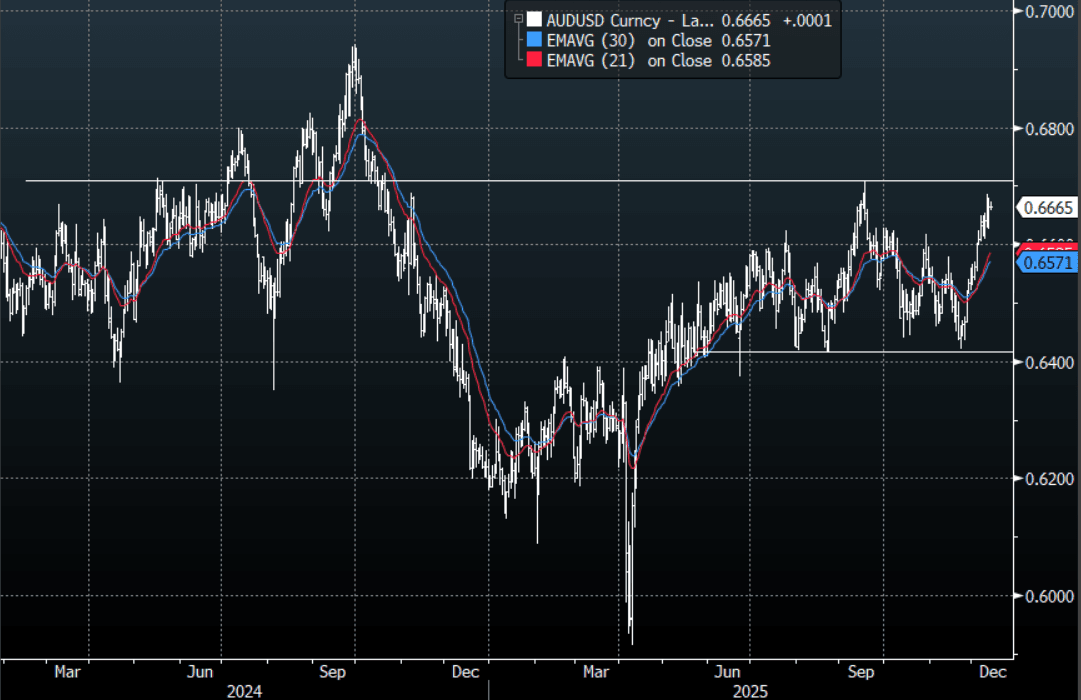

AUD: AUD/USD - Looking To Test 0.6700 As The USD Falters

The AUD/USD has had a range today of 0.6659 - 0.6674 in the Asia- Pac session, it is currently trading around 0.6665, +0.02%. The AUD whipped around yesterday but ultimately traded stronger as the USD looks to be breaking down thanks to the surprise dovish cut by the Fed. The AUD price action remains very constructive and a USD back under pressure should just add to its tailwinds. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. In the Asian session, I suspect the support back toward 0.6625-0.6645 will continue to find demand as the pair looks to rebuild momentum and have another look back toward the 0.6700 area. The AUD outperformance was previously being expressed more clearly in the crosses, could this dovish tilt from the Fed turn the spotlight back toward the AUD/USD.

- MNI INTERVIEW: RBA Feb Meeting Live, 4% Rate Over 2026 Eyed. The Reserve Bank of Australia Board could raise the 3.6% cash rate by 25 basis points as early as February, if Q4 underlying inflation prints above expectations, with the policy rate likely to move into the low 4% range over 2026, a former RBA senior economist told MNI in an interview.

- "Trump enlists 5 allies to counter China on rare earths and tech" - Politico via BBG: "The administration plans to launch the coalition of partners with the signing Friday of the Pax Silica Declaration, uniting Singapore, Australia, Japan, South Korea and Israel in a collaboration intended to address deficits in critical mineral access edging out China’s massive investment in its critical minerals and tech sector. The administration is actively looking to enlist other countries to join the group." NSN T74NO7BNAIO1 <GO>

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD922m). Upcoming Close Strikes : 0.6650(AUD855m Dec 15) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 39 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Closed Slightly Richer But Underperforms $-Bloc

NZGBs closed 1bp richer across benchmarks.

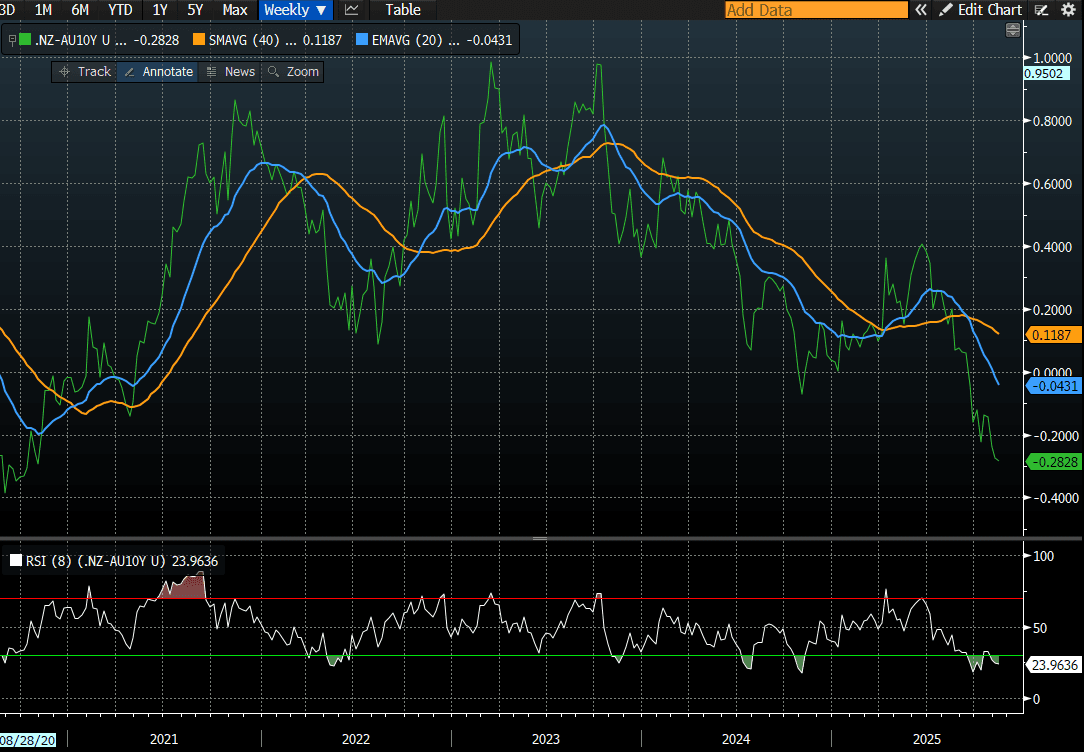

- On a relative basis, NZGBs have underperformed the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials both 3bps wider at +2bps and -27bps, respectively.

- Nevertheless, the NZ-AU 10-year yield differential remains close to its lowest level since 2020. At this level, investors could be lured into taking differential reversal trades. That said, such trades carry meaningful risk ahead of tomorrow’s October employment data. (see chart)

- Swap rates closed flat to 2bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed little changed across meetings. 28bps of easing is priced for November, with a cumulative 38bps by February 2026.

- The local calendar will see Card Spending data tomorrow.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond, NZ$150mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

- The NZ Treasury has today announced the appointment of the following joint lead managers to form the panel for the syndicated tap of the 15 May 2036 nominal bond: ANZ Bank; J.P. Morgan; UBS; and Westpac.

- As previously announced, the Treasury expects to launch this transaction before calendar year-end 2025, subject to market conditions. As per usual practice, if the syndication occurs, the scheduled bond tender for that week will be cancelled.

Bloomberg Finance LP

MNI EXCLUSIVE: Local Analysts On China's 2026 CPI Trends

Local analysts provide insight into China's 2026 CPI trends. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

ASIA: Inflation Green Shoots Could See Rates on Hold for Near Term (Part 2)

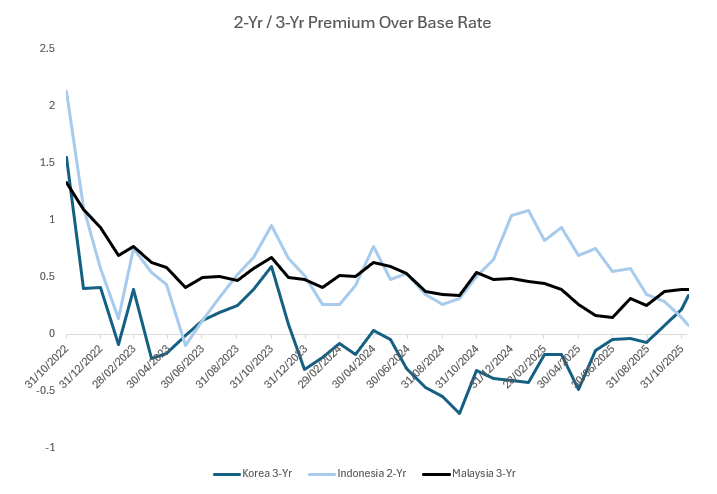

- Bond markets in the region have moved to price out cuts, yet the potential for further moves remains. In Korea and Malaysia we assess the 3-Yr (due to the presence of a bond future) versus the bas rate and the premium over the base rate. For Indonesia we use the 2-Yr.

- What we found is that since the mid part of 2025, the premium over has been increasing. A sign that can be interpreted as the bond market starting to question further rate cuts.

- During the mid part of this year this relationship was negative in Korea, but has moved to +33bps, pricing out cuts and suggesting the BOK is on hold for some time. When considering the last time the BOK was on hold for an extended period in mid 2023, this spread traded around +60bps for some time.

- In Indonesia, the premium over currently is +9bps yet in the period in late 2023, this relationship above +70bps.

- In Malaysia, the period in early 2024 when the BNM was on hold for an extended period saw this relationship get to +65bps whereas today it stands at +40bps

The analysis when added to Part 1 of "Inflation Green Shoots Could See Rates on Hold for Near Term" suggests that if inflation continues to increase at the pace it has been increasing, and BOK, BI and BNM are on hold for an extended period, short end rates have room to move higher from today's levels.

Fig 1: 2-Yr and 3-Yr Government Bond Yield Premium Over the Base Rate

source: Bloomberg Finance LP / MNI