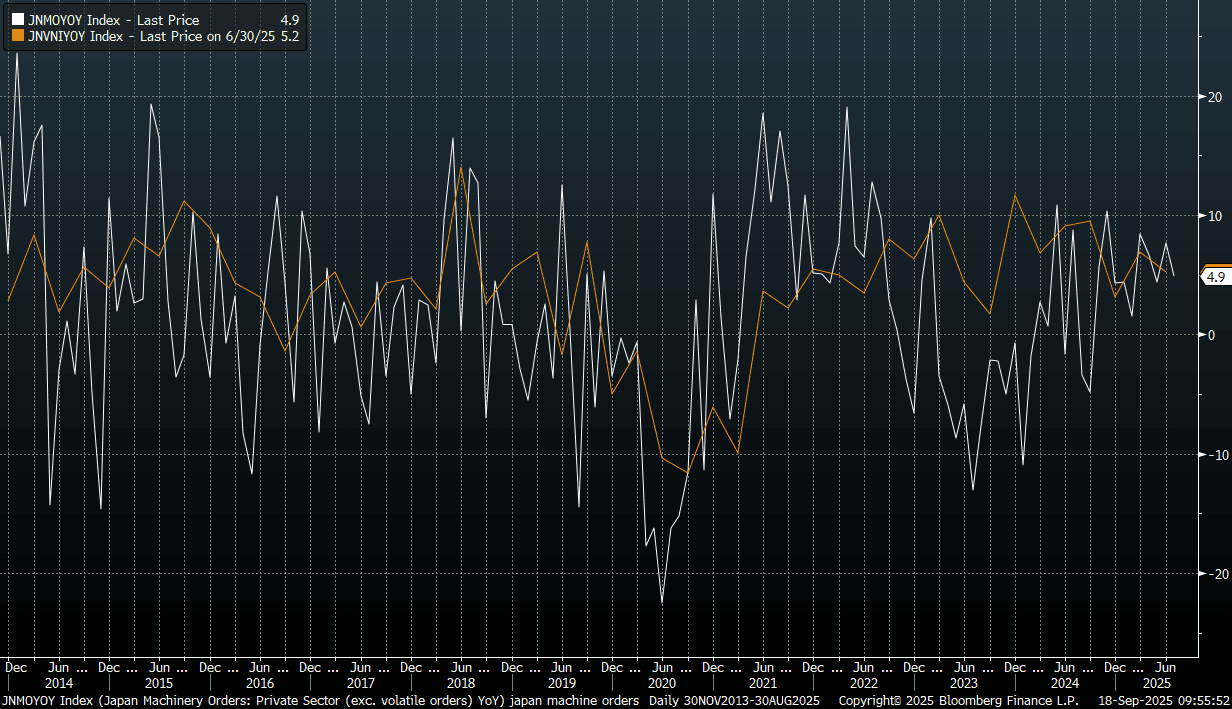

JAPAN DATA: July Core Machine Orders Below Forecasts, Y/Y Momentum Holding Up

Japan July core machine orders printed below forecasts. We fell 4.6%m/m in July against a -1.5% forecast (and after a 3.0% rise in June). In y/y terms we rose 4.9%, against a 5.2% forecast and 7.6% gain in June. The chart below shows core machine orders against capex for Japan, both in y/y terms. We are off recent highs, but the July machine orders update is not pointing to sharp weakening in y/y momentum.

- In terms of the detail, government/public machine orders were up 21.3%m/m, but this segment is very volatile. Manufacturing and non-manufacturing both recorded rises in the month, but this was likely due to volatile components, which are excluded from the core machine headline outcome.

Fig 1: Japan Core Machine Orders & Capex Y/Y

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open

TYU5 is trading 111-17+, up 0-01 from its close.

- The US 2-year yield opens around 3.76%.

- The US 10-year yield opens around 4.334%.

- (Bloomberg) - The air has started to seep out of the rate-cut-hope balloon, with a September cut now about 80% priced in. One more hot inflation (or consumer) print is all it will take to get us back to even odds, roiling bonds again. Deutsche Bank, for one, titled their recent note “Jury still out on September rate cut, but 50bps definitely out.”

- MNI US DATA: NY Fed Services Activity Sags As Sellers Hike Prices To Buoy Margins. The NY Fed's survey of regional services firms' business leaders showed a deterioration in activity and forward-looking sentiment in August, with inflation pressures remaining prevalent. The current general activity index fell for the first time since March, to -11.7 from -9.3 prior, with the business climate likewise worsening to -39.3 from -34.6. These are still better than the historically bad readings in April's survey amid heightened sensitivity to tariff-related news, but firmly negative by historical standards.

- Yields extended higher overnight, probing the pivotal resistance area within the greater 4.10%-4.65% range. The 4.35% area in 10-Year yields should still see demand initially, but the way the market keeps bouncing off levels just below 4.20% will be disconcerting for longs.

- Data/Events: Housing Starts, Building Permits

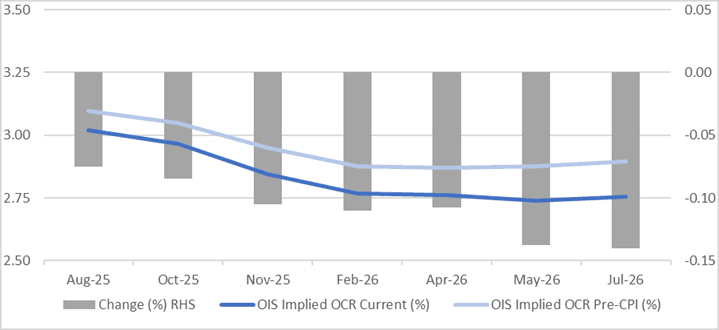

STIR: RBNZ-Dated OIS Softer Than Pre-CPI Levels Ahead Of RBNZ Decision

RBNZ-dated OIS pricing is slightly firmer across meetings ahead of tomorrow’s RBNZ Policy Decision.

- 23bps of easing is priced for tomorrow’s meeting, with a cumulative 41bps by November 2025.

- Notably, pricing is 8-14bps softer across meetings versus late July’s pre-CPI levels.

- NZ CPI rose less than economists expected in Q2. Headline CPI rose 0.5% q/q 2.7% y/y (estimate +0.6% and 2.8%). Tradeables rose 0.3% q/q, less than forecast, while non-tradeables were in line at 0.7% q/q.

Figure 1: RBNZ Dated OIS Current vs. Pre-CPI (%)

Source: Bloomberg Finance LP / MNI

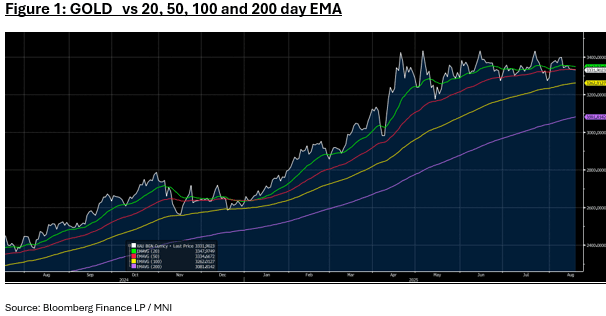

GOLD: Gold Quiet Ahead of Jackson Hole

- Gold tread water overnight finishing unchanged at US$3,332.95.

- As the Federal Reserve's annual get together at Jackson Hole nears, the gold market will be anxiously looking for signals on monetary policy.

- From Friday, the FED hosts Central Bankers from major central banks globally and with markets predicting an upcoming rate cut, they will be pouring over any comments to re-affirm that view.

- The Fed’s Raphael Bostic was quoted as saying that he is open to a cut in rates soon, noting that tariffs are creating pressures and that business profits could benefit from lower rates.

- Gold has opened weaker in the Asia trading day and attempting to hold below the 50-day EMA of $3,334.67. Below sits the 100-day EMA of $3,262.00.

- Exchange-traded funds added 147,088 troy ounces of gold to their holdings in the last trading session, bringing this year's net purchases to 9.28 million ounces, 11% higher according to BBG.