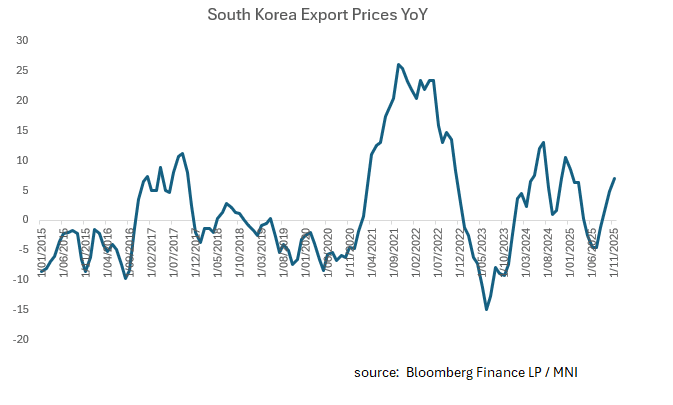

SOUTH KOREA: Export Prices Hit Highest Since January

- South Korea’s export prices rose 7.0% YoY in November 2025 compared with a year earlier, reversing earlier declines and marking a decent rebound in export price levels.

- On a monthly basis, the export price index increased 3.7% from October to November 2025.

- This marks five consecutive months of rising export prices — a continuation of an upward trend that began earlier in the year.

- A weaker Korean won boosted the export price index in won terms, amplifying the measured increase versus foreign currency-based prices.

- The rise was led mainly by manufactured goods, including computers, electronic and optical instruments, which posted notable price gains.

- Prices for agricultural and marine products also rose, adding to the overall positive contribution.

- Import prices rose 2.2% YoY in November as the ongoing weakness in the currency weighed on prices

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Corrective Phase Over, US Data Release Schedule Likely Next Week

Gold increased back above $4140 following concerning US ADP data but the move wasn’t held with it then falling to $4097.25. It has recovered somewhat to $4126.85 to be up 0.3% and 3.1% in November finding support from the weaker US dollar (BBDXY -0.1%). The market has around a 67% chance of a December Fed cut but gold’s response to the upcoming end of the US government shutdown signals that it thinks the delayed data will drive increased easing expectations when it is released.

- Advance ADP data suggested private sector job losses in the four weeks to 25 October but the providers noted the data is preliminary and could be revised.

- Our US analysts believe that the post-shutdown data schedule should be published next week but there is a risk that October CPI won’t be released. See their FAQ here.

- Bullion reached $4149.0 on Tuesday, remaining below initial resistance at $4161.4, 22 October high. The recent recovery in gold prices marks the end of the corrective phase which allowed the overbought condition to unwind. The bull trigger is at $4381.5. A decline below the 50-day EMA at $3890.0 would signal scope for a deeper retracement.

- Bloomberg reported gold ETF outflows in the 3 weeks to November 7 following 8 weeks of inflows.

- Silver rose to $51.252, remaining below initial resistance at $52.374, following the ADP data and then fell to $50.290. It then recovered to $51.221 to be up 1.4% on the day and 5.2% on the month. The trend remains bullish with the metal continuing to trade above the 50-day EMA at $46.484.

AUSSIE SWAPS: AU-NZ 1Y3M Spread Highest Since 2012

AU–NZ 1-year forward 3-month swap (1Y3M) spread at 103bps is now at its highest level since 2012.

- The 1Y3M differential is a proxy for the expected relative policy path over the next 12 months.

Bloomberg Finance LP

CNH: Lags Softer Dollar Backdrop, USD/CNH Risks Still Biased Lower

USD/CNH once again couldn't sustain sub 7.1200 levels, despite a softer USD backdrop as Tuesday trade unfolded (we were last 7.1220/25). The BBDXY index and DXY indices lost around 0.10%, as softer jobs data from the new weekly ADP release weighed. CNH was close to unchanged for Tuesday's session, while the broader technical backdrop remains the same. Expect moves up into the 7.1300/1400 region to draw selling interest, while downside targets are likely to focus on 7.1000 from a medium term standpoint.

- Spot USD/CNY finished up at 7.1173, while the CNY CFETS basket tracker edged down a little further to 97.87, consistent with softer USD index levels.

- The CNH/JPY cross was relatively steady, we track near 21.6470 in early Wednesday trade, with USD/JPY unable to test above 154.50 as softer US data weighed. This leaves recent highs in CNH/JPY intact, just above 21.70.

- For USD/CNH, downside risks will still likely emerge as the bias around US-CH 2yr yield differentials is still skewed lower over the medium term.

- The PBoC did state late yesterday, it will implement a moderately loose monetary policy, utilise various tools to maintain relatively loose social financing conditions, according to the Q3 monetary report released Tuesday. On FX, the report said it will maintain exchange rate flexibility, strengthen expectation guidance, prevent the risk of overshooting, and keep the yuan basically stable at a reasonable and balanced level. This is no change in the FX stance.

- On the data front, we still await Oct new loans and aggregate financing data. The PBoC also stated that slowing loan growth is not cause for concern as the economy shifts from high speed to high quality growth.