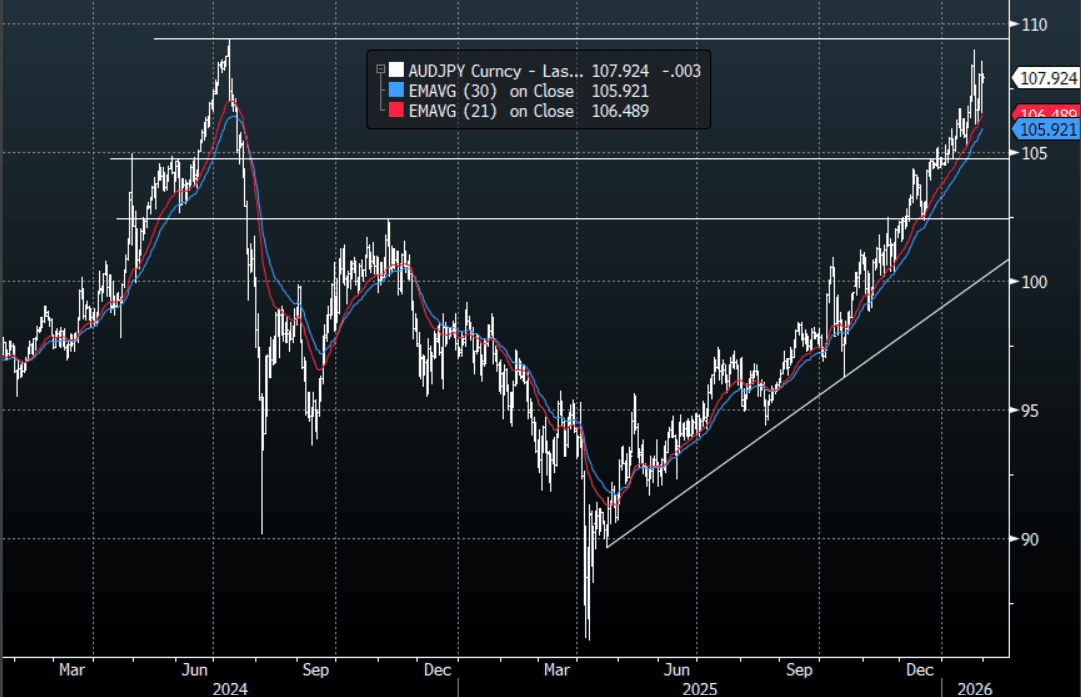

AUD: AUD/JPY - Falls Rapidly To 106.50 But Recovers With Risk Into The Close

The AUD/JPY range overnight was 106.53 - 108.48, Asia is currently trading around 107.95. The pair collapsed lower as Algo’s sold risk across the board in N/Y, but once the flows had been executed the pair drifted back to where it had started the day. AUD/JPY is up in rarified air though so some prudence is warranted up here, but for now the trend remains up and the pair looks like it will continue to be supported on dips. On the day, the first support is back toward the 106.00-106.50 area and then 104.50-105.00. The target is 109.50-110.00 and a break above there would potentially see another leg higher.

- The AUD/JPY Average True Range(ATR) for the last 10 Trading days: 118 Points

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

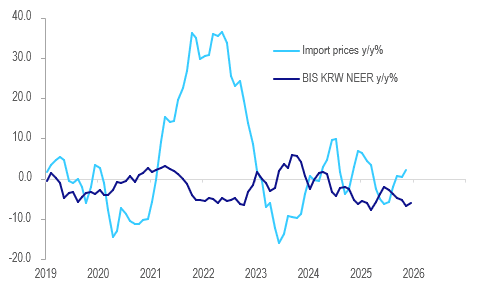

SOUTH KOREA: Inflation Remains Above BoK Target As Imported Inflation Rising

December CPI inflation printed in line with consensus with headline rising 0.3% m/m to 2.3% y/y down from November’s 2.4%. Core held at 2.0% y/y, around where it has been for most of 2025. 2025 headline inflation moderated 0.2pp to 2.1%, just above the Bank of Korea’s 2.0% goal. With inflation remaining above target and import price inflation creeping up while mortgage debt is growing due to rising house prices, the central bank is likely to leave rates at 2.5% for now, where they have been since May.

