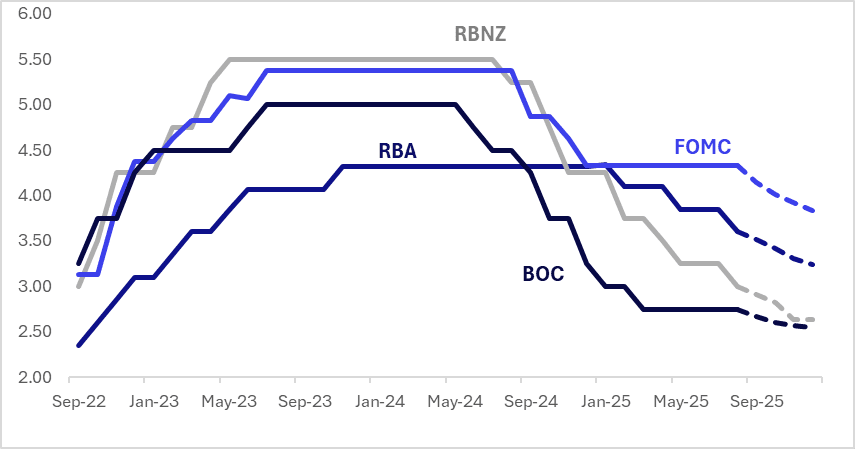

STIR: NZ Outperforms $-Bloc Over Past Week

Interest rate expectations across the $-bloc were mixed over the past week: New Zealand fell sharply by 19bps, the US firmed by 7bps, while Australia and Canada remained largely unchanged.

- In the US, all eyes are on Jackson Hole. Known WSJ Fed Watcher Nick Timiraos has published an article titled, "Divisions Grow Inside Fed Ahead of Decision on September Rate Cut – WSJ via BBG". The article presents contrasting views on the Fed outlook, with Cleveland Fed President Beth Hammack stating: ""I see an inflation picture that is too high and rising, and moving in the wrong direction," while adding: " The labor market remains "reasonably good," she said, creating no reason to lower interest rates at the Sept. 16-17 policy meeting."

- In New Zealand, the MPC believed that spare capacity is now greater and more persistent than expected in May. As a result, the MPC decided to cut rates 25bp to 3% and to give a distinctly dovish message with two members voting for a 50bp reduction. The revised OCR path now troughs 30bp below the May assumption at 2.55%. The Q4 average is at 2.7%, which implies cuts at both the 8 October and 26 November meetings, assuming the economy develops broadly as the RBNZ expected this month.

- Looking ahead, the next major regional events are the FOMC and BoC policy decisions on September 17, with markets assigning a 75% probability to a 25bp cut by the Fed and a 34% probability to a similar move by the BoC.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.84%, -49bps; Canada (BOC): 2.54%, -21bps; Australia (RBA): 3.24%, -36bps; and New Zealand (RBNZ): 2.63%, -37bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

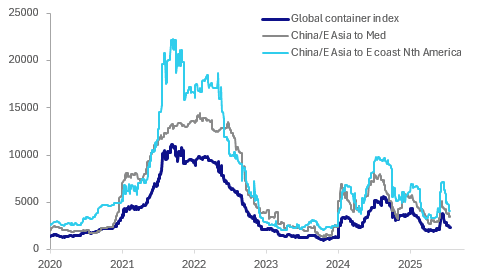

GLOBAL MACRO: July Sees Unwinding Of Sharp June Rise In Container Rates

Global container shipping rates have reflected the changes in demand related to US tariff deadlines but are down sharply compared to a year ago. Bloomberg container ship tracking data showed that departures were up in June ahead of the earlier July 9 deadline, but vessels departing for the US are down again in July. The tariff date was shifted to August 1.

Global FBX container rates USD/points

- Container shipping rates spiked in June, particularly for the China/East Asia to east coast of North America route. The total rose 57.5% m/m with the latter up 77.9% m/m. In contrast, the month average for July is down 26% m/m and 32.5% m/m respectively.

- Both indices are down over 50% on the year, which should help alleviate some cost pressures. Risks to shipping in the Red Sea drove a sharp increase in H1 2024, which has now dissipated.

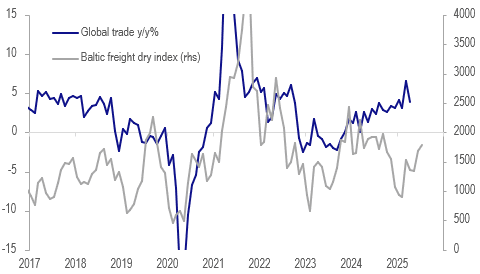

- While the Baltic Freight dry index (bulk commodity rates) also rose sharply in June (+25.3% m/m), it has continued to climb this month up another 6% m/m. It can be a lead indicator of global trade trends and it currently suggests that despite heightened uncertainty, it should hold up for now. Trade grew 3.8% y/y in April with exports up 4.7% y/y.

Global trade vs Baltic Freight Index

JAPAN: Local Media States PM Ishiba To Resign In August

Headlines have crossed from local newspaper Mainichi that PM Ishiba will resign by the end of August. Via Rtrs: "Japan's Prime Minister Shigeru Ishiba has made up his mind to resign, Mainichi newspaper reported on Wednesday."

- Earlier PM Ishiba wouldn't be drawn on speculation around his future, stating that he would assess the US-Japan trade deal details before making any decision.

- Still, in the aftermath of the weekend upper house result, which saw the ruling LDP coalition lose its majority, Ishiba's future has been speculated on.

- His removal odds per Polymarket has remained elevated this week, but sub recent highs.

- The market reaction has been for USD/JPY to rise, testing up through 147.00 (highs were at 147.20, but we sit back near 147.00 in latets dealings)Japan equities have also rallied further.

- JGB yields are higher across the curve so far today, with focus on the 40yr debt auction in a little while. Risks around fiscal slippage for Japan will remain elevated if Ishiba resigns.

JGBS AUCTION: 40Y Supply Faces Higher Yield But Flatter 10/40 Curve

The Japanese Ministry of Finance (MoF) is set to auction 400 billion of 40-year JGBs today. The previous 40-year auction of 500 billion was held on 28 May 2025.

- Today’s auction follows the announcement of a new trade deal between the U.S. and Japan. President Trump stated that Japan will invest $550 billion into the U.S. and open its markets further to U.S. car and agricultural exports. As part of the deal, Japan will impose a 15% reciprocal tariff on U.S. goods, lower than the previously threatened 25% rate.

- Cash JGBs are 3–8bps cheaper across the curve, with the benchmark 40-year yield up 3.4bps to 3.411%, compared to its recent cycle high of 3.60%.

- The current 40-year auction yield is tracking about 30bps higher than the previous auction.

- However, the 10s40s curve has flattened 30bps since reaching its recent peak.

- Results are due at 0435 BST / 1235 JST.