MNI EUROPEAN MARKETS ANALYSIS: Japan Fiscal Remains In Focus

- Focus remains on Japan's fiscal package from the new Takaichi regime. Whilst details aren't finalized, Rtrs notes the package could be larger than last year's. Japan asset sentiment has been fairly steady though (USD/JPY holding under 152.00, JGB futures a little higher). The USD is a touch softer elsewhere, with US Tsy yields ticking down a touch, while equity futures have been supported on dips.

- Profit taking in gold and silver begun on Tuesday continued early in Wednesday’s APAC trading but the declines have been more than unwound and both are now slightly higher on the day. Gold 1 month volatility remains very elevated.

- Later UK September CPI data print and ECB President Lagarde and Board members Buch and de Guindos speak.

MARKETS

US TSYS: Modest Declines in Yields Again Today

Bond futures finished -01 lower today for TYZ5 on low volumes, looking for a catalyst for the next move .

- The US 2-Yr did very little all morning before rising modestly to 3.465 in the afternoon trading session.

- The US 5-Yr ground was flat at 3.56%

- The 10-Yr has consolidated below 4.00%, rallying again modestly by -0.5bps to reach 3.96% in line with October 24 yield levels.

- The 30-Yr continues to outperform rallying -0.5bps overnight to reach 4.53%. Likely next inflection point could be the April lows of 4.40%.

- Yield moves are appearing disjointed relative to current interest rate pricing as the government shutdown continues as bond traders agonize over the potential impact on the economy. New ranges are being defined and as markets await the release of the September CPI, markets appeared skewed towards lower yields for now.

- There is limited Tier 1 data releases for markets to follow tonight, only MBG mortgage applications. Equity weakness in Asia will be watched for any follow through particularly as many bourses reach new highs.

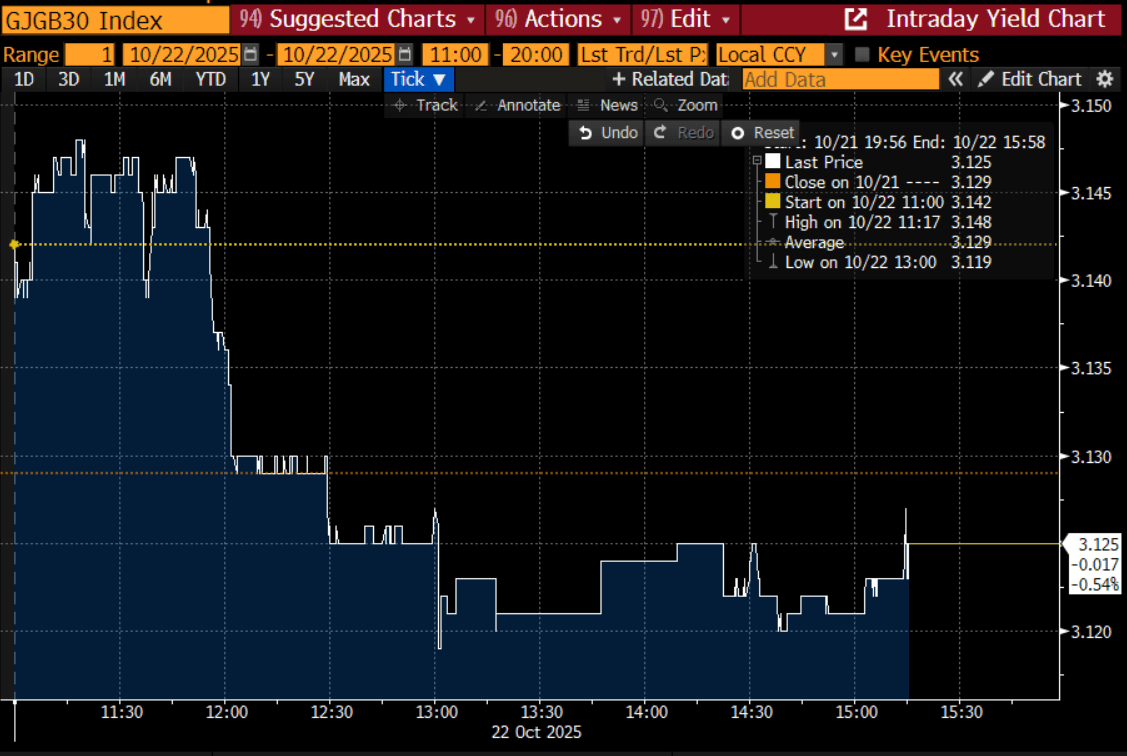

JGBS: Slightly Richer As Market Digests Fiscal Policy News

JGB futures are slightly stronger, +2 compared to the settlement levels, but well off session lows.

- Headlines have crossed from Japan's Growth Strategy Minister Minoru Kiuchi. Kiuchi stated that the focus now is compiling an economic stimulus package, albeit with one eye still on fiscal discipline (DJ) (and diverse funding sources). Various ministers are being consulted, with a focus on helping tariff impacted sectors. Kiuchi stated that no timeline is set for when the economic package will be compiled. Early focus for markets for the new Takaichi regime is fiscal stimulus, in terms of size and how it will be funded (particularly with parallels drawn with the Abenomics-like policy set).

- Cash US tsys are slightly richer in today's Asia-Pac session.

- Cash JGBs are flat to 1bps richer across benchmarks, but significantly better than early session yield highs, as the market digested today’s news on the fiscal policy.

- The benchmark 30-year yield is 0.6bp lower at 3.125% versus the session high of 3.148%. (see chart) Notably, the current yield is more than 20bps below the cycle high of 3.351%, hit shortly after Takaichi was announced as the LDP leader.

- Swap rates are little changed.

- Tomorrow, the local calendar will see Weekly International Investment Flow data alongside Auction for Enhanced-Liquidity 15.5-39 YR.

Bloomberg Finance LP

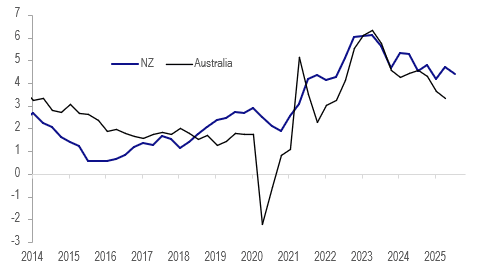

AUSTRALIA: NZ CPI Data Suggests Stable Q3 Australian Core

Q3 NZ CPI was released this week and given high correlations it has some information for Australia’s CPI out on 29 October. The RBNZ’s sector factor model measure of core was stable at 2.7% y/y in Q3 signalling that Australia’s may also remain around Q2’s 2.7%, which is consistent with monthly data. NZ’s domestic-related non-tradeables and services annual inflation moderated while goods and tradeables were higher.

Australia vs NZ underlying CPI y/y%

- NZ services inflation moderated to 4.4% y/y in Q3 from 4.7% while it picked up to 1.2% q/q from 1.1%. There is around an 85% correlation with Australia’s headline annual services inflation and 50% with the quarterly rate. Even if there is an increase in Australia’s quarterly rate in Q3 from Q2’s 0.7%, the 3.3% annual rate should moderate given it rose 1.1% q/q in Q3 2024.

- NZ’s services inflation has been running well ahead of Australia’s and has seen little disinflation since the start of 2024, which may be warning.

- It is worth noting though that the RBA focuses on market services (ex volatile items) which rose 0.6% q/q & 2.9% y/y in Q2. Governor Bullock has stated that the RBA was concerned about some of the components and sticky services prices overseas.

- NZ non-tradeables moderated 0.2pp to 3.5% y/y in Q3 and Australia’s could also ease given the correlation is over 90%. The two have been trending lower for around 2 years.

- NZ goods and tradeables inflation picked up in Q3, which given the global nature of many and high correlations Australia could see this too.

- Australia’s headline CPI continues to be impacted by temporary government electricity rebates and so it is currently not helpful to look at the relationship with NZ.

Australia vs NZ services CPI y/y%

Source: MNI - Market News/LSEG

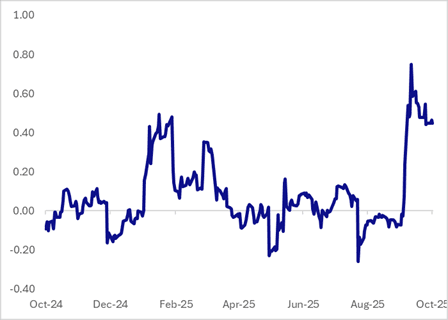

AUSSIE BONDS: Subdued Session, Market Scales Back Chances Of A Nov Cut

ACGBs (YM -0.5 & XM +1.0) are slightly mixed.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +15bps.

- The bills strip is -1 to -2 across contracts.

- A 25bp rate cut in November is assigned a 64% probability, with a cumulative 23bps of easing priced by year-end.

- Compared with previous instances in this easing cycle, the market appears less confident than usual about a November 4 cut.

- This caution aligns with the RBA’s pattern over the past year of easing less than what six-month forward expectations had implied. Those expectations currently sit around 3.20%, compared with the cash rate of 3.60%. (see chart)

- The local data calendar remains fairly quiet throughout the week.

- Today’s auction of the Jun-35 showed solid pricing for ACGBs, with the weighted average yield coming in 0.43bps below prevailing mid-yield. However, the cover ratio nudged lower to 2.9056x from 3.2958x at the previous auction.

- The AOFM plans to sell A$800mn of the 2.75% 21 November 2029 bond on Friday.

- QTC has priced a A$2 billion increase to its 4.50% August 22, 2035 A$ fixed rate benchmark bond, according to BofA Securities. - BBG

Figure 1: RBA Cash Rate Vs. OIS 6M1M (6M Ago)

Source: Bloomberg Finance LP / MNI

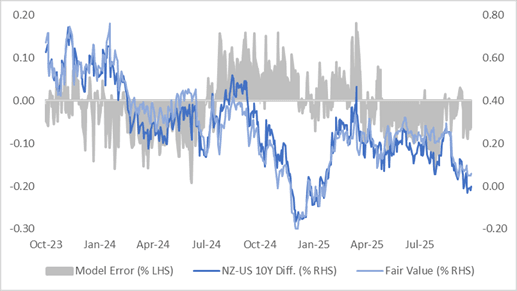

BONDS: Closed With A Bear-Flattener, NZ-US 10Y Diff Looks Too Low

NZGBs closed showing a bear-flattener, with benchmark yields flat to 2bps higher.

- On a relative basis, the NZGB 10-year has underperformed its US tsy counterpart, with the NZ-US yield differential 2bps higher at flat. (see chart)

- A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the current differential is 6bps below its estimated fair value of +6bp

- “NZ's central bank considered Hayley Gourley as a potential board member and recommended that option to the government before she was appointed to the MPC.” – BBG

- “NZ is relaxing climate reporting rules due to concerns over the cost to businesses, with companies listed on the NZX only having to provide disclosures if their market capitalisation is NZ$1 billion or more.” - BBG

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 39bps by February 2026.

- The local calendar will be empty until next Tuesday's release of Filled Jobs data for September.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

FOREX: USD Largely Holding Recent Gains, Japan Fiscal Package May Exceed Last Yr

The USD index sits a touch off Tuesday session highs, last near 1212. Cross asset trends have focused on gold volatility, although this hasn't spilled over much to the majors, with moves at 0.20% or less at this stage (AUD and NZD are ticking up). US equity futures have been supported on dips, while US Tsy yields continued to bias lower, which could be capping US upside, although this most recent BBDXY index bounce has come with the real US 10yr yield falling back to 1.70% (not far off Sep lows). Policy initiatives from the new Japan government have been the other focus point, but again Japan wide asset moves are not significant, with further details awaited.

- Japan's Growth Strategy Minister Minoru Kiuchi stated that the focus now is compiling an economic stimulus package, albeit with on eye still on fiscal discipline (DJ) (and diverse funding sources). Various ministers are being consulted, with a focus on helping tariff impacted sectors, along with cost of living relief. Kiuchi stated that no timeline is set on when the economic package will compiled.

- Following Rtrs reported: "JAPAN'S NEW PM TAKAICHI IS PREPARING ECONOMIC STIMULUS EXPECTED TO EXCEED LAST YEAR'S 13.9 TRILLION YEN ($92.2 BILLION), SOURCES SAY", although details aren't finalised yet, with the package potentially out next month.

- USD/JPY has held under 152.00 today, but dips to 151.50 have been supported. Japan equities are modestly higher, while JGB yields are drifting slightly lower.

- AUD and NZD have ticked up, likely aided by the rise in US equity futures. Local news flow has been light. AUD/USD is back around 0.6500, while NZD/USD has edged up to 0.5750, with upside focus to rest at the 0.5760 region (also note the 20-day EMA is at 0.5770/75).

- Later UK September CPI data print and ECB President Lagarde and Board members Buch and de Guindos speak.

ASIA STOCKS: Stocks Pull Back On AI-Related Profit Taking

Bellwether tech stocks declined over 1% today in Asia as a lackluster forecast from Texas Instruments saw it's stock fall, and others follow. After many of the key tech stocks in Asia hitting new highs recently, it is unsurprising to see falls as profit takers step in. Demand remains robust and export data from countries like Korea and Taiwan show that export growth remains strong, suggesting that whilst the outlook remains strong, a re-rating in expectations can occur.

- Major Asian bourses have hit new highs over the last week and have followed each other lower today, with the NIKKEI leading the falls. The NIKKEI is down -0.60% after hitting new highs yesterday as investors seek to understand the outcome of political negotiations to form a new government.

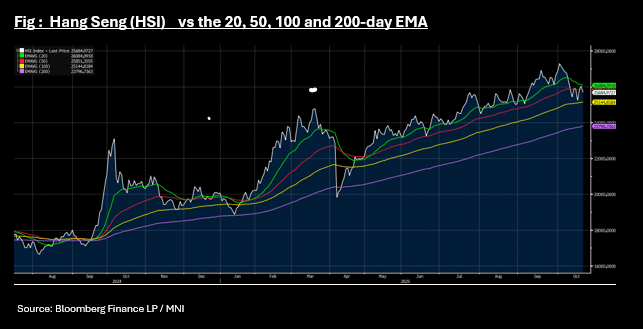

- China's major bourses are down also with the Hang Seng falling -1.3% and back below the 50-day EMA it trended above only yesterday. Other onshore bourses are down with the CSI 300 has pulled back -0.705 and near to the 20-day EMA again, whilst Shanghai and Shenzhen are down -0.45% and -0.55% respectively.

- The KOSPI is an outlier today, reaching yet another new high of 3,835 to be up +0.29%.

- Ahead of the BI decision later, the JCI is down -0.6% as markets await what appears to be an imminent rate cut.

- Headlines have crossed from Indian news source Mint, that a US-India trade deal will soon see tariff rates fall sharply. Some key quotes are outlined below, but notably the article states tariff rates may come down form 50% to 15-16%. Market optimism around a trade deal has been growing, given recent Trump remarks that India would curb Russian oil imports. The NIFTY 50 has reached a new high of 25,866, up +0.10% in morning trade.

OIL: Report US-India Deal Close Drives Oil Higher, EIA US Stock Data Out Later

Oil has found support today from data showing a US inventory drawdown and news that the US and India are close to a deal to gradually reduce India’s Russian oil imports and US tariffs. Less Indian consumption of Russian crude would increase its demand for other sources boosting prices. WTI is up 1.7% to $58.23/bbl following a high of $58.38, remaining below the 50-day EMA at $61.76. Brent is 1.5% higher at $62.26/bbl after reaching $62.47 (50-day EMA $65.35).

- A US-India trade deal is apparently close to completion which would allow the current 50% US duties to be reduced to around 15%, according to Bloomberg citing Mint. US President Trump has said recently that Indian PM Modi had agreed to ending imports of Russian oil. Mint is saying that the agreement could be announced at the 26-28 October ASEAN meeting.

- Oil has also found support from Tuesday’s announcement that a million barrels with delivery in December and January will be purchased for the US’ SPR, which reached a low in July 2023 and was only 17% higher last week.

- After rising the previous week, Bloomberg reported US oil inventories fell 3mn barrels last week, according to people familiar with the API data. Product stocks were also lower with gasoline down 0.2k and distillate 1mn. The official EIA data is out Wednesday.

- Later UK September CPI data print and ECB President Lagarde and Board members Buch and de Guindos speak.

Gold & Silver’s Early Wednesday Decline Short-Lived, USD Slightly Softer

Profit taking in gold and silver begun on Tuesday continued early in Wednesday’s APAC trading but the declines have been more than unwound and both are now slightly higher on the day. The moderate decline in the US dollar, unchanged US yields and weaker equities appear to have driven the recovery. Traders have been long, with the extent unclear due to the lack of CFTC positioning data because of the US government shutdown, and Tuesday’s sell off appears to have been driven by repositioning as both metals are in overbought territory.

- Gold reached a low of $4004.26, below the 20-day EMA at $4021.6, but has recovered to be 0.2% higher at $4131.2, just below support at $4140.8 and off today’s peak at $4143.28. It remains overbought.

- Silver fell to $47.550 earlier but is now up 0.5% to $48.94, still below the 20-day EMA at $49.089. The 50-day EMA at $44.996 is a level to watch.

- Equities are generally weaker with the Hang Seng down 1.3%, Nikkei -0.5% but S&P e-mini close to flat. Oil prices are stronger with WTI +1.7% to $58.20/bbl. Copper is down 0.1%.

- Later UK September CPI data print and ECB President Lagarde and Board members Buch and de Guindos speak.

MNI BOK Preview - October 2025: On Hold as Housing Remains Key

Download MNI BOK Preview Here:

We see the BOK on hold tomorrow due given:

- The Government's focus on the housing market with policies aimed at cooling prices.

- Trade uncertainties remaining, with no trade deal finalised and the Won suffering accordingly.

- Growth has been revised up moderately with export strength evident, yet remains below longer term averages.

- Inflation remains subdued and future expectations anchored, given ongoing downward pressure on oil.

SOUTH KOREA: BoK Market Pricing Expectations

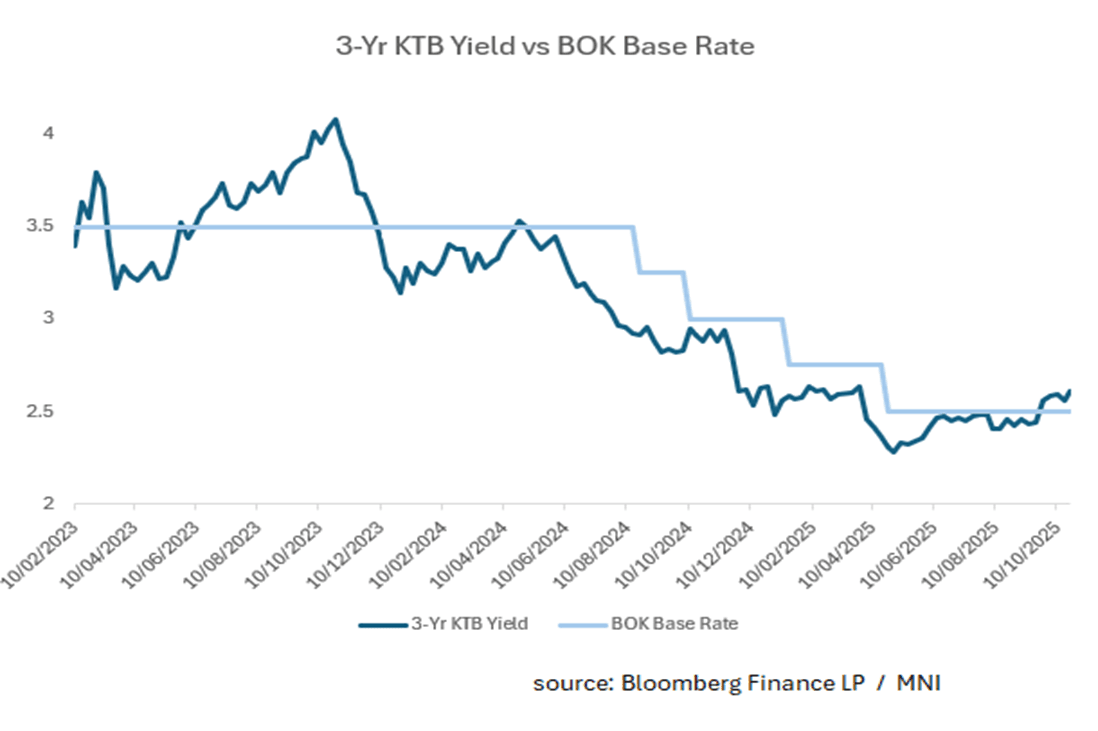

- Since October 2024 the Bank of Korea has cut rates four times but in April went on hold, following the release of the initial real estate policy changes by the then new government. The BOK then cut rates in again in May.

- Following the last BOK meeting the 3YR yield widened pushing out to near term highs of 2.63%, and is currently at 2.60% The move higher (and above the base rate) coincides with the various announcements of measures to calm the housing market and suggests the bond market is expecting little at tomorrow’s meeting.

- The 10YR government bond yield moved higher in September driven by 10-yr issuance, with lower-than-normal correlation to the move in US yields over that period.

- The bond curve and swaps curve have largely priced out the cuts priced in earlier this year. As at today, the bond curve has no cuts priced in over the next month and -8bps of cuts over the next three.

- The swaps curve doesn't have a full rate cut priced in now over next 12 months, expecting next to no movement in rates.

INDONESIA: Softer Activity Data Consistent With Another BI Rate Cut

Bank Indonesia (BI) is expected to cut rates for the fourth consecutive month at its decision today bringing them to 4.5%. Of the 39 analysts on Bloomberg 29 are forecasting another easing. BI seems to have become pro-growth in support of government efforts to boost the economy and away from its recent focus on FX stability. Lacklustre activity data since the 17 September decision backs another cut.

Indonesia activity outlook

Source: MNI - Market News/Bloomberg Finance L.P./LSEG

- In September BI noted that “economic growth in Indonesia must be increased in line with economic capacity” suggesting that it believes there is a negative output gap.

- It observed that Q3 consumption is “restrained” given lower sentiment driven by a weaker labour market. Q3 average consumer confidence was 1.8% below Q2 signalling that real consumption slowed in the quarter. Retail sales growth in August moderated to 3.5% y/y and auto sales continue to contract.

- Tourism has been a bright spot though with arrivals rising 12.2% y/y in August up from 10.8% y/y.

- Merchandise import growth has been weak falling 6.6% y/y in August signalling soft domestic demand growth.

- On the production side, the September S&P Global manufacturing PMI deteriorated to 50.4 from 51.5 but the Q3 average was still over 3 points above Q2 but below ASEAN’s level. The fall in production didn’t prevent an increase in hiring and confidence improved to its highest in four months.

- The PMI showed contracting overseas orders for the second month in Q3. Merchandise export growth held up in the 3-months to August though but given the frontloading of shipments to the US in the year to July, it is likely to moderate. Exports have remained strong to EM Asia but have slowed to the OECD.

Indonesia goods exports vs imports y/y% 3-mth ma

Source: MNI - Market News/LSEG

MALAYSIA: CPI Up to Target for First Time Since January

- Malaysia has seen moderating inflation for most of this year, causing the Central Bank to reduce inflation forecast ranges.

- Today's September result of +1.5% is the first time CPI YoY has printed in line with the bottom end of the new range since the beginning of the year.

- Moderating deflation is a thematic throughout the region, one that sees forecasters calling for rate cuts.

- However with last week's 3Q surprising to the upside at +5.2%, we see limited likelihood of a rate cut from the BNM this year.

- Bonds think so seemingly with the 10-Yr +5bps today at 3.51%.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 22/10/2025 | 0600/0700 | *** | Consumer inflation report | |

| 22/10/2025 | 0600/0700 | *** | Producer Prices | |

| 22/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 22/10/2025 | 1100/1300 | ECB de Guindos at Barcelona Real Assets Meeting | ||

| 22/10/2025 | 1225/1425 | ECB Lagarde Keynote at Frankfurt Finance & Future Summit | ||

| 22/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 22/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 22/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 22/10/2025 | 2000/1600 | Fed Governor Michael Barr | ||

| 23/10/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 23/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/10/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/10/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 23/10/2025 | - | ECB Lagarde at Euro Summit in Brussels | ||

| 23/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 23/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1330/1530 | ECB Lane Award Acceptance Speech |