NEW ZEALAND: Very Weak Growth Increases Chance Of Larger Rate Cut

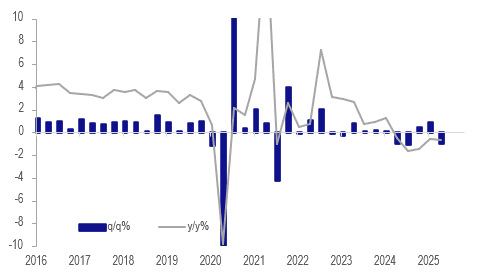

Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. With two votes for a 50bp cut in August, the risk of a larger move before year end is material.

NZ GDP y/y% production

- Statistics NZ reported that 10 out of 16 industries contracted in Q2 with manufacturing the largest falling 3.5% q/q. Construction was down 1.8% q/q with the sector continuing to struggle.

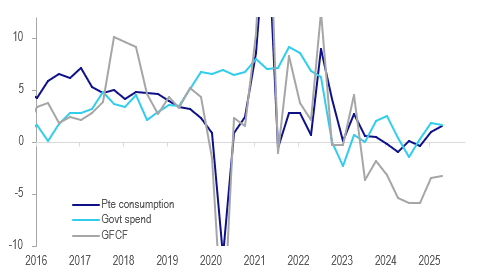

- Private and government consumption were the only positives in the expenditure measure of GDP rising 0.4% q/q and 0.1% q/q respectively. Household spending is gradually recovering with higher durables & non-durables, Q2 the third consecutive increase and the annual rate up to 1.5% from 1.0% and -1.0% a year ago.

- GFCF fell 1.1% q/q, the seventh quarterly decline in the last 2 years, with residential building down 1.9% q/q and other assets -0.9% q/q. GFCF is down 3.2% y/y after -3.4% in Q1.

- Goods & services exports fell 1.2% q/q to be up 0.7% y/y (Q1 3.6%) with goods down 2.6% q/q, driven by dairy & meat, and services -1.1% q/q. Imports rose 0.6% q/q driven by a 4.2% q/q increase in services.

NZ domestic demand y/y%

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Weaker Overnight, Peace Talks In Focus

In post-Tokyo trade, JGB futures closed weaker, -11 compared to settlement levels, with US tsys finished slightly weaker after an extremely subdued NY session.

- Attention was on the White House meeting on Ukraine, with President Trump hosting President Zelensky, Chancellor Merz, President Macron, Prime Ministers Starmer, Prime Minister Meloni, President Stubb, NATO Secretary General Rutte, and EC President Ursula von der Leyen.

- The upcoming Jackson Hole speech from Fed Chair Powell on Friday is muting activity too, as analysts wait for signals on a September rate cut.

- "As Jackson Hole steams into view, the bar for dovish rhetoric is high, lending a crucial pillar of support to the listless greenback. After a historically rough first half, the dollar has steadied and is drifting as expectations for Fed easing fluctuate. " – BBG

- (Bloomberg) -- Japan's auction of 20-year government bonds on Tuesday will be closely watched as the risk of a government spending surge weighs on investor appetite for super-long debt. The nation's longer-maturity bonds have been in sharp focus after the ruling coalition lost its majority at last month's upper house election.

- The local calendar will see 20-year supply.

AUSSIE BONDS: Cheaper, Another Light Data Calendar

ACGBs (YM -3.0 & XM -3.5) are weaker after US tsys finished mildly weaker on Monday.

- Limited data: August's NAHB/Wells Fargo Housing Market report showed little improvement in the homebuilding sector, with present sales weakening modestly and selling prospects steady/moderately better. The headline index fell 1 point to 32 - reverting back to June's level, which is around post-2022 lows.

- The NY Fed's survey of regional services firms' business leaders showed a deterioration in activity and forward-looking sentiment in August, with inflation pressures remaining prevalent. The current general activity index fell for the first time since March, to -11.7 from -9.3 prior.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential -3bps.

- The bills are -1 to -4, with the strip steeper.

- RBA-dated OIS pricing is mildly firmer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 36bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Today, the local calendar will see Westpac Consumer Confidence.

- This week, the AOFM plans to sell A$1500mn of the 1.25% 21 May 2032 bond on Wednesday and A$300mn of the 4.75% 21 June 2054 bond on Friday.

BONDS: NZGBS: Slightly Cheaper With US Tsys, RBNZ Decision Tomorrow

In local morning trade, NZGBs are 2bps cheaper after US tsys finished mildly weaker on Monday.

- August's NAHB/Wells Fargo Housing Market report showed little improvement in the homebuilding sector, with present sales weakening modestly and selling prospects steady/moderately better.

- Producer output prices rose 0.6% q/q in 2Q, while producer input prices rose 0.6% q/q.

- (MNI) RBNZ Decision - The RBNZ meets tomorrow and is likely to cut rates 25bp to 3.0%, the mid-point of its estimate of "neutral", after pausing at the July meeting. With measures of core inflation within the 1-3% target band, wages moderating and activity remaining subdued, the MPC is likely to determine that further easing is needed. It will also publish a revised outlook.

- The RBNZ will also release updated forecasts, and Governor Hawkesby will hold a press conference. On Thursday, he will appear before a parliamentary committee to talk about the latest Monetary Policy Statement.

- Swap rates are 2bps higher.

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for tomorrow, with a cumulative 41bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.