ASIA STOCKS: Global Tech Rally Benefits Asia

The global tech rally continues to support key markets in Asia with the Hang Seng Tech and the KOSDAQ up strongly. Chip related stocks were strong in Hong Kong following a regulatory ban on Nvidia, boosted expectations for growth for Chinese tech companies.

- The Hang Seng is down marginally by -0.18% whilst the CSI 300 is up +0.32%, Shanghai up +0.45% and Shenzhen up +0.70%.

- The NIKKEI is up +1.3% today, hitting new all time highs of 45,383.

- The KOSPI is up +1.13% to also reach a new high of 3,450.

- The FTSE Malay KLCI is down -0.81%, taking back all of yesterday's gains.

- The Jakarta Comp roared with the unexpected BI rate cut and is up at new all time highs of 8,046.

- The NIFTY 50 has opened Thursday strongly up +0.33% and has produced positive gains for the 17 of 19 last trading days.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

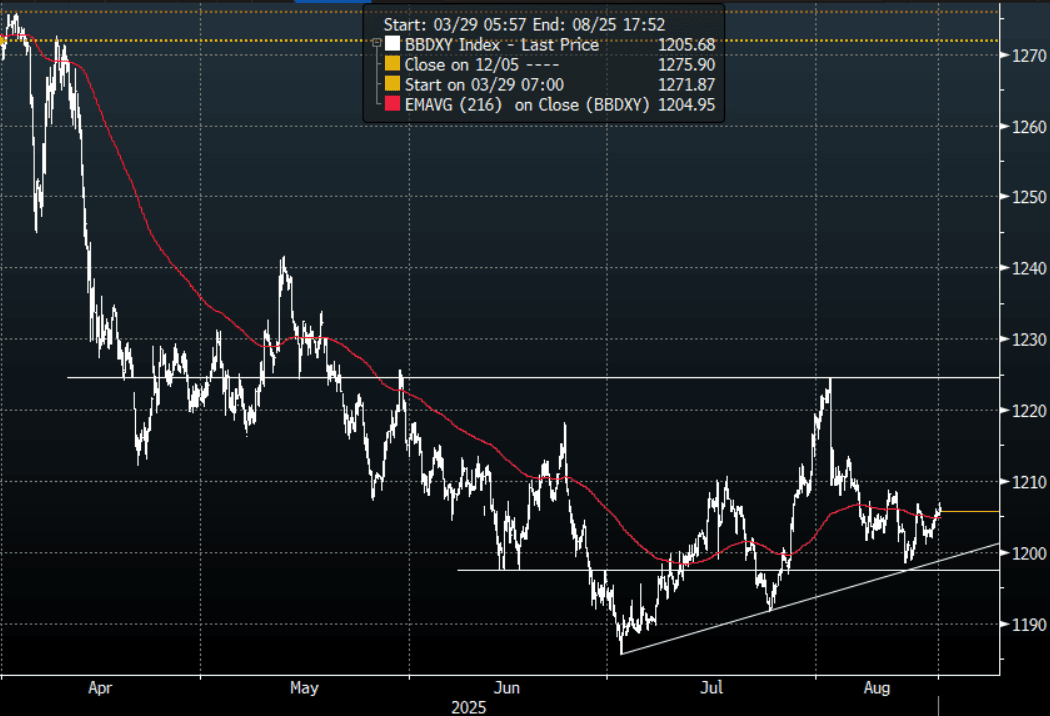

FOREX: Asia FX Wrap - USD Supported Into Jackson Hole

The BBDXY has had a range of 1205.00 - 1207.00 in the Asia-Pac session, it is currently trading around 1205, +0.05%. The USD found some demand as the market pares back some risk as we head into Jackson Hole at the end of the week. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows, but risk is more likely skewed to the USD shorts continuing to be reduced into Powell's speech.

- EUR/USD - Asian range 1.1639 - 1.1675, Asia is currently trading 1.1655. The market is trading sideways in a 1.1600-1.1750 range heading into Jackson Hole. The pair is unlikely to break out as await Powell's speech.

- GBP/USD - Asian range 1.3487 - 1.3514, Asia is currently dealing around 1.3500. Having broken back above its pivot look for dips to again be supported, first support seen now back towards 1.3400/1.3500.

- USD/CNH - Asian range 7.1854-7.1919, the USD/CNY fix printed 7.1359, Asia is currently dealing around 7.1860. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.20%, Gold $3337, US 10-Year 4.34%, BBDXY 1205, Crude Oil $62.95

- Data/Events : EZ ECB Current A/C, Italy Current A/C

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Closed Cheaper Ahead Of Tomorrow’s RBNZ Policy Decision

NZGBs closed near session cheaps, with benchmark yields 4bps higher.

- The RBNZ meets on Wednesday, August 30 and is likely to cut rates 25bp to 3.0%, the mid-point of its estimated "neutral" range. While it paused at the July meeting, it was with a clear easing bias.

- With the cut widely forecast, attention will be on the revised RBNZ outlook and tone of the statement and press conference. The focus is likely to be on the projected OCR path and whether it is revised lower, suggesting further easing towards stimulatory territory as excess capacity persists.

- With the focus on the medium-term, the 2026 and beyond inflation forecasts will be the important ones and should remain around the 2% band mid-point. See MNI Preview here:

- On Thursday, Governor Hawkesby will appear before a parliamentary committee to talk about the latest Monetary Policy Statement.

- Swap rates are 5-6bps higher.

- RBNZ dated OIS pricing closed firmer across meetings. 23bps of easing is priced for tomorrow, with a cumulative 39bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

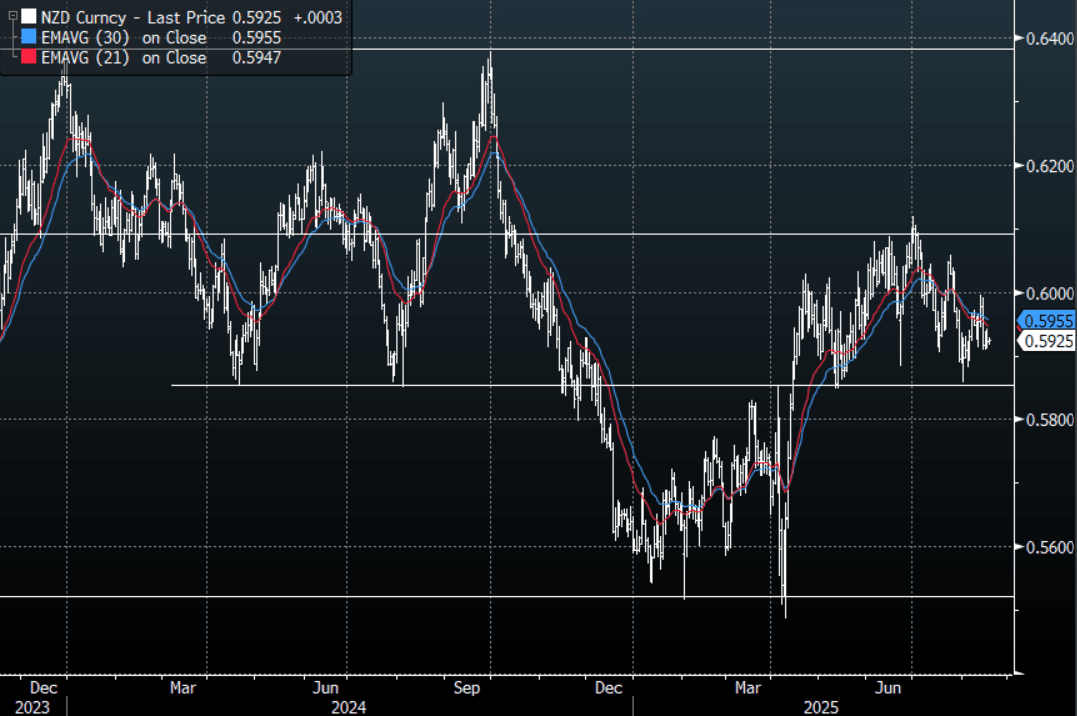

NZD: Asia Wrap - NZD/USD Consolidates Above 0.5900

The NZD/USD had a range of 0.5917 - 0.5929 in the Asia-Pac session, going into the London open trading around 0.5925, +0.05%. US rates extended higher looking towards Powell's speech at Jackson Hole later in the week, this has seen the USD see some demand return as the market pares back risk going into it. The NZD/USD again found some demand back towards 0.5900 and is consolidating just above there. While still firmly in the 0.5850-0.6150 range it's tough to discern any real direction, though risks are slightly skewed to more USD upside as positions are lightened heading in Jackson Hole. Risk has traded a little lower this morning, E-minis -0.20%, NQU5 -0.25%.

- MNI RBNZ Preview-August 2025: Rate Cut, Focus On OCR Path. The RBNZ meets tomorrow and is likely to cut rates 25bp to 3.0%, the mid-point of its estimated "neutral" range. While it paused at the July meeting, it was with a clear easing bias.

- With the cut widely forecast, attention will be on the revised RBNZ outlook and tone of the statement and press conference. The focus is likely to be on the projected OCR path and whether it is revised lower suggesting further easing towards stimulatory territory as excess capacity persists.

- With the focus on the medium-term, the 2026 and beyond inflation forecasts will be the important ones and should remain around the 2% band mid-point.

- RBNZ-dated OIS pricing is slightly firmer across meetings with 23bps of easing priced for tomorrow’s meeting, with a cumulative 41bps by November 2025.

- “NZ 2Q PRODUCER OUTPUT PRICES RISE 0.6% Q/Q" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5925(NZD400m Aug 20), 0.5980(NZD660m Aug 21). - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short adding slightly in the NZD -3679(Last -1811), the Leveraged community though reduced their own shorts slightly -4190(Last -6778).

- AUD/NZD range for the session has been 1.0952 - 1.0974, currently trading 1.0955. The Cross is trying to push higher but continues to stall back towards 1.1000 and will need a sustained break here to potentially extend. Until then the range looks to be 1.0850-1.1000.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P