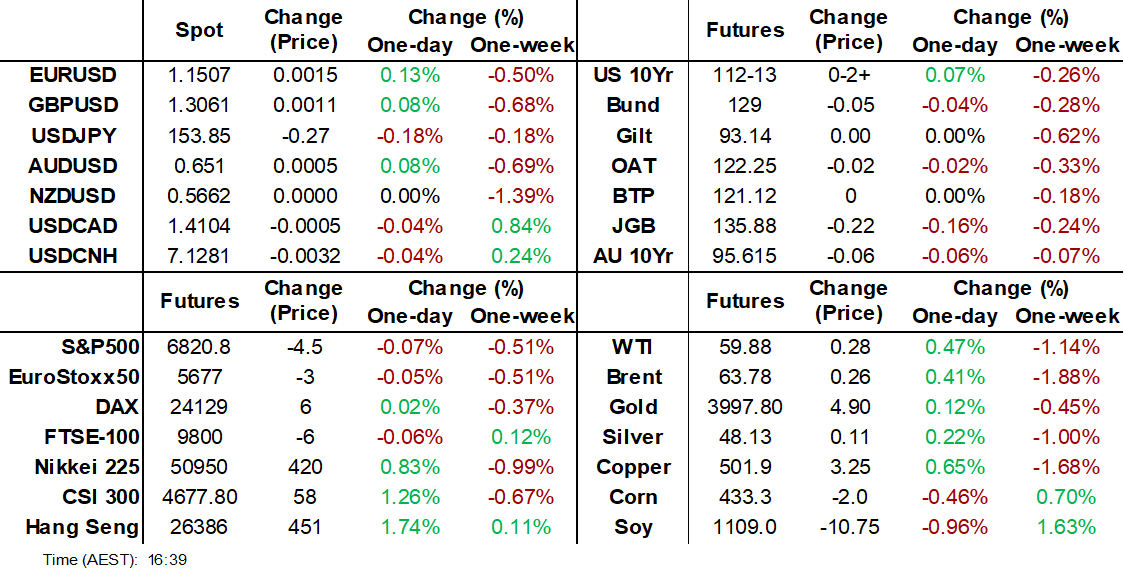

MNI EUROPEAN MARKETS ANALYSIS: Strong Asian Equity Rally

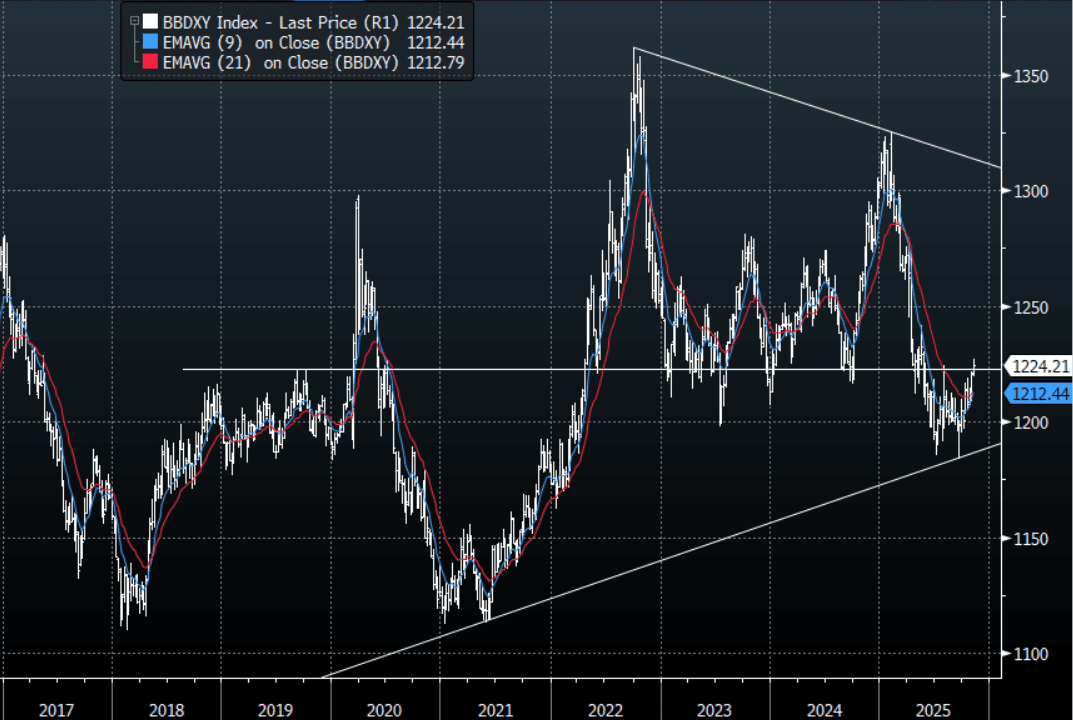

- The BBDXY has had a range today of 1223.95 - 1225.11 in the Asia-Pac session. The USD broke its run of consecutive highs as it stalled toward 1230 and has ended lower for the first time in quite a few days. The decision from the Supreme court though could have huge implications for both the USD and the Bond market.

- The September earnings data are unlikely to shift BOJ thinking. All eyes are on Ueda's speech on Dec 1 for Dec versus Jan hike risks.

- The lure of tech stocks for bargain hunters ended the two days of losses, with the NIKKEI and the KOSPI back in the positive whilst the Hang Seng led the regional bourses.

- Later there are numerous Fed speakers including Williams, Barr, Hammack, Waller, Paulson and Musalem. The ECB’s Schnabel, de Guindos, Buch and Lane also speak. The BoE is expected to be on hold.

MARKETS

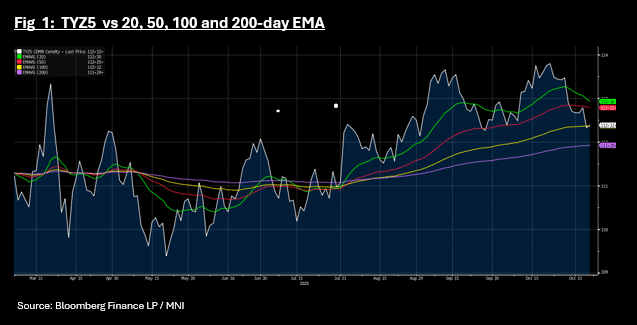

US TSYS: TYZ5 Back Above Key Tech Level

The overnight rally was sustained in Asia today with bond futures all up, albeit modestly. The 10-Yr TYZ5 is up +03 to 112-13+ in a low volume day, having trended below the 100-day EMA overnight. The rally today takes the 10-Yr back above the 100-day EMA.

Risk appetite in the Asia trading day was strong with regional bourses posting solid gains. Bonds got a bid also given the re-pricing overnight and cash down up to 1-2bps across the curve.

- The 2-Yr fell -1.2bps to 3.621%

- The 5-Yr is down -1.4bps to 3.751%

- The 10-Yr is down -1.6bps to 4.145%

- The 30-yr declined -1bps to 4.73%

The focus for issuance tonight is a US$110bn 4-week bill and a US$95bn 8-week bill auction.

Data releases are delayed tonight instead will have Fed Speakers Barr, Williams and Hammack.

JGBS: Weaker But Off Session Cheaps

JGB futures are weaker, -12 compared to settlement levels, but well above the session's worst levels.

- MNI Brief: Japan's inflation-adjusted real wages fell 1.4% y/y in September, marking the ninth consecutive month of decline after a 1.7% fall in August, preliminary data from the Ministry of Health, Labour and Welfare showed Thursday. The data highlight that nominal pay increases continue to lag inflation, leaving households squeezed by high living costs and adding pressure on the government to step up measures against rising prices.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's sell-off. The US 10-year yield hovers near one-month highs. Fed officials such as John Williams, Michael Barr, Beth Hammack, Christopher Waller, and Anna Paulson will speak later in the US session. The market is pricing a 70% probability of a 25bps rate cut in December.

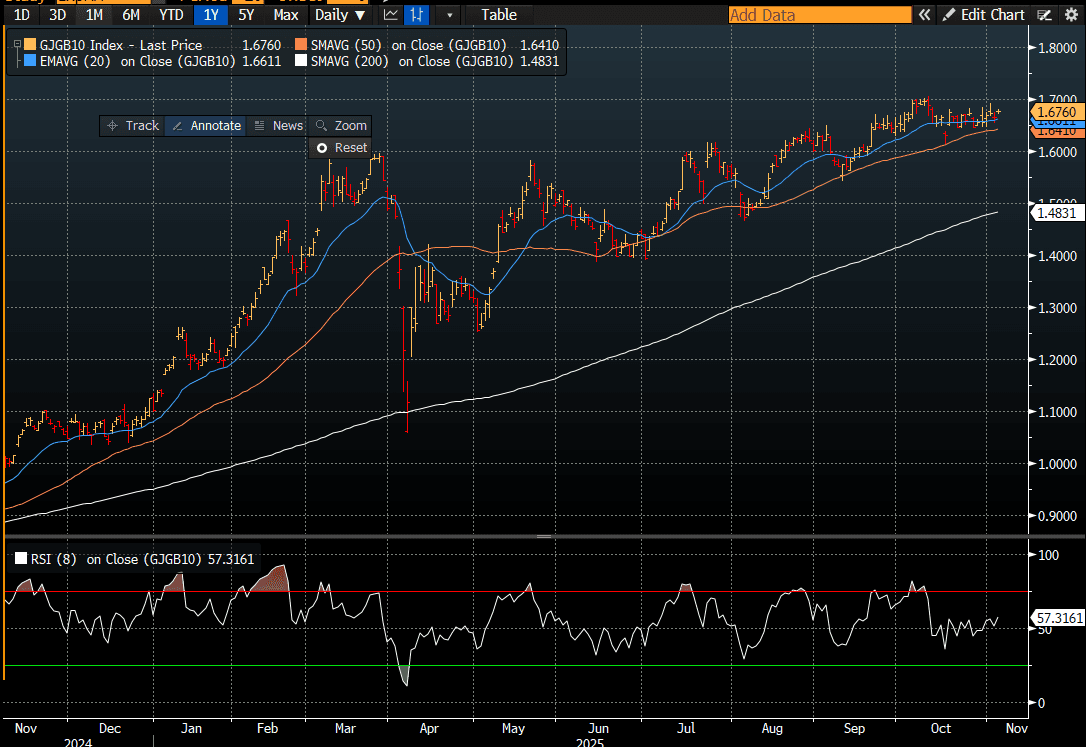

- Cash JGBs are flat to 1bp cheaper across benchmarks, with the 10-year underperforming. The benchmark 10-year yield is 1.2bps higher at 1.676% versus the cycle high of 1.705%. (see chart)

- Swap rates are flat to 2bps lower.

- Tomorrow, the local calendar will see Household Spending and Weekly International Investment Flow data alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

Source: Bloomberg Finance LP

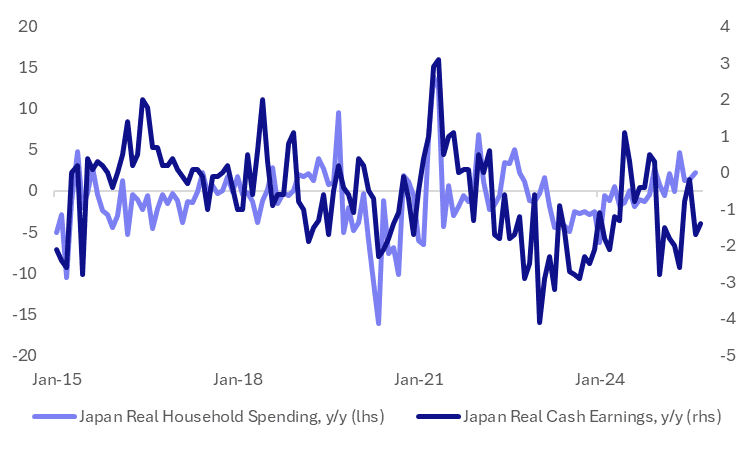

JAPAN DATA: Labour Earnings Still Negative, But Unlikely To Shift BoJ Thinking

Japan Sep labor cash earnings were close to market forecasts. Headline earnings rose 1.9%y/y, in line with market forecasts, while real earnings were -1.4%y/y (against a -1.5% forecast). Aug revisions meant we were coming from a lower base though, Real earnings were -1.7%y/y for Aug (originally reported as -1.4%), while nominal earnings were 1.3%y/y (originally reported as 1.5%). Real earnings have now been in negative territory for the whole of 2025 (in y/y terms). It's unlikely to shift BOJ thinking though. All eyes are on Ueda's speech on Dec 1 for Dec versus Jan hike risks. The central bank is also likely to rely on liaison around wage increases being negotiated and company reports, while the Q4 Tankan survey will also be watched closely.

- The chart below overlays real labour earnings and real household spending. Note we get the Sep update for household spending tomorrow. In recent months household spending trends have been firmer than real labour earning outcomes.

- Ueda stated at the last BoJ meeting that it was still too early to judge the extent of wage hikes in fiscal 2026, though it seems that these would only be slightly higher or lower than last year’s.

- Helping the headline results in Sep were a rebound in bonus payments, which tend to be volatile. They were up 4.5%y/y, after a -7.8%y/y outcome in August.

- Same sample base earnings in y/y terms were up 2.4% for cash, versus 1.9% prior. Scheduled pay rose 2.2%y/y, versus 2.4% in Aug. These trends are mostly positive, but we sit comfortably off 2024 highs.

Fig 1: Japan Real Labor Earnings & Household Spending Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Heavy Session As Market Digests A Cautious RBA

ACGBs (YM -4.5 & XM -6.0) are weaker and at or near session cheaps.

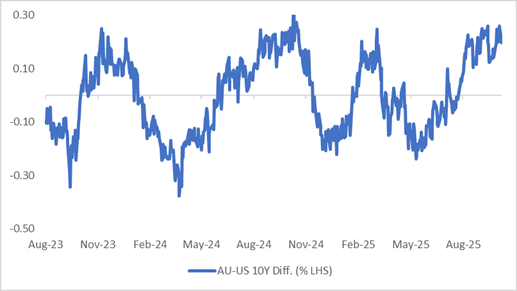

- Cash ACGBs are 4-5bps cheaper with the AU-US 10-year yield differential at +22bps. At this level, the spread has recoiled from the upper end of the 30bps range that has persisted since November 2022. (see chart)

- MNI RBA Review: The RBA Monetary Policy Board unanimously left rates at 3.6%, as was widely expected, and sounded generally cautious. Staff trimmed mean projections were revised higher over the rest of 2025 and 2026, with the important 2q/2q annualised rate returning to 3% in Q1 and 2.6% in Q4, which may allow a rate cut from May if this eventuates. Decisions remain highly data-dependent. (see link)

- The bills strip is weaker, with pricing -2 to -4 across contracts.

- RBA-dated OIS pricing is little changed following this week’s RBA Policy Decision. RBA-dated OIS pricing is showing a 25bp rate cut in December at a 10% probability, with a cumulative 18bps of easing priced by mid-2026. Notably, current pricing leaves levels some 22-26bps firmer than pre-Q3 CPI levels in late October.

- Tomorrow, the local calendar will see Foreign Reserves.

- The AOFM plans to sell A$800mn of the 3.00% 21 November 2033 bond on Friday.

Bloomberg Finance LP

RBA: MNI RBA Review-Nov 2025: Inflation Persistence Key To Outlook

- Dowload Full Report Here

- The RBA Monetary Policy Board unanimously left rates at 3.6%, as was widely expected, and sounded generally cautious. With risks "in both directions" and the degree of restrictiveness difficult to assess, the Board doesn't have a stance. Neither a cut nor a hike were discussed.

- Staff trimmed mean projections were revised higher over the rest of 2025 and 2026 with the important 2q/2q annualised rate returning to 3% in Q1 and 2.6% in Q4, which may allow a rate cut from May if this eventuates.

- Decisions remain highly data dependent and will be made on a "meeting-by-meeting basis".

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 10% probability, with a cumulative 18bps of easing priced by mid-2026.

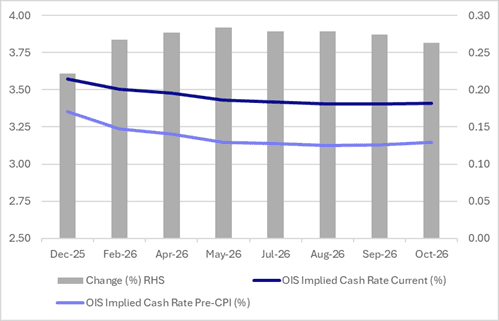

STIR: Little Change Since RBA Decision But Much Firmer Than Late-Oct

RBA-dated OIS pricing is little changed since this week’s RBA Policy Decision.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 10% probability, with a cumulative 18bps of easing priced by mid-2026.

- Notably, current pricing leaves levels some 22-26bps firmer than pre-Q3 CPI levels in late October.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI

Source: Bloomberg Finance LP / MNI

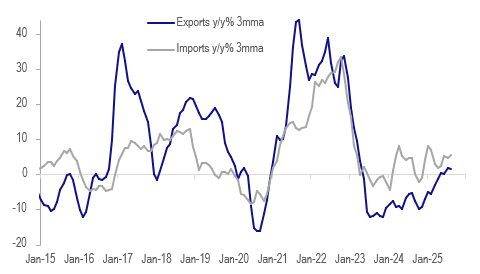

AUSTRALIA DATA: Gold Prices Boosted Exports But Sep Commodities Generally Robust

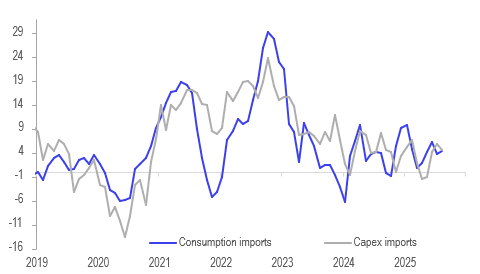

Australia’s September merchandise trade surplus widened as expected printing at $3938mn driven by a 7.9% m/m jump in exports driven by higher gold prices. Through volatility, the surplus continues its gradual downtrend which it began late in 2025. Capex imports suggests an investment recovery.

Australia merchandise exports vs imports y/y% 3-mth moving average

Source: MNI - Market News/ABS

- Global USD gold prices rose 8.9% m/m and in AUD 7.2% in September. Australia’s non-monetary gold exports rose 62.2% m/m in September to be up 119.2% y/y. Gold shipments have been highly correlated with recent monthly changes in goods exports which rose 7.9% m/m & 9.7% y/y.

- Non-rural goods were stronger up 3.7% m/m but up only 0.5% y/y after declining 8.5% y/y, the first rise in annual growth since March 2023. The increase was broad-based across commodities with many posting both higher volumes and values. Rural exports rose 0.7% m/m to be up 14.6% y/y, outperforming non-rural.

- Exports to China and Korea were strong in September but continued to fall to Japan, Taiwan and India. Growth remained elevated to the US and UK but contracted to Germany.

- Merchandise imports remained robust rising 1.1% m/m and 11.1% y/y up from 8.2% y/y. The September monthly increase was driven by capital goods up 6.7% m/m & 9% y/y, which is positive for the investment outlook as the strength was across major components (ex aircraft). Consumer goods fell 1.2% m/m but were still 7.4% y/y higher.

Australia merchandise imports y/y% 3-mth moving average

Source: MNI - Market News/ABS

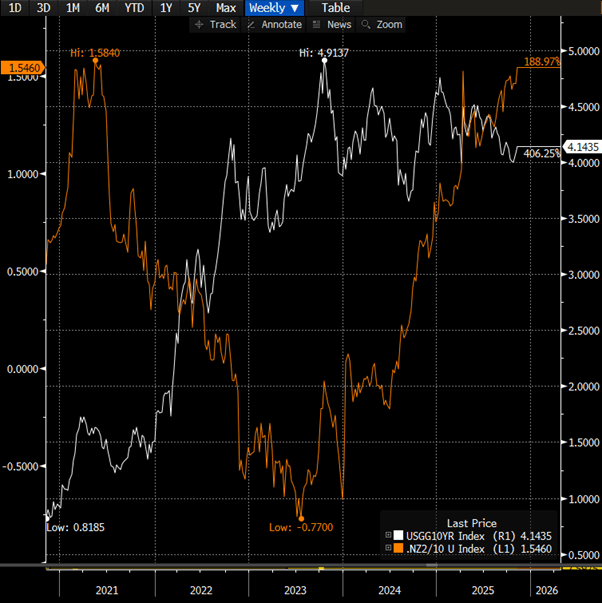

BONDS: NZGBS: Bear-Steepener Pushes Curve Towards 2021 Highs

NZGBs closed showing a bear-steepener, with benchmark yields 1-5bps higher.

- Today’s move leaves the NZGB 2/10 yield curve at 155bps and near its steepest level since 2021. When the curve was last this steep, the OCR stood at 0.25%, compared with 2.5% today. Although the NZ–US 10-year yield differential is near its 2021 level, the US 10-year yield is now 4.16%, up from 1.65% at that time. (see chart)

- The NZGB 10-year outperformed its $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 3bps and 1bps narrower on the day.

- Today’s weekly supply was received with solid demand. Cover ratios ranged from 3.24x (May-54) to 3.97x (Apr-29).

- Swap rates closed 1-4bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed slightly softer across meetings. 28bps of easing is priced for November, with a cumulative 36bps by February 2026.

- Tomorrow, the local calendar will be empty. The next release of note will be the RBNZ's Inflation Expectations data on Tuesday.

Bloomberg Finance LP

FOREX: Asia-Pac FX: USD Drifts Lower, Focus On Supreme Court Tariff Ruling

The BBDXY has had a range today of 1223.95 - 1225.11 in the Asia-Pac session; it is currently trading around 1224, -0.10%. The USD broke its run of consecutive highs as it stalled toward 1230 and has ended lower for the first time in quite a few days. The 1230 area remains tough resistance, a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made and the dips remain very shallow pointing to a reduction in shorts. The decision from the Supreme court though could have huge implications for both the USD and the Bond market. Should they reject the Trump administration's arguments, the US would have to pay back something in the region of $100 billion in tariffs collected, which would have huge ramifications on the deficit as well as funding going forward.

- EUR/USD - Asian range 1.1487 - 1.1509, Asia is currently trading 1.1505. The pair’s momentum lower stalled below 1.1500, I suspect rallies will now be sold into with the first resistance back toward the 1.1600 area.

- GBP/USD - Asian range 1.3046 - 1.3065, Asia is currently dealing around 1.3060. The pair found some support back toward 1.3000 yesterday. I continue to favor fading rallies though as GBP looks like it has put in a medium term top. First sell zone back toward 1.3150 and then the more important 1.3300 area. BOE today could provide some movement.

- Cross asset : SPX -0.05%, Gold $3985, US 10-Year 4.1450%, BBDXY 1224, Crude Oil $59.84

- Data/Events : France Private Sector Payrolls, Spain Industrial Production, Germany HCOB Germany Construction PMI, EZ Retail Sales

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

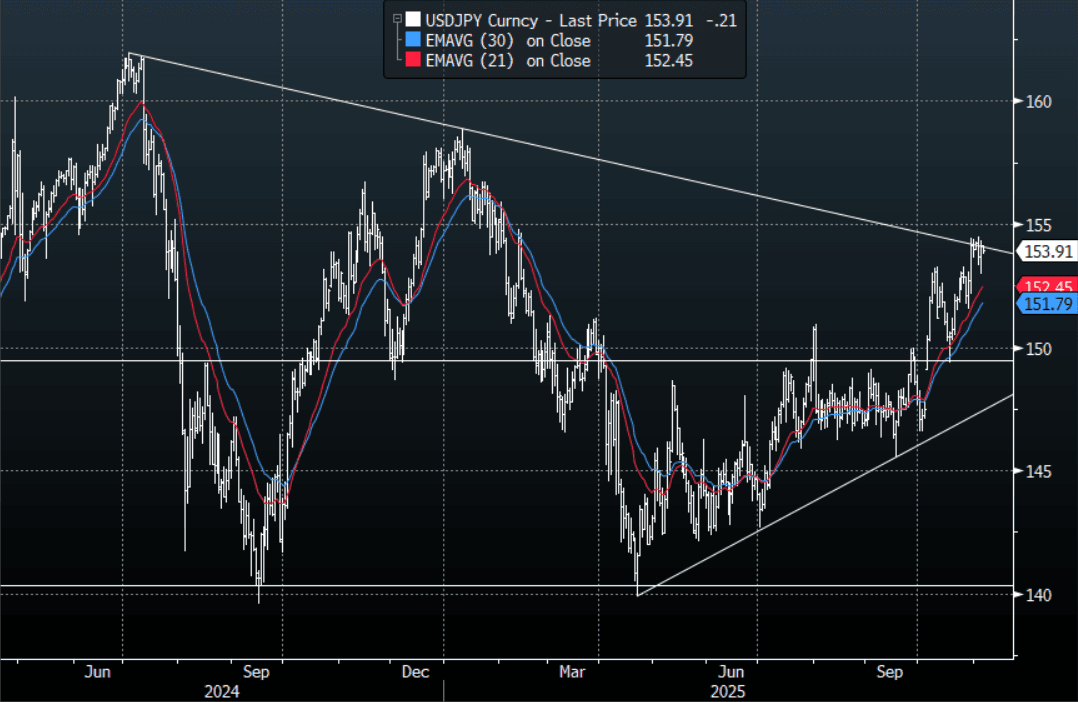

JPY: Asia-Pac: USD/JPY Struggles To Hold Above 154.00

The USD/JPY range today has been 153.80 - 154.36 in the Asia-Pac session, it is currently trading around 153.90, -0.15%. The pair bounced strongly yesterday off the 153.00 area as cross-Yen did an about face as risk recovered paring back losses overnight. A lot depends on what your view is for risk from here, should the price action of the last few days signal that we could be putting in a top and a correction of sorts plays out then I suspect the resistance around the 154/155 area should continue to offer solid resistance. If we see a similar price action to what we have all year and risk just goes straight back to make new all-time highs as we head into the year-end rally then it's highly probable this resistance gives way and we target levels closer to 160.00.

- MNI BRIEF: Japan Sept Real Wages Negative For Ninth Month. Japan’s inflation-adjusted real wages fell 1.4% y/y in September. The data highlight that nominal pay increases continue to lag inflation, leaving households squeezed by high living costs and adding pressure on the government to step up measures against rising prices.

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.00($1.14b), 155.00($1.88b), 155.35($1.38b). Upcoming Close Strikes : none - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

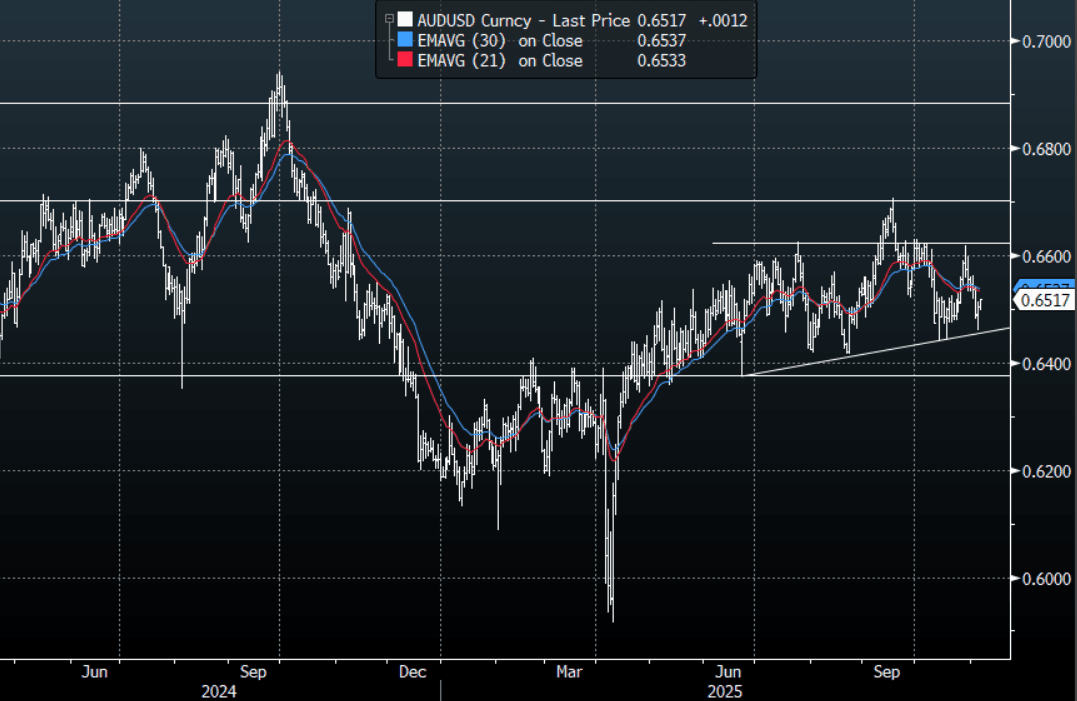

AUD: Asia-Pac: AUD/USD Recovers Back Above 0.6500

The AUD/USD has had a range today of 0.6497 - 0.6517 in the Asia- Pac session, it is currently trading around 0.6515, +0.20%. Was that it ? The dip buyers in risk look once again to be in control and what looked like the start of a correction has quickly petered out. The AUD/USD finds itself back in the middle of its now familiar range, having chopped sideways between 0.6350-0.6650 since April this year. A lot rides on how risk trades from here, should this potential correction lower play out then the USD should again come to the fore, but if that was the extent of the correction and we start building toward a year end rally for risk assets then the AUD can again start to outperform. The pivot for the AUD is around 0.6550, above there and we start to turn toward the top of the range again.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6490(AUD487m), 0.6550(AUD 479m), 0.6600(AUD567m). Upcoming Close Strikes : 0.6450(AUD544m Nov 11), 0.6500(AUD1.02b Nov 7), 0.6600(AUD682m Nov 7)- BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

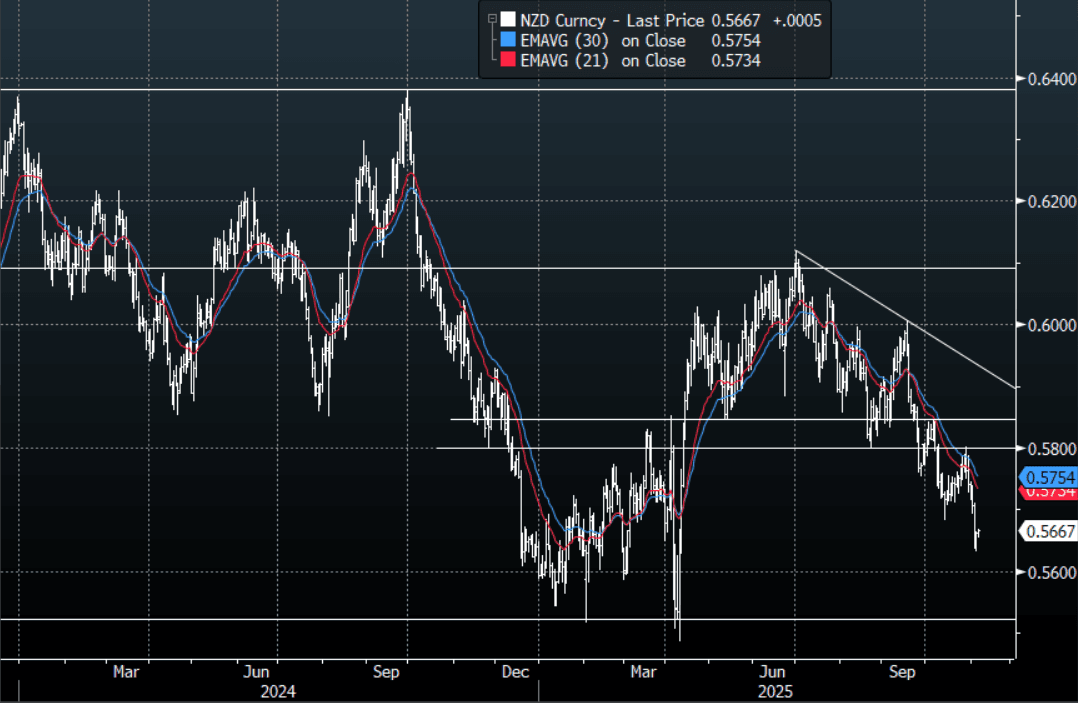

NZD: Asia-Pac: NZD/USD - Finds Bids Below 0.5650

The NZD/USD had a range of 0.5655 - 0.5668 in the Asia-Pac session, going into the London open trading around 0.5665, +0.02%. Was that it ? The dip buyers look once again to be in control and what looked like the start of a correction for risk has quickly petered out. The NZD move lower has stalled finding some demand below 0.5650 as risk stabilsed. While price remains below the 0.5800/50 area I suspect rallies will continue to be faded looking for a potential move back towards the 0.5500/0.5600 area. The NZD stands out as a vehicle to short against a resurgent USD but it is worth noting that because of the size of the market it can very quickly become all positioned the same way. I think the USD will need to do the heavy lifting from here and break above its pivotal resistance for the NZD to test the 0.5500 lows. The first sell zone on the day would be back toward the 0.5700-0.5725 area.

- MNI AU - NZ 2/10 Yield Curve Steepest Since 2021: The NZ 2/10 yield curve has steepened to its highest level since 2021. When the curve was last this steep, the OCR stood at 0.25%, compared with 2.5% today. Although the NZ-US 10-year yield differential is near its 2021 level, the US 10-year yield is now 4.16%, up from 1.65% at that time.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5730(NZD496m), 0.5780(NZD305m). Upcoming Close Strikes : none - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Bourses Rebound as Tech Bargain Hunters Emerge

The lure of tech stocks for bargain hunters ended the two days of losses, with the NIKKEI and the KOSPI back in the positive whilst the Hang Seng led the regional bourses. The likes of SK Hynix Inc in Korea had fallen almost 8% in two days, yet has recovered half of that in today's rally. In what is often the next step in a sector rally such as this is M&A and there are reports today that Softbank Group Corp. shares rose 0.5% as it explored a potential takeover of US chipmaker Marvell Technology Inc. BBG also reports that the MSCI global stock index saw the number of Chinese companies has climbed for the first time in nearly two years, setting up the market for more inflows from passive investors.

- The HSI is up +1.64% leading the regional gains, taking it back above its 20-day EMA having bounced on the 50-day EMA. The CSI 300 is up +1.2%, Shanghai +0.88% and Shenzhen up +0.90%.

- The Nikkei fell -4.20% in two day, but has bounced on the tech rebound - up +1.3% today whilst the KOSPI rose +1.5%.

Ahead of the Central Bank decision later, the FTSE Malay KLCI is trending sideways whilst the JCI in Indonesia is up marginally and the SE Thai by +0.7%

OIL: Saudi Cuts Prices To Asia, Fed Speakers Later On Thursday

Oil prices are moderately higher but within a narrow range during today’s APAC trading after Wednesday’s 1.5% fall and mixed EIA US inventory report that suggested robust product demand. The as expected Saudi reduction in prices across its crude grades for Asian customers helped the stabilisation, as the move could increase regional demand. A softer US dollar has been supportive (BBDXY -0.1%).

- WTI is up 0.4% to $59.80/bbl after reaching $59.86 off the intraday low of $59.55. Brent is 0.3% higher at $63.72/bbl following a high of $63.78.

- The EIA reported a US crude oil inventory build of 5.2mn barrels last week after destocking of 6.86mnm. However, gasoline stocks fell 4.7mn barrels, and distillate was down 0.6mn, the fifth consecutive weekly decline for both suggesting demand remains solid. The 0.6pp decline in refining utilisation to 86%, 4.5pp below the same time last year, helped to drive the crude stock build and product drawdown.

- Later there are numerous Fed speakers including Williams, Barr, Hammack, Waller, Paulson and Musalem. The ECB’s Schnabel, de Guindos, Buch and Lane also speak. The BoE is expected to be on hold.

- US October Challenger job cuts are likely to be monitored closely given October payrolls will be delayed due to the government shutdown. Also German September IP, euro area September retail sales, Q3 French payrolls and October UK construction PMI print.

Gold Slightly Higher But Still In Range, Will Watch Upcoming Fed Speakers

Gold prices are moderately higher in Thursday’s APAC session supported by a softer US dollar (BBDXY -0.1%) and slightly lower yields. The chance of a December Fed rate cut has also risen also boosting non-interest bearing bullion. The market has been range trading this week driven by uncertainty over the outlook for the next Fed decision. Gold is up 0.2% to $3987.0 today off the high of $3990.43.

- With US data scarce due to the government shutdown, ADP October employment was watched closely. With a 42k rise after two consecutive falls, it signalled that the labour market remains soft but may have stabilised. Looking forward, the swathe of Fed speakers on Thursday will be monitored for thinking regarding upcoming decisions.

- Silver is 0.5% higher at $48.24 after reaching $48.263 following a low of $47.738. Like gold it has traded between resistance at $49.456, 23 October high, and support at $46.089, 50-day EMA. The trend in the metal remains bullish and any declines are considered corrective.

- Equities are generally stronger with the Nikkei up 1.4% and CSI 300 +1.3% but S&P e-mini flat. Oil prices are higher with WTI +0.4% to $59.86/bbl. Copper is up 0.6%.

- Later there are numerous Fed speakers including Williams, Barr, Hammack, Waller, Paulson and Musalem. The ECB’s Schnabel, de Guindos, Buch and Lane also speak. The BoE is expected to be on hold. US October Challenger job cuts are likely to be monitored closely given October payrolls will be delayed due to the government shutdown. Also German September IP, euro area September retail sales, Q3 French payrolls and October UK construction PMI print.

US: Air Traffic To Be Cut 10% - Rtrs, Shutdown Ending Odds Rise Towards End Nov

Headlines have crossed from Reuters that the US will cut air traffic by 10% at 40 major airports by this Friday, unless the government shutdown is ended. It notes: "U.S. Transportation Secretary Sean Duffy confirmed on Wednesday that he would order a 10% reduction in scheduled air traffic at 40 major airports starting Friday unless a deal to end the federal government shutdown is reached." Odds of the shutdown ending in the second half of Nov have risen, but our US team noted overnight the Democrats negotiating stance has likely been hardened in the aftermath of the recent election results.

- This comes as the shutdown enters the longest on record (now into its 36th day), with air traffic disruptions only to add to the economic downside risks.

- Our US team noted overnight that the Democrats stance around negotiations has likely hardened after yesterday's election results. Focus remains on the funding bill, with health insurance subsidies still seen as sticking point. They note: "Sarah Ferris at CNN reports on X, “Senate Dems involved in talks to end shutdown are using election to try to spur GOP to back a framework to temporarily extend ACA with some reforms to reopen govt, per 2 sources. “With that it ends fast; without we stare at each other another week.” The report appears to confirm that the ‘blue wave’ overperformance at yesterday’s elections has bolstered Democrats' position that a hardline stance on reopening the government is endorsed by voters."

- Per Polymarket, odds of the shutdown ending by Nov 12-15 sit at 22, up modestly from the start of the week. Odds of the shutdown ending by Nov 16 or later sit at 40.3, per Polymarket, also up from earlier in the week. The market is expecting the shutdown to be over by end Nov, with odds at 93, per Polymarket.

BCB: On Hold As Expected, Contractionary Policy Needed For Long Period

The BCB kept interest rates on hold as expected at 15%. The central bank noted the significant uncertainties surrounding the outlook, including the upside and downside risks for the inflation backdrop, along with trade/tariff uncertainties. See the full statement here:

- It noted: "The current scenario continues to be marked by deanchored inflation expectations, high inflation projections, resilience on economic activity and labor market pressures. Ensuring the convergence of inflation to the target in an environment with deanchored expectations requires a significantly contractionary monetary policy for a very prolonged period."

- And "The current scenario, marked by heightened uncertainty, requires a cautious stance in monetary policy. The Committee evaluates that maintaining the interest rate at its current level for a very prolonged period will be enough to ensure the convergence of inflation to the target. The Committee emphasizes it will remain vigilant, that future monetary policy steps can be adjusted and that it will not hesitate to resume the rate hiking cycle if appropriate."

- This may temper easing expectations, albeit at the margin for Q1 next year. As our policy team noted in their preview: "All eyes are now on when the BCB might begin easing and whether it will keep the hawkish tone, with most expecting a cut in the first quarter of 2026, some in January, others in March."

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 06/11/2025 | 0700/0800 | ** | Industrial Production | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0800/0900 | ** | Industrial Production | |

| 06/11/2025 | 0800/0900 | ** | Unemployment | |

| 06/11/2025 | 0810/0910 | ECB Schnabel At ECB Money Market Conference | ||

| 06/11/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/11/2025 | 0830/0930 | ECB De Guindos On Natixis Webinar | ||

| 06/11/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 06/11/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/11/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1230/1230 | BOE Press Conference | ||

| 06/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 06/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 06/11/2025 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 06/11/2025 | 1400/1400 | Decision Maker Panel Data | ||

| 06/11/2025 | 1500/1000 | * | Ivey PMI | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 06/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 06/11/2025 | 1530/1030 | BOC Governor Macklem testifies at Senate. | ||

| 06/11/2025 | 1600/1100 | NY Fed's John Williams | ||

| 06/11/2025 | 1600/1100 | Fed Governor Michael Barr | ||

| 06/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 06/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 06/11/2025 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 06/11/2025 | 1830/1930 | ECB Lane At IMF Conference | ||

| 06/11/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 06/11/2025 | 2030/1530 | Fed Governor Christopher Waller | ||

| 06/11/2025 | 2130/1630 | Philly Fed's Anna Paulson | ||

| 06/11/2025 | 2230/1730 | St. Louis Fed's Alberto Musalem | ||

| 07/11/2025 | 2330/0830 | ** | Household spending | |

| 07/11/2025 | 0700/0800 | ** | Trade Balance | |

| 07/11/2025 | 0745/0845 | * | Foreign Trade | |

| 07/11/2025 | 0800/0300 | New York Fed's John Williams | ||

| 07/11/2025 | 1110/1110 | BOE Saporta At ECB Money Market Conference | ||

| 07/11/2025 | 1200/0700 | Fed Vice Chair Philip Jefferson | ||

| 07/11/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 07/11/2025 | - | *** | Trade | |

| 07/11/2025 | - | BOE MPG Agenda Published | ||

| 07/11/2025 | 1330/0830 | *** | Labour Force Survey | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/1430 | ECB Elderson At Bundesbank Event |