ASIA STOCKS: China Rally Continues, Thailand Up As Ex-PM Thaksin Cleared

The standout so far today in Asia Pac equities is further gains in China mainland stocks. The CSI 300 is up close to 1.2%, putting the index near the 4340 region. Elsewhere trends are mixed. US equity futures sit little changed in the first part of Friday dealings, with all eyes on Fed Chair Powell's speech at Jackson Hole later today US time. Market focus will be on September easing hints, while earlier remarks from Fed Governors showed conflicted viewpoints on the current inflation/labor market trade off (per the WSJ).

- The CSI 300 continues its recent strong rally into the weekend. Earlier headlines that US chip maker Nvidia will suspend producing H20 chips has aided local China chip makers. This development is likely to mean domestic consumers of chips have to rely more on chips made in China. Elsewhere, gains look to mostly reflect better earnings results.

- Onshore media also noted that private funds attracted strong inflows into local stocks in July: China’s private securities investment funds attracted over 100 billion yuan (approximately $13.9 billion) in fresh capital in July, as investors flocked to equity-focused products amid signs of recovery in the domestic stock market, Shanghai Securities News reports." (via BBG)

- The HSI is up as well, last around 0.30% higher.

- Japan markets are mixed, with the Topix up 0.4%, but the NKY 225 down 0.15%. July inflation data saw headline pressures ease as expected, while core measures remained sticky.

- In Thailand, ex-PM Thaksin was cleared of a Royal insult charge, although this ruling may be appealed. We also have further political cases coming up in Thailand. Still, the SET is up around 0.90% so far, with a good bulk of the move since the Thaksin headlines crossed.

- Most other SEA markets are up at this stage, while India has opened down. Australia and NZ are weaker, with NZ curbing post RBNZ gains from earlier this week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Asia Wrap - AUD/USD Moves Higher As Risk Reacts Positively To Trade Deal

The AUD/USD has had a range of 0.6548 - 0.6569 in the Asia- Pac session, it is currently trading around 0.6565, +0.15%. The pair pushed higher in the New York session as the USD came back under pressure with US yields pushing lower. The follow through below 0.6500 was quite disappointing for AUD shorts but with Stocks making new highs and risk outperforming, it makes it a hard environment for AUD/USD to collapse in. The pair looks to be consolidating in a 0.6450 - 0.6600 range as the market awaits a catalyst to provide clearer direction.

- AUSTRALIA DATA: Westpac Lead Indicator Signals Around Trend Growth. The Westpac lead indicator for June fell 0.03% m/m following an upwardly-revised 0.05% rise. The 6-month rate, which leads detrended growth by 3 to 9 months, is hovering just above zero signalling that growth is likely to return to around trend towards year end. Westpac believes that sluggish growth and the Q2 CPI outcome on July 30 will enable the RBA to cut 25bp on August 12 but it will maintain a “gradual easing cycle”.

- (Bloomberg) -- Australia’s economy will expand 0.5% in 2Q, according to the latest median estimate from a Bloomberg News survey conducted from July 17 to July 22.

- "AUSTRALIAN PRUDENTIAL REGULATION AUTHORITY - KEEPS ITS MACROPRUDENTIAL POLICY SETTINGS STEADY" - RTRS

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD603m), 0.6500(AUD445m), 0.6580(AUD403m) . Upcoming Close Strikes : none - BBG

- CFTC Data shows Asset managers have maintained their shorts -38267, the Leveraged community added slightly to their shorts to -20048.

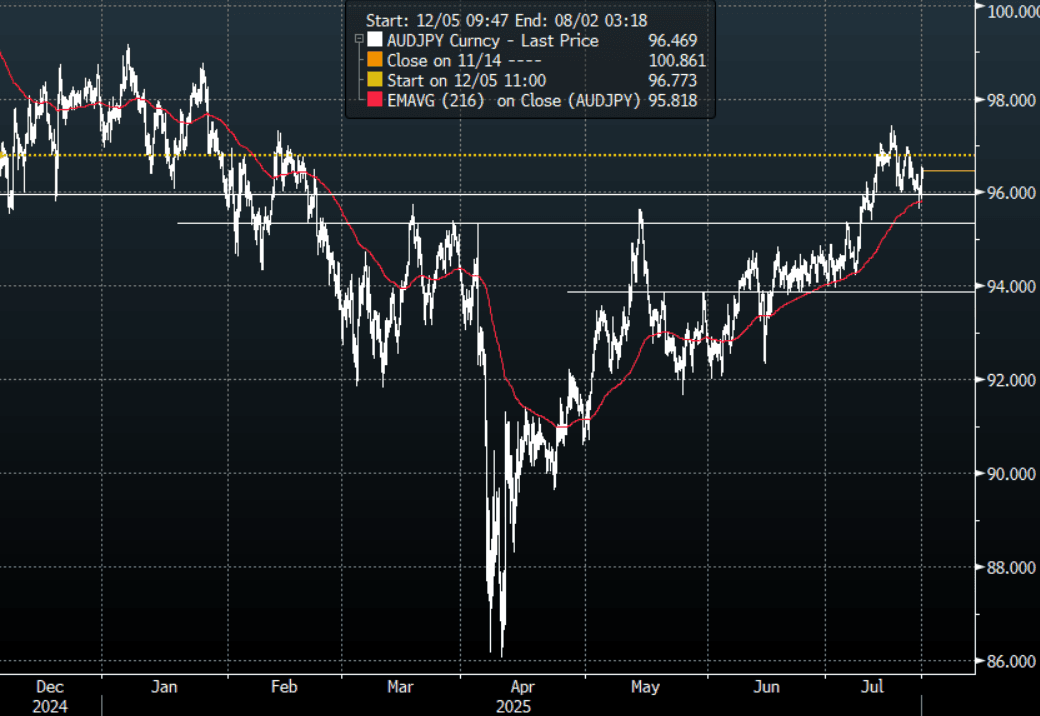

- AUD/JPY - Today's range 95.85 - 96.55, it is trading currently around 96.45, +0.35%. The pair continued to trade heavily overnight. The support has held between 95.00 - 96.00, demand has materialised first up, and the trade deal between the US and Japan should provide it with some tailwinds initially.

Fig 1: AUD/JPY spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Asia Wrap - Yields Move Higher, Led By The Long-End

The TYU5 range has been 111-06 to 111-10+ during the Asia-Pacific session. It last changed hands at 111-07, down 0-06 from the previous close.

- The US 2-year yield has edged higher trading around 3.844%, up 0.01 from its close.

- The US 10-year yield has moved higher trading around 4.365%, up 0.02 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, expect supply around 4.30/35% first up. A close back below 4.30% would begin to get the bulls excited once more and the chopfest within the range will continue.

- Nick Timiraos on X: Goldman: "Market participants seem to agree that the risk to Fed independence is rising, as 5-year 5-year forward inflation swaps have recently decoupled higher from their prior close relationship with the 2-year note yield."

- Bloomberg - “Lawrence Summers backed Scott Bessent’s questioning of the Fed’s non-monetary policy activities, saying that there were some areas that are distinct from the broader issue of central bank independence.”