- The moderation in headline was driven by lower food inflation which moderated to 3.6% y/y from 4.7% in November, which should reassure the BoK given its concern over rising living costs. Transportation inflation remained elevated though at 3.2% y/y unchanged from October. Other categories were little changed except miscellaneous goods & services which may have been impacted by higher global gold & silver prices.

- The BIS KRW NEER is down 5.9% y/y in December after recording six consecutive monthly declines. The weaker currency is pushing imported inflation higher which rose 2.2% y/y in November up from 0.5%. It has risen each month since July, in line with the fall in the NEER.

- The next BoK decision is on 15 January.

South Korea import prices vs BIS KRW NEER y/y%

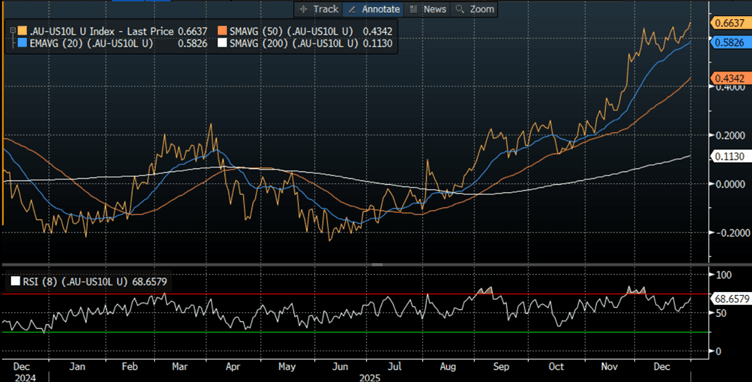

AUSSIE BONDS: Modestly Cheaper, AU-US 10Y Diff At Fresh High

ACGBs (YM -3.0 & XM -3.0) are modestly cheaper in today’s pre-holiday shortened session.

- Cash US tsys showed little reaction to the FOMC minutes release for the December meeting yesterday. The key paragraph from the December FOMC meeting minutes (link here) indicates (as did the meeting Dot Plot) a sizeable minority of members seeing no further easing through end-2026, but a base case among a solid if narrow majority that further limited cuts would ensue if the data cooperate.

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential at +65bps, a fresh cycle high.

- The bills strip is cheaper, with pricing -2 to -4 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 108% by June and 163% by December 2026.

- By the end of January, Australians should have a clearer picture of whether they can expect interest rate hikes in 2026. Quarterly inflation data, due to be released on January 28, will confirm or allay RBA fears that upward price pressures are entrenched in the economy.

Bloomberg Finance LP

US TSYS: Slightly Weaker Ahead Of NY Holiday

TYH6 is dealing at 112-20+, -0-02+ from closing levels in today's Asia-Pac session

- Yesterday, US tsys closed modestly mixed after the bell, curves twist steeper with the short end outperforming: 2s10s +2.168 at 67.531, 5s30s +0.409 at 113.113.

- Inside session ranges on lighter volumes (TYH6 just over 900k, despite some chunky block sales in 5s and 10

- s) as those present digest the Dec FOMC minutes release with varying opinions on labour, inflation outlooks and risk metrics.

- TYH6 trades 112-20.5 (-2.5) vs. 112-17 low / 112-25.5 high, 10Y yld at 4.1258% (+.0156). Trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection.

- Key short-term resistance has been defined at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

- Markets will close early (1300ET; 1600ET Globex) Wednesday for New Years eve, re-open/electronic trade Thursday evening for Friday's order of business. Tomorrow's shortened session sees Weekly Jobless Claims (0830ET). Followed by US Treasury supply: 4W, 8W & 17W bills at 1130ET.