/2025 | 0945/1145 | ECB Schnabel Chairs Panel at ECB Research Conference | ||

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 18/09/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 18/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/09/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 18/09/2025 | 1915/1515 | BOC speech on payments ecosystem from director Ron Morrow. | ||

| 18/09/2025 | 2000/1600 | ** | TICS | |

| 19/09/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/09/2025 | 2330/0830 | *** | CPI | |

| 19/09/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 19/09/2025 | 0600/0700 | *** | Public Sector Finances | |

| 19/09/2025 | 0600/0700 | *** | Retail Sales | |

| 19/09/2025 | 0600/0800 | ** | PPI | |

| 19/09/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade |