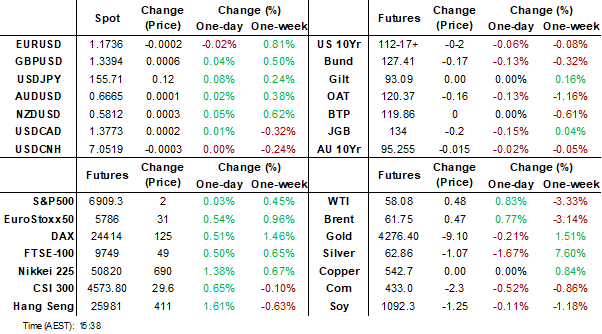

MNI EUROPEAN MARKETS ANALYSIS: USD Holding Lower For The Week

- The USD index is marginally up from recent lows, but still holding the bulk of its weekly loss. G10 FX trends have been relatively steady so far in Friday trade, likewise for US yields.

- Expectations for a 25bp rate hike (from 0.50% to 0.75%) at the BOJ's December 18-19 meeting have strengthened over the past week. New Zealand data today was encouraging for Q4 growth momentum, particularly in terms of consumer spending.

- Looking ahead, we have UK data, including Oct monthly GDP. German and French final CPI outcomes for Nov are also out.

MARKETS

US TSYS: Yields Mixed as TYH6 Fails Key Resistance

US 10-Yr bond futures are down -02+ to 112-12 in Friday afternoon trade, having reached a high of 112-14+ earlier. In a light volume trading day the US 10-Yr attempted to break above the 100-day EMA of 112-14+ only to fail and fall back below. Downside resistance is at 111-30 being the 200-day EMA.

Cash markets were mixed Friday during the Asian trading day with the long end underperforming. There is no auctions tonight and bond markets may likely remain subdued as it looks ahead to next week's data releases.

- The 2-Yr is at 3.528% down -1.4bps today. Range for the week 3.52% - 3.61%

- The 5-Yr is at 3.724% down -1.2bps today. Range for the week 3.72% -3.75%

- The 10-Yr is at 4.158% unchanged today. Range for the week 4.15% - 4.19%

- The 30-Yr is at 4.808% up +0.6bps today. Range for the week 4.78% - 4.80%

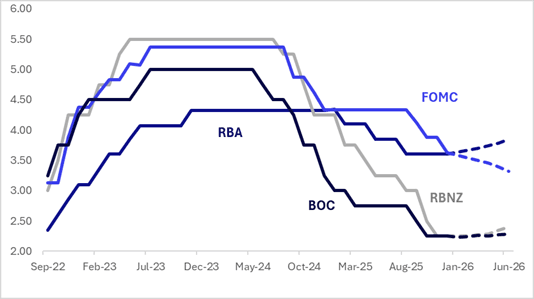

STIR: $-Bloc Pricing Firms Over The Week Despite Few Surprises From CB Decisions

Interest rate expectations across the $-bloc firmed over the past week out to June 2026, led by New Zealand (+18bps) and Canada (+12bps), while Australia firmed by 7bps and the US edged higher by 4bps.

- The main events over the past week were the central bank meetings in Australia, the US and Canada.

- The RBA left the cash rate at 3.60%, as widely expected, but signalled that inflation risks have shifted to the upside. The Board did not consider rate cuts and does not expect them in the foreseeable future. While it did not explicitly consider a rate hike, it discussed circumstances under which one might be needed.

- The FOMC delivered what was widely anticipated to be a “hawkish cut” at the December meeting, lowering the Funds rate range by 25bp to 3.50%-3.75% while portraying a cautious stance on further adjustments in the Statement and Dot Plot. But with most of the main communications having been well-anticipated, the meeting outcome brought some slight dovish surprises and a concomitant market reaction.

- The BOC left the key rate unchanged at 2.25%. Governor Macklem said the economy had beaten some of the dire scenarios officials and investors had laid out earlier this year as the US imposed tariffs. Officials will be "symmetric" in reviewing potential shocks that could motivate the next rate change, he said.

- The next key regional events are the FOMC and BoC on January 28. The market assigns just a 2% chance of a 25bps cut by the BoCin January, while the US market is 23% priced.

- Looking ahead to June 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.32%, -31bps; Canada (BOC): 2.29%, +4bp; Australia (RBA): 3.85%, +25bps; and New Zealand (RBNZ): 2.46%, +21bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

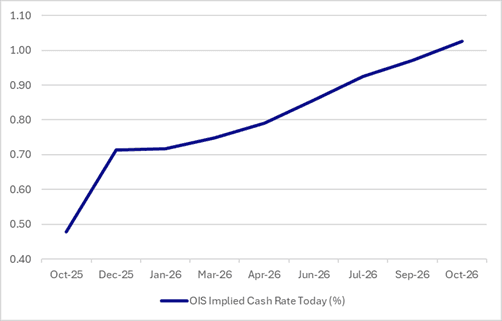

STIR: BoJ Hike 94% Priced For Next Week With Two By September-2026

Expectations for a 25bp rate hike (from 0.50% to 0.75%) at the BOJ's December 18-19 meeting have strengthened over the past week.

- In early December, BOJ Governor Kazuo Ueda said that even if the policy rate were raised to 0.75% from 0.50%, overall financial conditions would remain accommodative.

- When asked about the merits of a rate increase and the likelihood of a move this month, Ueda did not shy away from discussing specifics — including the probability of a hike — during that press conference.

- BOJ-dated OIS currently assigns an 94% probability to a 25bp hike in December, rising to 108% by March 2026. As recently as 21 November, markets saw less than a 20% chance of a December move.

- Notably, investors are now pricing in two 25bp hikes by September 2026.

Figure 1: BoJ-Dated OIS – Today

Source: Bloomberg Finance LP / MNI

JGBS: Twist-Flattener With Mkt Convinced A Hike Is Coming Next Week

JGB futures are weaker and near session lows, -16 compared to settlement levels.

- Expectations for a 25bp rate hike (from 0.50% to 0.75%) at the BOJ’s December 18–19 meeting have strengthened over the past week. Governor Ueda signalled earlier this month that the Bank may be ready to move, shortly after the yen fell to a 10-month low against the dollar, heightening concerns about imported inflation. Nearly two-thirds of analysts surveyed by Bloomberg expect the BOJ to lift rates roughly every six months from this month onward, with the median terminal rate for the cycle forecast at 1.25%.

- Markets now assign a 94% probability to a hike next week, with another increase priced in by September 2026 (see chart).

- (Bloomberg) The Topix financials gauge is heading for its highest close this century, with investors convinced a BOJ interest-rate hike is a done deal for next week.

- Cash US tsys are 1bp richer to 1bp cheaper, with a steepening bias, in today's Asia-Pac session.

- Cash JGBs have twist-flattened across benchmarks, with yields 1.5bps higher (10-year) to 4.5bps lower (30-year).

- Swap rates are 2bps higher to 1bp lower, with a flatter curve.

- On Monday, the local calendar will see the Tankan Survey and the Tertiary Industry Index.

Source: Bloomberg Finance LP / MNI

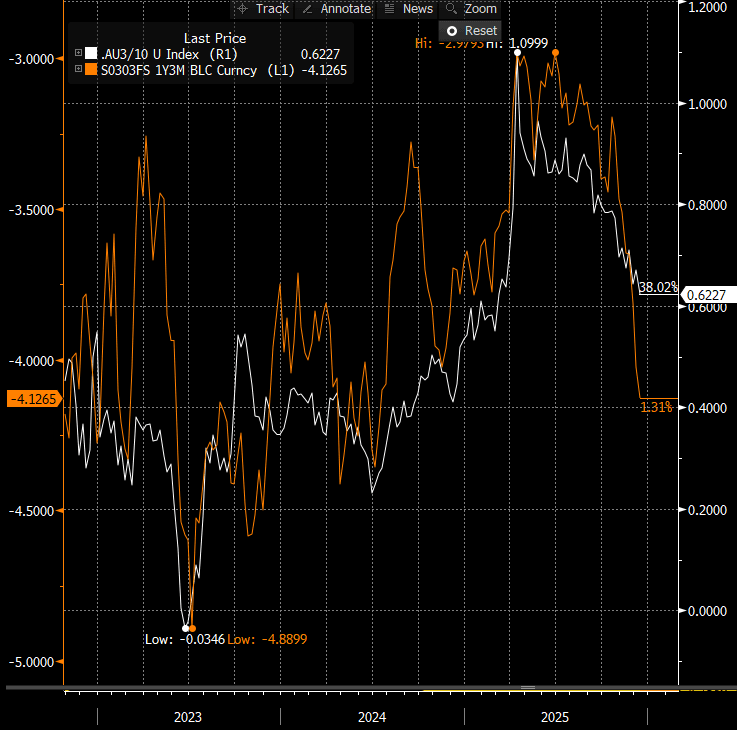

AUSSIE BONDS: Slightly Cheaper After A Subdued Data-Light Session

ACGBs (YM -0.5 & XM -2.0) are slightly weaker after a subdued session.

- Cash US tsys are 1bp richer to 1bp cheaper, with a steepening bias, in today's Asia-Pac session.

- Cash ACGBs are flat to 2bps cheaper, and the AU–US 10-year yield differential is at +58bps, near its widest level since mid-2022. A simple regression of the 10-year spread against the AU–US 1-year forward 3-month swap rate (1Y3M) differential over the past two years indicates that the current level is broadly in line with fair value.

- The 3/10 curve sits at its flattest since March. The recent curve flattening has occurred alongside a steady rise in market forward expectations for the RBA cash rate. A simple regression of the 3s/10s curve against the 1Y3M rate over the past three years suggests the current curve is roughly 20bps too steep relative to its fair value (see chart).

- The bills strip has twist-flattened, with pricing -2 to +2.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 31% for February to 99% by June and 166% by December 2026.

- On Monday, the local calendar will be empty.

- Next week, the AOFM plans to sell A$X1000mn of the 4.25% 21 October 2036 bond on Wednesday.

Bloomberg Finance LP

NEW ZEALAND: Nov Card Spending Surges, Pointing To Improving Q4 Consumption

New Zealand Nov card spending trends showed a notable improvement on Oct outcomes. This points to improving spending momentum as Q4 unfolds, strengthening the broader economic backdrop. This points to an on hold back drop for the RBNZ.

- Retail spending rose 1.2%m/m, after a 0.2% rise in Oct. Total spending was up 1.9%m/m, after a revised 0.2% gain in Oct. For this segment it was the strongest outcome since Dec last year in m/m terms. In y/y terms, total card spending was up 1.4%, ending an extended run of negative outcomes. Retail spend was +2.2%, versus a 0.3%y/y gain in Oct.

- Most of the sub-categories posted firm m/m rises for Nov, services up 2.8%, non retail industries 3.9% higher. Apparel and industries both rose over 2%m/m as well.

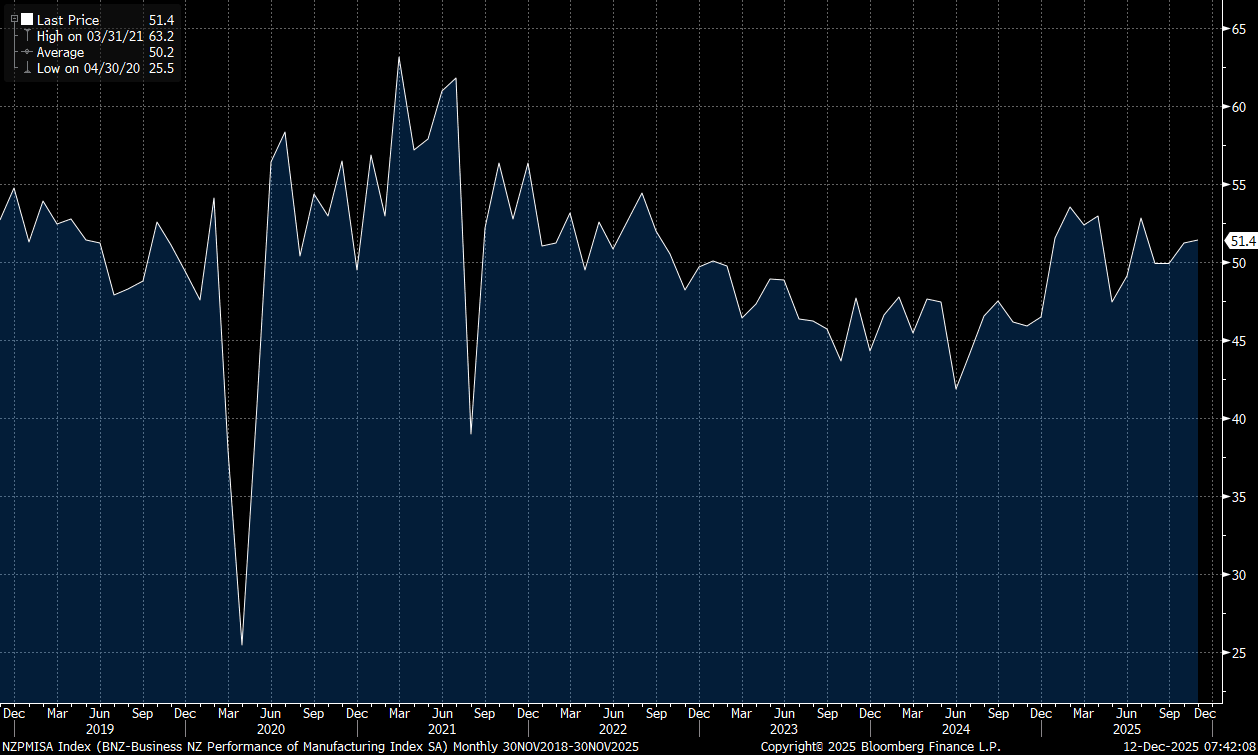

NEW ZEALAND: PMI Edges Up, Employment Index Bounces, New Orders Ease

New Zealand's BusinessNZ manufacturing PMI edged up to 51.4 in Nov, from a revised 51.2 outcome in Oct. This leaves us off recent cycle highs (53.6) in Feb of this year. Post Covid highs in the index were in the 60-65 region, see the chart below, so whilst the index remains in expansion, the pace of recovery looks to be fairly modest.

- In terms of the detail, it was mixed. Encouragingly, the employment sub index rose to 52.4 from 48.3 in Oct. This is the highest read since April of this year. New orders moderated though to 51.9, from 54.5 in Oct. Production edged up to 52.8 from 52.0 prior.

- Note next week we get Q3 GDP out on Thursday, with the market consensus looking for growth to return to positive territory.

Fig 1: NZ Manufacturing PMI Points To Expansion

Source: Business NZ/BNZ/Bloomberg Finance L.P./MNI

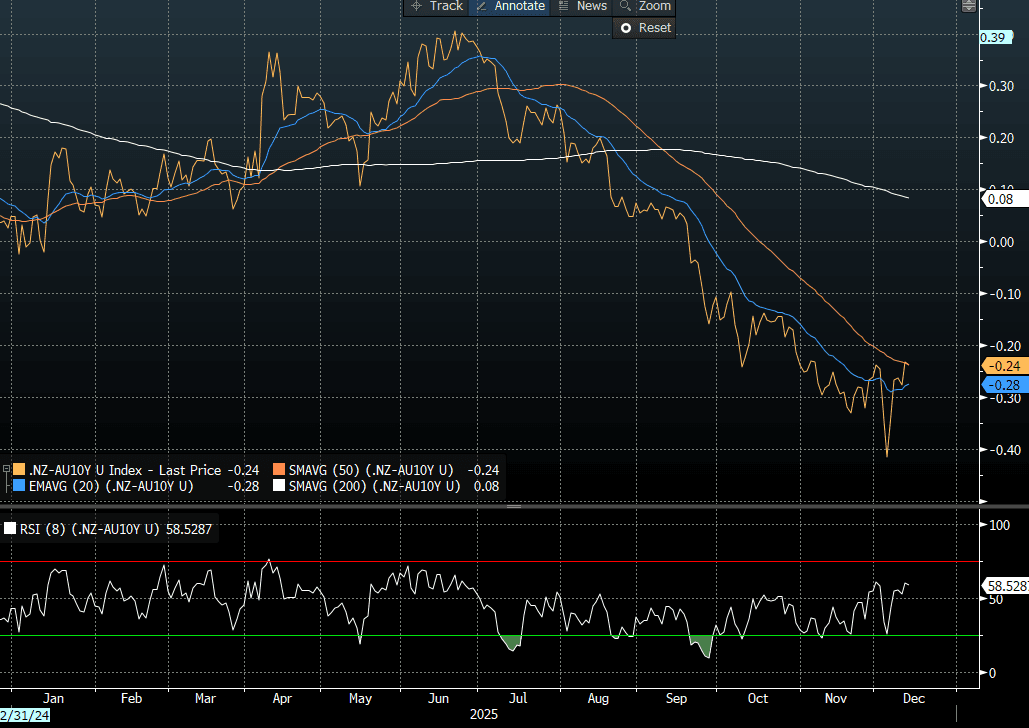

BONDS: NZGBS: Modest Bear-Steepener To End Another Heavy Week

NZGBs closed showing a bear-steepener, with benchmark bonds flat to 3bps higher.

- On a relative basis, however, NZGBs matched the performance of their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials little changed. Nevertheless, as the chart below shows, the NZ-AU spread has rebounded sharply from its lowest level since 2020 following the recent RBNZ policy decision and guidance (see chart).

- Cash US tsys are 1bp richer to 0.5bp cheaper, with a steepening bias, in today's Asia-Pac session.

- Swap rates closed flat to 2bps higher, with the 2s10s curve steeper.

- RBNZ-dated OIS pricing closed slightly softer across meetings. No tightening is priced for February, while November 2026 assigns 60bps.

- Interest rate expectations across the $-bloc firmed over the past week out to June 2026, led by New Zealand (+18bps) and Canada (+12bps), while Australia firmed by 7bps and the US edged higher by 4bps.

- On Monday, the local calendar will see the Performance Services Index.

Bloomberg Finance LP

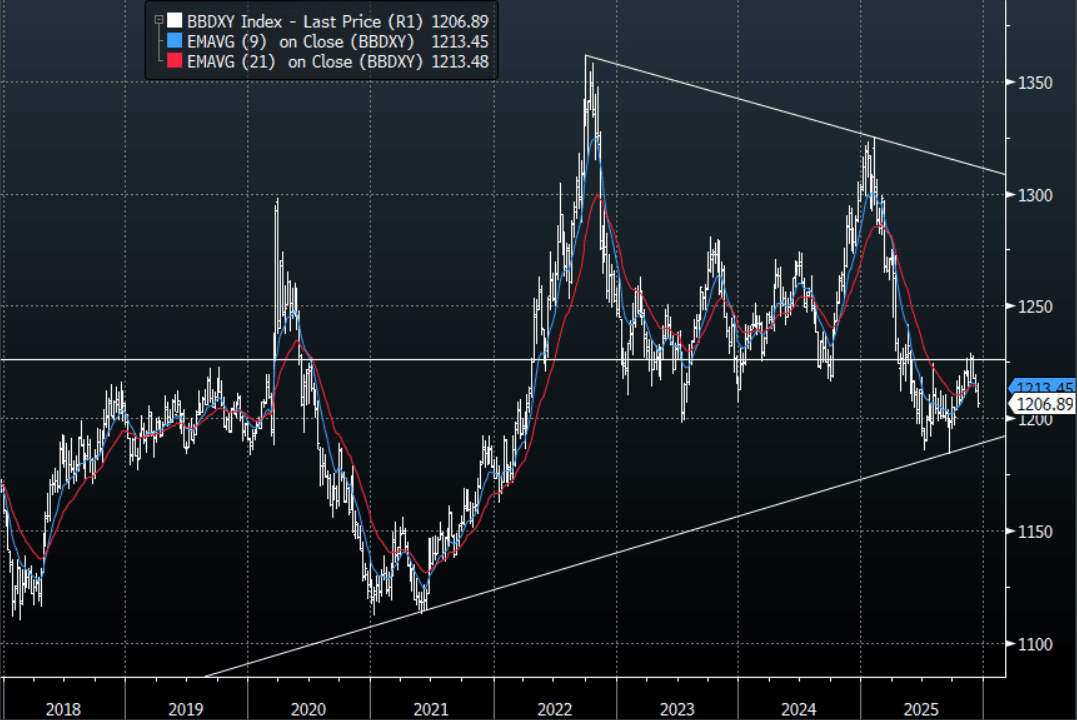

FOREX: USD - BBDXY Trading Heavy After Breaking Below 1210

The BBDXY has had a range today of 1205.87 - 1206.88 in the Asia-Pac session; it is currently trading around 1206, +0.05%. The unexpected dovish tilt from the FOMC has put the USD firmly back under pressure and this move had another extension lower overnight after breaking below the 1210 support. If the market has read the FOMC correctly the USD could be in some trouble here as it looks to reassert the downtrend. On the day look for resistance again back towards the 1209-1212 area where sellers should remerge initially, looking for a test of the overnight lows. Support is in the 1204/05 area; a move below here would target 1198-1200.

- EUR/USD - Asian range 1.1731-1.1746, Asia is currently trading 1.1735. The pair has broken higher as the USD comes back under pressure. On the day, dips toward 1.1690-1710 should be supported initially, looking to retest above the 1.1750 area again.

- GBP/USD - Asian range 1.3386-1.3400, Asia is currently dealing around 1.3390. The pair stalled above 1.3400 overnight but still trades underlying bid for now. On the day GBP should see support back toward the 1.3325-1.3345 area, looking for a retest of the highs seen above 1.3400.

- Cross asset : SPX -0.05%, Gold $4270, US 10-Year 4.16%, BBDXY 1206, Crude Oil $58.05

- Data/Events : Germany CPI, France CPI, Spain CPI

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

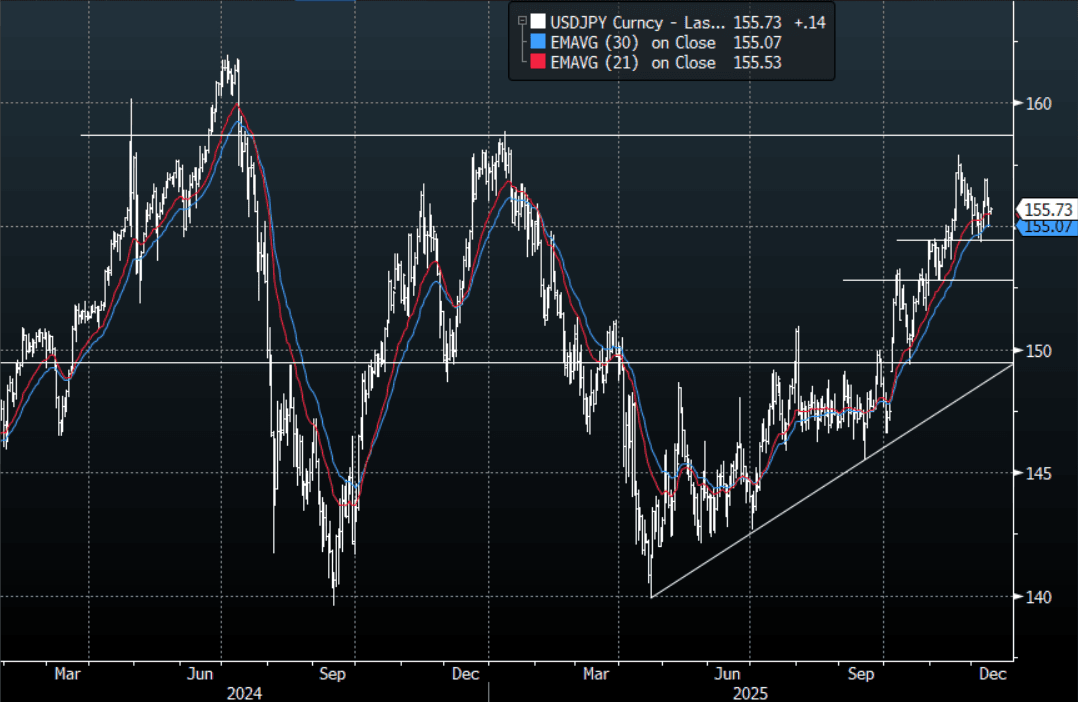

JPY: USD/JPY - Yen Weakness Hits Pause For Now

The USD/JPY range today has been 155.45 - 155.77 in the Asia-Pac session, it is currently trading around 155.70, +0.05%. The pair continued to build on its move lower overnight in reaction to a dovish Fed. The market was clearly wrong-footed looking for a hawkish cut and has had to pare back those trades. The market has been pricing in the fact that the Yen move looks likely to force the BOJ into action in December. This together with a dovish Fed could be enough to halt the Yen falling out of bed for now. Technically USD/JPY is in an uptrend, the first big support is back toward the 152.50-154.50 area. In today's Asian session, look for resistance back toward the 155.90-156.20 area, should this hold, look for a retest of the overnight lows at some point and then another examination of the support below.

- MNI POLICY: BOJ To Keep Neutral, Terminal Rate View. The Bank of Japan will maintain its current 1-2.5% estimated range for the neutral interest rate following the next hike widely expected at the Dec. 18-19 meeting, and will continue to assess whether its policy rate remains appropriately accommodative using indicators such as bank lending, the Tankan survey and capital investment, keeping the door open for further rate hikes, MNI understands.

- Bloomberg - “Nomura strategists recommend buying the yen against the dollar as a key trade for 2026. They believe Japan’s government may resist prolonged currency weakness, citing potential tailwinds like narrowing rate differentials and an improving trade balance.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.55b), 157.50($899m). Upcoming Close Strikes : 156.50($1.2b Dec 15) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 96 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

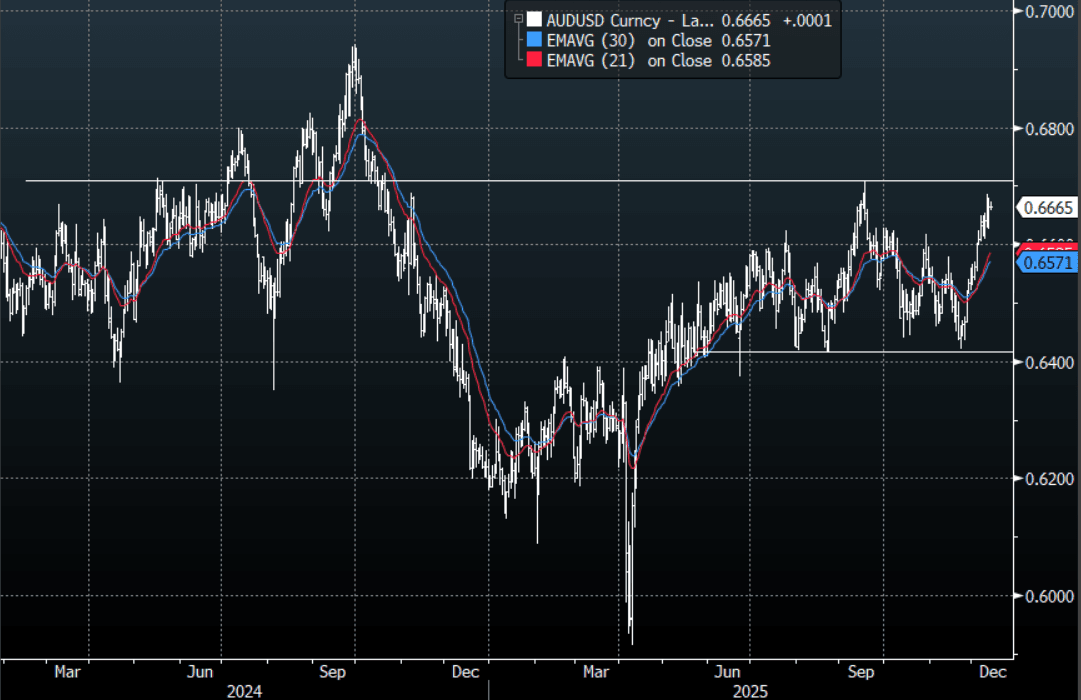

AUD/USD - Looking To Test 0.6700 As The USD Falters

The AUD/USD has had a range today of 0.6659 - 0.6674 in the Asia- Pac session, it is currently trading around 0.6665, +0.02%. The AUD whipped around yesterday but ultimately traded stronger as the USD looks to be breaking down thanks to the surprise dovish cut by the Fed. The AUD price action remains very constructive and a USD back under pressure should just add to its tailwinds. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. In the Asian session, I suspect the support back toward 0.6625-0.6645 will continue to find demand as the pair looks to rebuild momentum and have another look back toward the 0.6700 area. The AUD outperformance was previously being expressed more clearly in the crosses, could this dovish tilt from the Fed turn the spotlight back toward the AUD/USD.

- MNI INTERVIEW: RBA Feb Meeting Live, 4% Rate Over 2026 Eyed. The Reserve Bank of Australia Board could raise the 3.6% cash rate by 25 basis points as early as February, if Q4 underlying inflation prints above expectations, with the policy rate likely to move into the low 4% range over 2026, a former RBA senior economist told MNI in an interview.

- "Trump enlists 5 allies to counter China on rare earths and tech" - Politico via BBG: "The administration plans to launch the coalition of partners with the signing Friday of the Pax Silica Declaration, uniting Singapore, Australia, Japan, South Korea and Israel in a collaboration intended to address deficits in critical mineral access edging out China’s massive investment in its critical minerals and tech sector. The administration is actively looking to enlist other countries to join the group." NSN T74NO7BNAIO1 <GO>

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD922m). Upcoming Close Strikes : 0.6650(AUD855m Dec 15) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 39 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

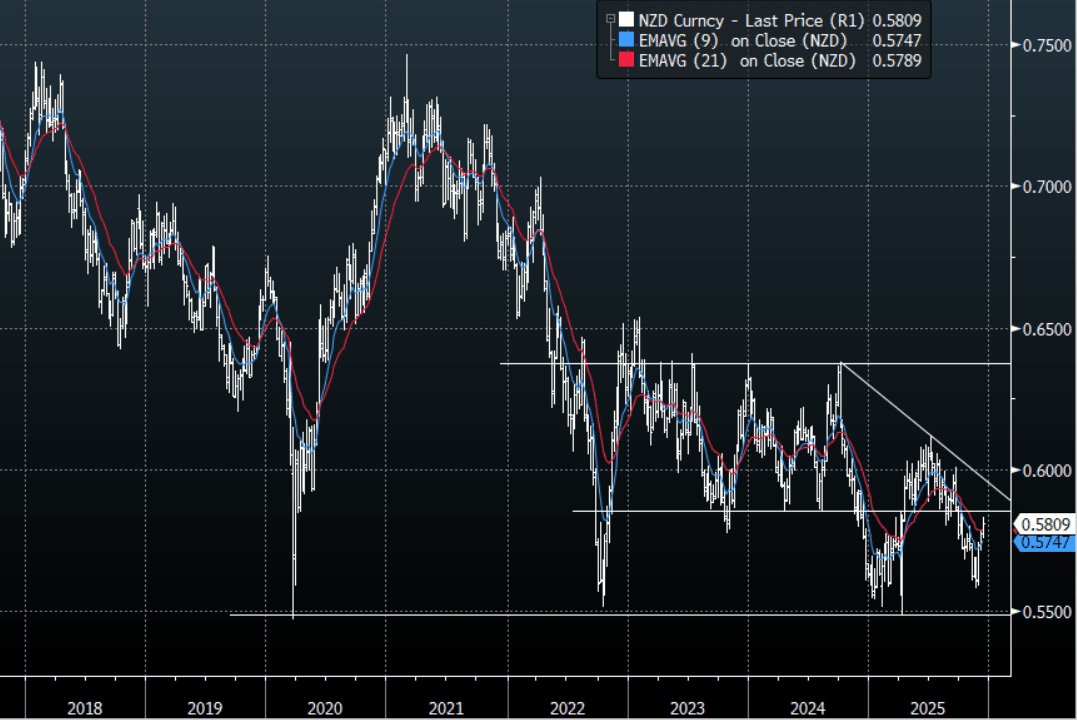

NZD/USD - Challenging Resistance Above 0.5800

The NZD/USD had a range today of 0.5806-0.5821 in the Asia-Pac session, going into the London open trading around 0.5810, +0.02%. The NZD is attempting to push back above the 0.5800 area, aided by a weak USD. On the day, watch to see if price can get any momentum back above 0.5800 as it tries to work through what should be stubborn resistance on the first attempt. First support on the day is around the 0.5770-0.5790 area if this does not hold it could signal a retracement to the more important 0.5730 area. I have this area between 0.5800-0.5900 as being decent longer-term resistance so will be watching to see if sellers do emerge to provide some headwinds to a NZD that looks to be gathering pace.

- MNI AU - Nov Card Spending Surges, Pointing To Improving Q4 Consumption: New Zealand Nov card spending trends showed a notable improvement on Oct outcomes. This points to improving spending momentum as Q4 unfolds, strengthening the broader economic backdrop. This points to an on hold back drop for the RBNZ.

- MNI AU - PMI Edges Up, Employment Index Bounces, New Orders Ease : New Zealand's BusinessNZ manufacturing PMI edged up to 51.4 in Nov, from a revised 51.2 outcome in Oct. This leaves us off recent cycle highs (53.6) in Feb of this year. While the index remains in expansion, the pace of recovery looks to be fairly modest.

- "NZ RAISES MINIMUM WAGE 2% TO NZ$23.95/HR FROM APR. 1" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD306m). Upcoming Close Strikes : 0.5780(NZD344m Dec 17), 0.5800(NZD315m Dec 17), 0.5850(NZD328m Dec 17) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 36 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: FED Rate Cuts Continue to Support Stocks, Eyes Next Week on BOJ

The positive momentum from a U.S. Federal Reserve interest rate cut continued to give markets a boost into the end of the week with major markets positive Friday. Ongoing expectations for a December rate hike from the BOJ next week remain, though later in the week JGBs and the NIKKEI have brushed off those fears. Chinese inflation data for October continued to rise whilst exports for November were significantly ahead of expectations, both supporting the outlook for fourth quarter growth. A disappointing cloud revenue result from Oracle impacted the tech sector Thursday with some key tech names set for a modest weekly decline. Starved of economic data of late, today's Malaysia October Industrial Production was stronger than expected, giving the equity market a boost and supporting a strong weekly gain.

- The NIKKEI is up +0.70% today, enough to turn marginally positive for the week, having recovered from tech sector led falls Thursday.

- China's major bourses are mixed to positive Friday, yet remain down for the week after heavy falls mid week. The Hang Seng is up over 1.3% Friday yet remains down -0.79% whilst the CSI 300 is up +0.22% and down -0.49%.

- Despite the challenges for some tech stocks, the KOSPI has recovered Friday with gains of +0.80% to push weekly gains just over 1%

- The NIFTY 50 saw profit takers emerge earlier in the week and ahead of the FED, with three successive days of falls. Whilst recovering today with gains of +0.40%, the NIFTY is one track for a fall of around -0.7% for the week.

- The FTSE Malay is up +0.67% today after strong gains Thursday and on track for its biggest weekly gain since early October.

- The Jakarta Composite hit new highs Monday only for profit takers to emerge. The modest gains of +0.45% today sees the JCI edge back into positive territory for the week.

ASIA STOCKS: Net Inflows For Tech Pays Remain Positive Past Week

Net equity inflow trends for the past 5 trading days have been mixed for EM Asia markets, see the table below. South Korea and Taiwan remain firmly positive at around the +$1.5bn mark. We did see some wobbles through Thursday trade, as Oracle's results cast a fresh shadow over the chip/AI related demand outlook. Still, broader global equity market trends are mostly positive for aggregate indices as we approach year end. Both the Kospi and Taiex have struggled to make fresh highs, but dips remain supported. As we approach year end, both markets remain in a net outflow posture for 2025 to date, and it would take quite strong inflows over the coming weeks to reverse this trend.

- In India, uncertainty continues to prevail over the US-India trade deal. The Chief Economic Advisor for India stating yesterday that most the key issues are now bedded down and that he would be surprised if an agreement wasn't in place by March next year. US comments have been promising around gaining access to Indian agricultural markets (although markets await details and on US tariff relief for India as part of broader trade agreement). Indian equities have mostly tracked lower since the start of the month.

- In South East Asia, Indonesia remains the most positive story although year to date it still maintains a net outflow stance.

- In Thailand focus will be on the election, to be held in the next 45-60 days. The local stock markets has struggled and is back close to Nov lows.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 283 | 1569 | -4213 |

| Taiwan (USDmn) | -417 | 1540 | -4498 |

| India (USDmn)* | -228 | -332 | -17560 |

| Indonesia (USDmn) | 82 | 91 | -1577 |

| Thailand (USDmn) | -28 | 33 | -3256 |

| Malaysia (USDmn) | -19 | -168 | -4785 |

| Philippines (USDmn) | -13 | -81 | -827 |

| Total (USDmn) | -341 | 2652 | -36715 |

| * Data Up To Dec 10 |

Source: Bloomberg Finance L.P./MNI

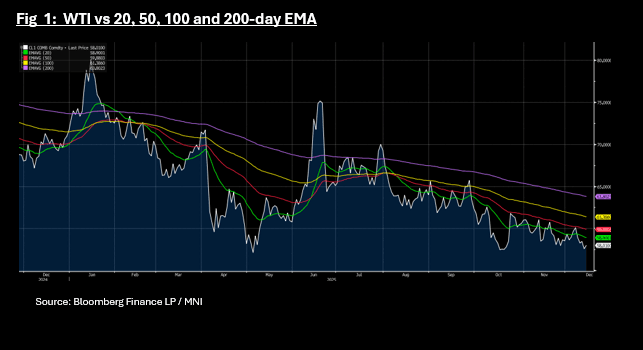

Oil Steadies, Set for Heavy Losses for Week

- Oil markets moved modestly positive in the Asia trading day, with WTI recovering back to US$58 bbl. WTI however remains down over 3% after a volatile week where the push pull of the FED and various news items on supply, weighed heavy on prices.

- Brent is up +0.19% to US$61.69 bbl but down over 3% for the week, the biggest weekly fall since October. All major moving averages are trending downwards gently a sign that the bearish trend may play out for some time to come.

- OPEC+ forecasts are now at odds with industry forecasts following the release of their latest projections. OPEC+ points to a balanced supply demand outlook whereas industry forecasts suggest a supply excess next year with one of the leading oil trading houses describing it as a 'super glut'. OPEC+ is known to be too optimistic in its forecasts missing year end estimates over the last two years. OPEC+ has agreed to pause further output increases during Q1 next year following increases in 2025.

- Brazilian oil output is coming back on line from issues that took out over 300,000 barrels a day last month, increasing the probability of an oversupply in 2026.

- Recent attacks by Ukraine on one of the primary export terminals for Kazakh oil has limited output by an estimated 250k barrels per day

- Ukraine attacked Lukoil's Caspian seal oil field with long range drones halting output for more than 20 wells at the offshore field.

- The seizure of the Venezuelan oil tanker by US military could be the start of a meaningful drop in oil exports from the sanctioned country with independent research firm Rapidan Energy Group suggesting up to 30% of Venezuela's oil exports are now at risk. (per BBG). According to comments from the White House, the seizure of the tanker is just the start of the US military upping the pressure on the Maduro government.

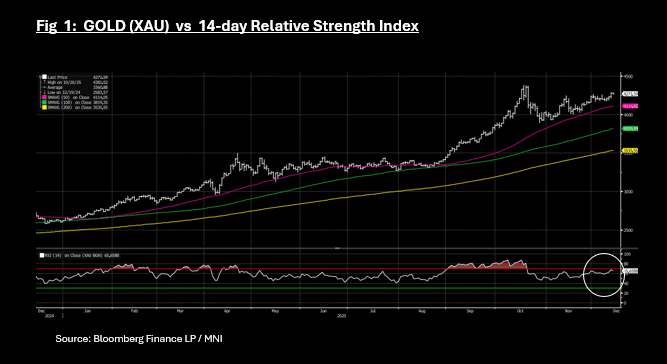

- Gold has delivered a strong gain for the week as the FED resumed rate cuts, and the fear of a hawkish outlook recedes.

- Gold is marginally down today at US$4,269.90, yet remains up by +1.7% for week.

- The sell off may be technically driven as gold neared overbought on the 14-day relative strength index. Falls today during the Asia trading day sees bullion move back below.

- With trade war related risks abating, gold's fortunes are aligned with the outlook for US interest rates next year. A lower interest rate in the US is a support to gold as it lowers funding costs to purchase.

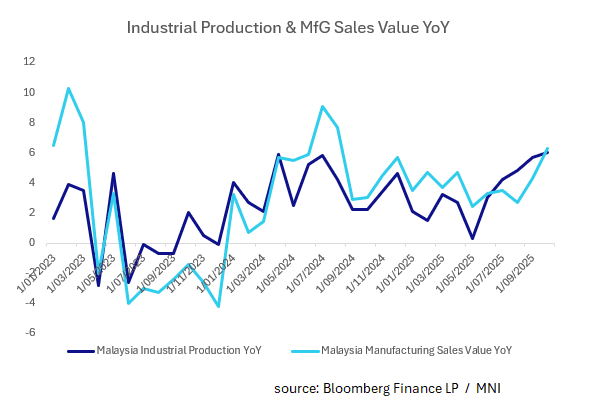

MALAYSIA: Industrial Production Up Again, Rate Outlook Extended

- Malaysia's October Industrial production topped expectations at 6.0%, marking the fifth month of consecutive increases.

- Manufacturing continues to power output in Malaysia with a jump of 6.5% in October and mining up 5.8%

- Manufacturing Sales Value YoY increased 6.3%, the biggest increase since July 2024.

- Over the next 12 months, the prevailing outlook among economists domestically in Malaysia is that Bank Negara Malaysia (BNM) will likely maintain its Overnight Policy Rate (OPR) at the current level of 2.75% given robust economic output, strong domestic demand and contained inflation.

- The U.S. Federal Reserve cutting interest rates helps narrow the interest rate gap with Malaysia. A narrower differential is expected to support the Malaysian ringgit and attract capital flows, making it less likely BNM will need to adjust rates to defend the currency.

- Currently the 3-YR MGS has a premium of +32bps over the BNM policy rate, a sign that bond investors expect little chance of a rate cut in 2026.

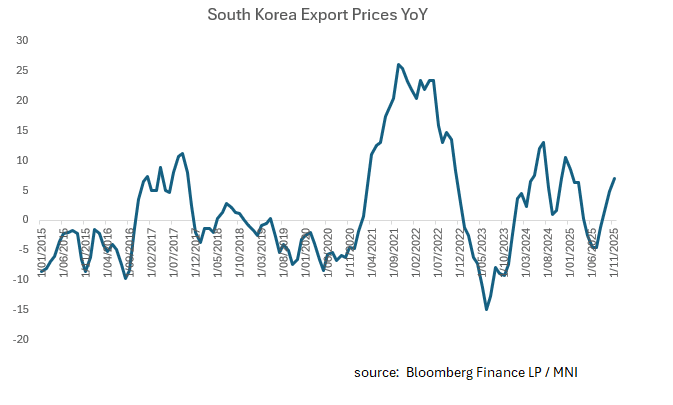

SOUTH KOREA: Export Prices Hit Highest Since January

- South Korea’s export prices rose 7.0% YoY in November 2025 compared with a year earlier, reversing earlier declines and marking a decent rebound in export price levels.

- On a monthly basis, the export price index increased 3.7% from October to November 2025.

- This marks five consecutive months of rising export prices — a continuation of an upward trend that began earlier in the year.

- A weaker Korean won boosted the export price index in won terms, amplifying the measured increase versus foreign currency-based prices.

- The rise was led mainly by manufactured goods, including computers, electronic and optical instruments, which posted notable price gains.

- Prices for agricultural and marine products also rose, adding to the overall positive contribution.

- Import prices rose 2.2% YoY in November as the ongoing weakness in the currency weighed on prices

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 12/12/2025 | 0700/0700 | *** | UK Monthly GDP | |

| 12/12/2025 | 0700/0800 | ** | Unemployment | |

| 12/12/2025 | 0700/0700 | ** | Trade Balance | |

| 12/12/2025 | 0700/0700 | ** | Index of Services | |

| 12/12/2025 | 0700/0700 | ** | Index of Production | |

| 12/12/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/12/2025 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/12/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/12/2025 | 0745/0845 | *** | HICP (f) | |

| 12/12/2025 | 0800/0900 | *** | HICP (f) | |

| 12/12/2025 | 0930/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 12/12/2025 | - | *** | Money Supply | |

| 12/12/2025 | - | *** | Social Financing | |

| 12/12/2025 | - | *** | New Loans | |

| 12/12/2025 | 1300/0800 | Philly Fed's Anna Paulson | ||

| 12/12/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 12/12/2025 | 1330/0830 | * | Building Permits | |

| 12/12/2025 | 1330/0830 | ** | Wholesale Trade | |

| 12/12/2025 | 1330/0830 | Cleveland Fed's Beth Hammack | ||

| 12/12/2025 | 1535/1035 | Chicago Fed's Austan Goolsbee | ||

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |