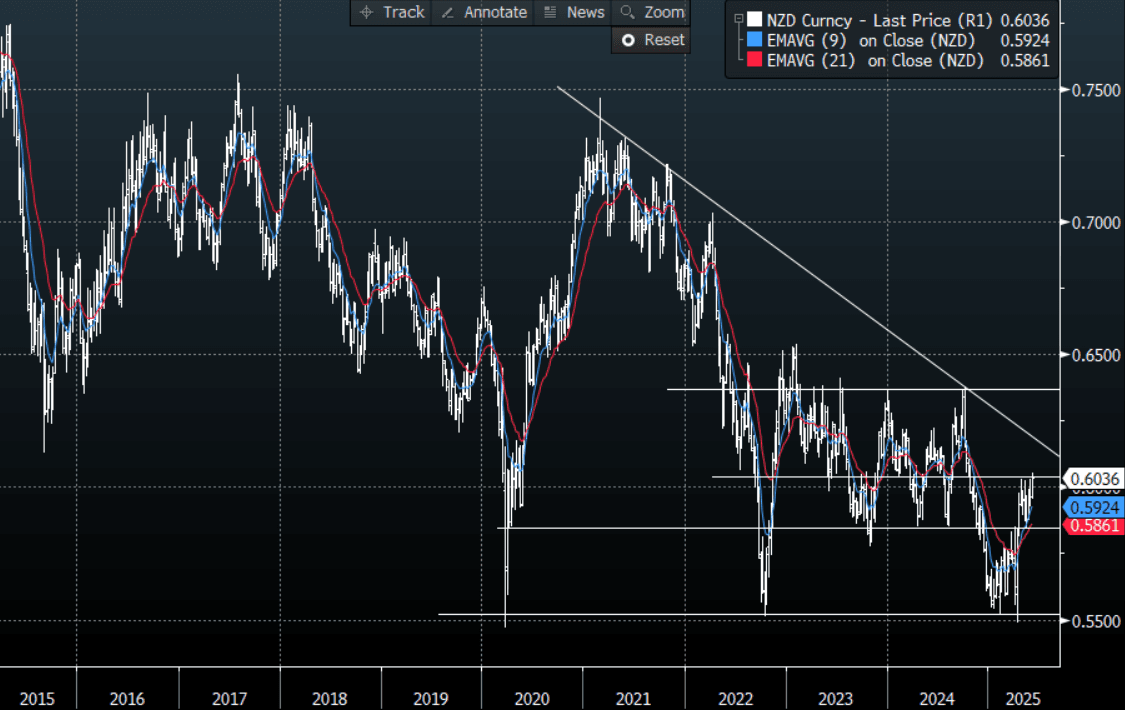

NZD: Asia Wrap - NZD Drifts Higher, Eyeing A Break Above 0.6050

The NZD/USD had a range of 0.6025 - 0.6043 in the Asia-Pac session, going into the London open trading around 0.6035. The NZD has had a quiet session consolidating its recent gains above 0.6000 and now eyes a move above 0.6050.

- ASB Sees All Meetings “Live” But July RBNZ Hold Likely: At its May meeting, the RBNZ said that rates were now in the “neutral zone” and the MPC now no longer had a bias but would monitor events and data very closely. ASB still sees all meetings in 2025 as “live” given that risks are skewed to the downside, but given current uncertainty, it has “pencilled in 25bp cuts in August and October” which still leaves its end-2025 OCR forecast at 2.75%.

- The NZD found solid demand just below 0.6000 as dips remain well supported, aided by the USD again coming under renewed pressure.

- The support back towards 0.5850 has held very well, and while this continues to hold expect buyers to be around on dips. A clear break above 0.6050 could provide the spark for the next leg higher. Can the market be aggressive and sustain a move above this area pre NFP remains to be seen. A low NFP print might be the catalyst it needs though to finally extend higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5990(NZD390m), 0.5895(NZD304m). Upcoming Close Strikes : 0.5880(NZD300m June 10)

AUD/NZD range for the session has been 1.0762 - 1.0776, currently trading 1.0765. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone from the RBNZ last week and AUD/NZD could now see supply on bounces. The sell zone is back towards 1.0800/25 with the first target being around 1.0650.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRALIA DATA: House Approvals Weak In March

Building approvals in March were significantly weaker than expected falling 8.8% m/m with the more stable private houses component down 4.5% m/m. Multi-dwelling approvals fell 15.1% m/m, the second consecutive monthly fall. Housing shortages persist and this is an unfortunate development but appears also to have been impacted by Cyclone Alfred with Queensland recording a drop in house approvals but Victoria was also weak.

- Total building approvals are now up 13.4% y/y after 26.5% y/y in February with private houses down 3.3% y/y, the lowest since November 2023, but apartments still up 47.1% y/y.

- The ABS said that the weakness in house approvals was driven by Queensland and Victoria, while for non-houses there was a sharp drop in Victoria.

- The value of total residential building approved fell 7.6% m/m in March.

- Victoria is making up over half of the value of non-residential building, which may be crowding out the residential sector given skill shortages in construction.

Australia no. of residential building approvals y/y%

AUSTRALIA DATA: Q1 Spending Volumes Flat, March Saw Cyclone Impact

March household spending was weaker-than-expected falling 0.3% m/m to be up 3.5% y/y after an upwardly-revised +0.3% m/m & 3.6% y/y. Q1 volume data was also released, which is now seasonally adjusted. It showed no growth on the quarter, in line with retail sales, to be up only 0.9% y/y after +1.6% q/q & 2.3% y/y in Q4, consistent with the view that the RBA is likely to ease 25bp on May 20. Private consumption in the national accounts is likely to be close to flat in Q1 when it is released on June 4.

Australia household consumption volumes q/q% sa

- The decline in March was impacted by Cyclone Alfred with it falling 1.3% m/m in Queensland but food spending there rose 2.9% m/m.

- The March weakness was driven particularly by services spending which fell 0.7% m/m but is still up 5.1% y/y. Goods rose 0.1% m/m to be up 2.3% y/y.

- Non-discretionary expenditure continues to exceed discretionary as cost-of-living pressures persist. The former was flat in March to be up 4.4% y/y, while the latter fell 0.4% m/m to be steady at 3.0% y/y.

- The softness in Q1 volumes was driven by alcohol & tobacco spending (-5.9% q/q & -16.5% y/y) and hotels & restaurants (-1.2% q/q & -0.7% y/y). Recreation & culture posted another solid quarterly rate.

Australia consumption discretionary vs non-discretionary y/y%

Source: MNI - Market News/ABS

AUSSIE BONDS: Cheaper Despite Weaker Domestic Data

ACGBs (YM -3.0 & XM -6.0) are weaker and near Sydney session cheaps.

- Building approvals fell 8.8% m/m (estimate -1.5%) in March versus a revised -0.2% in February.

- “Australia's household spending declined 0.3% in March, contrary to a forecast 0.2% increase, due to the impact of a major storm in the nation's northeast. Spending dropped in Queensland by 1.3%, particularly in transport and health, and nationally, six of the nine spending categories declined in March.” (per BBG)

- Cash US tsys dealings in today’s Asia-Pac session with Japan out. TYM5 is slightly cheaper.

- Cash ACGBs are 3-6bps cheaper, with the AU-US 10-year yield differential at -2bps.

- Today’s auction result extended the recent trend of firm pricing for ACGBs, with the weighted average yield printing 0.28bps through prevailing mids, according to Yieldbroker. However, demand moderated somewhat, as reflected by a cover ratio of 2.4833x, down from 2.7067x at the previous auction.

- The bills strip has bear-steepened, with pricing flat to -4 across contracts.

- RBA-dated OIS pricing is flat to 2bps firmer across meetings today. A 50bp rate cut in May is given a 3% probability, with a cumulative 103bps of easing priced by year-end.