MNI EUROPEAN MARKETS ANALYSIS: JGB Yields Down Despite Auction

- Major macro trends have been fairly muted across US equity futures, Tsy futures and the USD. The market awaits key event risks later. We have the ECB later today, then NFP tomorrow in the US.

- JGB futures are sharply stronger and at Tokyo session highs, +46 compared to settlement levels, after quickly reversing initial weakness following today’s poor 30-year auction. Earlier we had Japan labor earnings data, which was a touch below expectations. In Australia, household spending started Q2 on a soft note

- Later the Fed’s Kugler, Harker & Schmid as well as BoE’s Greene & Breeden speak. The ECB is expected to cut rates 25bp and the decision will be followed by President Lagarde’s press conference. US jobless claims, May Challenger job cuts, April trade & final Q1 productivity/ULC, and April German factory orders & euro area PPI print.

MARKETS

US TSYS: Asia Wrap - Yields Drift Higher

The TYU5 range has been 111-01 to 111-05+ during the Asia-Pacific session. It last changed hands at 111-01+, down 0-02 from the previous close.

- The US 2-year yield has edged higher, dealing around 3.8809%, up 0.01 from its close.

- The US 10-year yield has moved higher, trading around 4.3709%, up 0.2 from its close.

- MNI FED: Beige Book: Economic Activity Declining Slightly. The June 4 Beige Book reported that "economic activity has declined slightly since the previous report". Uncertainty was a key theme, with manufacturing activity and household consumption showing signs of weakness. Overall the outlook remained "slightly pessimistic and uncertain".

- Bob Elliott on X: “For all the bond dooming around these parts, it seems the long end performed just fine in response to the suite of negative growth data today. Those folks who have sworn off bonds should take heed.” https://x.com/BobEUnlimited/status/1930405270682849614

- "FED'S KASHKARI SAYS LABOR MARKET SHOWING SOME SIGNS OF SLOWING, FED MUST WAIT AND SEE AS ECONOMY FACES UNCERTAINTY" - BBG

- The 10-year yield is attempting to break its support around 4.35/40%. Yields need to hold around this area to continue to build for a move higher, the market positioning is short and would now be worried about what a lower NFP print could signal.

- Data/Events: Trade Balance, Initial Jobless Claims, NFP tomorrow night will be hugely important.

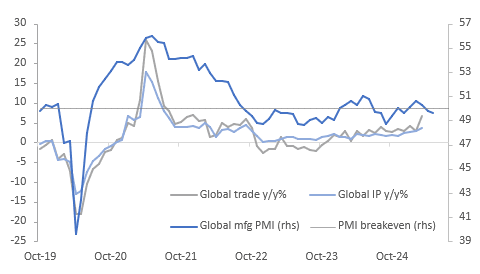

GLOBAL MACRO: Manufacturing PMI Signalling Slower Future IP Growth

The JP Morgan manufacturing PMI for May fell 0.2 points to 49.6, the weakest reading this year, signalling that activity in the sector shrank marginally in the month after US tariffs were announced and then delayed 90 days. This signals that the pickup in global IP growth in March is unlikely to be sustained and probably reflected a frontloading of production ahead of expected tariffs. However, the future output component of the PMI rose 3 points to 60.2, well above the breakeven-50, signalling that businesses expect growth to improve.

Global growth

- The deterioration in manufacturing production was driven by the intermediate and investment goods sectors, while consumer goods remained above 50 and saw increased growth in May. India saw the strongest growth in the month, while China, UK, Japan and UK saw output contract.

- The decline in output growth appears to have been driven by a deterioration in new orders due to weaker domestic demand while export orders continued to contract but at a slower rate in May. Despite this there was a slowdown in labour shedding.

- The inflation picture also improved in May with both input and output price pressures moderating. JP Morgan notes that delivery times rose to their longest in 6 months.

- Global IP growth picked up to 3.7% y/y in March from 2.9%, the highest since September 2022, while global trade rose 6.6% y/y after 3.0%, the strongest since December 2021. The PMI indicates that both of these may slow in coming months.

JGBS: Market Quickly Reverses Initial Weakness After Poor 30Y Auction

JGB futures are sharply stronger and at Tokyo session highs, +46 compared to settlement levels, after quickly reversing initial weakness following today’s poor 30-year auction.

- The 30-year JGB auction delivered poor results, suggesting weak investor demand. The low price fell short of dealer expectations, per a Bloomberg survey. Moreover, the cover ratio fell to 2.9215x from 3.0739x, and the auction tail lengthened significantly to 0.49 from 0.30.

- “Recent auctions in Japan, Australia, and South Korea have shown weak demand, and investors are demanding more compensation to hold long-dated bonds due to growing anxiety about fiscal deficits. The trend of higher global yields is a warning sign from investors that governments cannot keep borrowing at the pace they did when interest rates were close to zero.” (per BBG)

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's strong data-induced rally. The focus is now on today's weekly jobless claims, trade balance, and unit labour costs data.

- Cash JGBs are 2-7bps richer across benchmarks, with a flatter curve. The benchmark 30-year yield is 6.8bps lower at 2.883% after today's supply.

- Swap rates are 2-5bps lower.

- Tomorrow, the local calendar will see Household Spending and Coincident/Leading Index data.

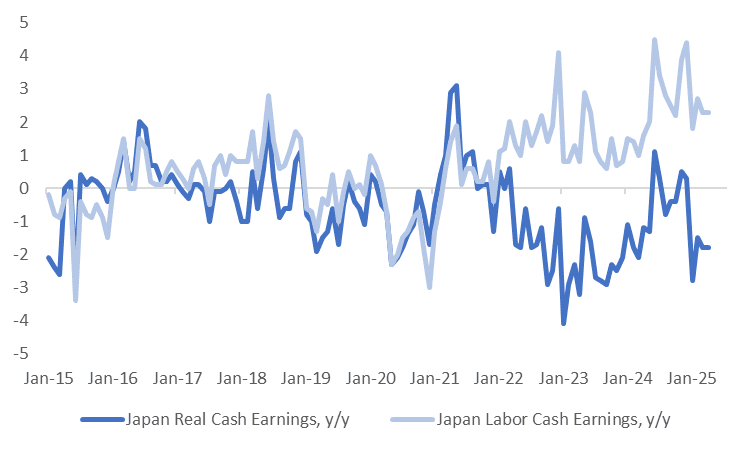

JAPAN DATA: Real Earnings Remain Firmly Negative, Scheduled Pay Firms Y/Y

Japan April labor earnings data were slightly below market forecasts, but we did see positive revisions. Nominal earnings rose 2.3%y/y, versus 2.6% projected. The March print was revised higher to 2.3%y/y (originally reported as a 2.1% gain). In real terms earnings were -1.8%y/y (against a -1.6% forecast and revised -1.8% outcome for March). Cash earnings on a same sample basis were 2.6%y/y, also below forecasts of 2.8% y/y, but March was revised higher to 2.7%y/y. Full-time pay, on the same base, was 2.5%y/y, above the 2.3% forecast. prior was 2.1%.

- The chart below plots nominal and real cash earnings in y/y terms. Nominal earnings are off highs but still elevated by historical standards. The lack of positive trends in real earnings will be a disappointment for the authorities though. We have had a few positive y/y readings in recent years, but these have proved fleeting.

- Bonus payments were +4.1%y/y, versus the 14.5% pace seen in March. Hours worked were -1.2%y/y, compared with -2.7% in March.

- On the same sample basis, scheduled and full time pay saw y/y rises compared to the March outcome. We are sub 2024 y/y highs for these metrics, but still this helps offset to some degree the disappointing headline nominal and real earning outcomes.

- The data is unlikely to shift near term BoJ thinking, with the mid June policy meeting outcome expected to deliver no policy rate change.

Fig 1: Japan Nominal & Real Cash Earnings - Y/Y

Source: MNI - Market News/Bloomberg

JAPAN DATA: Local Appetite For Offshore Bonds Waned Into End May, Equities Sold

Japan local investors were net sellers of both offshore bonds and stocks last week. This was the final week of May, with modest net selling of offshore bonds. Still for the month, we had healthy net buying (with ¥4.2trln in net purchases for the last 5 weeks). Global bond returns were close to flat for the month of May. We saw larger selling of offshore equities. This marked the third straight week of outflows, although we are still net positive for 2025 to date.

- In terms of inflows into Japan bonds, there was a notable step up by offshore investors in terms of purchases. The ¥1.165Trln in net inflows was the strongest weekly pace since mid April. This comes at a time when we have seen faltering appetite at longer dated JGB auctions. The earlier 10yr auction this week saw firm demand. Later today we have a 30yr auction.

- Offshore investors continued to buy local stocks, which marked the 9th straight week of inflows into this space.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending May 30 | Prior Week |

| Foreign Buying Japan Stocks | 336.1 | 309.1 |

| Foreign Buying Japan Bonds | 1165.4 | -332.8 |

| Japan Buying Foreign Bonds | -118.0 | 100.4 |

| Japan Buying Foreign Stocks | -1144.1 | -524.7 |

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Modestly Richer, Narrow Ranges, Jun-31 Supply Tomorrow

ACGBs (YM +2.0 & XM +2.5) sit slightly stronger after dealing in relatively narrow ranges in today’s Sydney session.

- (MNI) Our policy reaction function is signalling that rates on hold around 3.85% is consistent with the economic outlook. The RBA reduced its trimmed mean inflation projection by 0.1pp to 2.6% so that the inflation gap is now only 0.1pp and also revised down its growth projections due to current global trade uncertainty and slower-than-expected private consumption growth.

- The model is updated for yesterday’s Q1 GDP data, but given much of the softness was due to weather events, a July 8 rate cut is likely to be more dependent on more timely monthly data releases and trade negotiation progress.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's strong data-induced rally.

- Cash ACGBs are 2bps richer, with the AU-US 10-year yield differential at -13bps vs. -20bps yesterday.

- The bills strip has twist-flattened, with pricing -1 to +2.

- RBA-dated OIS pricing suggests a 25bp rate cut in July is an 86% probability, with a cumulative 81bps of easing priced by year-end.

- Tomorrow, the local calendar will see Foreign Reserves data and the AOFM’s planned sale of A$800mn of the 1.50% 21 June 2031 bond.

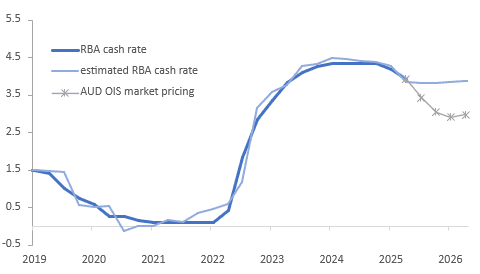

AUSTRALIA: Inflation Gap Impact On Rate Estimates Offset By Output Gap

Our policy reaction function is signalling that rates on hold around 3.85% is consistent with the economic outlook. The RBA reduced its trimmed mean inflation projection by 0.1pp to 2.6% so that the inflation gap is now only 0.1pp and also revised down its growth projections due to current global trade uncertainty and slower-than-expected private consumption growth. The model is updated for yesterday’s Q1 GDP data but given much of the softness was due to weather events, a July 8 rate cut is likely to be more dependent on more timely monthly data releases and trade negotiation progress.

- The underlying inflation variable in the equation leads by two quarters and is therefore forward looking. The slight positive inflation gap adds pressure for higher rates.

- Our estimate for the output gap has been negative for a year and it continues to show spare capacity going forward, thus putting downward pressure on the cash rate estimates.

- These two effects essentially offset each other in our simple model and with the lagged dependent variable anchoring the calculation, it estimates rates troughing at the end of 2025 at around 3.80%, close the current 3.85%. They then trend gradually towards 3.90%.