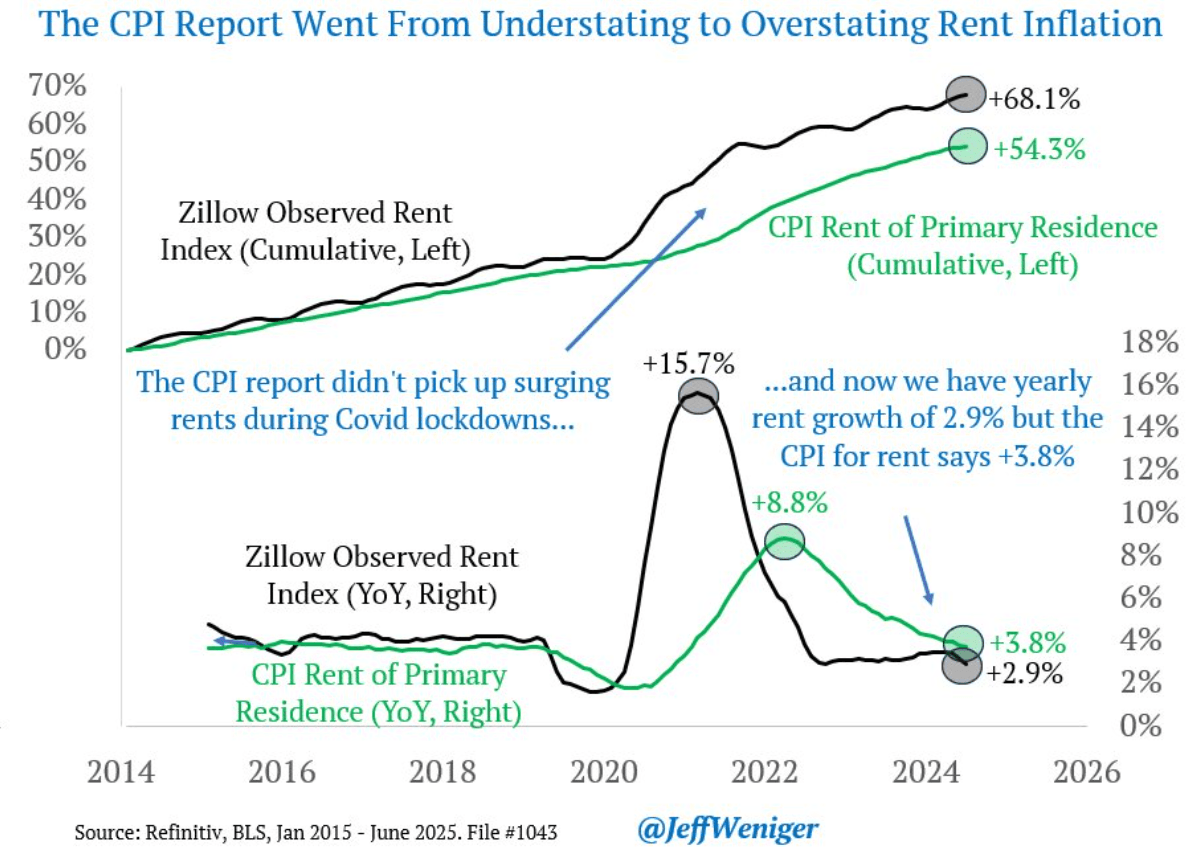

- Jeff Weniger on X: “Understand this and you'll be ahead of 99% of the public on official inflation dynamics. Similar to work by my WisdomTree colleague @JeremyDSchwartz, we see that the CPI for rent is still playing catch-up after the Covid money splash. The CPI reports of 2025 are overstating rent and will continue to do so until the catch-up is complete.” See Graph Below.

Data/Events: MBA Mortgage Applications, Existing Home Sales

Fig 1: CPI Vs CPI For Rent

Source: MNI/@JeffWeniger/Refinitiv

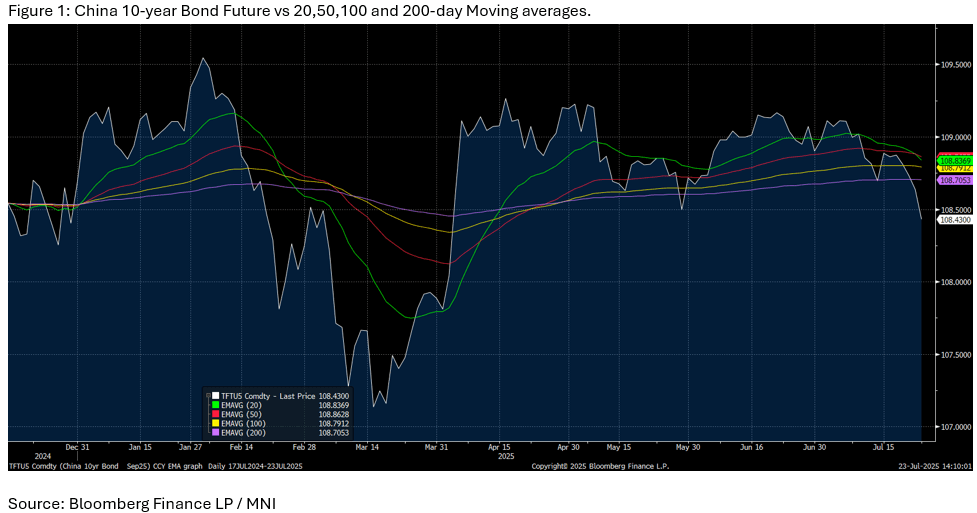

CHINA: Bond Futures Down Heavily in Morning Session

- China bond futures are down in the morning session with the 10-year having its largest one day fall since May.

- The 10-year is down -0.20 at 108.43 and has traded below all major moving averages which it had not done since late May.

- The PBOC withdrew liquidity during this morning's OMO marking three consecutive days of withdrawals.

- The 2-year future is also down, by -0.04 to 102.36 and remains below all major moving averages. The nearest being the 20-day EMA of 102.43.

- The 10YR CGB is higher by +1.5bp to 1.71%