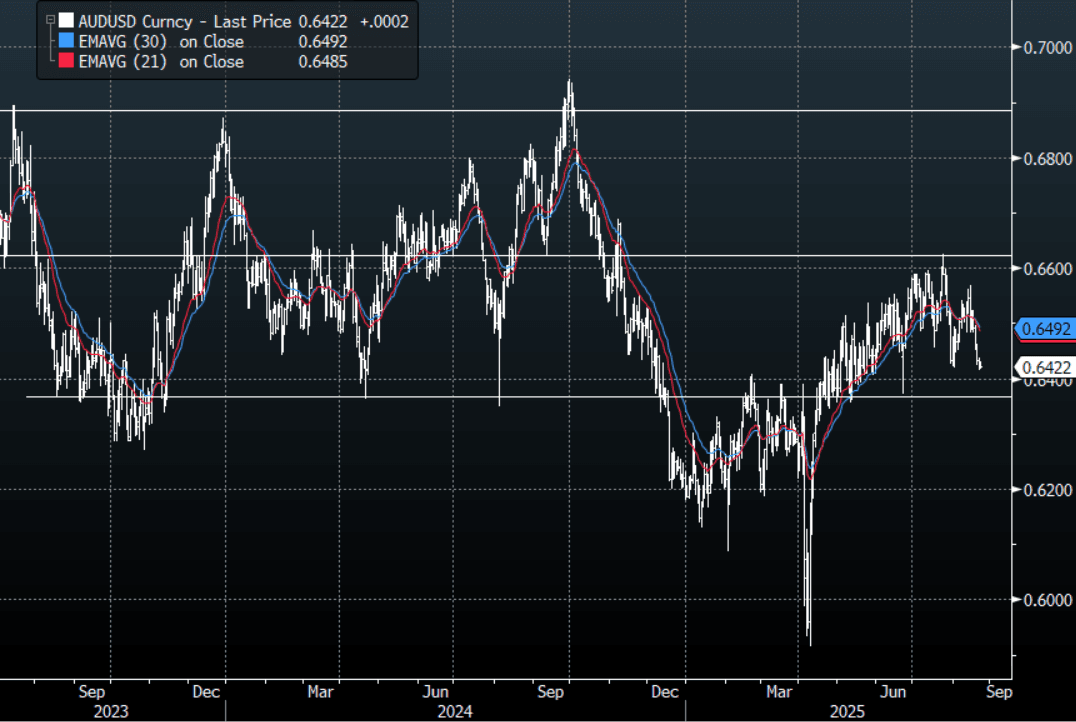

AUD: Asia Wrap - AUD/USD Consolidates Above 0.6400 Into Jackson Hole

The AUD/USD has had a range of 0.6419 - 0.6430 in the Asia- Pac session, it is currently trading around 0.6425, +0.05%. The AUD has traded sideways in an exceptionally quiet session. The AUD is consolidating just above 0.6400 heading into Jackson Hole. Pivotal support is back towards 0.6300/50 which has been the bottom in its recent multi-month range of 0.6350-0.6650.

- Bloomberg - “Nvidia told suppliers Samsung and Amkor to stop production of its H20 AI chip after Beijing urged local firms to avoid using it, The Information reported. Nasdaq futures gave up their gains.”

- “Bank of America expects further downside in the US dollar. The dollar’s July recovery looks to be short-lived as further stagflationary risks are mounting, wrote Alex Cohen, the US bank’s New York-based FX strategist. Potential rate cuts amid increasing inflation create fertile ground for dollar depreciation, while investors also need to contend with the possibility of US data credibility erosion.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD350m). Upcoming Close Strikes : 0.6525(AUD570m Aug 27) - BBG

- AUD/JPY - Asia-Pac range 95.20 - 95.51, Asia is trading around 95.50. The pair found some demand around 94.50 and has bounced overnight, sellers should be around back towards 96.00 now. A sustained break below the 94.00/94.50 area is needed to potentially begin a trend lower again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Yields Move Higher, Led By The Long-End

The TYU5 range has been 111-06 to 111-10+ during the Asia-Pacific session. It last changed hands at 111-07, down 0-06 from the previous close.

- The US 2-year yield has edged higher trading around 3.844%, up 0.01 from its close.

- The US 10-year yield has moved higher trading around 4.365%, up 0.02 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, expect supply around 4.30/35% first up. A close back below 4.30% would begin to get the bulls excited once more and the chopfest within the range will continue.

- Nick Timiraos on X: Goldman: "Market participants seem to agree that the risk to Fed independence is rising, as 5-year 5-year forward inflation swaps have recently decoupled higher from their prior close relationship with the 2-year note yield."

- Bloomberg - “Lawrence Summers backed Scott Bessent’s questioning of the Fed’s non-monetary policy activities, saying that there were some areas that are distinct from the broader issue of central bank independence.”

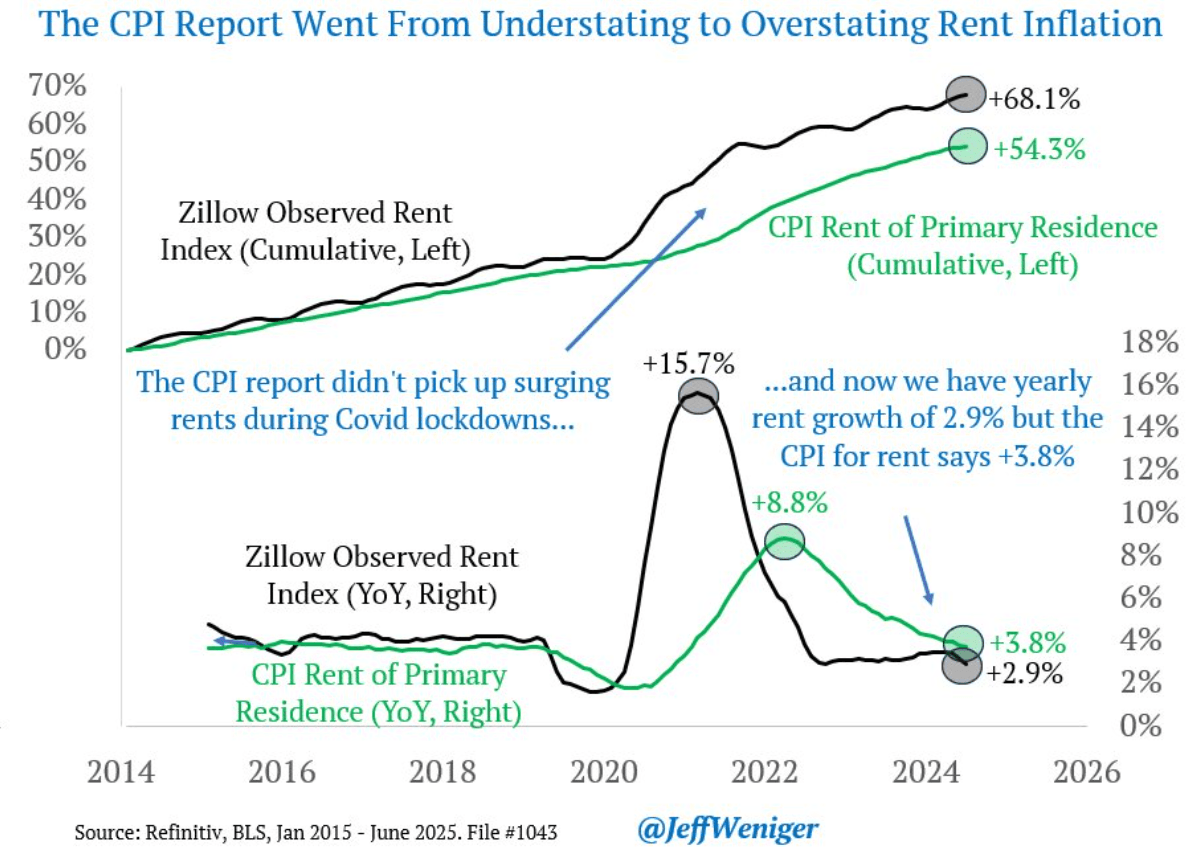

- Jeff Weniger on X: “Understand this and you'll be ahead of 99% of the public on official inflation dynamics. Similar to work by my WisdomTree colleague @JeremyDSchwartz, we see that the CPI for rent is still playing catch-up after the Covid money splash. The CPI reports of 2025 are overstating rent and will continue to do so until the catch-up is complete.” See Graph Below.

Data/Events: MBA Mortgage Applications, Existing Home Sales

Fig 1: CPI Vs CPI For Rent

Source: MNI/@JeffWeniger/Refinitiv

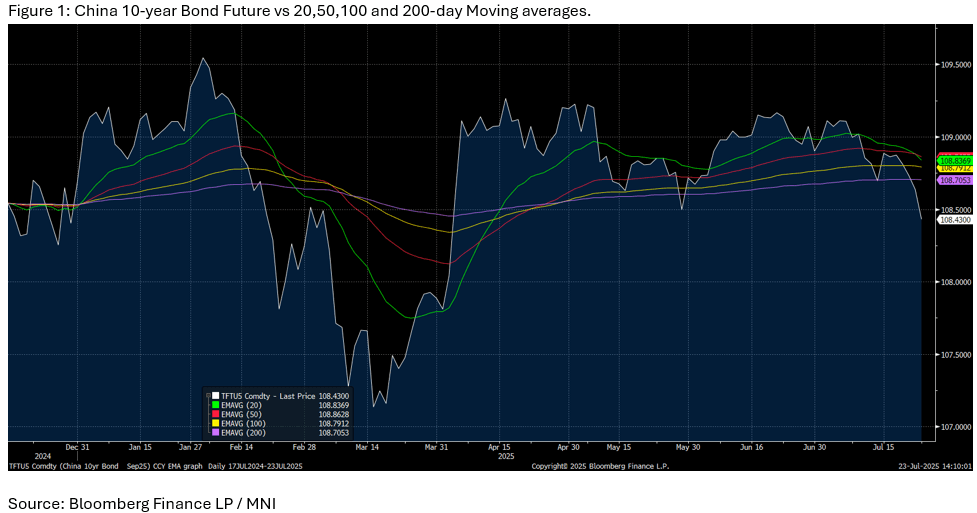

CHINA: Bond Futures Down Heavily in Morning Session

- China bond futures are down in the morning session with the 10-year having its largest one day fall since May.

- The 10-year is down -0.20 at 108.43 and has traded below all major moving averages which it had not done since late May.

- The PBOC withdrew liquidity during this morning's OMO marking three consecutive days of withdrawals.

- The 2-year future is also down, by -0.04 to 102.36 and remains below all major moving averages. The nearest being the 20-day EMA of 102.43.

- The 10YR CGB is higher by +1.5bp to 1.71%

GOLD: US-Japan Trade Deal Boosts Risk Appetite Weighing On Gold

Gold prices have trended moderately lower today following the conclusion of a trade deal between Japan and the US lifting optimism that others, especially the EU and China, may also be able to reach an agreement before August 1. Bullion had a strong start to the week rising almost 2.5% over Monday/Tuesday. Today it is down 0.2% to $3423.6/oz but off the intraday low of $3419.27 with the BBDXY USD index and US yields slightly higher.

- Gold continues to be supported by concerns over Fed independence.

- Silver is also lower at -0.1% to $39.25 after rising to $39.38 but off today’s low of $39.13. It was up almost 3% over Monday/Tuesday.

- US imports from Japan, including autos, will face a 15% tariff down from the 24% announced in April but higher than the current average below 5%. This lower rate is in exchange for $550bn of Japanese investment in the US.

- Treasury Secretary Bessent is scheduled to meet China officials in Stockholm next week with the aim of extending the current hold on tariffs.

- The US-Japan trade deal has driven an improvement in risk appetite with equities higher (Nikkei +3.2%, Hang Seng +1.1% & S&P e-mini +0.2%). Oil prices are higher with WTI +0.3% to $65.48/bbl and copper up 0.9%.

- Later June US existing home sales and preliminary July euro area consumer confidence print.