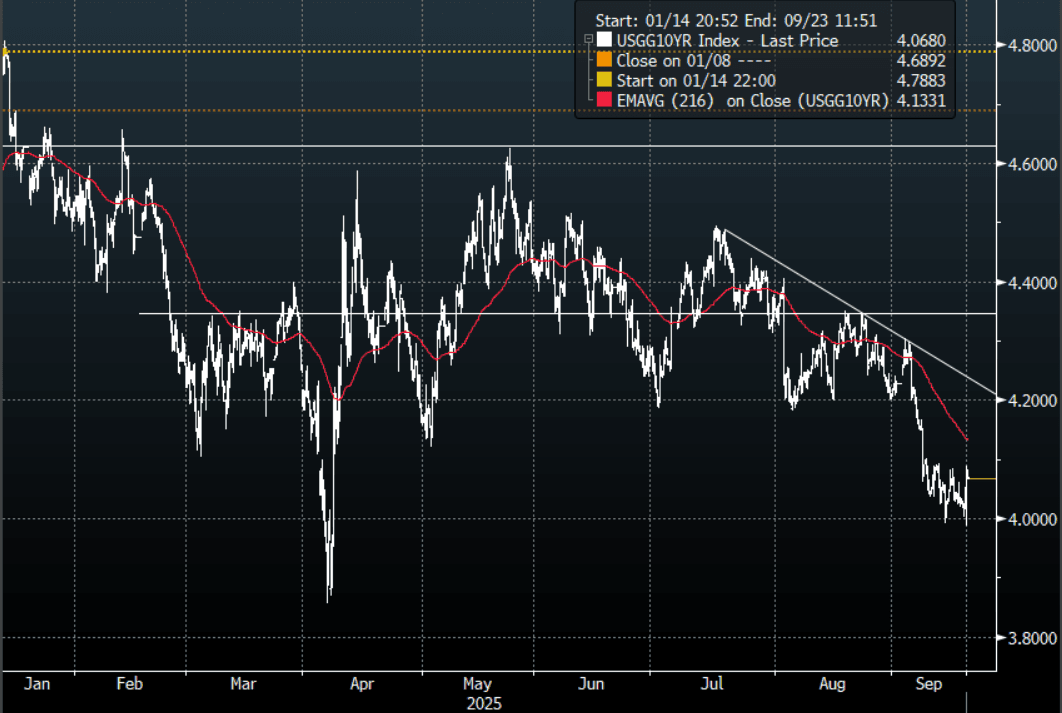

US TSYS: Asia Wrap - Yields Edge Lower

The TYZ5 range has been 113-00 to 113-07 during the Asia-Pacific session. It last changed hands at 113-06+, up 0-02 from the previous close.

- The US 2-year yield has edged lower trading 3.536%, down 0.02 from its close.

- The US 10-year yield has edged lower trading around 4.068%, down 0.02 from its close.

- (Bloomberg) -- The Federal Reserve’s first interest rate cut since December to shield the jobs market collides with a revision higher for its economic growth and inflation forecasts, leaving the central bank ever-more data dependent.

- RenMac on X: “We have two sided risks which means there is no risk free path.” The next two meetings should be priced closer to a coin flip for rate cuts.”

- Jim Bianco on X: “This meeting was a mess. One member of the FOMC thinks the Fed is going to HIKE rates this year. One (Stephen Miran) thinks it is going to cut 1.25% this year (5 cuts over two meetings). Add to this is Powell using the term "Risk Management" to describe this cut. If this is the case now, then the Fed cannot also be data dependent. Both cannot be true at the same time.”

- Data/Events: Initial Jobless Claims, Philadelphia Fed Business Outlook, Leading Index, Net Long-term TIC Flows

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Mixed Trends, Australia Underperforms, HK/China Holding Up

Asian markets are mixed in the first part of Tuesday trade, although aggregate moves for most markets are not much beyond 0.50% at this stage. US equity futures are down a touch, after little net change in cash trade on Monday. There have been a host of headlines related to Trump meeting with Ukraine President Zelenskyy and key EU leaders. Trump also spoke with Russian President Putin. Next steps will reportedly be a Putin/Zelenskyy meeting, although no time or place has been set yet. Broader market impact has been limited so far from these headlines.

