JAPAN DATA: Real Earnings Remain Firmly Negative, Scheduled Pay Firms Y/Y

Japan April labor earnings data were slightly below market forecasts, but we did see positive revisions. Nominal earnings rose 2.3%y/y, versus 2.6% projected. The March print was revised higher to 2.3%y/y (originally reported as a 2.1% gain). In real terms earnings were -1.8%y/y (against a -1.6% forecast and revised -1.8% outcome for March). Cash earnings on a same sample basis were 2.6%y/y, also below forecasts of 2.8% y/y, but March was revised higher to 2.7%y/y. Full-time pay, on the same base, was 2.5%y/y, above the 2.3% forecast. prior was 2.1%.

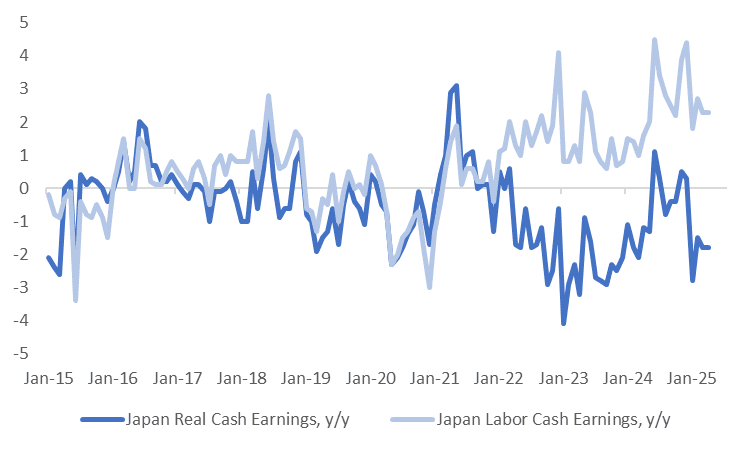

- The chart below plots nominal and real cash earnings in y/y terms. Nominal earnings are off highs but still elevated by historical standards. The lack of positive trends in real earnings will be a disappointment for the authorities though. We have had a few positive y/y readings in recent years, but these have proved fleeting.

- Bonus payments were +4.1%y/y, versus the 14.5% pace seen in March. Hours worked were -1.2%y/y, compared with -2.7% in March.

- On the same sample basis, scheduled and full time pay saw y/y rises compared to the March outcome. We are sub 2024 y/y highs for these metrics, but still this helps offset to some degree the disappointing headline nominal and real earning outcomes.

- The data is unlikely to shift near term BoJ thinking, with the mid June policy meeting outcome expected to deliver no policy rate change.

Fig 1: Japan Nominal & Real Cash Earnings - Y/Y

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Modestly Cheaper, Subdued Monday, FOMC On Wed

ACGBs (YM -3.0 & XM -3.5) are modestly cheaper after further selling of US tsys on Monday.

- A stronger-than-expected ISM services index helped US equities recover early losses and pushed up US yields. The UK and some Asian markets were closed for holidays.

- The US ISM services index unexpectedly rose 0.8pts in April, against expectations for a modest fall following the steep fall in March. Both the employment and new orders indices rose. The prices paid index rose 4.2pts to a more than two-year high of 65.1.

- Focus remains on Wednesday's FOMC rate announcement.

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at -4bps.

- The bills strip is flat to -2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 50bp rate cut in May is given a 2% probability, with a cumulative 104bps of easing priced by year-end.

- Today, the local calendar will see Building Approvals and Household Spending data.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond today, A$1000mn of the 3.75% 21 April 2037 bond on Wednesday and A$700mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Cheaper After Another Heavy Session For US Tsys

In local morning trade, NZGBs are 2-3bps cheaper across benchmarks after another heavy session for US tsys. US tsys did, however, finish off session cheaps as rates reacted to a reversal in US equities.

- Generally quiet session on lighter volumes (TYM5 <1M) with multiple spring holidays around the globe: Japan, China, HK, South Korea, and the UK. The EU was open, however.

- Focus remains on Wednesday's FOMC rate announcement at 1400ET. The FOMC is expected to extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement.

- US yields gapped higher after higher-than-expected ISM Services data, climbing to the highest levels since January 2023.

- Swap rates are flat to 2bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is little changed across meetings. 26bps of easing is priced for May, with a cumulative 76bps by November 2025.

- Today, the local calendar will see ANZ Commodity Price data.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 2.75% May-51 bond.

JPY: USDJPY - JPY Benefits From The Move Lower In USD/Asia

The overnight range was 143.54 - 144.43, Asia is currently trading around 143.75.

- Bloomberg - Taiwan’s central bank sought to tamp down speculation on foreign exchange markets, saying market chatter is partially responsible for the local currency’s two straight days of wild appreciation not seen since the 1980s. Given the move in USD/TWD the market will be fixated on potential trade deal headlines this week.

- The FOMC on Wednesday will be watched closely, MNI Economist - “The FOMC will extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement. As the FOMC awaits clarity in both government policy and the data on the degree to which one if not both dual mandate targets will be missed, most participants will continue to support a holding pattern until there is a clearer signal to act. Don’t anticipate any meaningful changes in the Statement, though any signal that the Fed is looking seriously at “soft” survey data to assess the outlook could be significant.”

- USD/JPY the 145.50/1.4700 area proved to be tough to get through initially. The JPY has benefited from the capitulation in a host of USD/Asia trades, led by USD/TWD.

- Look for some support initially back towards 143.00, but we would probably need another catalyst to test below that again. Which probably makes a range of 143-147 for the week likely.

- CFTC data shows Asset managers continuing to add to already significant JPY longs, leveraged funds seems to have pared their shorts back a little.

- Data : US FOMC on Wednesday

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg