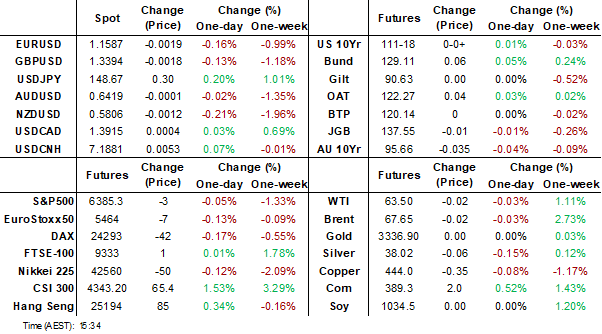

MNI EUROPEAN MARKETS ANALYSIS: USD Firms Ahead Of Jackson Hole

- The USD has mostly tracked higher as the market awaits Fed Chair Powell's speech at Jackson Hole. US yields sit down a touch, led by the front end.

- On the data front, Japan's July CPI was close to expectations, with headline pressures continuing to ease, but core measures remained sticky.

- China equities continue to rally, while the South Korean won bucked the stronger USD trend.

- Looking ahead, global focus turns to Fed Chair Powell’s speech at Jackson Hole. Canada retail sales data are also scheduled.

MARKETS

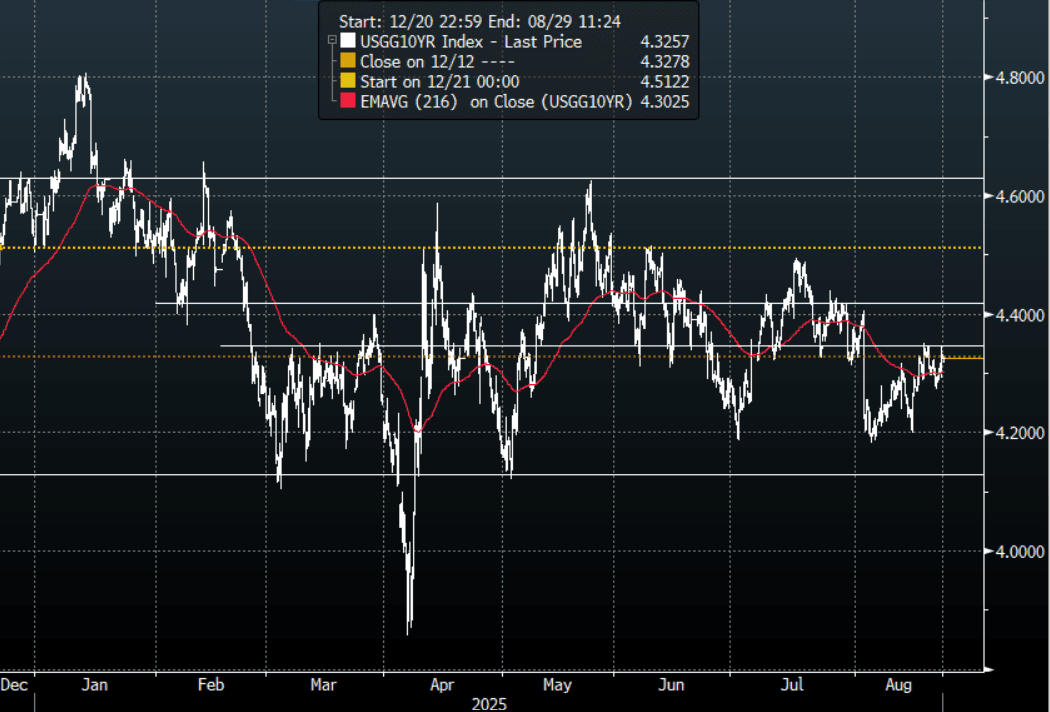

US TSYS: Front-End Edges Lower In Quiet Session

The TYU5 range has been 111-15 to 111-20 during the Asia-Pacific session. It last changed hands at 111-18, up 0-00+ from the previous close.

- The US 2-year yield has edged lower trading around 3.783%, down 0.01 from its close.

- The US 10-year yield is trading around 4.325%.

- 10-Year Yields are still firmly within its wider 4.10%-4.65% range. The 4.35% pivot area continues to hold for now, the market will now be waiting for any clues from Powell's upcoming Jackson Hole speech.

- In the US, all eyes are on Jackson Hole. Known WSJ Fed Watcher Nick Timiraos has published an article titled, "Divisions Grow Inside Fed Ahead of Decision on September Rate Cut - WSJ via BBG". The article presents contrasting views on the Fed outlook, with Cleveland Fed President Beth Hammack stating: ""I see an inflation picture that is too high and rising, and moving in the wrong direction," while adding: " The labor market remains "reasonably good," she said, creating no reason to lower interest rates at the Sept. 16-17 policy meeting."

- Zerohedge on X: “UBS: "All eyes are on Fed Chair Powell’s speech at the Jackson Hole Symposium. While markets are hoping for forward guidance on rate cuts, there’s a growing sense that Powell may deliver a retrospective “exit” speech, potentially disappointing those looking for dovish signals."

- Otavio Costa on X: “The probability of rate cuts has already fallen by nearly 30 percentage points, yet still hovers around 70%. In my view, expectations are likely to shift further — from near-certainty of cuts to none at all. To be clear, this is not supportive for risk assets.”

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

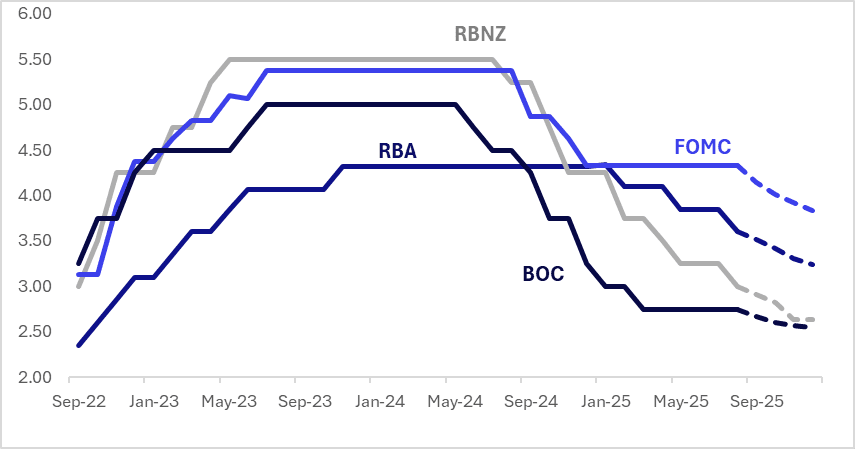

STIR: NZ Outperforms $-Bloc Over Past Week

Interest rate expectations across the $-bloc were mixed over the past week: New Zealand fell sharply by 19bps, the US firmed by 7bps, while Australia and Canada remained largely unchanged.

- In the US, all eyes are on Jackson Hole. Known WSJ Fed Watcher Nick Timiraos has published an article titled, "Divisions Grow Inside Fed Ahead of Decision on September Rate Cut – WSJ via BBG". The article presents contrasting views on the Fed outlook, with Cleveland Fed President Beth Hammack stating: ""I see an inflation picture that is too high and rising, and moving in the wrong direction," while adding: " The labor market remains "reasonably good," she said, creating no reason to lower interest rates at the Sept. 16-17 policy meeting."

- In New Zealand, the MPC believed that spare capacity is now greater and more persistent than expected in May. As a result, the MPC decided to cut rates 25bp to 3% and to give a distinctly dovish message with two members voting for a 50bp reduction. The revised OCR path now troughs 30bp below the May assumption at 2.55%. The Q4 average is at 2.7%, which implies cuts at both the 8 October and 26 November meetings, assuming the economy develops broadly as the RBNZ expected this month.

- Looking ahead, the next major regional events are the FOMC and BoC policy decisions on September 17, with markets assigning a 75% probability to a 25bp cut by the Fed and a 34% probability to a similar move by the BoC.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.84%, -49bps; Canada (BOC): 2.54%, -21bps; Australia (RBA): 3.24%, -36bps; and New Zealand (RBNZ): 2.63%, -37bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: Subdued Session, Market Awaits Jackson Hole

JGB futures are unchanged compared to the settlement levels.

- Japan July nationwide CPI was close to market expectations. Headline printed at 3.1%y/y, in line with market forecasts, while prior was 3.3%. The ex fresh food measure was slightly above expectations at 3.1% (3.0% was forecast and June printed at 3.3%). The ex fresh food, energy core measure was steady at 3.4%y/y, in line with the consensus estimate (3.4% was also the June outcome).

- Cash US tsys are slightly richer, with a steepening bias, in today's Asia-Pac session ahead of Jackson Hole.

- Federal Reserve Chair Jerome Powell will deliver opening remarks at the Kansas City Fed's annual Jackson Hole symposium on Friday at 10 a.m. ET, and Andrew Bailey, Christine Lagarde and Kazuo Ueda, leaders of the Bank of England, ECB and Bank of Japan, respectively, will discuss labour market transition on a panel Saturday at 12:25 p.m. ET.

- Cash JGBs are flat to 1bp cheaper across benchmarks, with a steepening bias.

- Swap rates are flat to 1bp lower, with swap spreads tighter.

- On Monday, the local calendar will see Coincident/Leading Index and Dept Sales data.

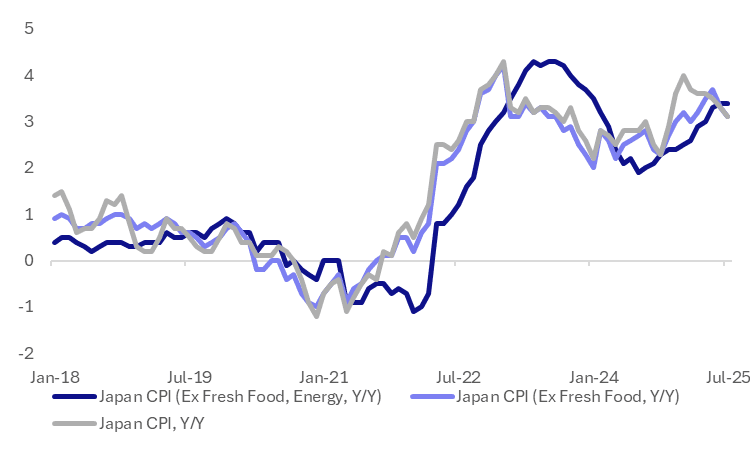

JAPAN DATA: Headline CPI Moderates, Core Measures Stay Sticky

Japan July nationwide CPI was close to market expectations. Headline printed at 3.1%y/y, in line with market forecasts, while prior was 3.3%. The ex fresh food measure was slightly above expectations at 3.1% (3.0% was forecast and June printed at 3.3%). The ex fresh food, energy core measure was steady at 3.4%y/y, in line with the consensus estimate (3.4% was also the June outcome).

- The chart below plots the trends for these inflation metrics. Headline is now comfortably off 2025 highs (3.7%), but core measures are seeing less downside momentum in recent months.

- Still, the core measure which excludes all food and energy was steady at 1.6%y/y, which is where we have been on this metric since March of this year.

- In terms of the m/m outcomes, goods prices rose 0.2%, down slightly from the 0.3% pace seen in June. Services were up 0.1%, after a flat June outcome.

- By sub-category food prices rose 0.4%m/m, although fresh food was down slightly (-0.2%, continuing the recent trend for this sector) Utilities prices are back to falling in m/m terms, off a further 0.8% in July, helping lower headline inflation pressures.

- Clothing was the other soft point, down -1.0%, while other categories were mostly up in m/m terms. Notably entertainment rebound 0.8%, after a 1.0% drop in June. Transport, up 0.6%m/m, was the next strongest result.

- In y/y terms outside of utilities moving to -0.2% from 3.4% in June, there wasn't a big shift relative to June outcomes for the other categories.

- Underlying core pressures remain sticky, particularly the ex fresh food, energy measure. It keeps the BoJ towards further tightening, but it is unlikely to shift thinking ahead of the Sep policy meeting (i.e. that action needs to be taken at that meeting). Note we get August Tokyo CPI next Friday.

Fig 1: Japan CPI Trends Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Cheaper, All Eyes Turn To Jackson Hole

ACGBs (YM -3.0 & XM -3.5) are weaker after a subdued session ahead of Jackson Hole.

- Cash US tsys are slightly richer, with a steepening bias, in today's Asia-Pac session ahead of Jackson Hole.

- Known WSJ Fed Watcher Nick Timiraos has published an article titled, "Divisions Grow Inside Fed Ahead of Decision on September Rate Cut - WSJ via BBG". The article presents contrasting views on the Fed outlook, with Cleveland Fed President Beth Hammack stating: ""I see an inflation picture that is too high and rising, and moving in the wrong direction," while adding: " The labor market remains "reasonably good," she said, creating no reason to lower interest rates at the Sept. 16-17 policy meeting."

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at -1bp.

- The bills strip has bear-steepened, with pricing -1 to -4.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in September is given a 27% probability, with a cumulative 34bps of easing priced by year-end.

- On Monday, the local calendar will be empty, ahead of the RBA Minutes on Tuesday.

- Next week, the AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2028 bond on Friday.

BONDS: NZGBS: Modest Bear-Steepener Ahead Of Jackson Hole

NZGBs closed cheaper but off the session’s worst levels, with benchmark yields 2-4bps higher.

- Cash US tsys are slightly richer, with a steepening bias, in today's Asia-Pac session ahead of Jackson Hole. Federal Reserve Chair Jerome Powell will deliver opening remarks at the Kansas City Fed's annual Jackson Hole symposium on Friday at 10 a.m. ET, and Andrew Bailey, Christine Lagarde and Kazuo Ueda, leaders of the BoE, ECB and BoJ, respectively, will discuss labour market transition on a panel Saturday at 12:25 p.m. ET

- (Bloomberg) – “New Zealand’s central bank should establish a prudential policy committee and appoint new board members with bank regulation expertise, according to a recommendation from a parliamentary inquiry into banking competition.”

- (Bloomberg) - "The Reserve Bank of New Zealand views the recent lull in economic activity as temporary, according to Chief Economist Paul Conway. Conway said the central bank doesn't need to be overtly stimulatory with policy, and that the economy is expected to pick up in response to the current policy settings."

- Swap rates closed modestly higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 1-2bps firmer across meetings. 17bps of easing is priced for August, with a cumulative 35bps by November 2025.

- On Monday, the local calendar will see Retail Sales Ex Inflation data.

FOREX: Asia FX Wrap - USD Extends Higher Into Jackson Hole

The BBDXY has had a range of 1210.14 - 1211.97 in the Asia-Pac session, it is currently trading around 1212, +0.10%. The USD saw further reduction of shorts overnight as we await Powell's speech at Jackson Hole. Depending on the contents of Powell's speech this could change very quickly but the BBDXY looks to be putting in a third higher low which would be a worrying sign to the bears that we could be putting in a short-term base. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. A hawkish tilt from Powell would potentially see these gains extend.

- EUR/USD - Asian range 1.1589 - 1.1617, Asia is currently trading 1.1590. The market is trading sideways in a 1.1600-1.1750 range heading into Jackson Hole. The pair is unlikely to extend too far as the market awaits Powell's speech.

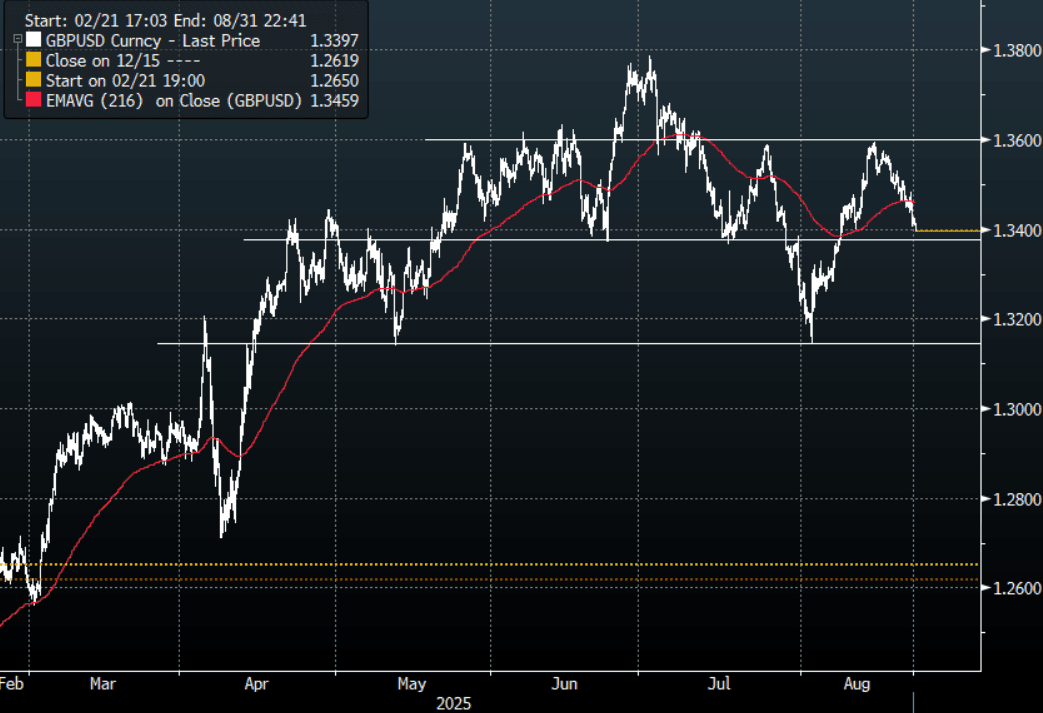

- GBP/USD - Asian range 1.3401 - 1.3423, Asia is currently dealing around 1.3400. Having broken back above its pivot look for dips to again be supported, with risk retracing the pair is probing its first support seen towards 1.3400. A move back below 1.3350 risks a move to the bottom of the range once more.

- USD/CNH - Asian range 7.1817-7.1882, the USD/CNY fix printed 7.1321, Asia is currently dealing around 7.1880. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.01%, Gold $3330, US 10-Year 4.325%, BBDXY 1212, Crude Oil $63.49

- Data/Events : EZ Negotiated Wages, Germany GDP, France Business & Man Confidence/Retail Sales

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

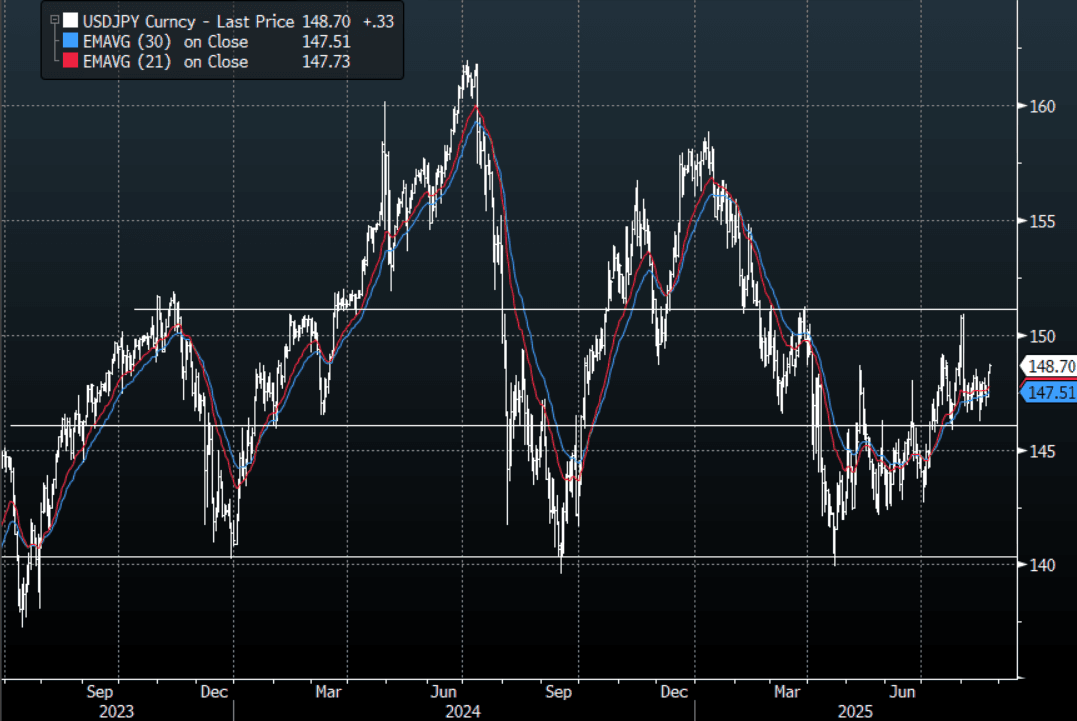

JPY: Asia Wrap - USD/JPY Extends Above 148.50

The Asia-Pac USD/JPY range has been 148.28-148.72, Asia is currently trading around 148.70, +0.22%. USD/JPY managed to push strongly off its 146/147 support area overnight as the USD saw more gains due to the market reducing shorts ahead of Powell's speech. Price still remains firmly within the wider 146.00-151.00 range. CFTC Data shows leveraged funds have bought this dip in USD/JPY betting the support remains intact. The buyers are expecting a more hawkish lean from Powell.

- Japan Headline CPI Moderates, Core Measures Stay Sticky : Japan July nationwide CPI was close to market expectations. Headline printed at 3.1%y/y, in line with market forecasts, while prior was 3.3%. The ex fresh food measure was slightly above expectations at 3.1% (3.0% was forecast and June printed at 3.3%). The ex fresh food, energy core measure was steady at 3.4%y/y, in line with the consensus estimate (3.4% was also the June outcome).

- (Bloomberg) - “The yen looks vulnerable to domestic stagflation and the looming risk of a non-committal Fed. USD/JPY’s tight link with short-term spreads leaves it exposed to shifts in Fed expectations. Traders have recently scaled back bets on a September interest-rate cut thanks to stronger US data. There’s the increasing chance that Powell’s Jackson Hole speech will further push back the prospect of easing.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.90($1.59b).Upcoming Close Strikes : 148.00($912m Aug 26), 147.95($885m Aug 27), - BBG.

- CFTC data shows last week asset managers maintained their JPY longs +60866( Last +60532), leveraged funds used the dip to add to their newly built short JPY position -41257(Last -29308).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

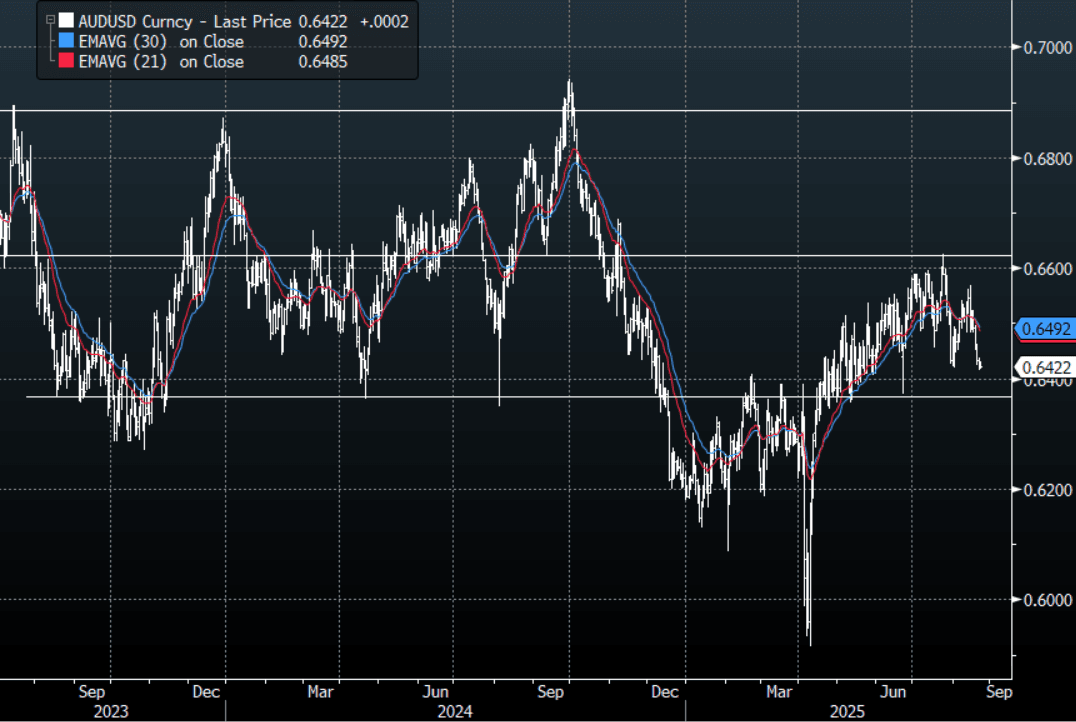

AUD: Asia Wrap - AUD/USD Consolidates Above 0.6400 Into Jackson Hole

The AUD/USD has had a range of 0.6419 - 0.6430 in the Asia- Pac session, it is currently trading around 0.6425, +0.05%. The AUD has traded sideways in an exceptionally quiet session. The AUD is consolidating just above 0.6400 heading into Jackson Hole. Pivotal support is back towards 0.6300/50 which has been the bottom in its recent multi-month range of 0.6350-0.6650.

- Bloomberg - “Nvidia told suppliers Samsung and Amkor to stop production of its H20 AI chip after Beijing urged local firms to avoid using it, The Information reported. Nasdaq futures gave up their gains.”

- “Bank of America expects further downside in the US dollar. The dollar’s July recovery looks to be short-lived as further stagflationary risks are mounting, wrote Alex Cohen, the US bank’s New York-based FX strategist. Potential rate cuts amid increasing inflation create fertile ground for dollar depreciation, while investors also need to contend with the possibility of US data credibility erosion.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD350m). Upcoming Close Strikes : 0.6525(AUD570m Aug 27) - BBG

- AUD/JPY - Asia-Pac range 95.20 - 95.51, Asia is trading around 95.50. The pair found some demand around 94.50 and has bounced overnight, sellers should be around back towards 96.00 now. A sustained break below the 94.00/94.50 area is needed to potentially begin a trend lower again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

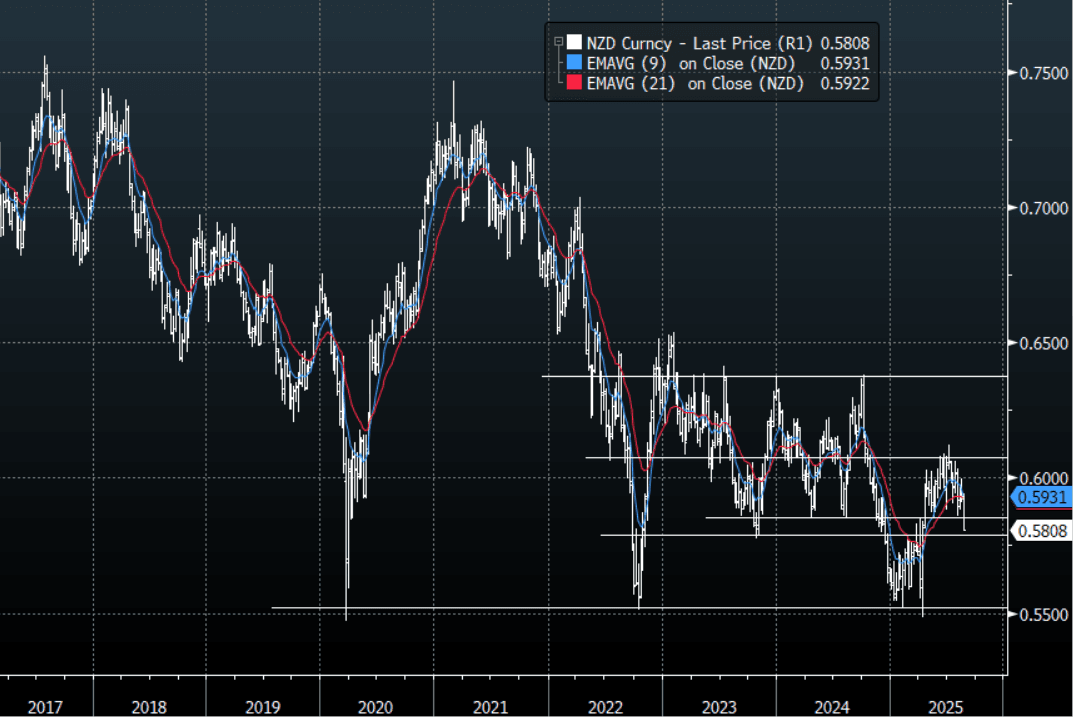

NZD: Asia Wrap - NZD/USD Trades Heavy Still, Just Above 0.5800 Support

The NZD/USD had a range of 0.5808 - 0.5823 in the Asia-Pac session, going into the London open trading around 0.5810, -0.15%. The NZD is consolidating into Jackson Hole just above the pivotal support in the 0.5800 area, but with the break lower on the dovish RBNZ would expect sellers to be around on bounces back toward the 0.5900 area, CFTC data shows lots of room to add to shorts. US Futures have turned lower today on Nvidia, E-minis -0.02%, NQU5 -0.10%.

- (Bloomberg) - “The Reserve Bank of New Zealand views the recent lull in economic activity as temporary, according to Chief Economist Paul Conway. Conway said the central bank doesn't need to be overtly stimulatory with policy, and that the economy is expected to pick up in response to the current policy settings.”

- "NZ AGRICULTURE MINISTER MCCLAY MET WITH US'S GREER THIS WEEK. AGREE DAIRY FARMERS IMPORTANT TO BOTH GOVERNMENTS, STEEL, ALUMINUM, PHARMACEUTICALS TIMBER ALSO DISCUSSED. AGREE TRADE OFFICIALS TO MEET OVER COMING MTHS.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6200(NZD355m Aug 27) - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short adding slightly in the NZD -3679(Last -1811), the Leveraged community though reduced their own shorts slightly -4190(Last -6778).

- AUD/NZD range for the session has been 1.1030 - 1.1051, currently trading 1.1050. The dovish RBNZ has seen the Cross surge higher breaking back above 1.100 convincingly. This move should now see dips supported as it looks to build momentum to push higher.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China Rally Continues, Thailand Up As Ex-PM Thaksin Cleared

The standout so far today in Asia Pac equities is further gains in China mainland stocks. The CSI 300 is up close to 1.2%, putting the index near the 4340 region. Elsewhere trends are mixed. US equity futures sit little changed in the first part of Friday dealings, with all eyes on Fed Chair Powell's speech at Jackson Hole later today US time. Market focus will be on September easing hints, while earlier remarks from Fed Governors showed conflicted viewpoints on the current inflation/labor market trade off (per the WSJ).

- The CSI 300 continues its recent strong rally into the weekend. Earlier headlines that US chip maker Nvidia will suspend producing H20 chips has aided local China chip makers. This development is likely to mean domestic consumers of chips have to rely more on chips made in China. Elsewhere, gains look to mostly reflect better earnings results.

- Onshore media also noted that private funds attracted strong inflows into local stocks in July: China’s private securities investment funds attracted over 100 billion yuan (approximately $13.9 billion) in fresh capital in July, as investors flocked to equity-focused products amid signs of recovery in the domestic stock market, Shanghai Securities News reports." (via BBG)

- The HSI is up as well, last around 0.30% higher.

- Japan markets are mixed, with the Topix up 0.4%, but the NKY 225 down 0.15%. July inflation data saw headline pressures ease as expected, while core measures remained sticky.

- In Thailand, ex-PM Thaksin was cleared of a Royal insult charge, although this ruling may be appealed. We also have further political cases coming up in Thailand. Still, the SET is up around 0.90% so far, with a good bulk of the move since the Thaksin headlines crossed.

- Most other SEA markets are up at this stage, while India has opened down. Australia and NZ are weaker, with NZ curbing post RBNZ gains from earlier this week.

ASIA STOCKS: Taiwan Outflows Exceed $3bn In Past Week, Thailand Flows Negative

Despite a rebound in Taiwan equities yesterday, offshore investors continued to pare back recent inflows. We saw a further $411mn in net outflows, bringing outflows in the past 5 day trading days to over $3.2bn. This has also significantly curbed YTD inflows for the local market. South Korea also saw outflow pressures continue yesterday, albeit at a fairly modest pace. Key global tech equity indices finished down in Thursday trade, but losses weren't as large compared to earlier in the week. The key near term focus will likely rest with Powell's speech tonight at Jackson Hole, with focus on hints around whether the Fed will ease at the September meeting.

- Elsewhere, Indian flows have returned to modest outflow pressures, leaving the 5 -day sum as a touch negative.

- The recent bias has also been for outflow pressures from Thailand. Since Aug 13 we have had outflows each trading day. The SET index sits off recent highs but has stabilized somewhat in recent sessions. A series of three high-profile court cases scheduled to take place in quick succession over the next few weeks represents a critical juncture in Thailand’s political cycle. See this link for more details.

- Malaysian outflows continued, but Indonesian inflows remained a bright spot for the region yesterday.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -59 | -925 | -5392 |

| Taiwan (USDmn) | -411 | -3233 | 1257 |

| India (USDmn)* | -34 | -58 | -12756 |

| Indonesia (USDmn) | 42 | 223 | -3191 |

| Thailand (USDmn) | -86 | -153 | -2073 |

| Malaysia (USDmn) | -13 | -156 | -3470 |

| Philippines (USDmn)* | 3 | -21 | -617 |

| Total (USDmn) | -559 | -4323 | -26243 |

| * Data Up To Aug 20 |

Source: Bloomberg Finance L.P/MNI

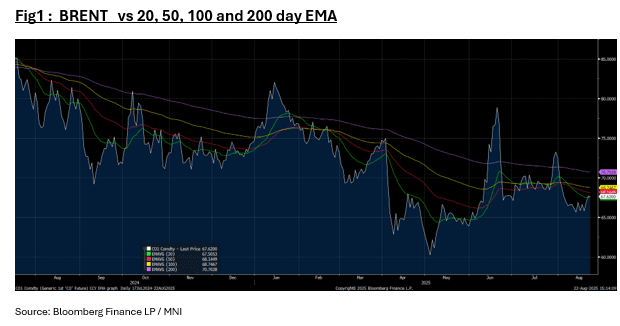

Oil Trending Sideways into Weekend

- Oil prices have done very little in the Asia trading day despite further headlines from the Trump administration.

- Comments from the Trump administration that they expected additional tariffs on India as a result of the country's Russian crude purchases had driven prices higher overnight but that momentum stalled in Asia. This came as India pledged to keep buying Russian oil "depending on the financial benefit", according to Vinay Kumar, India's ambassador in Moscow.

- Elsewhere, Asian oil refiners have been buying crude from further afield, including the US, Brazil, and Nigeria, due to President Donald Trump's trade and foreign policy approach.

- The region that consumes around 35-40% of the world's oil historically buys the majority of its supply from the middle east. However US trade and foreign policy has seen purchases from the US to Brazil and Nigeria increase.

- Norway's second-biggest oil and gas company Aker BP ASA said exploration in the Norwegian North Sea resulted in one of the largest discoveries of oil made on the continental shelf in the last decade.

- WTI is steady at US$63.50 bbl to remain over 1% higher for the week. It remains however below all major moving averages, the nearest being the 20-day EMA of $64.36.

- Brent is trading around where it started at US$67.60 in the Asia trading day. Brent has had a very strong week, up over +2.6% which has seen it trade above the 20-day EMA of $67.50.

Gold Down Modestly Ahead of Jackson Hole

- Gold fell in Asia trading today as it waited for signals on interest rates from Jackson Hole.

- Gold is down -0.30% at US$3328.92 and remains below the all time high in June of $3,432.

- Gold had clung on to minor weekly gains, however today's falls puts it down by -0.20% for the week.

- Gold has traded in tight ranges this week and remains wedged between the 20-day EMA of $3,344.20 and the 50-day EMA of $3,334.50

- Swiss gold exports to the US surged last month to the highest since March, with shipments of bullion jumping to almost 51 tons in July. Record bullion exports worth more than $36 billion made up more than two-thirds of Switzerland's trade surplus with the US in the first quarter.

- Gold is expected to hold onto gains into 2026 following a rally to a record earlier this year, Australia's biggest listed miner of the metal said after reporting that full-year profit more than doubled

MALAYSIA: Country Wrap: CPI Up, Remains Below Target

- Malaysia's CPI release for July came in at +1.2%, slightly up on June's +1.1%. Core CPI YoY is at +1.8%. Food and alcoholic bevs +1.9%YoY, Housing Water and Electricity +1.3%, recreation services and culture +0.8%YoY and Transport +0.4% YoY. The Bank Negara CPI target band for 2025 is 2.0% - 3.5% and this is the 12th consecutive print below the lower band. The BNM cut rates by 25bps at their last meeting in July and does not meet again until September 04. (source MNI)

- The Malaysian government continues efforts to attract investments to special economic zones as part of the 13MP. The economy minister noted the focus remains on electronics industries, natural resources, cargo and trade and rubber based industries (source Bernama)

- The FTSE Malay KLCI is up +0.32% today and on track for a positive week. Rising 4 out of the five trading days, the SE bourse is set to deliver over +1.3% of gains.

- The Ringgit is down -0.13% today at 4.2310 as most regional crosses were weak. The Ringgit is down -0.45% over the last five trading days in what has been a data light week in Malaysia.

- Bonds had rallied leading into today's CPI with the 10-year initially -3bps tigher for the week. However post the marginally higher than expected CPI they have given back those gains and the 10-year is on track to finish flat for the week at 3.39%

CHINA: Country Wrap: China Focused on Steady Growth

- China is confident and well-prepared to continue promoting steady growth in and improving the quality of foreign trade, the Ministry of Commerce said Thursday. Currently, global economic and trade development continues to face significant uncertainties, with multiple international organizations noting that tariff barriers have substantially increased global trade costs, ministry spokesperson He Yongqian told a press conference. These tariff barriers have seriously affected the efficiency and stability of global industrial and supply chains, posing downward risks to global trade, the spokesperson said. (source China Daily)

- China has launched a pilot program for green foreign debt financing in a bid to attract the inflow of global capital into the country's green sector. (source Xinhua)

- The major China bourses have delivered gains Friday but remain mixed over the week. The Hang Seng is up +0.32% at yet remains down for the week by -0.30% after falling 3 out of the five trading days. The CSI 300 is up +1.25% today and +3.31% for the week. Shanghai is up +0.70% today and +2.7% for the week and Shenzhen is better by +0.85% and +3.3% week to date.

- Yuan Reference Rate at 7.1321 Per USD; Estimate 7.1874

- The CGB 10-year is at 1.76%, +2bps higher for the week.

SOUTH KOREA: Country Wrap: Further Housing Restrictions to Come

- The government said Thursday it will impose restrictions on housing purchases by foreigners in Seoul, Incheon and major parts of Gyeonggi Province in an effort to block speculative demand fueled by overseas capital inflows. The Ministry of Land, Infrastructure and Transport said the measure to place foreign home buyers subject to the Real Estate Transaction Reporting Act was approved at a meeting of the Central Urban Planning Committee earlier in the day. (source Yonhap)

- The Bank of Korea is expected to maintain its accommodative stance, despite tailwinds from the U.S.-South Korean deal to lower President Trump's blanket tariff and signs of a recovery in consumption, Nomura economists led by Jeong Woo Park write in a note. The central bank is likely to remain cautious about South Korea's recovery path because tariffs could still adversely affect exports later, they say. Nomura expects the bank to revise up its 2025 and 2026 GDP growth forecasts to 0.9% and 1.8%, respectively, from 0.8% and 1.6% previously. The BOK is likely to hold the policy rate next week before possibly cutting it in October, Nomura says. (source BBG)

- The KOSPI is up today by +0.86% and has made a minor recovery from losses earlier in the week. However it remains lower and is set to lose ground by around -1.7% for the week.

- The Won is the best of the regional performers today, as most lost ground. With gains of +0.45% it marks a modest turnaround from earlier in the week yet remains down by -0.30% in the last five trading days.

- Korea's 10-year Govt Bond is +6bps higher in yield this week following one of the largest 10-year government bond auctions of the year at the beginning of the week.

ASIA FX: USD/TWD Firms Again, USD/KRW Finds Selling Interest Near 1400

In North East Asia FX, trends have been mixed. USD/TWD has climbed higher, but now sits off session highs. USD/CNH is up but remains within recent ranges. USD/HKD is also firmer, trending back towards 7.8200. USD/KRW is lower though bucking these trends.

- Spot USD/TWD has continued its recent trend move higher, the pair getting to 30.68 before selling interest emerged. We were last at 30.59, still down 030% in TWD terms for the session. Weekly losses are close to 2%. Local equities are back lower today, while the past trading week has seen over $2.3bn in equity outflows from offshore investors. This, along with a firmer USD backdrop more broadly, have weighed on TWD. We are through all key EMAs except the 200-day, which is around 31.02 on the topside.

- USD/KRW spot got to lows of 1391.2 in earlier dealings before stabilizing. We were last near 1393/94, around 0.40% stronger in won terms. We didn't see any fresh headline drivers for the move, and it looked isolated compared to other USD/Asia moves, or the G10. Resistance has been evident in the pair around the 1400 level so far this week, albeit with a brief test above this level in Thursday trade. The Kospi is tracking higher, while offshore investors have purchased around $142mn of local stocks today, which could be supports.

- USD/CNH has firmed, last near 7.1890. This is short of recent highs (7.1931) but fits with the generally firmer USD tone seen against the majors.

- USD/HKD spot is pushing higher, last at 7.8175. The recent bounce is outperforming some US-HK yield differential trends. The 3 mth spread is only marginally above recent lows, last +158bps. HKD T/N pts are still negative at -3.86.

ASIA FX: THB Reacts Little To Ex PM Thaksin Being Cleared, USD Firms Elsewhere

In South East Asia markets, the bias has been for a firmer USD, with dollar gains in the 0.20-0.30% region. This fits with the trends seen for the majors, where the dollar is gravitating higher ahead of Powell's Jackson Hole speech later.

- USD/THB is trading with a positive bias in the first part of Friday dealings, like most other parts of the region. The pair was last around 32.66, up 0.15% versus end Thursday levels. This is fresh highs back to early August and through the 50-day EMA resistance point. The 100-day EMA is further north, close to 32.87. Headlines crossed earlier that ex-PM Thaksin has been cleared of a Royal Family insult charge. FX reaction was limited, while onshore equities pushed higher. However, there are other up-coming cases which could still create political instability. Other headlines have crossed from the Deputy FinMin that tax measures to boost consumption before year end are being considered.

- USD/IDR is up around 0.35%, putting the pair into the 16340/45 region, fresh multi week highs. The 1 month NDF is little changed though, so this largely looks like catch up to USD gains from Thursday's session.

- Onshore Philippine markets have returned, with USD/PHP rebounding back above 57.00, but it remains within recent ranges.

- USD/MYR is above 4.2300 in latest dealings, earlier highs were close to 4.2360. Today's CPI underscored the weakness in inflation and for some domestic observers points to a need for further monetary policy action.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 22/08/2025 | 0600/0800 | ** | Unemployment | |

| 22/08/2025 | 0600/0800 | *** | GDP (f) | |

| 22/08/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 22/08/2025 | 0900/1100 | Q2 Negotiated Wage Growth | ||

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1400/1000 | Fed Chair Jerome Powell | ||

| 22/08/2025 | 1400/1000 | *** | US Fed Chair Speech | |

| 22/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 22/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |