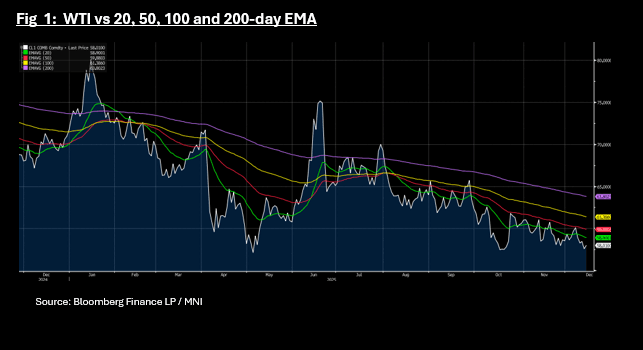

OIL: Oil Steadies, Set for Heavy Losses for Week

- Oil markets moved modestly positive in the Asia trading day, with WTI recovering back to US$58 bbl. WTI however remains down over 3% after a volatile week where the push pull of the FED and various news items on supply, weighed heavy on prices.

- Brent is up +0.19% to US$61.69 bbl but down over 3% for the week, the biggest weekly fall since October. All major moving averages are trending downwards gently a sign that the bearish trend may play out for some time to come.

- OPEC+ forecasts are now at odds with industry forecasts following the release of their latest projections. OPEC+ points to a balanced supply demand outlook whereas industry forecasts suggest a supply excess next year with one of the leading oil trading houses describing it as a 'super glut'. OPEC+ is known to be too optimistic in its forecasts missing year end estimates over the last two years. OPEC+ has agreed to pause further output increases during Q1 next year following increases in 2025.

- Brazilian oil output is coming back on line from issues that took out over 300,000 barrels a day last month, increasing the probability of an oversupply in 2026.

- Recent attacks by Ukraine on one of the primary export terminals for Kazakh oil has limited output by an estimated 250k barrels per day

- Ukraine attacked Lukoil's Caspian seal oil field with long range drones halting output for more than 20 wells at the offshore field.

- The seizure of the Venezuelan oil tanker by US military could be the start of a meaningful drop in oil exports from the sanctioned country with independent research firm Rapidan Energy Group suggesting up to 30% of Venezuela's oil exports are now at risk. (per BBG). According to comments from the White House, the seizure of the tanker is just the start of the US military upping the pressure on the Maduro government.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Local Analysts On China's 2026 CPI Trends

Local analysts provide insight into China's 2026 CPI trends. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

ASIA: Inflation Green Shoots Could See Rates on Hold for Near Term (Part 2)

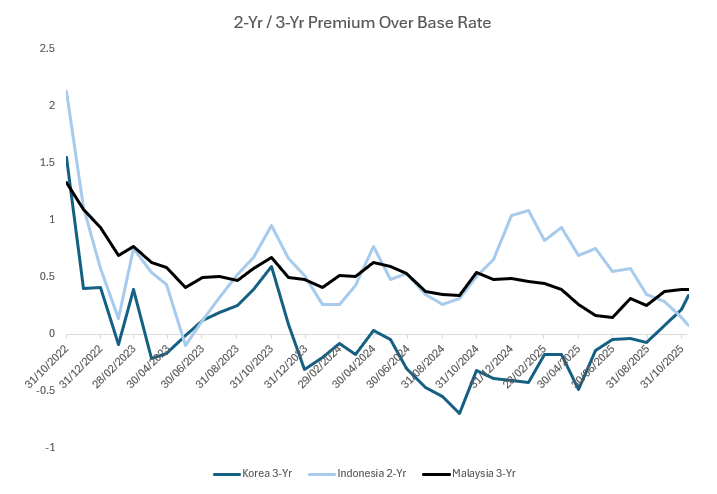

- Bond markets in the region have moved to price out cuts, yet the potential for further moves remains. In Korea and Malaysia we assess the 3-Yr (due to the presence of a bond future) versus the bas rate and the premium over the base rate. For Indonesia we use the 2-Yr.

- What we found is that since the mid part of 2025, the premium over has been increasing. A sign that can be interpreted as the bond market starting to question further rate cuts.

- During the mid part of this year this relationship was negative in Korea, but has moved to +33bps, pricing out cuts and suggesting the BOK is on hold for some time. When considering the last time the BOK was on hold for an extended period in mid 2023, this spread traded around +60bps for some time.

- In Indonesia, the premium over currently is +9bps yet in the period in late 2023, this relationship above +70bps.

- In Malaysia, the period in early 2024 when the BNM was on hold for an extended period saw this relationship get to +65bps whereas today it stands at +40bps

The analysis when added to Part 1 of "Inflation Green Shoots Could See Rates on Hold for Near Term" suggests that if inflation continues to increase at the pace it has been increasing, and BOK, BI and BNM are on hold for an extended period, short end rates have room to move higher from today's levels.

Fig 1: 2-Yr and 3-Yr Government Bond Yield Premium Over the Base Rate

source: Bloomberg Finance LP / MNI

ASIA: Inflation Green Shoots Could See Rates on Hold for Near Term

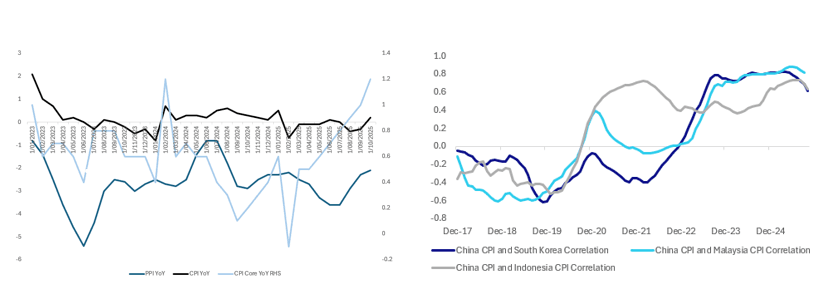

- Over the weekend, China's YoY CPI rose to +0.2%, after months of flipping between very modest to no inflation and deflation. Core inflation however jumped to +1.2%, it's highest reading in over a year.

- The Q3 Monetary Policy Report described inflation as 'weak' whilst the broader economy as stable and fundamentals solid. Following this report Goldman Sachs pushed their rate cut call out to Q1 2026, from Q4 2025.

- Over the last decade in various cycles China's deflation challenges have impacted the region. In 2014-16 a commodity slump pushed on a slowing economy after years of heavy investment particularly in manufacturing resulting in Asia facing cheap Chinese imports, which pushed PPIs in the region negative. From 2018-19 the early stages of the trade war under the Trump administration resulted in manufacturing excesses being dumped in the region, pushing down producer prices. Again in 2023-25 manufacturing overcapacity, particularly from EV related industries has seen extreme price competition, pushing down producer prices in the region.

- PPI's correlation to CPI is strong. Likewise CPI's correlation to Core. As core rises, it is likely to result in CPI rises, which in turn can feed into PPI. Whilst PPI and CPI remain negative and barely positive, it is their delta that raises the most interest. From their lows they have retraced 40% for PPI and 120% for CPI and with Core CPI now pushing to it's highest since 2022, are we about to see a bottoming and or a resurgence of inflation and what does that mean for the region and the rate cycle?

Fig 1: China PPI YoY, CPI YoY and Core CPI YoY & China CPI Correlations with Korea, Malaysia + Indonesia - Rolling 3yrs

source: Bloomberg Finance LP / MNI

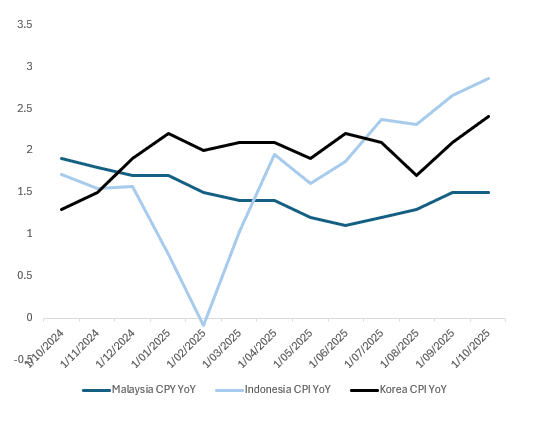

- Regionally, whilst on an historical comparison CPI remains low, the delta of CP from lows is worth noting.

Fig 2: Malaysia, Indonesia & Korea CPI YoY

source: Bloomberg Finance LP / MNI

- When looking back, Malaysia' meeting last week could mark the turning point in the rates cycle for region. Bank Negara (BNM) held rates steady with a balanced assessment of inflation and growth, a view likely re-enforced by the US trade deal. The BNM sees inflation as contained through 2026 noting global costs moderating. The BNM cuts rates only once whereas the Bank Indonesia five times and Bank of Korea four times.

- The BOK faces a housing crisis with house price escalation at the forefront of policymakers minds. When added to the trend in CPI, it suggests the BOK could be on hold for some time.

- In Indonesia, the Rupiah has lost -2.5% over the last three months and is down -3.4% year to date. This at a time when 3Q GDP topped 5% and the JCI is up 40% from the trade war induced April lows.

- As US rate cuts now appear less certain, the outlook in Asia appears similar. What could follow for Asia's Central Bank's could be an extended hold, with those markets with rate cuts priced in still, progressively taking them out.

- The Goldman Sachs change may just be the start of more to come across the region, as rate cut expectations get pushed out. Central Bank's need to maintain flexibility to cut rates further and worry about taking rates too low especially if their currencies are pressurized.

- The BOK is on hold for now with the BNM joining them. Markets will watch with interest as the BI deals with the competing interests of a pro-growth government and a currency that won't rally.