ASIA FX: USD Higher Against SEA, IDR Lower Post BI Cut, THB Down As Well

In SEA FX, the USD is biased higher in the first part of Thursday trade. US nominal Tsy yields have dipped slightly, but this follows late Wednesday gains (as Fed Chair Powell's comments around confidence in the economy drove moves, after the earlier FOMC 25bps cut). Note the US 10yr real yield ended Wednesday around 1.68%, so not making fresh lows, which has likely provided some dollar support against SEA FX.

- Outside of these broader US developments focus has been on local news flow. In Indonesia fallout is evident from yesterday's surprise BI cut. It appears that the central bank has become more focused on growth than FX developments with it saying its “decision is consistent with joint efforts to stimulate economic growth”. Spot USD/IDR has risen above 16500 (up +0.50%), which has been a firm resistance point since May of this year. No sign of BI intervention headlines yet, but this will be a watch point for markets.

- USD/THB is rising as well, last at 31.80/85, up around 0.35%. Recent highs rest at 31.965, whilst the 20-day EMA is around 32.03, while the 50-day EMA (which we have been above since April) is back at 32.285. Headlines crossed a short while ago - "THAI BAHT IS LIKELY TO RISE FURTHER DUE TO CAPITAL INFLOWS INTO BONDS AND STOCKS - INCOMING DEPUTY FINMIN and "*THAI NOMINATED FIN MIN EKNITI: PREPARES MEASURES TO MANAGE BAHT" - BBG. The incoming FinMin also stated that discussions have been held with the BoT. It remains to be seen what measures are announced, but for the moment it is providing caution on chasing USD/THB lower.

- USD/PHP has risen back above 57.00, off around 0.30% in PHP terms. We remain within recent ranges. From the central bank: "*BSP'S ABENOJA: WE MAY BE NEAR THE APPROPRIATE INTEREST RATES" - BBG.

- USD/MYR is also higher, but at 4.1960, remains sub the 4.2000 level. USD/GSD is back around 1.2800, which was a support zone recently, so may now act as a resistance point.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Cheaper, Cons Conf Highest Since 2022

ACGBs (YM -5.0 & XM -6.0) are weaker and near session cheaps.

- Westpac's consumer confidence is trending towards the breakeven 100-level. Sentiment rose 5.7% m/m to 98.5 in August, the highest since February 2022, before the last tightening cycle began. The RBA's third rate cut this year on August 12 helped to boost confidence but the improvement was not just seen amongst mortgage holders. Governor Bullock also pointed out that further easing is consistent with inflation at the target mid-point.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest losses.

- Cash ACGBs are 5-6bps cheaper with the AU-US 10-year yield differential -1bps.

- The bills are -1 to -7, with the strip steeper.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in September is given a 27% probability, with a cumulative 34bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will be empty.

- This week, the AOFM plans to sell A$1500mn of the 1.25% 21 May 2032 bond on Wednesday and A$300mn of the 4.75% 21 June 2054 bond on Friday.

OIL: Crude Lower As Steps Taken Towards Peace In Ukraine

Oil prices have continued their downtrend after stabilising Monday after talks between Presidents Trump and Zelenskyy and European leaders appear to have been constructive with most sounding positive, although President Macron sounded sceptical that President Putin wants peace. A peace deal would likely result in an easing of sanctions on Russia which could see an increase in global oil supplies at a time of a significant market surplus.

- WTI is down 0.7% to $62.97/bbl (initial support at $61.94), close to the intraday low, while Brent is 0.6% lower at $66.17, above support at $65.01.

- A meeting between Zelenskyy and Putin could happen before the end of August with another including Trump to occur thereafter. He agreed that discussions of territory were between Ukraine and Russia, while security for Ukraine will principally be provided by Europe but the US will also be “involved” with Trump saying that “we’ll give them good protection”.

- US threats to impose punitive tariffs on those who buy Russian oil currently appear shelved but if that remains the case will depend on how Russia negotiates.

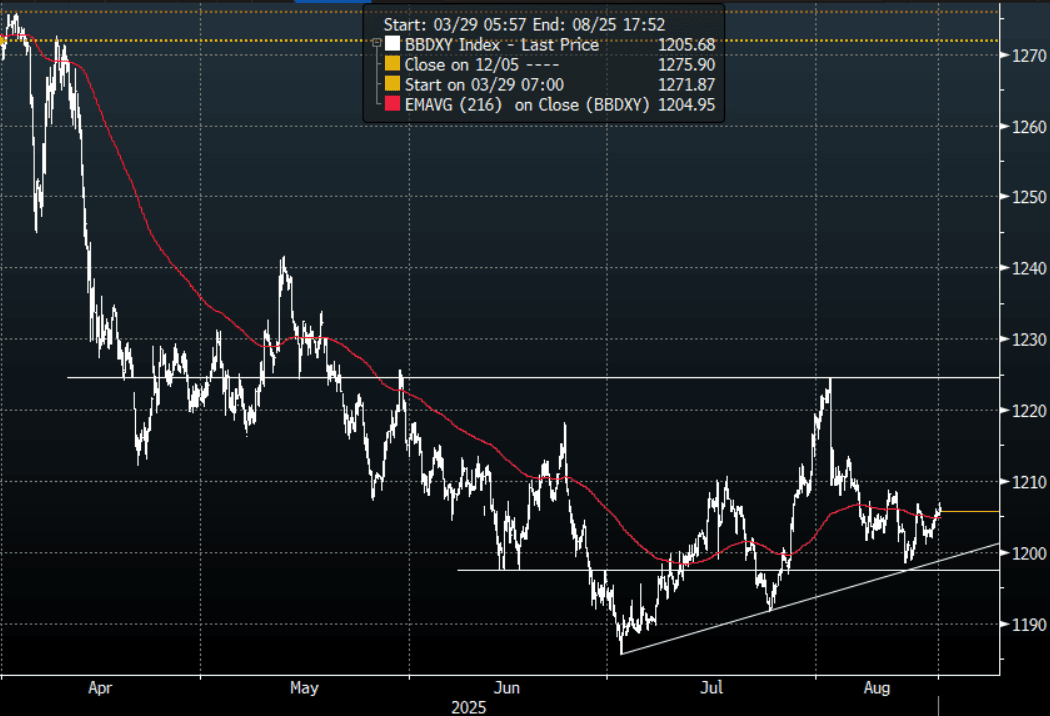

FOREX: Asia FX Wrap - USD Supported Into Jackson Hole

The BBDXY has had a range of 1205.00 - 1207.00 in the Asia-Pac session, it is currently trading around 1205, +0.05%. The USD found some demand as the market pares back some risk as we head into Jackson Hole at the end of the week. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows, but risk is more likely skewed to the USD shorts continuing to be reduced into Powell's speech.

- EUR/USD - Asian range 1.1639 - 1.1675, Asia is currently trading 1.1655. The market is trading sideways in a 1.1600-1.1750 range heading into Jackson Hole. The pair is unlikely to break out as await Powell's speech.

- GBP/USD - Asian range 1.3487 - 1.3514, Asia is currently dealing around 1.3500. Having broken back above its pivot look for dips to again be supported, first support seen now back towards 1.3400/1.3500.

- USD/CNH - Asian range 7.1854-7.1919, the USD/CNY fix printed 7.1359, Asia is currently dealing around 7.1860. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.20%, Gold $3337, US 10-Year 4.34%, BBDXY 1205, Crude Oil $62.95

- Data/Events : EZ ECB Current A/C, Italy Current A/C

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P