- The RBA considers risks around its outlook, which are currently elevated due to global trade events, and many more variables than just GDP and trimmed mean CPI.

- The AUD OIS market has rates trending down into Q1 2026 where they are expected to stabilise in around March.

Australia policy reaction function using trimmed mean inflation

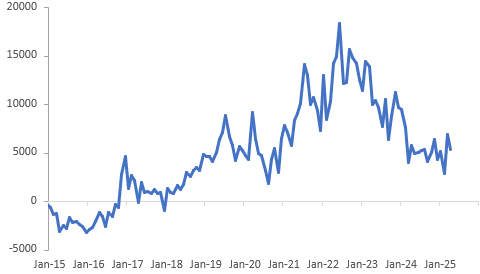

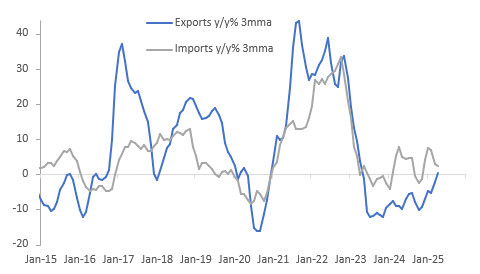

AUSTRALIA DATA: Softer Exports But Capex Imports Up, Surplus Within Recent Range

The April merchandise trade surplus narrowed $1.5bn to $5.4bn but remained above the Q1 average and in line with the levels seen since the end of the post-Covid rebound. There was some payback in the month for the strong increase in March exports, while imports rose at their highest monthly rate since December.

Australia merchandise trade balance $mn

- Merchandise exports fell 2.4% m/m to be up 4.0% y/y in April after +7.2% m/m & +4.6% y/y. Shipments were supported by broad-based strong growth in rural goods (+9.4% m/m & 29.6% y/y).

- The decline in the total was due to a sharp fall in non-monetary gold, which is volatile, but non-rural was down 2.1% m/m to be down 3.6% y/y due to contractions in metal ores and coal, while other mineral fuels and metals rose.

- Goods imports rose 1.1% m/m to be up 5.6% y/y after -2.4% & -2.3% respectively.

- After a very weak March, capex goods posted a broad-based rebound of 7.5% m/m in April to be up 2.8% y/y. Consumer goods were also robust rising 2.8% m/m to be up 6.4% y/y driven by clothing and vehicles. Intermediate imports remained weak with the third straight decline in April at 5.3% m/m but up 1.2% y/y impacted by lower fuel prices.

Australia goods exports vs imports y/y% 3-mth moving average

Source: MNI - Market News/ABS

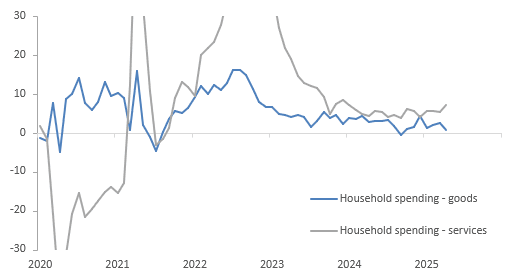

AUSTRALIA DATA: Consumption Made A Soft Start To Q2

Household spending started Q2 on a soft note with the small increase narrowly driven by non-discretionary expenditure and Queensland. The total rose 0.1% m/m in April to be up 3.7% y/y after weather-affected March was revised higher to a 0.1% m/m fall but up 3.8% y/y.

- Goods spending fell 1.1% m/m to be up only 0.9% y/y down from 2.6% y/y, while services jumped 1.5% m/m to be up 7.2% y/y following 5.3% y/y in March. Tourism expenditure had been impacted by extreme weather in Queensland and NSW in March. Spending in Queensland rebounded 2.0% m/m after falling 1.3%.

- The growth in services was driven by recreation, eating out (hotels & restaurants +2.2%) and health while goods were negatively impacted by less spending on clothing (-3.5%) and vehicles.

- Discretionary spending fell 0.2% m/m to be 3.0% higher on a year ago down from 3.4%. This was the second straight monthly decline. In contrast non-discretionary expenditure rose 0.6% m/m to be up 4.9% y/y after 4.7%.

- The household spending release will replace retail sales from 1 August.

Australia household consumption y/y%

BONDS: NZGBS: Bull-Steepener, Apr-29 Supply Sees ~6.0x Cover

NZGBs closed showing a bull-steepener, with benchmark yields 1-3bps lower. While the 2-year finished at session bests, the 10-year yield closed some 4bps higher than its low.

- The April 2029 note auction recorded a bid-to-cover ratio of 5.30x — the second highest since the bond's introduction in 2018, trailing only the 5.995x peak in November 2023. Meanwhile, the May 2035 bond saw a ratio of 2.74x, a notable improvement from 2.11x at its last issuance in December.

- New residential lending falls ~NZ$70m m/m to NZ$8.0b. New residential on fixed terms drops to 70% from 75%.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's strong data-induced rally. The focus is now on today's weekly jobless claims, trade balance, and unit labour costs data.

- "Fed's Kashkari says the labor market is showing some signs of slowing; the Fed must wait and see as the economy faces uncertainty." – Bloomberg

- RBNZ appoints Kate Le Quesne to the new role of Assistant Governor, Enterprise Services.

- Swap rates closed 3-5bps lower, with the 5-year leading.

- RBNZ dated OIS pricing closed flat to 5bps softer across meetings. 6bps of easing is priced for July, with a cumulative 33bps by November 2025.

- Tomorrow, the local calendar will be empty.

FOREX: Asia FX Wrap - BBDXY Can't Bounce, Eye's 1200 Pivot

The BBDXY has had a range of 1207.21 - 1209.24 in the Asia-Pac session, it is currently trading around 1208. “The EU asked China to address its export restrictions on rare earths and magnets, which are causing disruptions for the European car industry. The Asian nation has introduced a tracking system for the products, Reuters reported”. China Data - CAIXIN PMI Services Rises in May: Following the disappointing May CAIXIN PMI Manufacturing, all eyes were on the CAIXIN PMI Services. May's result of +51.1 will be a welcome relief to market watchers. The USD looking at breaking some crucial levels against a range of currencies, the NFP print tomorrow night will be a key input to determine if these can follow through.

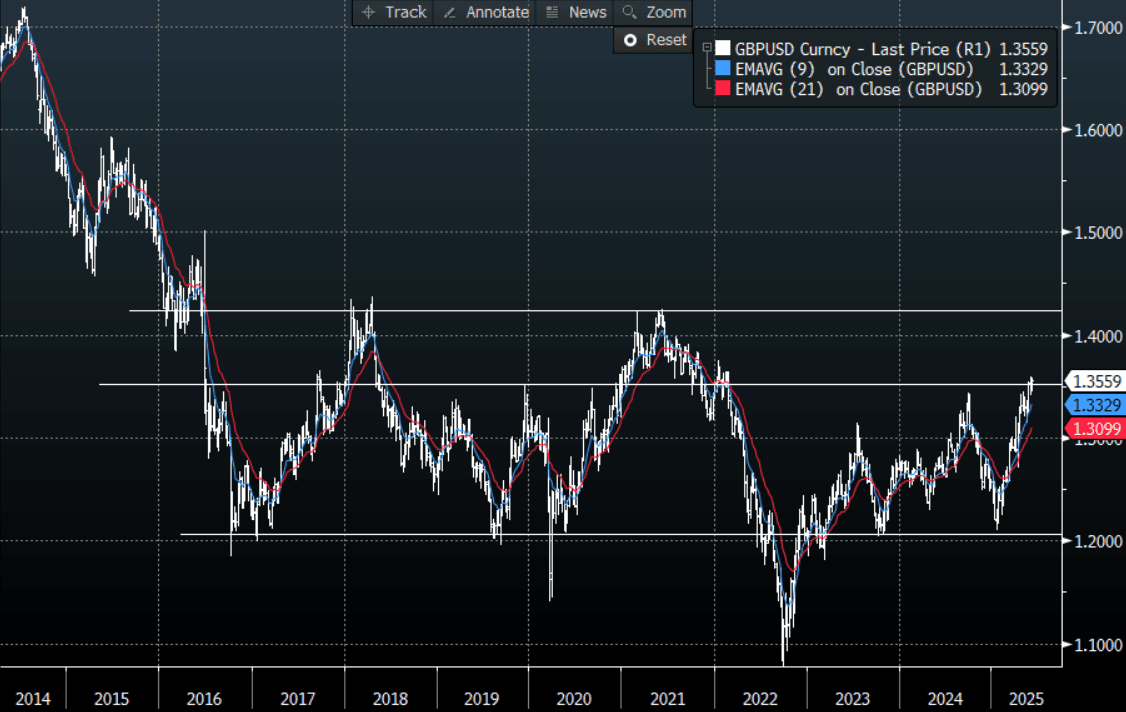

- EUR/USD - Asian range 1.1411 - 1.1435, Asia is currently trading 1.1420. EUR has drifted sideways during the Asian session. Dips should continue to find support while price holds above 1.1100/1200.

- GBP/USD - Asian range 1.3541 - 1.3566, Asia is currently dealing around 1.3560. The GBP is attempting another run higher but is struggling to gain any momentum on a 1.3500 handle. Like USD/JPY its looking to break key weekly levels, NFP will have a say in whether it can be sustained.

- USD/CNH - Asian range 7.1701 - 7.1814, the USD/CNY fix printed 7.1865. Asia is currently dealing around 7.1790. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX -0.10%, Gold $3375, US 10-Year 4.37%, BBDXY 1208, Crude oil $62.64

Data/Events : Germ Factory Orders, Italy Retail sales, EZ PPI, ECB

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

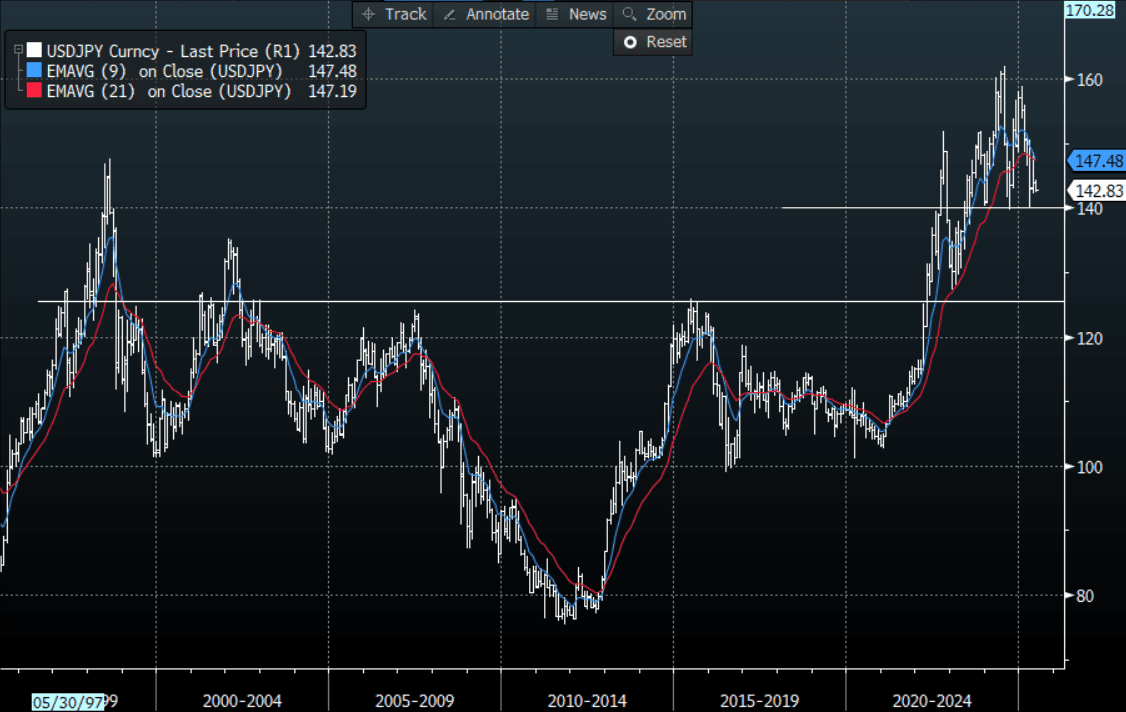

JPY: Asia Wrap - Moves Back To 143.00

The Asia-Pac USD/JPY range has been 142.53 - 142.97, Asia is currently trading around 142.85. USD/JPY had a pop higher just after the Japanese Fix but has failed to follow through above 143.00 in our session.

- April labor earnings data were slightly below market forecasts, but we did see positive revisions. Nominal earnings rose 2.3%y/y, versus 2.6% projected. The March print was revised higher to 2.3%y/y.

- In terms of inflows into Japan bonds, there was a notable step-up by offshore investors in terms of purchases. The 1.165trln in net inflows was the strongest weekly pace since mid-April. This comes at a time when we have seen a faltering appetite at longer-dated JGB auctions.

- The bounce in USD/JPY did not last very long with good selling above 144.00 and aided by the USD again coming under renewed selling pressure.

- A break below 142.00 in USD/JPY and all eyes will once again turn to the pivotal 140.00 area. Will the market be able to challenge the 140.00 area without first seeing what the NFP print is ? A lower NFP and you have to think the market attempts to break lower.

- Traders will be watching the long term pivotal area around 140.00. A break would really see this move accelerate opening up a bigger move back to 125/130

- Sellers should be around today on any bounce back towards the 144.00 area.

Options : Close significant option expiries for NY cut, based on DTCC data: 140.00($2b), 143.00($1.28b). Upcoming Close Strikes : 140.00($1.13b June 6), 142.00($1.56b June 6), 140.00($1.04b June 9).

Fig 1 : USD/JPY Spot Monthly Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - Treads Water With An Eye On 0.6550

The AUD/USD has had a range of 0.6489 - 0.6509 in the Asia- Pac session, it is currently trading around 0.6495. The AUD has had a very quiet session, treading water as it eyes testing the 0.6550 area.

- AUSTRALIA DATA: Consumption Made A Soft Start To Q2. Household spending started Q2 on a soft note with the small increase narrowly driven by non-discretionary expenditure and Queensland. The total rose 0.1% m/m in April to be up 3.7% y/y after weather-affected March was revised higher to a 0.1% m/m fall but up 3.8% y/y.

- AUSTRALIA DATA: Softer Exports But Capex Imports Up, Surplus Within Recent Range. The April merchandise trade surplus narrowed $1.5bn to $5.4bn but remained above the Q1 average and in line with the levels seen since the end of the post-Covid rebound.

- The AUD moved higher overnight bouncing off the demand seen around 0.6450 as the USD came under heavy selling pressure.

- Price is back in the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate. Price looks set to test the top end of the range but I am not sure how far it extends until we get confirmation of a slowdown in labor from the NFP tomorrow night.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6490(AUD1.14b). Upcoming Close Strikes : 0.6300(AUD 1.47b June 6), 0.6420(AUD771m June 10)

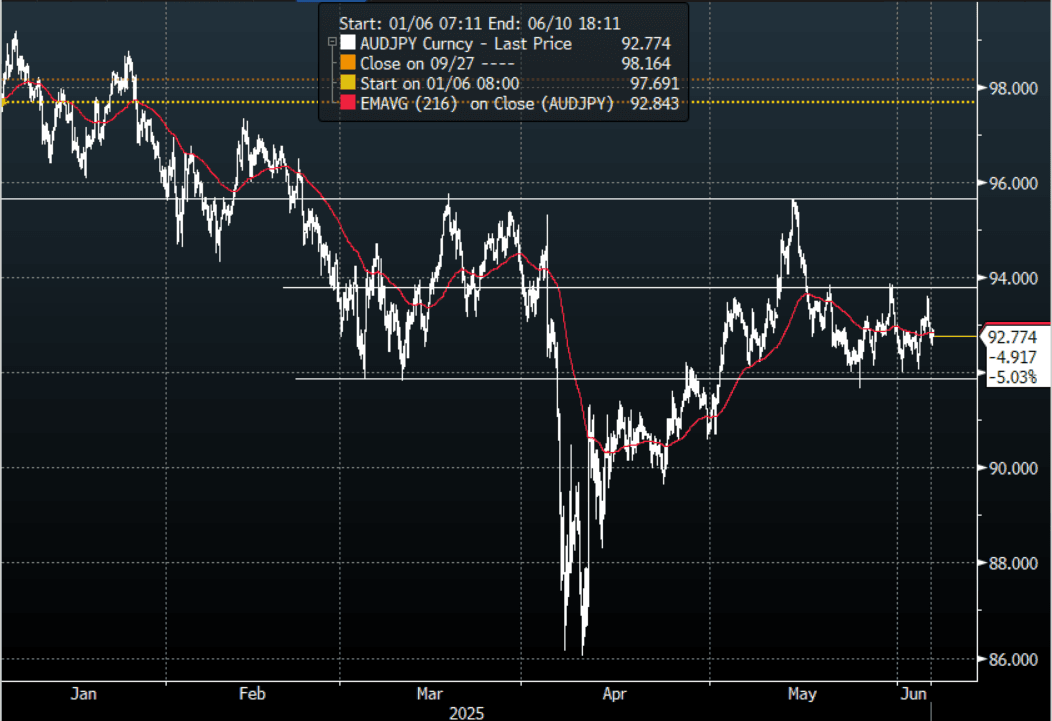

AUD/JPY - Today's range 92.56 - 92.91, it is trading currently around 92.80. Range looks 92.00 - 94.00 for now, a sustained break sub 91.50/92.00 will bring focus back to towards the lows again.

Fig 1: AUD/JPY spot Hourly Chart

Source: MNI - Market News/Bloomberg

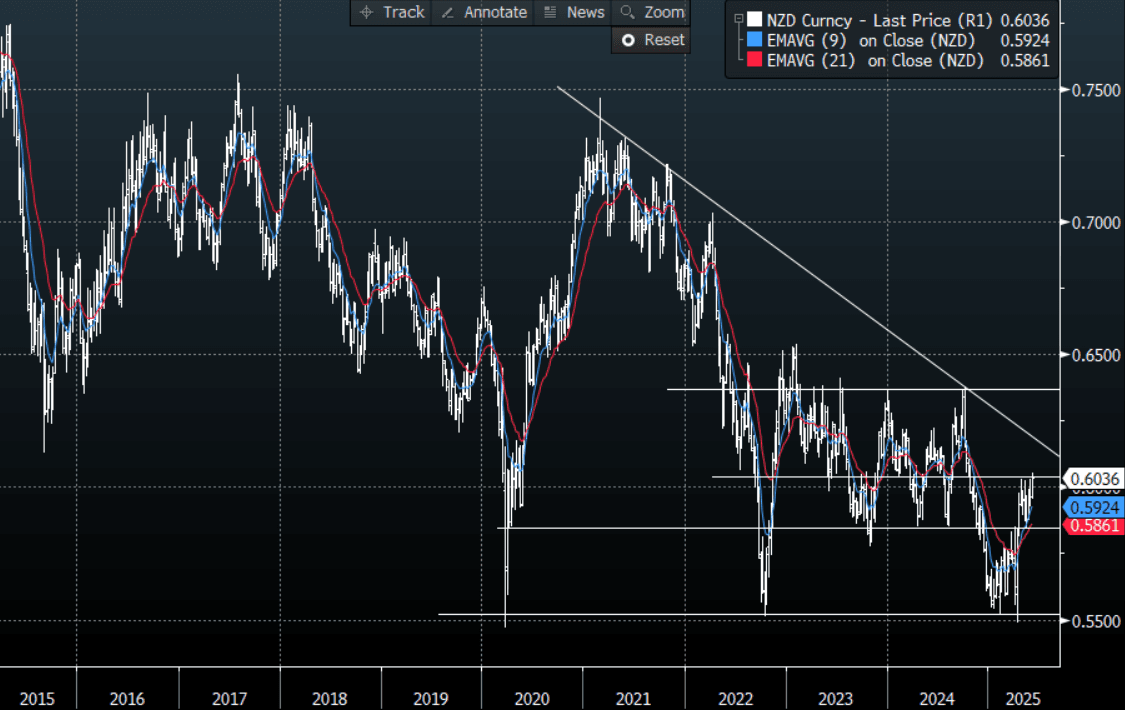

NZD: Asia Wrap - NZD Drifts Higher, Eyeing A Break Above 0.6050

The NZD/USD had a range of 0.6025 - 0.6043 in the Asia-Pac session, going into the London open trading around 0.6035. The NZD has had a quiet session consolidating its recent gains above 0.6000 and now eyes a move above 0.6050.

- ASB Sees All Meetings “Live” But July RBNZ Hold Likely: At its May meeting, the RBNZ said that rates were now in the “neutral zone” and the MPC now no longer had a bias but would monitor events and data very closely. ASB still sees all meetings in 2025 as “live” given that risks are skewed to the downside, but given current uncertainty, it has “pencilled in 25bp cuts in August and October” which still leaves its end-2025 OCR forecast at 2.75%.

- The NZD found solid demand just below 0.6000 as dips remain well supported, aided by the USD again coming under renewed pressure.

- The support back towards 0.5850 has held very well, and while this continues to hold expect buyers to be around on dips. A clear break above 0.6050 could provide the spark for the next leg higher. Can the market be aggressive and sustain a move above this area pre NFP remains to be seen. A low NFP print might be the catalyst it needs though to finally extend higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5990(NZD390m), 0.5895(NZD304m). Upcoming Close Strikes : 0.5880(NZD300m June 10)

AUD/NZD range for the session has been 1.0762 - 1.0776, currently trading 1.0765. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone from the RBNZ last week and AUD/NZD could now see supply on bounces. The sell zone is back towards 1.0800/25 with the first target being around 1.0650.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: A Positive Day for Major Bourses

South Korea's KOSPI rose again today on post election optimism. Korean stocks were supported by the rally in Nvidia's stock with Samsung Electronics and SK Hynix benefitting.

- China's Hang Seng delivered its third day of gains up +0.42% and is up over +2.5% for the week. The CSI 300 didn't take the lead only rising +0.07%, Shanghai a mere +0.08% and Shenzhen up just +0.11%.

- The KOSPI has now rallied three days straight and is up just over 1% today, and over 3% on election optimism.

- Having rallied yesterday to break six straight days of losses, the FSE Malaysia KLCI is up +0.40% today.

- The Jakarta Composite has had a strong day rising +0.70%, following up from yesterday's gains.

- The FTSE Straits Times did very little up +0.02% and the PSEi in the Philippines went the other way down -0.15%

- India's NIFTY 50 is up +0.55% backing up from yesterday's gains.

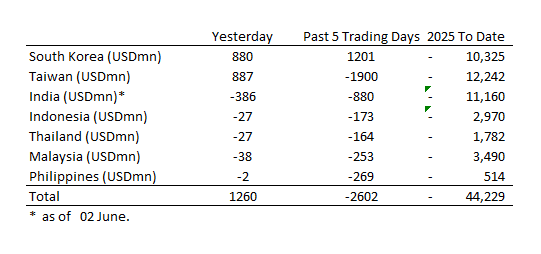

ASIA STOCKS: Large Inflows for Korea and Taiwan

Large inflows for two of the major markets dominated flow data for the 3rd as others saw outflows.

- South Korea: Recorded inflows of +$880m yesterday, bringing the 5-day total to +$1,201m. 2025 to date flows are -$10,325. The 5-day average is +$240m, the 20-day average is +$100m and the 100-day average of -$101m.

- Taiwan: Had inflows of +$887m as yesterday, with total outflows of -$1,900 m over the past 5 days. YTD flows are negative at -$12,242. The 5-day average is -$380m, the 20-day average of +$180m and the 100-day average of -$131m.

- India: Had outflows of -$386m as of the 3rd, with total outflows of -$880m over the past 5 days. YTD flows are negative -$11,160m. The 5-day average is -$176m, the 20-day average of +$28m and the 100-day average of -$112m.

- Indonesia: Had outflows of -$27m as of yesterday, with total outflows of -$173m over the prior five days. YTD flows are negative -$2,970m. The 5-day average is -$35m, the 20-day average +$5m and the 100-day average -$30m.

- Thailand: Recorded outflows of -$27m as of yesterday, outflows totaling -$164m over the past 5 days. YTD flows are negative at -$1,782m. The 5-day average is -$33m, the 20-day average of -$4m and the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$38m as of yesterday, totaling -$253m over the past 5 days. YTD flows are negative at -$3,490m. The 5-day average is -$57m, the 20-day average of +$5m and the 100-day average of -$25m.

- Philippines: Saw outflows of -$2m yesterday, with net outflows of -$269m over the past 5 days. YTD flows are negative at -$514m. The 5-day average is -$54m, the 20-day average of -$14m the 100-day average of -$5m.

OIL: Crude Down Marginally On Saudi Position To Keep Increasing Output

Oil prices are lower again during today’s APAC trading after falling around a percent on Wednesday following disappointing US data and Saudi Arabia keeping its options open to increase output further. WTI is down 0.4% to $62.59/bbl, holding just above the 50-day EMA, after reaching $62.81 earlier. Brent is 0.3% lower at $64.68/bbl after a high of $64.93. The USD index is little changed.

- OPEC has already increased production targets by 411kbd three times this year and Saudi Arabia said it is considering another 411kbd in both August and September to make the most of summer travel demand. It likely also wants to increase its market share but risks pushing prices substantially lower. If the tariff-driven increase in uncertainty drives slower global growth and thus energy demand, it might rethink this position.

- Later the Fed’s Kugler, Harker & Schmid as well as BoE’s Greene & Breeden speak. The ECB is expected to cut rates 25bp and the decision will be followed by President Lagarde’s press conference. US jobless claims, May Challenger job cuts, April trade & final Q1 productivity/ULC, and April German factory orders & euro area PPI print.

Gold Range Trading Ahead Of Friday’s Payrolls, Fed Speak Later

After rising moderately on Wednesday, gold is slightly lower during today’s APAC session. It is down 0.1% to $3368.4 off the intraday high of $3384.18 as it continues to trade below initial resistance at $3392.2, 3 June high. US yields and the greenback are slightly higher, while equities in the region are generally stronger.

- Bullion is set to remain highly sensitive to trade and geopolitical developments, with current issues remaining unresolved.

- It rose on the back of disappointing US data yesterday and will be monitoring May payrolls on Friday closely for signs of recent uncertainty impacting the labour market. 126k new jobs are expected with the unemployment rate steady at 4.2%. An undershoot may increase expectations of Fed cuts in 2025, thus boosting gold prices.

- Geopolitical and trade tensions as well as concern about the greenback appear to be prompting an increase in central bank buying of gold for their reserves, especially by China, according to Bloomberg.

- Equities are mainly higher with the Hang Seng up 0.4% and KOSPI +1.0% but Nikkei is down 0.5% and the S&P e-mini flat. Commodities are generally lower with WTI -0.4% to $62.59/bbl, iron ore down to around $95/t, silver -0.1% to $34.47 but copper slightly higher.

- Later the Fed’s Kugler, Harker & Schmid as well as BoE’s Greene & Breeden speak. The ECB is expected to cut rates 25bp and the decision will be followed by President Lagarde’s press conference. US jobless claims, May Challenger job cuts, April trade & final Q1 productivity/ULC, and April German factory orders & euro area PPI print.

CHINA: Country Wrap: CAIXIN PMI Services Rises in May

- Following the disappointing May CAIXIN PMI Manufacturing, all eyes were on the CAIXIN PMI Services. April had delivered a +50.7 result and market expectations were for an improvement to +51.0. May's result of +51.1 will be welcome relief to market watchers. Despite this improvement, the CAIXIN PMI composite slipped into contraction at +49.6, driven by the decline in manufacturing PMI. (source MNI Market News)

- The EU has urged China to stop restricting the export of rare earth minerals and magnets, with the bloc’s trade chief saying its industries are in an “alarming situation”. The request was made during a meeting between the sides’ top commerce officials in Paris on Tuesday. It comes as sectors across Europe raise the alarm about a shortage of rare earths, which are used to manufacture hi-tech goods ranging from electric cars and smartphones to military tanks and aircraft. “I informed my Chinese counterpart about the alarming situation in the European car industry, but I would say industry as such because clearly rare earths and permanent magnets are absolutely essential for industrial production,” Maros Sefcovic said on Wednesday, briefing reporters a day after his meeting with Chinese Commerce Minister Wang Wentao. (source SCMP)

- China's Hang Seng delivered its third day of gains up +0.42% and is up over +2.5% for the week. The CSI 300 didn't take the lead only rising +0.07%, Shanghai a mere +0.08% and Shenzhen up just +0.11%.

- Yuan Reference Rate at 7.1865 Per USD; Estimate 7.1783

- The PBOC maintained a tight grip on liquidity with a withdrawal via the OMO this morning. Bonds are better bid with the CGB 10YR at 1.70%

SOUTH KOREA: Country Wrap: Holding Companies to Perform

- JPMorgan upgrades Korean holding companies Samsung C&T, SK Inc. and LG Corp. to overweight from neutral, citing expectations for improved corporate governance in the nation after Lee Jae-myung’s election victory. The Democratic Party is “preparing the commercial code revision sooner than initial expectations” and “we see a greater scale of revision (including presidential pledges) that could accelerate capital market reform and corporate governance structure improvement in Korea,” analysts including Jay Kwon write in a note (source BBG)

- South Korea's inflation fell below 2% in May for the first time in five months, increasing 1.9% from the same period last year, but the Bank of Korea warned of persistent risks, Yonhap News reported Wednesday. The South Korean central bank's deputy governor Kim Woong cited exchange rate volatility, global oil prices, and US tariff policies as key concerns, the report said. While inflation may edge up in June due to base effects, it is expected to ease into the 1% range in the second half, driven by weak demand and lower oil prices, it said. (source BBG)

- The KOSPI has now rallied three days straight and is up just over 1% today, and over 3% on election optimism.

- The Won was the best regional performer gaining +0.37% to 1,358.74

- Bonds rallied today after yesterday's record sell off. The long end was hit hard yesterday following a very weak auction. The 30yr finished higher in yield by +13bps yesterday and unsurprisingly has rallied today, lower by -3bps. KTB 10yr at 2.88%

INDIA: Country Wrap: RBI to Cut Rates at June Meeting

- RBI Preview: We see the RBI cutting rates at the June meeting given Inflation falling below target, Ongoing concerns about global uncertainties feeding into data such as industrial production and concerns about the currency not currently a factor. (source MNI Market News)

- With US trade negotiators set to reach India Thursday for a two-day visit, the India-US trade deal negotiations are entering their final stage and could soon see Delhi opening its market and lowering tariffs on a range of American products - from select agricultural goods to defence equipment. This is in exchange for concessions on reciprocal tariffs and improved access to the US market for India's labour-intensive sectors such as textile and leather products. The White House said Tuesday that the US had asked countries to make their best offers on trade negotiations by Wednesday, as the July 8 deadline for reciprocal tariffs is just five weeks away. "I can confirm the merits and the content of the letter. The United States Trade Representative (USTR) sent this letter to all of our trading partners just to give them a friendly reminder that the deadline is coming up," White House spokesperson Karoline Leavitt said. (source BBG)

- India's NIFTY 50 is up +0.55% backing up from yesterday's gains.

- The rupee was marginally weaker today, down -0.05% at 95.94

- Bonds are lower in morning's trade with the IGB 10yr at 6.24%

CHINA: CAIXIN PMI Services Rises in May

- Following the disappointing May CAIXIN PMI Manufacturing, all eyes were on the CAIXIN PMI Services

- April had delivered a +50.7 result and market expectations were for an improvement to +51.0.

- May's result of +51.1 will be welcome relief to market watchers.

- Despite this improvement, the CAIXIN PMI composite slipped into contraction at +49.6, driven by the decline in manufacturing PMI.

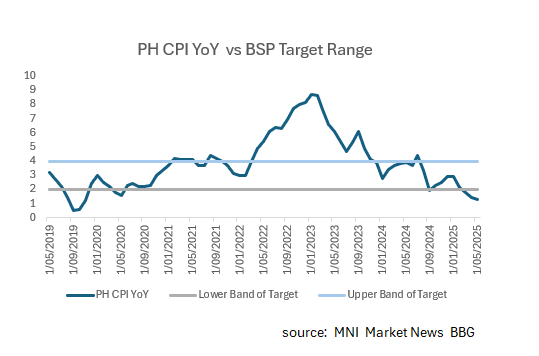

PHILIPPINES: CPI Moderates Further

- The Philippines' consumer prices rose in line with market expectations for May

- Consumer prices rose 1.3% YoY (Survey +1.3%) in May versus +1.4% in April, according to the Philippine Statistics Authority

- Core consumer prices rose 2.2% YoY

- Capital region consumer prices rose 1.7% YoY

- Consumer prices rose 1.9% YoY from January to May

- Consumer prices fell 0.1% MoM (estimate -0.1%)

- Inflation rose at slowest pace since Nov. 2019

- The Central Bank (the BSP) has a target inflation range of 2-4% YoY. Recent reports suggest they are contemplating moving to a fixed 2% YoY

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 05/06/2025 | 0545/0745 | ** | Unemployment | |

| 05/06/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/06/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 05/06/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/06/2025 | 0745/0845 | BOE's Greene Opening Remarks at Econdat Conference 2025 | ||

| 05/06/2025 | 0800/1000 | * | Retail Sales | |

| 05/06/2025 | 0830/0930 | Decision Maker Panel data | ||

| 05/06/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/06/2025 | 0900/1100 | ** | PPI | |

| 05/06/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 05/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 05/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 05/06/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1245/1445 | ECB Press Conference | ||

| 05/06/2025 | 1400/1000 | * | Ivey PMI | |

| 05/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 05/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/06/2025 | 1600/1200 | Fed Governor Adriana Kugler | ||

| 05/06/2025 | 1620/1220 | BOC Deputy Kozicki speech | ||

| 06/06/2025 | 2330/0830 | ** | Household spending | |

| 06/06/2025 | 0600/0800 | ** | Trade Balance | |

| 06/06/2025 | 0600/0800 | ** | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Foreign Trade | |

| 06/06/2025 | 0830/1030 | ECB Lagarde Video Message For CIBP Anniv | ||

| 06/06/2025 | 0900/1100 | ** | Retail Sales | |

| 06/06/2025 | 0900/1100 | *** | GDP (final) | |

| 06/06/2025 | 0900/1100 | * | Employment | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1230/0830 | *** | Employment Report | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey |