ASIA STOCKS: FED Rate Cuts Continue to Support Stocks, Eyes Next Week on BOJ

The positive momentum from a U.S. Federal Reserve interest rate cut continued to give markets a boost into the end of the week with major markets positive Friday. Ongoing expectations for a December rate hike from the BOJ next week remain, though later in the week JGBs and the NIKKEI have brushed off those fears. Chinese inflation data for October continued to rise whilst exports for November were significantly ahead of expectations, both supporting the outlook for fourth quarter growth. A disappointing cloud revenue result from Oracle impacted the tech sector Thursday with some key tech names set for a modest weekly decline. Starved of economic data of late, today's Malaysia October Industrial Production was stronger than expected, giving the equity market a boost and supporting a strong weekly gain.

- The NIKKEI is up +0.70% today, enough to turn marginally positive for the week, having recovered from tech sector led falls Thursday.

- China's major bourses are mixed to positive Friday, yet remain down for the week after heavy falls mid week. The Hang Seng is up over 1.3% Friday yet remains down -0.79% whilst the CSI 300 is up +0.22% and down -0.49%.

- Despite the challenges for some tech stocks, the KOSPI has recovered Friday with gains of +0.80% to push weekly gains just over 1%

- The NIFTY 50 saw profit takers emerge earlier in the week and ahead of the FED, with three successive days of falls. Whilst recovering today with gains of +0.40%, the NIFTY is one track for a fall of around -0.7% for the week.

- The FTSE Malay is up +0.67% today after strong gains Thursday and on track for its biggest weekly gain since early October.

- The Jakarta Composite hit new highs Monday only for profit takers to emerge. The modest gains of +0.45% today sees the JCI edge back into positive territory for the week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

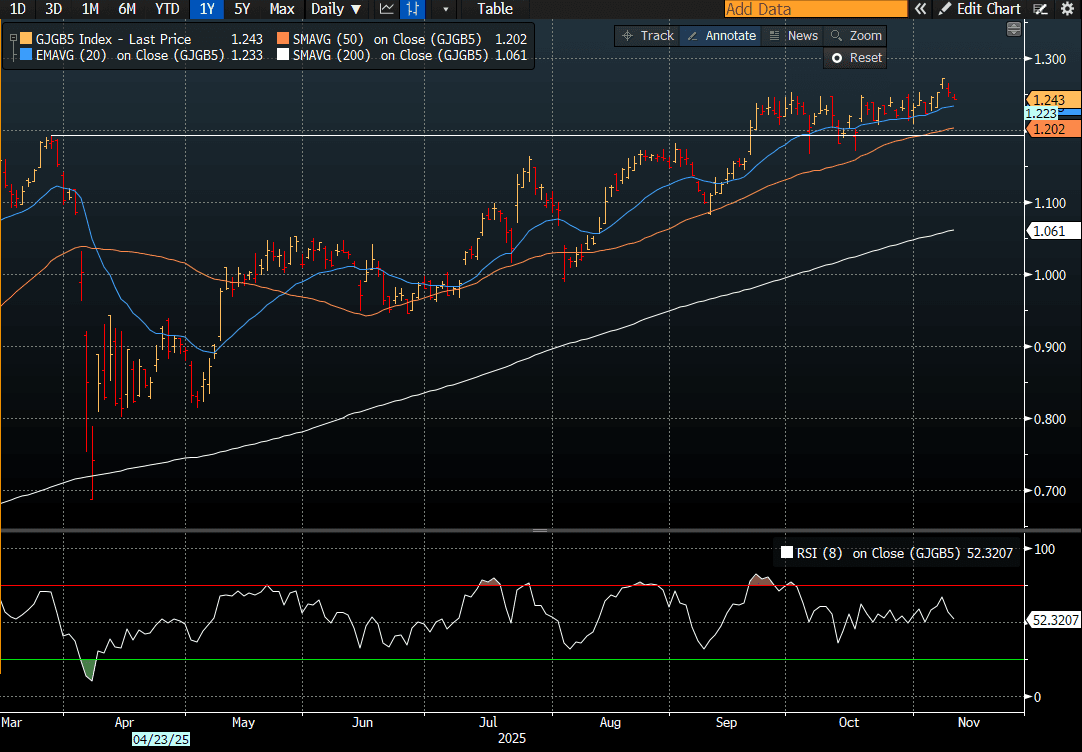

JGBS: 5Y Richer Ahead Of Tomorrow's Supply, Long-End Cheaper

JGB futures are stronger and at session highs, +14 compared to settlement levels, on a data-light day.

- Cash US tsys are 2-4bps richer in today's Asia-Pac session after being closed yesterday for Veterans Day.

- Cash JGBs are 1.5bps richer (7-year) to 1.5bps cheaper (20- and 40-year) across benchmarks. The benchmark 5-year yield is 0.9bp at 1.243% versus the cycle high of 1.272% (see chart).

- Ahead of tomorrow's 5-year supply, the 2s/5s curve has steepened to near its cycle high of 32bps, last reached in late 2023.

- Regression analysis shows a strong pro-cyclical, but atypical, relationship between the 5-year yield and the 2s/5s curve over the past 12 months.

- This dynamic is supported by expectations that the 5-year sector will sit in the "sweet spot" for increased issuance, as Prime Minister Sanae Takaichi looks to deploy her first stimulus package to jump-start the economy.

- Swap rates are 1bp lower to 1bp higher, with a steepening bias.

- Tomorrow, the local calendar will see PPI and International Investment Flow data alongside 5-year supply.

Source: Bloomberg Finance LP

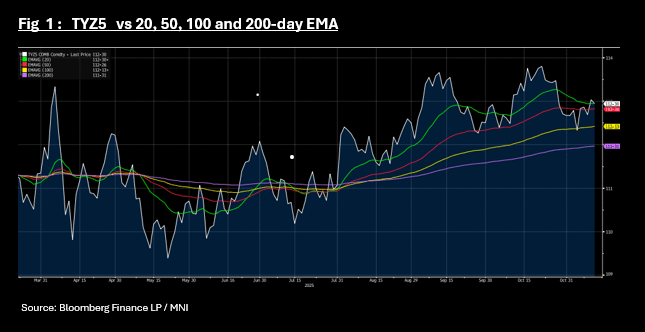

US TSYS: TYZ5 Nears Key Tech Level, Cash Yields Lower Across Curve

US treasury futures were mostly lower along with bond yields in a disjointed, post holiday market. The 10-Yr bond future TYZ5 is down -03 at 112-30, in touch with the 20-day EMA. A break lower could bring the 50-day EMA of 112-26+ into focus.

Cash's morning rally moderated somewhat in the afternoon, but remains a very strong day with bond yields lower across the curve.

- The 2-Yr is at 3.56% (-3.3bps)

- The 5-Yr is at 3.673% (-4.2bps)

- The 10-yr is at 4.083% (-3.5bps)

- The 30-Yr is at 4.683% (-2.3bps)

FED speakers dominate tonight with Williams, Paulson, Waller, Bostic, Miran and Collins all speaking throughout Wednesday, whilst economic data remains on hold.

Investors will focus on the US$42bn 10-Yr issuance as the next guide for market demand, with markets remaining fixated on the US shutdown outcome.

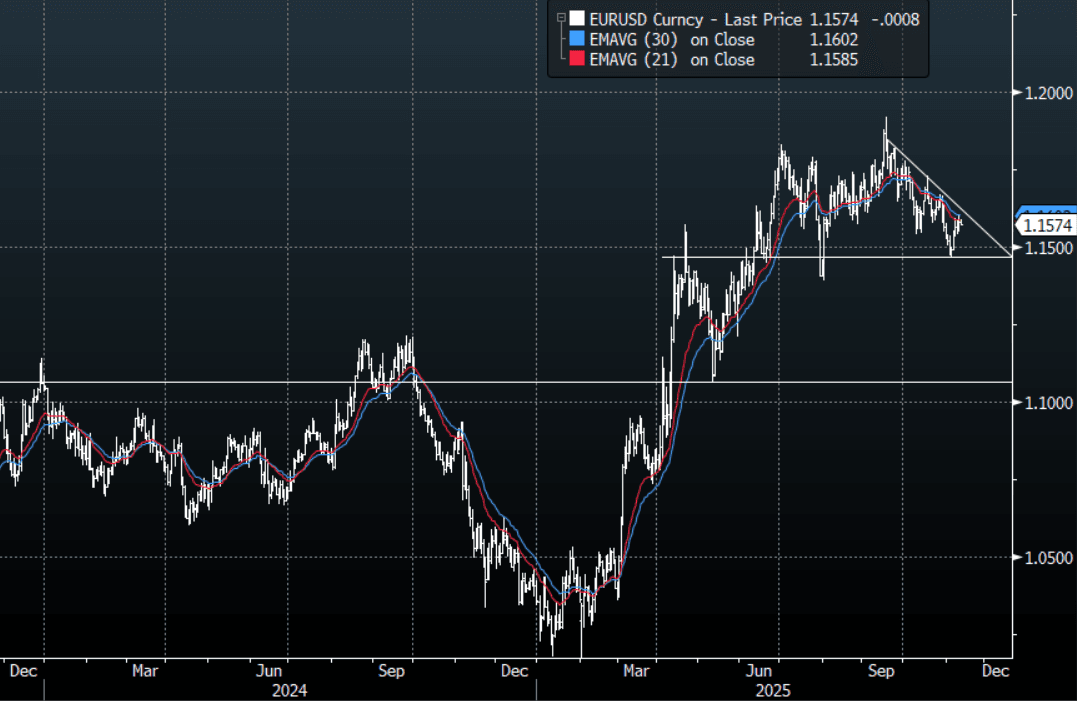

FOREX: Asia-Pac FX: USD Retraces ADP Losses

The BBDXY has had a range today of 1217.77 - 1219.65 in the Asia-Pac session; it is currently trading around 1219, +0.15%.The USD has retraced most of its move lower from overnight in reaction to a weaker ADP print. I am caught a little undecided on the USD at the moment, I liked the fade into 1230 initially but short term I expect dips back toward 1210-1215 to now be supported first up. We could chop around sideways for a while while the market decides which way to go. Above 1230 and we could start to break higher, below 1205 and the downtrends momentum could be re-engaged. Short-term while the 12221/22 area caps price my bias would be for a test toward the 1210-1215 support, above there and the market will look back toward the 1230 area once again.

- EUR/USD - Asian range 1.1571 - 1.1587, Asia is currently trading 1.1572. The pair continued to build on its support below 1.1500, I suspect rallies will now find sellers toward the 1.1650 area initially. This 1.1650-1.1700 area has been the pivot within the larger 1.1400-1.1900 range over the past few months. On the day a move back below 1.1530-1.1540 needed to turn lower again.

- GBP/USD - Asian range 1.3130 - 1.3164, Asia is currently dealing around 1.3130. The pair is trading sideways consolidating on a 1.31 handle. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I suspect the 1.3250-1.3300 area is the place to fade if we see that level again.

- Cross asset : SPX +0.15%, Gold $4110, US 10-Year 4.08%, BBDXY 1219, Crude Oil $60.85

- Data/Events : Germany Wholesale Price Index/CPI/Current Account Balance, Italy Industrial Production,

Fig 1: EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P