BONDS: NZGBS: Modest Bear-Steepener Ahead Of Jackson Hole

NZGBs closed cheaper but off the session’s worst levels, with benchmark yields 2-4bps higher.

- Cash US tsys are slightly richer, with a steepening bias, in today's Asia-Pac session ahead of Jackson Hole. Federal Reserve Chair Jerome Powell will deliver opening remarks at the Kansas City Fed's annual Jackson Hole symposium on Friday at 10 a.m. ET, and Andrew Bailey, Christine Lagarde and Kazuo Ueda, leaders of the BoE, ECB and BoJ, respectively, will discuss labour market transition on a panel Saturday at 12:25 p.m. ET

- (Bloomberg) – “New Zealand’s central bank should establish a prudential policy committee and appoint new board members with bank regulation expertise, according to a recommendation from a parliamentary inquiry into banking competition.”

- (Bloomberg) - "The Reserve Bank of New Zealand views the recent lull in economic activity as temporary, according to Chief Economist Paul Conway. Conway said the central bank doesn't need to be overtly stimulatory with policy, and that the economy is expected to pick up in response to the current policy settings."

- Swap rates closed modestly higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 1-2bps firmer across meetings. 17bps of easing is priced for August, with a cumulative 35bps by November 2025.

- On Monday, the local calendar will see Retail Sales Ex Inflation data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap - BBDXY Looks Heavy Below 1200

The BBDXY has had a range of 1195.19 - 1197.06 in the Asia-Pac session, it is currently trading around 1196, +0.05%. The USD again fell very easily overnight, aided by the move lower in US yields. The market is much more comfortable selling USD’s, while below 1220 rallies should continue to find supply. What stands out overnight though is the USD could not move higher while the risk of Powell being removed hung over its head, last night both Trump and Bessent pulled back from that scenario and intimated Powell would complete his term. US yields have moved lower as a result taking the USD with it, does that mean the USD now goes down in all scenarios ?

- EUR/USD - Asian range 1.1731 - 1.1749, Asia is currently trading 1.1735. The pair bounced off its first support around the 1.1600 area. The price still looks a little stretched in the short term, first support around 1.1550/1600 then more importantly the 1.1450 area.

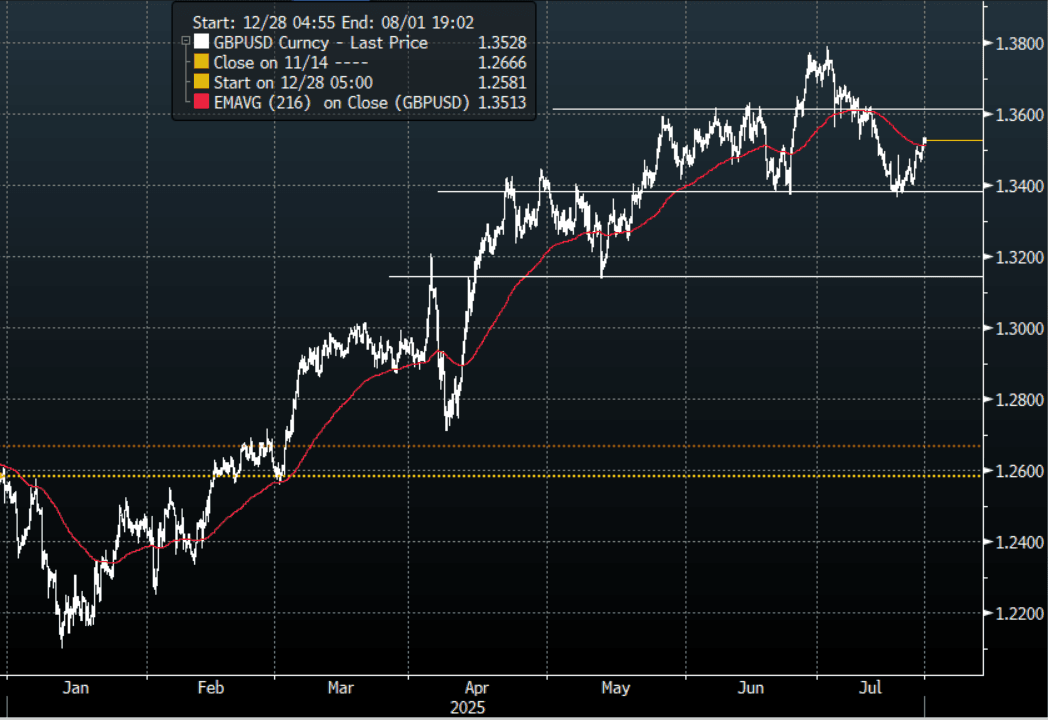

- GBP/USD - Asian range 1.3517 - 1.3535, Asia is currently dealing around 1.3525. The support around 1.3350/1.3400 has proved to be solid first up. Bounces back towards 1.3500/1.3550 should now see offers initially. While the support holds the market will be encouraged to continue to play from the long side.

- USD/CNH - Asian range 7.1592 - 7.1727, the USD/CNY fix printed 7.1414, Asia is currently dealing around 7.1600. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.25%, Gold $3423, US 10-Year 4.364%, BBDXY 1206, Crude oil $65.54

- Data/Events : EZ Consumer Confidence

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

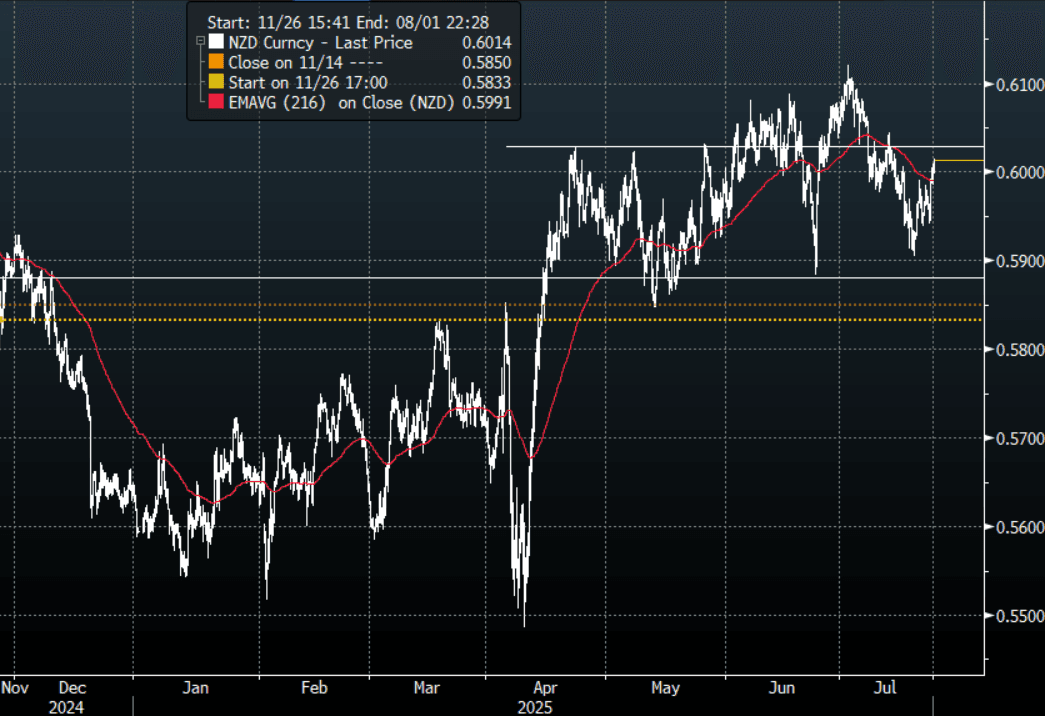

NZD: Asia Wrap - NZD/USD Pushing Back Above 0.6000, Can It Put A Base In?

The NZD/USD had a range of 0.5985 - 0.6014 in the Asia-Pac session, going into the London open trading around 0.6015, +0.20%. The pair had a decent move higher in the New York session as the USD came back under pressure with US yields pushing lower. Depending what your view is this 0.6020/0.6050 area looks an attractive fade, the danger though is the USD which is looking sickly once more and should it capitulate the NZD could build momentum higher again. Price will need a sustained break back above the 0.6025/50 area to signal a potential base might be in place.

- Satish Ranchhod(Westpac) on LinkedIn: “Inflation in New Zealand has picked up to 2.7%, and it’s on course to rise back up to around 3% by the end of this year, it’s a mixed picture under the surface. With softness in demand, we are seeing lower inflation in parts of the domestic economy, especially the housing sector. However, we’re continuing to see large increases in administered prices like council rates and electricity charges. At the same time, import prices are starting to push higher again. We continue to expect another 25bp cut from the RBNZ in August. However, with headline inflation pushing higher, the RBNZ will be cautious about the extent and timing of any further rate cuts.”.

- (Bloomberg) -- RBNZ publishes new residential mortgage lending data for June, on its website. Lending to all borrowers NZ$8.26b, Gains 47% y/y, Increases 3.5% m/m after seasonal adjustment: RBNZ.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6010(NZD302m July 24). - BBG

- CFTC Data shows Asset Managers slightly reduced their newly built longs in NZD +8192, the Leveraged community has continued to reduce their shorts last week -6744.

- AUD/NZD range for the session has been 1.0915 - 1.0940, currently trading 1.0920. The cross moved higher in response to the NZ CPI. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: Crude Supported By US-Japan Deal But Focus Now On China & EU

While oil markets are off their highs following the announcement of a US-Japan trade deal, they are still up today but continue to range trade. WTI is 0.4% higher at $65.54/bbl after reaching $65.82 earlier, while Brent is +0.3% to $68.77/bbl following a peak of $69.10. The USD index is slightly higher.

- US imports from Japan, including autos, will face a 15% tariff down from the 24% announced in April but higher than the current average below 5%. This lower rate is in exchange for $550bn of Japanese investment in the US.

- Attention remains on negotiations with the EU and China. Treasury Secretary Bessent is scheduled to meet China officials in Stockholm next week with the aim of extending the current hold on tariffs beyond August 12. The talks may also include China’s continued consumption of Russian and Iranian crude.

- Industry-based data showed a small US crude inventory drawdown with a larger one for gasoline but distillate was higher. The official EIA data is out later today and while the supply/demand balance remains a concern is likely to be a focus.

- Malaysia has decided not to cut fuel subsidies and the price of RON95 fuel will actually fall to MYR 1.99/L as part of a package to support households.

- Later June US existing home sales and preliminary July euro area consumer confidence print.