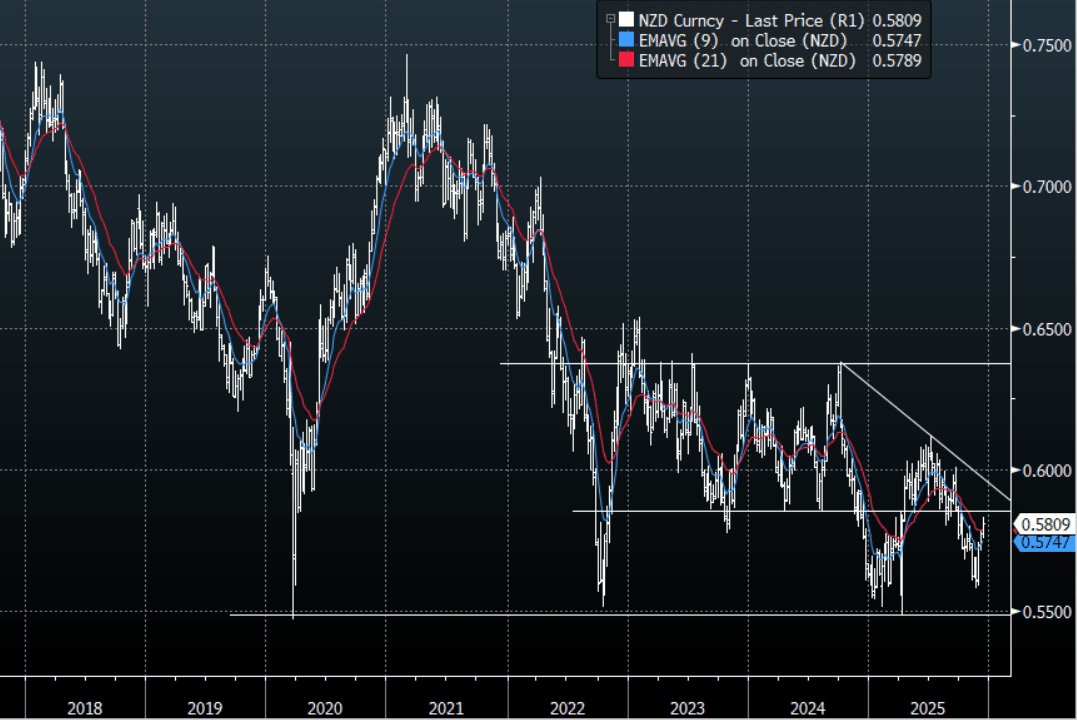

NZD: NZD/USD - Challenging Resistance Above 0.5800

The NZD/USD had a range today of 0.5806-0.5821 in the Asia-Pac session, going into the London open trading around 0.5810, +0.02%. The NZD is attempting to push back above the 0.5800 area, aided by a weak USD. On the day, watch to see if price can get any momentum back above 0.5800 as it tries to work through what should be stubborn resistance on the first attempt. First support on the day is around the 0.5770-0.5790 area if this does not hold it could signal a retracement to the more important 0.5730 area. I have this area between 0.5800-0.5900 as being decent longer-term resistance so will be watching to see if sellers do emerge to provide some headwinds to a NZD that looks to be gathering pace.

- MNI AU - Nov Card Spending Surges, Pointing To Improving Q4 Consumption: New Zealand Nov card spending trends showed a notable improvement on Oct outcomes. This points to improving spending momentum as Q4 unfolds, strengthening the broader economic backdrop. This points to an on hold back drop for the RBNZ.

- MNI AU - PMI Edges Up, Employment Index Bounces, New Orders Ease : New Zealand's BusinessNZ manufacturing PMI edged up to 51.4 in Nov, from a revised 51.2 outcome in Oct. This leaves us off recent cycle highs (53.6) in Feb of this year. While the index remains in expansion, the pace of recovery looks to be fairly modest.

- "NZ RAISES MINIMUM WAGE 2% TO NZ$23.95/HR FROM APR. 1" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD306m). Upcoming Close Strikes : 0.5780(NZD344m Dec 17), 0.5800(NZD315m Dec 17), 0.5850(NZD328m Dec 17) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 36 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

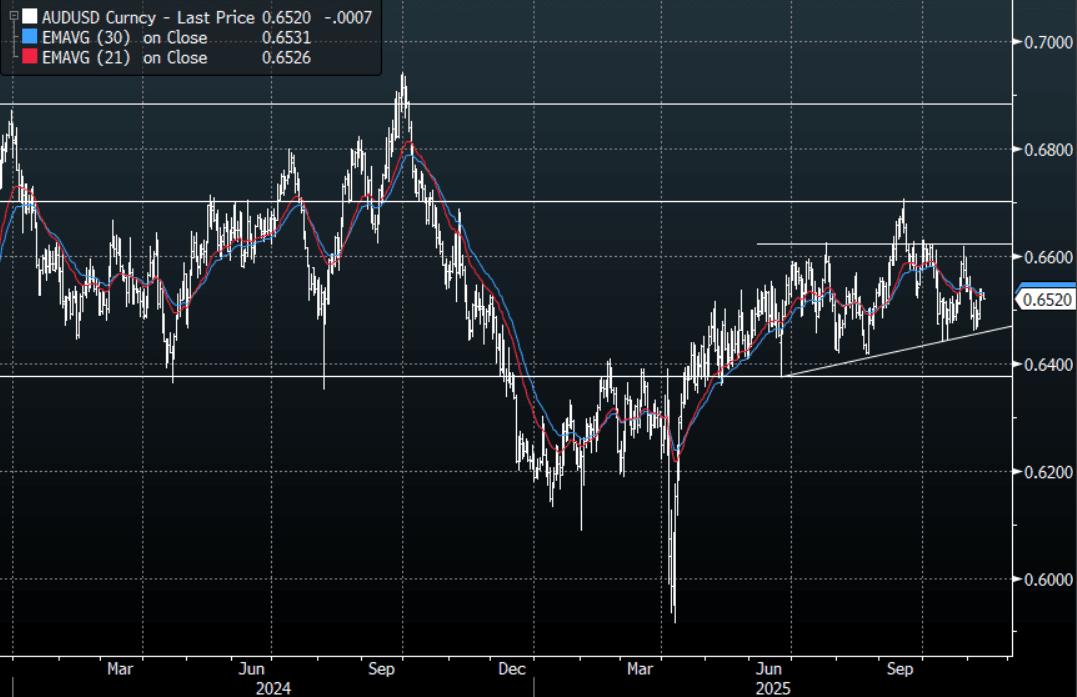

AUD: Asia-Pac: AUD/USD Drifts Lower

The AUD/USD has had a range today of 0.6520 - 0.6532 in the Asia- Pac session, it is currently trading around 0.6520, -0.10%. The AUD/USD has drifted sideways in our session consolidating its gains above 0.6500. The AUD will be one of the main beneficiaries while this positive sentiment dominates the market. The AUD/USD needs a sustained push above the 0.6550 area for the focus to turn back toward the 0.6650/0.6700 year highs. Look for intra-day dips toward 0.6480-0.6500 to be supported if this move higher is to come to fruition.

- MNI AU - Strong Home Lending May Contribute To Extended RBA Hold. The RBA noted this month that “the housing market is continuing to strengthen, a sign that recent interest rate reductions are having an effect”. The lending data is consistent with this and likely to add to its caution about easing further.

- Hauser Says RBA Debating Current Policy Stance - Per RTRS: Headlines have crossed from an Rtrs interview with RBA Deputy Governor Hauser. Rtrs notes: "A top Australian central banker said on Wednesday that there was increasing debate about whether the current cash rate of 3.6% is restrictive enough to keep inflation in check, adding that the question is critical for the policy outlook."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD1.37b), 0.6530(AUD 939m). Upcoming Close Strikes : 0.6520(AUD852m Nov 13), 0.6750(AUD2.17b Nov 14) - BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

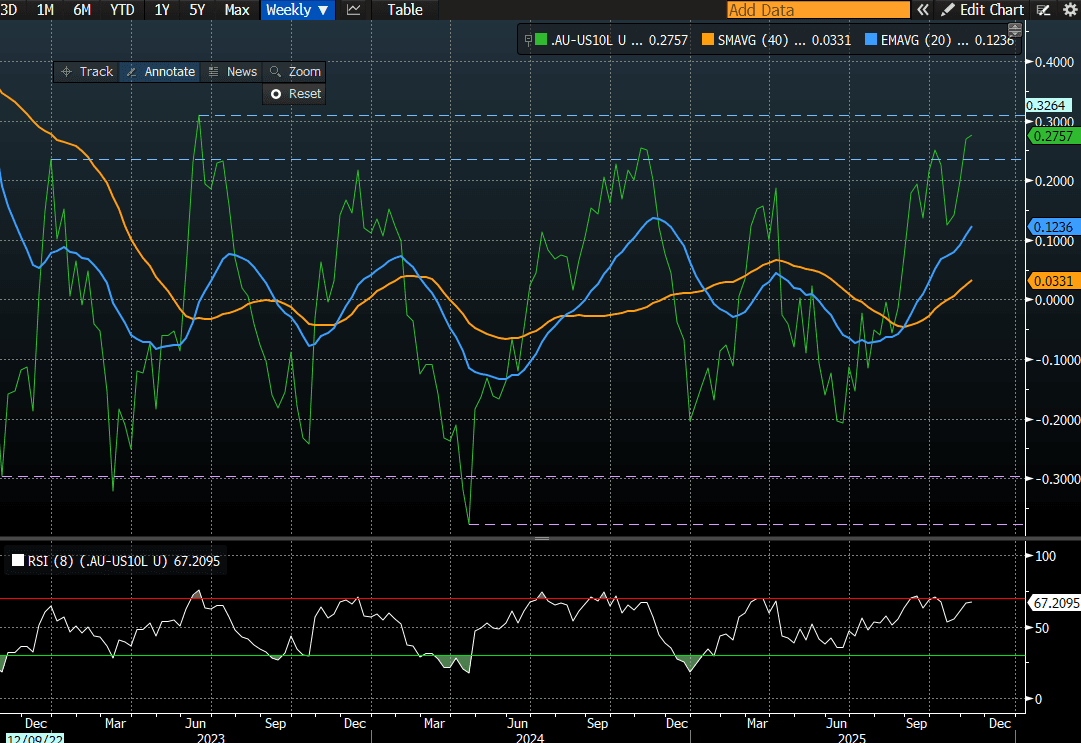

AUSSIE BONDS: Richer But AU-US 10Y Diff At Range Top Ahead Of Jobs Data

ACGBs (YM +1.5 & XM +2.0) are modestly stronger despite today’s much stronger-than-expected home loan data.

- The recovery in home lending began in Q2 after the RBA began easing in February and the 75bp to August appears to have contributed to the sharp rise.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +29bps. At this level, investors may be tempted to position for a narrowing in the differential, as it sits near the top of its well-defined ±30bps trading range (see chart).

- However, such trades carry meaningful risk ahead of tomorrow’s October employment data. The unemployment rate rose 0.2pp to 4.5% in September.

- The unemployment rate is widely expected to normalise somewhat at 4.4% but there are a few economists who expect it to stay at 4.5% or fall back to 4.3%.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 9% probability, with a cumulative 16bps of easing priced by mid-2026.

- The AOFM plans to sell A$800mn of the 1.75% 21 November 2032 bond on Friday.

Bloomberg Finance LP

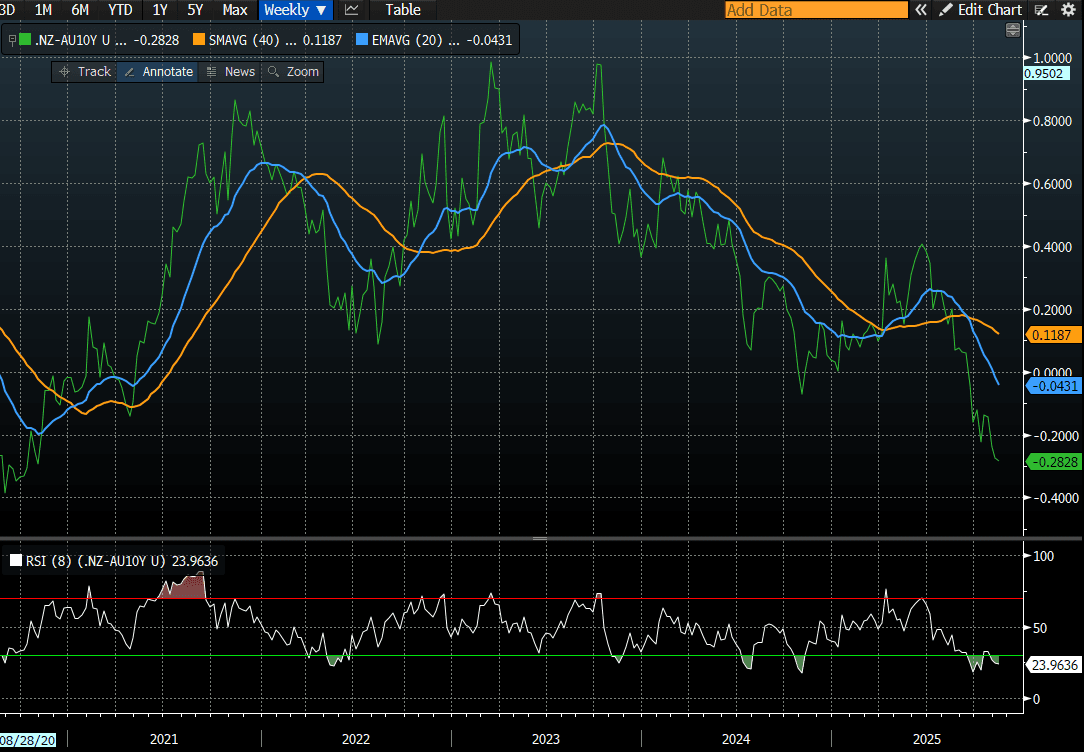

BONDS: Closed Slightly Richer But Underperforms $-Bloc

NZGBs closed 1bp richer across benchmarks.

- On a relative basis, NZGBs have underperformed the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials both 3bps wider at +2bps and -27bps, respectively.

- Nevertheless, the NZ-AU 10-year yield differential remains close to its lowest level since 2020. At this level, investors could be lured into taking differential reversal trades. That said, such trades carry meaningful risk ahead of tomorrow’s October employment data. (see chart)

- Swap rates closed flat to 2bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed little changed across meetings. 28bps of easing is priced for November, with a cumulative 38bps by February 2026.

- The local calendar will see Card Spending data tomorrow.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond, NZ$150mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

- The NZ Treasury has today announced the appointment of the following joint lead managers to form the panel for the syndicated tap of the 15 May 2036 nominal bond: ANZ Bank; J.P. Morgan; UBS; and Westpac.

- As previously announced, the Treasury expects to launch this transaction before calendar year-end 2025, subject to market conditions. As per usual practice, if the syndication occurs, the scheduled bond tender for that week will be cancelled.

Bloomberg Finance LP