OIL: Report US-India Deal Close Drives Oil Higher, EIA US Stock Data Out Later

Oil has found support today from data showing a US inventory drawdown and news that the US and India are close to a deal to gradually reduce India’s Russian oil imports and US tariffs. Less Indian consumption of Russian crude would increase its demand for other sources boosting prices. WTI is up 1.7% to $58.23/bbl following a high of $58.38, remaining below the 50-day EMA at $61.76. Brent is 1.5% higher at $62.26/bbl after reaching $62.47 (50-day EMA $65.35).

- A US-India trade deal is apparently close to completion which would allow the current 50% US duties to be reduced to around 15%, according to Bloomberg citing Mint. US President Trump has said recently that Indian PM Modi had agreed to ending imports of Russian oil. Mint is saying that the agreement could be announced at the 26-28 October ASEAN meeting.

- Oil has also found support from Tuesday’s announcement that a million barrels with delivery in December and January will be purchased for the US’ SPR, which reached a low in July 2023 and was only 17% higher last week.

- After rising the previous week, Bloomberg reported US oil inventories fell 3mn barrels last week, according to people familiar with the API data. Product stocks were also lower with gasoline down 0.2k and distillate 1mn. The official EIA data is out Wednesday.

- Later UK September CPI data print and ECB President Lagarde and Board members Buch and de Guindos speak.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Asia Wrap - AUD/USD Consolidates Around 0.6600, AM's Reduce Shorts

The AUD/USD has had a range of 0.6581 - 0.6604 in the Asia- Pac session, it is currently trading around 0.6595, +0.02%. US stocks initially tried lower on the H-1B visa story but have failed to follow through in our session. The USD retracement continues to grind higher, time will tell how long the reprieve lasts. The AUD/USD should still see dips supported for now with the first buy-zone back towards the 0.6550 area.

- MNI - In today's testimony to the House of Representatives Standing Committee on Economics, RBA Governor Bullock stated that the RBA expects recent interest rate cuts to support household and business spending. Labour market conditions are near full employment, though unemployment has risen slightly since the last meeting, with some tightness remaining. Household consumption growth is expected to continue as real incomes rise. Since the August meeting, domestic data have been broadly in line with or slightly stronger than expectations. The overall economic outlook remains clouded by uncertainty.

- "BULLOCK: RBA GETTING CLOSER TO MISSION ACCOMPLISHED ON CPI, RECENT CHINESE ECONOMIC DATA HAVE NOT BEEN SO GREAT - [RTRS]"

- "RBA'S HUNTER: LOOKS LIKE ECONOMY IS IN A `CYCLICAL UPTURN” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6510(AUD356m), 0.6525(AUD705m), 0.6600(AUD546m). Upcoming Close Strikes : 0.6600(AUD703m Sept 24), 0.6650(AUD908m Sept 23), 0.6720(AUD791m Sept 24) - BBG

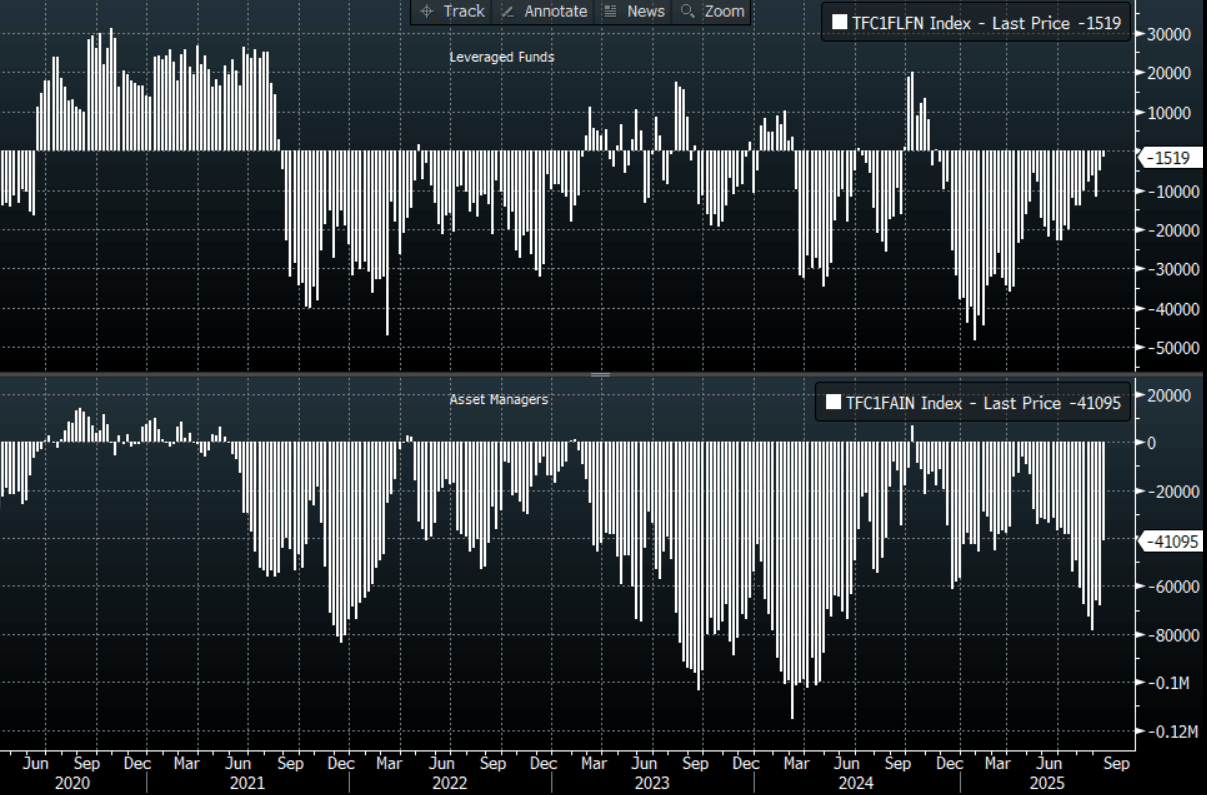

- CFTC Data last week shows Asset managers started to significantly reduce their shorts, -41095(Last -68333). The Leveraged community has pulled back their shorts to be almost flat, -1519(Last -5081).

- AUD/JPY - Asia-Pac range 97.48 - 97.85, Asia is trading around 97.85.The pair has stalled towards 98.50, dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

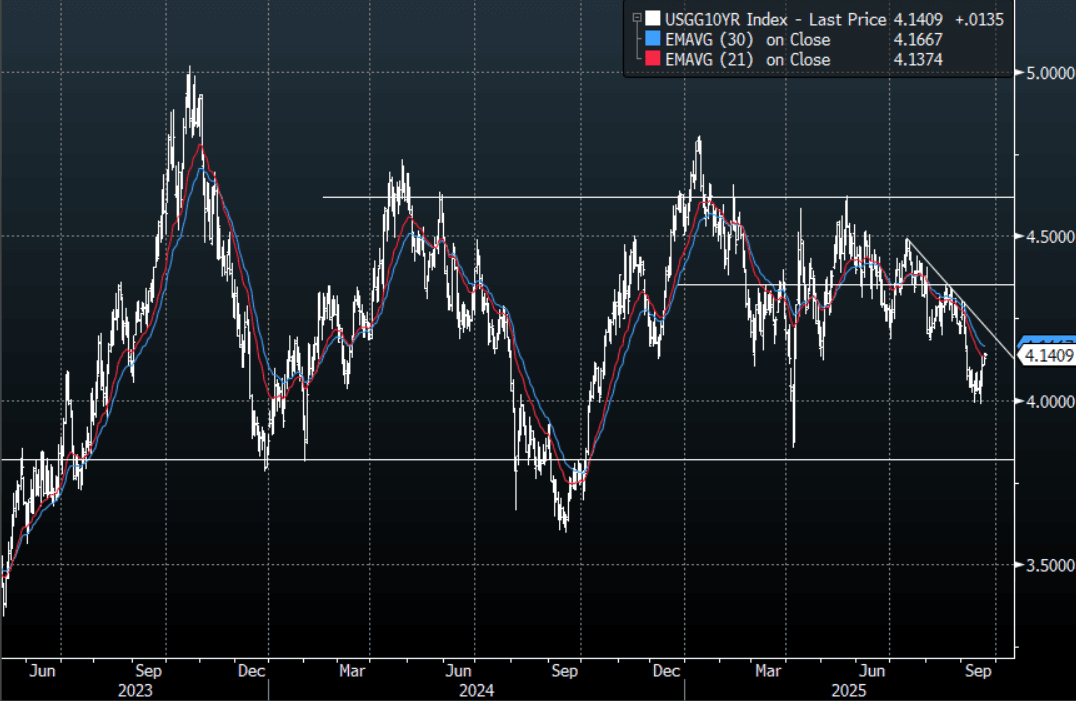

US TSYS: Asia Wrap - Yields Continue To Retrace Higher

The TYZ5 range has been 112-22 to 112-27+ during the Asia-Pacific session. It last changed hands at 112-23, down 0-01 from the previous close.

- The US 2-year yield has edged higher trading 3.578%, up 0.01 from its close.

- The US 10-year yield is trading around 4.141%, up 0.01 from its close.

- 10-Year Yields could not extend below 4.00% and have bounced as the Fed could not meet the markets very dovish expectations. The first buy-zone is now back towards the 4.20% area where I suspect demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- Robin Brooks on X: “Germany's real 10-year yield crossed above 1% this month, the first time it's been here since 2011. This is a destabilizing force for the Euro zone, because it pushes up yields everywhere else, including for highly indebted countries. It's already impacting Spain and France...”

- ISABELNET on X: “LEI - A 0.5% decline in the US Leading Economic Index (LEI) in August 2025 indicates an ongoing slowdown in US economic activity.”

- (Bloomberg) -- Asset-manager net long position in long-bond futures was unwound at a rapid pace in the week to Sept. 16., CFTC data shows. Other bigger positioning shifts saw hedge funds cover shorts in 5-year note futures while asset managers extended net long in ultra-long bond futures.

- Data/Events: Chicago Fed Nat Activity Index

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

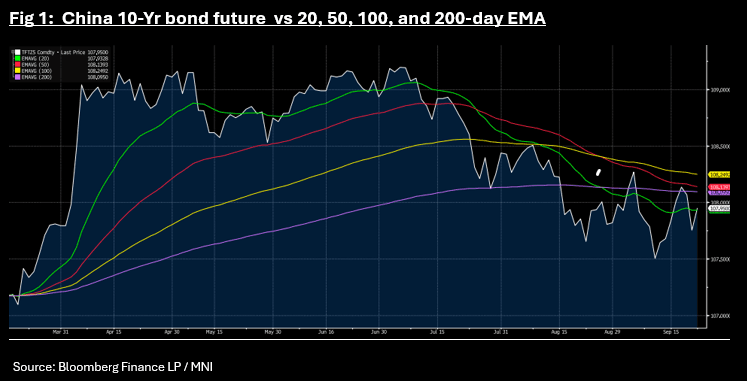

CHINA: Bond Futures Rally in Morning Trade

- Following the daily 7-day OMO, a CNY300bn 140-day reverse repo was issued this morning.

- The 10-Yr bond future is up +0.195 at 107.95, its biggest jump since August whilst the 10-Yr CGB is down at 1.79%.

- The gains push the 10-Yr above the 20-day EMA of 107.93.