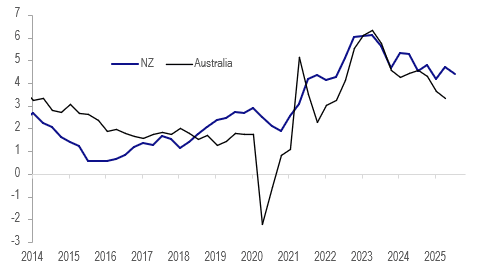

AUSTRALIA: NZ CPI Data Suggests Stable Q3 Australian Core

Q3 NZ CPI was released this week and given high correlations it has some information for Australia’s CPI out on 29 October. The RBNZ’s sector factor model measure of core was stable at 2.7% y/y in Q3 signalling that Australia’s may also remain around Q2’s 2.7%, which is consistent with monthly data. NZ’s domestic-related non-tradeables and services annual inflation moderated while goods and tradeables were higher.

Australia vs NZ underlying CPI y/y%

- NZ services inflation moderated to 4.4% y/y in Q3 from 4.7% while it picked up to 1.2% q/q from 1.1%. There is around an 85% correlation with Australia’s headline annual services inflation and 50% with the quarterly rate. Even if there is an increase in Australia’s quarterly rate in Q3 from Q2’s 0.7%, the 3.3% annual rate should moderate given it rose 1.1% q/q in Q3 2024.

- NZ’s services inflation has been running well ahead of Australia’s and has seen little disinflation since the start of 2024, which may be warning.

- It is worth noting though that the RBA focuses on market services (ex volatile items) which rose 0.6% q/q & 2.9% y/y in Q2. Governor Bullock has stated that the RBA was concerned about some of the components and sticky services prices overseas.

- NZ non-tradeables moderated 0.2pp to 3.5% y/y in Q3 and Australia’s could also ease given the correlation is over 90%. The two have been trending lower for around 2 years.

- NZ goods and tradeables inflation picked up in Q3, which given the global nature of many and high correlations Australia could see this too.

- Australia’s headline CPI continues to be impacted by temporary government electricity rebates and so it is currently not helpful to look at the relationship with NZ.

Australia vs NZ services CPI y/y%

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: BBDXY - Grinds Back Toward 1200

The BBDXY range Friday night was 1196.37 - 1200.34, Asia is currently trading around 1199, +0.05%. The USD continues to grind out gains as the market is being forced to recalibrate, having gone into last week's FOMC a little over its skis in terms of positioning. How far can this market retrace, I suspect sellers would be all over a bounce back toward the 1200/1210 area initially. A break below 1180 has been put off for now, but it feels like it's just a question of time before we have another look down there.

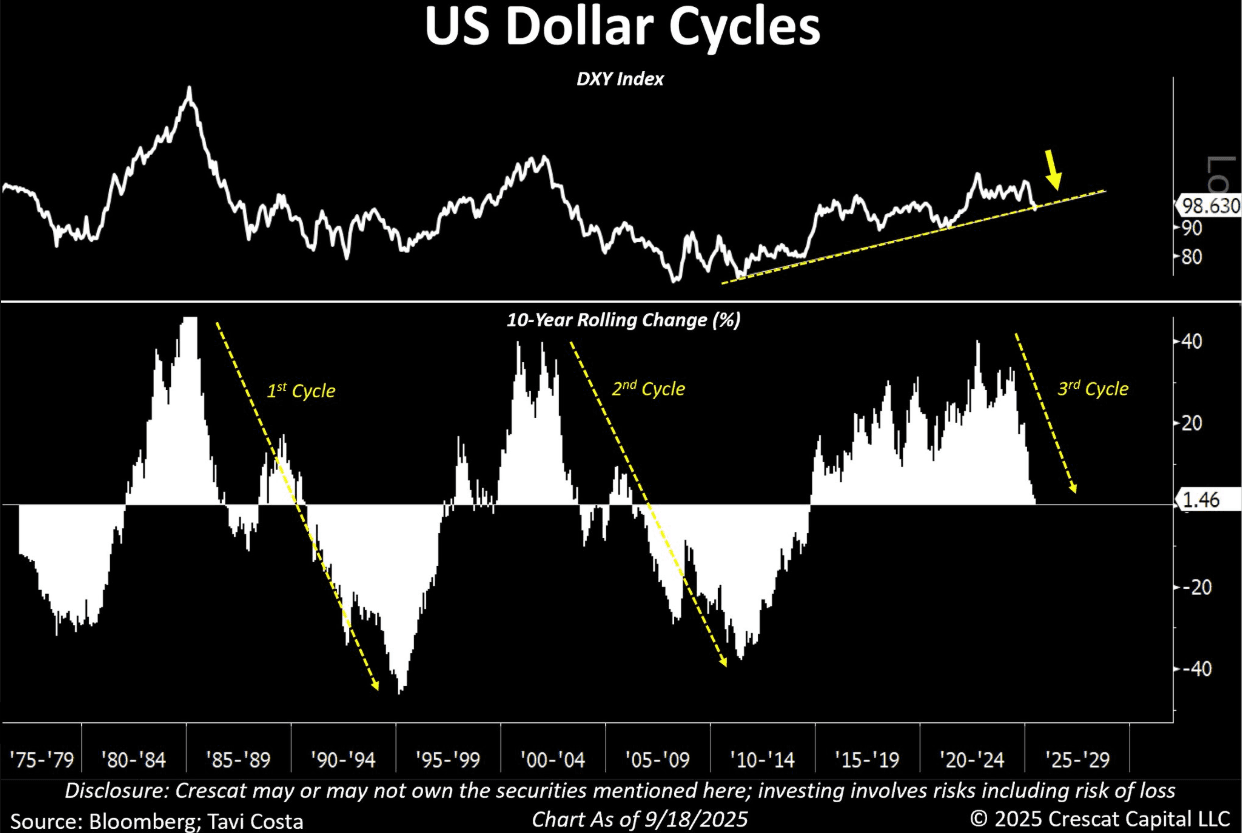

- Otavio Costa on X: “When you consider that the Fed’s preferred inflation gauge is not only near 3% but also inflecting higher, this rate cut was more than a policy change — it was a statement. This is no longer monetary policy; it’s fiscal necessity. The Fed’s latest, unspoken mandate is to ease the government’s debt burden. ”

- “The real story here is the US dollar: As weak as it appears, the DXY is sitting on a 14-year support level that, in my view, looks ready to break. The dollar anchors global assets, and on a 10-year rolling basis it’s arguably already broken down. That’s likely the beginning of a secular trend.”

- “My 2 cents: Expect EM equities, EM debt, and gold miners — all leveraged dollar-bear trades — to keep drawing capital, in my view.” See Graph Below.

- (Bloomberg) -- Bank of America Corp. is sticking with a positive view on emerging-market local markets following this week’s Fed meeting, arguing that carry trades in the developing world remain the best option for investors that want to sell the US dollar but struggle to find G10 alternatives to buy.

Fig 1: US Dollar Cycle

Source: MNI - Market News/@TaviCosta/Bloomberg

MNI: CHINA PBOC CONDUCTS CNY240.5 BLN VIA 7-DAY REVERSE REPO MON

- CHINA PBOC CONDUCTS CNY240.5 BLN VIA 7-DAY REVERSE REPO MON

- CHINA PBOC CONDUCTS CNY300 BLN VIA 14-DAY REVERSE REPO MON

CHINA SETS YUAN CENTRAL PARITY AT 7.1106 MON VS 7.1128

- CHINA SETS YUAN CENTRAL PARITY AT 7.1106 MON VS 7.1128