INDONESIA: BI Cuts In “Joint Effort” To Boost Growth

Bank Indonesia (BI) unexpectedly cut rates 25bp to 4.75%, the third consecutive monthly easing, which is unusual. It is especially surprising given it has intervened to defend the rupiah in the last few weeks due to political instability and previously emphasised the importance of FX and financial stability. President Prabowo has a growth target of 8% (Q2 GDP grew at 5.1% y/y) and BI may also be shifting more towards supporting the economy.

- BI’s accompanying statement added the phrase “joint efforts to stimulate economic growth”, which suggests that it may be supporting government policy.

- It has left its growth forecast unchanged for 2025 at “above the midpoint of the 4.6-5.4% range”. It does expect H2 2025 to improve due to the “strengthening policy synergy between Bank Indonesia and the Government”.

- BI will continue watching economic and price developments for opportunities to ease further assuming IDR stability. It will continue its macroprudential policies to boost lending, which it has been doing for some time.

- It noted that “economic growth in Indonesia must be increased in line with economic capacity” suggesting that it believes there is a negative output gap. It observes that consumption in Q3 is “restrained” given lower sentiment driven by a weaker labour market.

- It also mentioned that capex needs to be supported by “accelerating the realisation of various government priority programs”, which is an addition to the statement.

- USDIDR reached a peak of 16440 on Wednesday but finished down 0.1% at 16430. It peaked at 16498 following the replacement of Finance Minister Indrawati. With the Fed also cutting rates 25bp on Wednesday, the US-Indonesian rate differential held steady but at an 18 month low.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Crosses - Momentum Higher Stalls Approaching Jackson Hole

US equities traded sideways overnight, consolidating as the market awaits Powell's Jackson Hole speech. This morning US futures have seen very little movement, ESU5 -0.05%, NQU5 -0.05%. The JPY crosses momentum higher looks to have stalled for now.

- EUR/JPY - Overnight range 172.05 - 172.68, Asia is trading around 172.25. This pair is looking to regain momentum to challenge the year's highs, but with Jackson Hole approaching and risk being pared back that seems to have stalled for now.

- GBP/JPY - Overnight 199.39 - 200.27, Asia trades around 199.45. This pair failed once more to extend above 200 yet again. A sustained move back above 200.00 is needed to generate fresh impetus higher, but with risk being pared back it is doubtful it will see anything definitive until Jackson Hole is out the way.

- NZD/JPY - Overnight range 87.37 - 87.68, Asia is currently dealing 87.60. The pair found solid demand towards the 87.00 area, price looks comfortable back in the middle of its 96.50-99.00 range

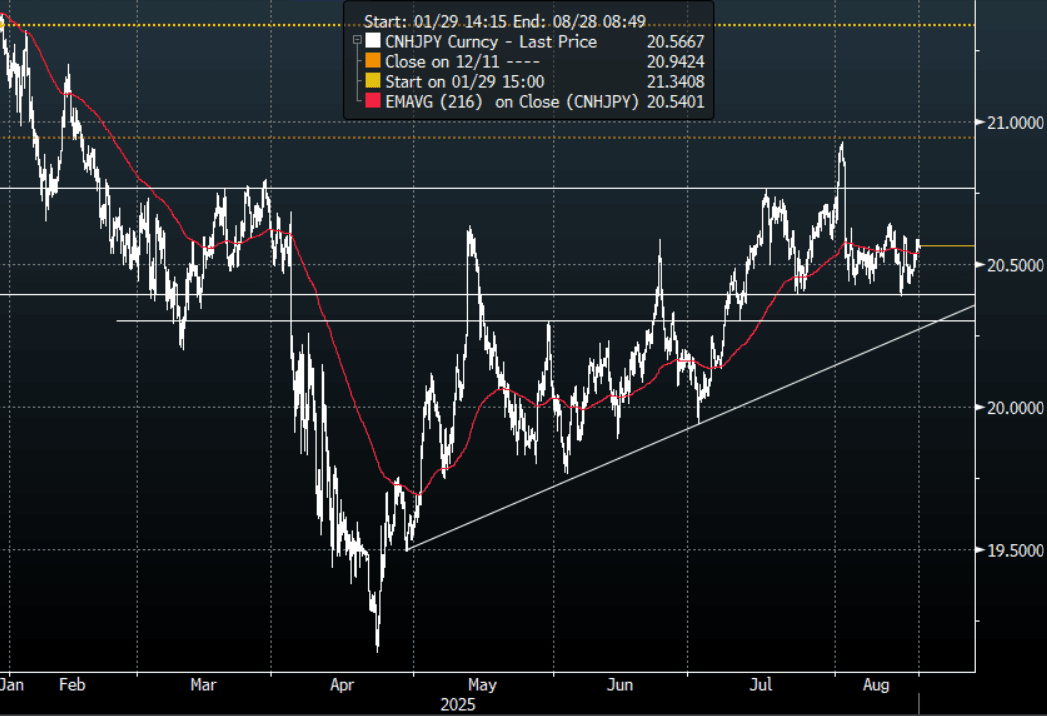

- CNH/JPY - Overnight range 20.4858 - 20.5888, Asia is currently trading around 20.5600. This pair continues to find solid demand back towards its pivotal support between 20.30/20.40. A sustained break back below 2.3000 is needed to turn momentum lower again, until then it looks comfortable in a 20.4000-20.8000 range.

Fig 1 : CNH/JPY 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

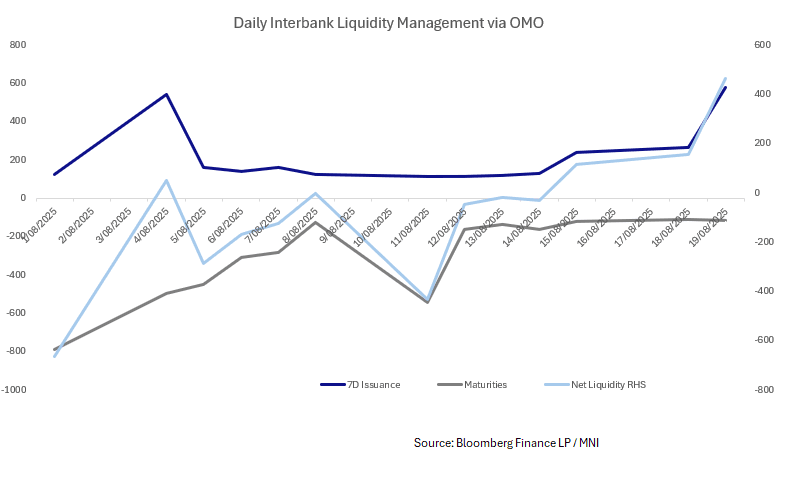

CHINA: Central Bank Injects CNY465.7bn via OMO

- The PBOC issued CNY580.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY114.6bn.

- Net liquidity injects CNY465.7bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.46%, from prior close of 1.51%.

- The China overnight interbank repo rate is at 1.54%, from the prior close of 1.45%.

- The China 7-day interbank repo rate is at 1.50%, from the prior close of 1.53%.

AUSSIE BONDS: Holding Cheaper, Cons Conf Surges After RBA Cut

ACGBs (YM -4.0 & XM -4.0) remain weaker after the negative lead-in from US tsys overnight.

- (Bloomberg) “Australia’s consumer confidence surged in August after the Reserve Bank cut interest rates for the third time this year and signaled further easing is likely. The data suggest “this long run of consumer pessimism may finally be coming to an end,” said Matthew Hassan, Westpac’s head of Australian macro forecasting. The prospect of further easing “looks to have reinforced consumer expectations that mortgage interest rates are headed lower, giving a broad-based boost to sentiment,” Hassan said.”

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest losses.

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential -2bps.

- The bills are -1 to -5, with the strip steeper.

- RBA-dated OIS pricing is mildly firmer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 35bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- This week, the AOFM plans to sell A$1500mn of the 1.25% 21 May 2032 bond on Wednesday and A$300mn of the 4.75% 21 June 2054 bond on Friday.