INDONESIA: Softer Activity Data Consistent With Another BI Rate Cut

Bank Indonesia (BI) is expected to cut rates for the fourth consecutive month at its decision today bringing them to 4.5%. Of the 39 analysts on Bloomberg 29 are forecasting another easing. BI seems to have become pro-growth in support of government efforts to boost the economy and away from its recent focus on FX stability. Lacklustre activity data since the 17 September decision backs another cut.

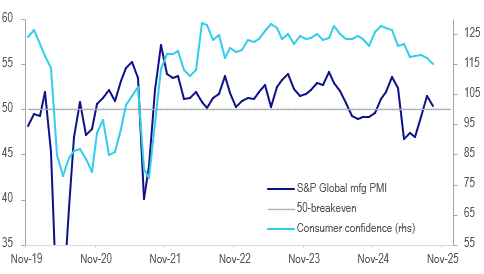

Indonesia activity outlook

Source: MNI - Market News/Bloomberg Finance L.P./LSEG

- In September BI noted that “economic growth in Indonesia must be increased in line with economic capacity” suggesting that it believes there is a negative output gap.

- It observed that Q3 consumption is “restrained” given lower sentiment driven by a weaker labour market. Q3 average consumer confidence was 1.8% below Q2 signalling that real consumption slowed in the quarter. Retail sales growth in August moderated to 3.5% y/y and auto sales continue to contract.

- Tourism has been a bright spot though with arrivals rising 12.2% y/y in August up from 10.8% y/y.

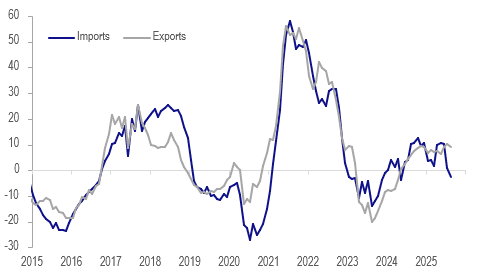

- Merchandise import growth has been weak falling 6.6% y/y in August signalling soft domestic demand growth.

- On the production side, the September S&P Global manufacturing PMI deteriorated to 50.4 from 51.5 but the Q3 average was still over 3 points above Q2 but below ASEAN’s level. The fall in production didn’t prevent an increase in hiring and confidence improved to its highest in four months.

- The PMI showed contracting overseas orders for the second month in Q3. Merchandise export growth held up in the 3-months to August though but given the frontloading of shipments to the US in the year to July, it is likely to moderate. Exports have remained strong to EM Asia but have slowed to the OECD.

Indonesia goods exports vs imports y/y% 3-mth ma

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures At Lows At Lunch

At the Tokyo lunch break, JGB futures are weaker and at session lows, -12 compared to the settlement levels.

- See the full MNI BoJ Review here.

- The BOJ kept rates at 0.5%, but two members dissented in favour of a 25bp hike, arguing the price target is “more or less achieved” and rates should move “closer to neutral,” highlighting stronger hawkish voices within the board.

- Ueda remained balanced, noting “underlying inflation is approaching 2%, but the 2% level has not yet been reached” and that there is “little sign of tariff having impact on Japan’s economy,” while emphasising ongoing global uncertainty and data dependency.

- Views diverge—some expect a hike in October following the Tankan Survey and LDP leadership election, while others see January 2026 as the base case. Political risks (e.g., dovish LDP candidates) and Fed-driven yen appreciation could delay tightening.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after Friday’s modest sell-off.

- Cash JGBs are slightly weaker across benchmarks, led by the futures-linked 7-year (+2.3bps). The benchmark 10-year yield is 0.6bp higher at 1.651% versus the cycle high of 1.653% set on Friday.

- Swap rates are 1-2bps higher. Swap spreads are mostly wider.

STIR: BOJ-Dated OIS Firmer Than Pre-MPM Levels

Markets had been positioned for a cautious, wait-and-see approach from the BoJ at this meeting.

- Nevertheless, at the time of writing, BOJ-dated OIS pricing was ~5bps firmer across meetings versus Friday’s pre-MPM levels.

- Moreover, post-MPM moves leave 2026 meetings 4-15bps firmer than early August levels.

- Current OIS pricing implies just a 50% probability of a 25bp hike in October, rising to 62% by November and 86% by December.

Figure 1: BOJ-Dated OIS – Today Vs. August 1, 2025

Source: Bloomberg Finance LP / MNI

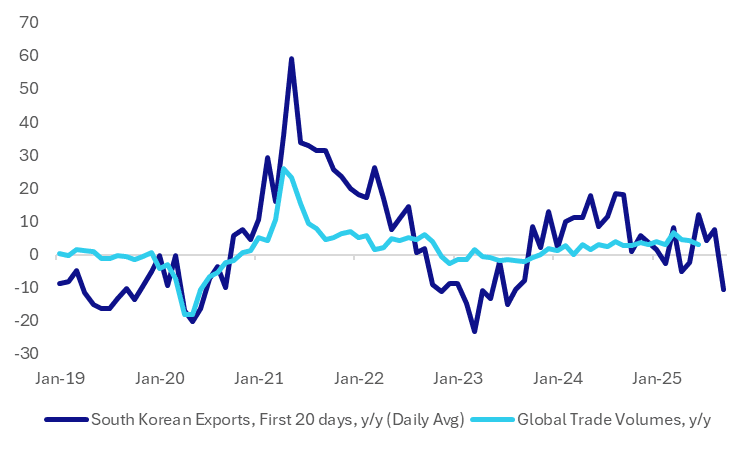

MACRO UPDATE: South Korea Exports Give Warning Sign For Global Trade

The earlier first 20-days of September trade data for South Korea flashed a warning sign for global trade growth (albeit with caveats on the data). The chart below plots the daily average of the first 20-days export growth in y/y terms against global trade volumes, also in y/y terms.

- The daily average which takes into account differences in working days between years, fell to -10.6%y/y in Sep, the weakest print since late 2023. The last time we were this soft global trade volumes was also in negative territory.

- Arguably the result may not surprise the market too much, given higher tariff levels are expected to weigh on trade growth as we progress towards the end of 2025.

- Also via BBG: "Monday’s trade data show a larger-than-usual gap between seasonally adjusted and unadjusted figures because of the shifting Chuseok holidays... The real question is how much momentum can be sustained after the Chuseok holidays.”

- The headline figure was much stronger at +13.5%y/y for the first 20-days of Sep.

- This will be a watch point for the local authorities, given President Lee is keenly focused on boosting growth. More broadly, given South Korea's key role in global supply chains, the data will be watched for signs of broader trends in the global trade outlook.

Fig 1: South Korea First 20-days Exports Y/Y (Daily Average) and Global Trade Volumes Y/Y

Source: Bloomberg Finance L.P./MNI