- At the lunch time break, China and Hong Kong markets are a touch higher. The CSI is near 4245, as the onshore equity rally continues. The HSI is up just under 0.20%. Southbound stocks flows are firmer than yesterday but at this stage well short of the surge to record highs we saw last Friday.

- Onshore media also note the surge in retail accounts opened this year. "In the first seven months of 2025, 14.5 million new retail accounts were opened on the Shanghai Stock Exchange, a 37% year-over-year increase, according to exchange data" (per Securities Daily, via BBG).

- Japan markets are down slightly but the Topix is still above 3100 at this stage. South Korea's Kospi and the Taiex in Taiwan are both off by around 0.30% so far today.

- Australia's ASX 200 is down close to 0.80%, the worst performer in the region so far today. Weakness from CSL, post its full year results, have weighed. Commodity bellwether BHP also reported lower profits, although its share price is holding up.

- In South East Asia, Singapore and Malaysia are up around 0.50%, while the Philippines and Indonesia are down slightly. Indian markets are ticking up in the first part of trade, after solid gains on Monday.

AUD: Asia Wrap - AUD/USD Probes Below 0.6500

The AUD/USD has had a range of 0.6485 - 0.6497 in the Asia- Pac session, it is currently trading around 0.6490, -0.05%. US rates extended higher looking towards Powell's speech at Jackson Hole later in the week, this has seen the USD see some demand return as the market pares back risk going into it. The AUD continues to consolidate around 0.6500, firmly in the middle of its 0.6350-0.6650 range with no clear direction. Perhaps risks slightly skewed towards more USD short covering as we approach Jackson hole with the risk Powell is not as Dovish as the market.

- AU Data: Sentiment Improving Towards Neutral As Real Incomes Rise. Westpac’s consumer confidence is trending towards the breakeven 100-level. Sentiment rose 5.7% m/m to 98.5 in August, the highest since February 2022, before the last tightening cycle began. The RBA’s third rate cut this year on August 12 helped to boost confidence but the improvement was not just seen amongst mortgage holders. Governor Bullock also pointed out that further easing is consistent with inflation at the target mid-point.

- " Yuan May Strengthen Past 7 Per Dollar, Top China Economist Says. The yuan may see further gains past 7 against the dollar, according to a top Chinese economist, as debate grows among market participants over whether Beijing will allow it to appreciate." - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6515(AUD744m), 0.6390(AUD380m). Upcoming Close Strikes : 0.6500(AUD454m Aug 21), 0.6600(AUD1.34b Aug 21) - BBG

- CFTC Data shows Asset managers added to their shorts -67449(Last -60729), the Leveraged community though reduced their own shorts -10121(Last -13997).

- AUD/JPY - Asia-Pac range 95.81 - 96.10, Asia is trading around 96.05. The pair found good demand last week towards 95.50, price is now firmly back into the 94.50-97.50 range looking for clearer direction.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Asia Wrap - Yields Edge Higher In A Quiet Session

The TYU5 range has been 111-15 to 111-19+ during the Asia-Pacific session. It last changed hands at 111-16, down 0-00+ from the previous close.

- The US 2-year yield has edged higher trading around 3.77%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.34%, up 0.01 from its close.

- Yields extended higher overnight, probing the pivotal resistance area within the greater 4.10%-4.65% range. The 4.35% area in 10-Year yields should still see demand initially, but the way the market keeps bouncing off levels just below 4.20% will be disconcerting for longs.

- "S&P Affirms US ‘AA+/A-1+’ Sovereign Rtgs; Outlook Stable. "Outlook remains stable, reflecting expectation of continued resilience in the US economy Credible, effective monetary policy execution; high, but not rising, fiscal deficits that underpin the increase in net general government debt; and the $5 trillion increase in the debt ceiling. Sees net general government debt to approach 100% of GDP given structurally rising nondiscretionary interest and aging-related expenditure" via BBG

- Lance Roberts on X: “ While everyone is enamored with the bull market, the macro environment continues deteriorating. The IMF expects economic growth in the US to be below 2% and the Eurozone at 1% next year. Which is why Central Banks have been cutting rates at the fastest pace since 2020.”

- Data/Events: Housing Starts, Building Permits