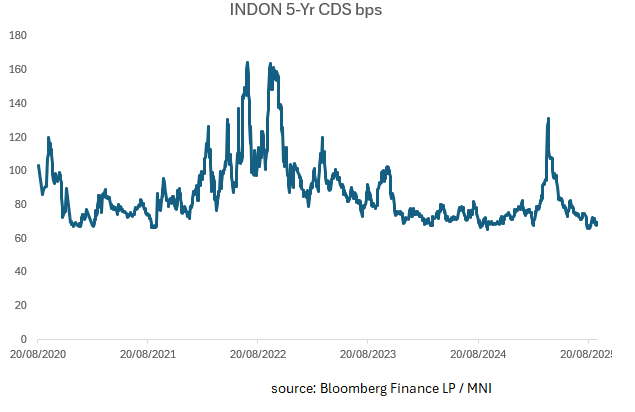

INDONESIA: Case for Further CDS Tightening Seems Limited

Sep-18 01:28

- The performance of the INDON 5-Yr CDS since April has been remarkable, tightening from the wides of +131bps to a low of +66bps in August.

- With the new FinMin seemingly underwriting the President's ambitious growth targets, we highlighted recently that the options available are walking away from the deficit cap of 3% and or lower rates.

- The new FinMin has already made some policy adjustments withdrawing US$12bn equivalent from the Central Bank and distributing to the state owned banks with instructions to lend. he FinMin has indicated that the new Sovereign Wealth Fund Danantara will be used increasingly to help achieve the growth targets.

- However, it seems unlikely that Danantara and increased lending alone will supersize growth. Government spending must rise, which creates risk of challenging the deficit cap (3% of GDP).

- Central Bank rates may need to be cut yet at this point, the Bank Indonesia remains ' independent '. Yet the idea of independence may now be in question following the BI's surprise cut in rates overnight. Only 2 of 38 forecasts on BBG suggested a cut with the main Indonesian banks in the no change camp, as were we.

- So soon after the surprising change of the FinMin for the BI to cut in the face of limited need, especially when their currency is the worst performer in the region. The BI appears to be shifting from a strong emphasis on financial stability to a much more pro-growth bias/outlook.

- With 5-Yr CDS near tights, the potential for rallying from here seems limited.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Crosses - Momentum Higher Stalls Approaching Jackson Hole

Aug-19 01:26

US equities traded sideways overnight, consolidating as the market awaits Powell's Jackson Hole speech. This morning US futures have seen very little movement, ESU5 -0.05%, NQU5 -0.05%. The JPY crosses momentum higher looks to have stalled for now.

- EUR/JPY - Overnight range 172.05 - 172.68, Asia is trading around 172.25. This pair is looking to regain momentum to challenge the year's highs, but with Jackson Hole approaching and risk being pared back that seems to have stalled for now.

- GBP/JPY - Overnight 199.39 - 200.27, Asia trades around 199.45. This pair failed once more to extend above 200 yet again. A sustained move back above 200.00 is needed to generate fresh impetus higher, but with risk being pared back it is doubtful it will see anything definitive until Jackson Hole is out the way.

- NZD/JPY - Overnight range 87.37 - 87.68, Asia is currently dealing 87.60. The pair found solid demand towards the 87.00 area, price looks comfortable back in the middle of its 96.50-99.00 range

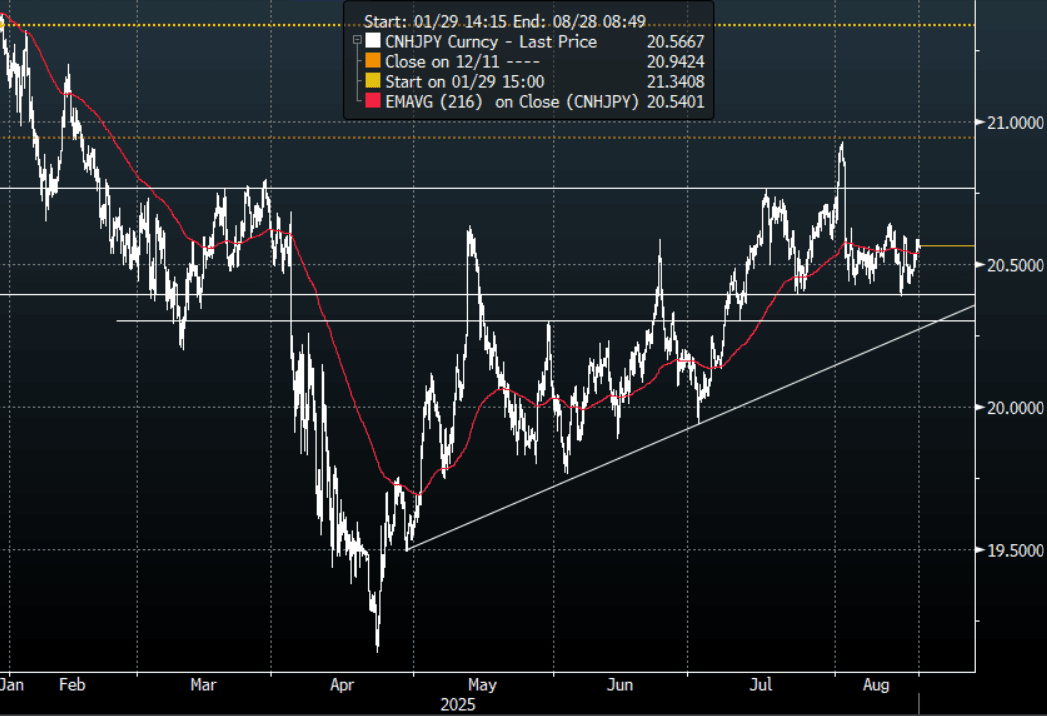

- CNH/JPY - Overnight range 20.4858 - 20.5888, Asia is currently trading around 20.5600. This pair continues to find solid demand back towards its pivotal support between 20.30/20.40. A sustained break back below 2.3000 is needed to turn momentum lower again, until then it looks comfortable in a 20.4000-20.8000 range.

Fig 1 : CNH/JPY 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

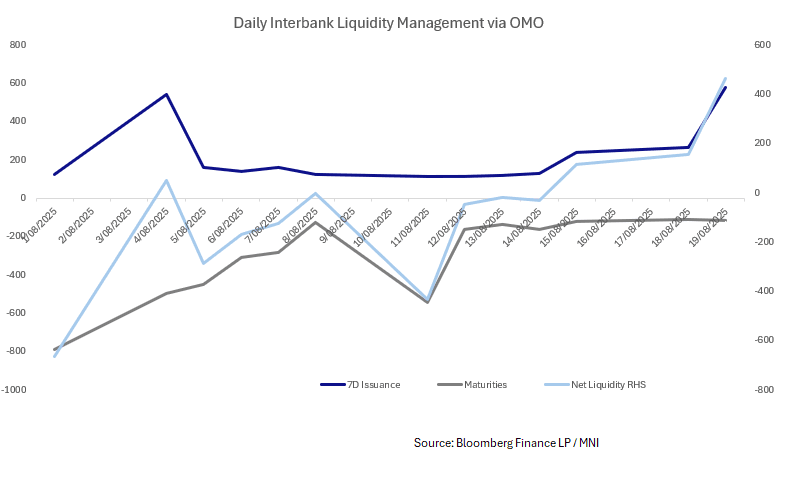

CHINA: Central Bank Injects CNY465.7bn via OMO

Aug-19 01:25

- The PBOC issued CNY580.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY114.6bn.

- Net liquidity injects CNY465.7bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.46%, from prior close of 1.51%.

- The China overnight interbank repo rate is at 1.54%, from the prior close of 1.45%.

- The China 7-day interbank repo rate is at 1.50%, from the prior close of 1.53%.

AUSSIE BONDS: Holding Cheaper, Cons Conf Surges After RBA Cut

Aug-19 01:22

ACGBs (YM -4.0 & XM -4.0) remain weaker after the negative lead-in from US tsys overnight.

- (Bloomberg) “Australia’s consumer confidence surged in August after the Reserve Bank cut interest rates for the third time this year and signaled further easing is likely. The data suggest “this long run of consumer pessimism may finally be coming to an end,” said Matthew Hassan, Westpac’s head of Australian macro forecasting. The prospect of further easing “looks to have reinforced consumer expectations that mortgage interest rates are headed lower, giving a broad-based boost to sentiment,” Hassan said.”

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest losses.

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential -2bps.

- The bills are -1 to -5, with the strip steeper.

- RBA-dated OIS pricing is mildly firmer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 35bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- This week, the AOFM plans to sell A$1500mn of the 1.25% 21 May 2032 bond on Wednesday and A$300mn of the 4.75% 21 June 2054 bond on Friday.