ASIA STOCKS: Stocks Pull Back On AI-Related Profit Taking

Bellwether tech stocks declined over 1% today in Asia as a lackluster forecast from Texas Instruments saw it's stock fall, and others follow. After many of the key tech stocks in Asia hitting new highs recently, it is unsurprising to see falls as profit takers step in. Demand remains robust and export data from countries like Korea and Taiwan show that export growth remains strong, suggesting that whilst the outlook remains strong, a re-rating in expectations can occur.

- Major Asian bourses have hit new highs over the last week and have followed each other lower today, with the NIKKEI leading the falls. The NIKKEI is down -0.60% after hitting new highs yesterday as investors seek to understand the outcome of political negotiations to form a new government.

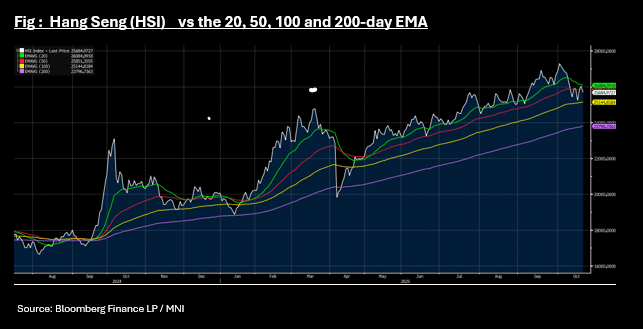

- China's major bourses are down also with the Hang Seng falling -1.3% and back below the 50-day EMA it trended above only yesterday. Other onshore bourses are down with the CSI 300 has pulled back -0.705 and near to the 20-day EMA again, whilst Shanghai and Shenzhen are down -0.45% and -0.55% respectively.

- The KOSPI is an outlier today, reaching yet another new high of 3,835 to be up +0.29%.

- Ahead of the BI decision later, the JCI is down -0.6% as markets await what appears to be an imminent rate cut.

- Headlines have crossed from Indian news source Mint, that a US-India trade deal will soon see tariff rates fall sharply. Some key quotes are outlined below, but notably the article states tariff rates may come down form 50% to 15-16%. Market optimism around a trade deal has been growing, given recent Trump remarks that India would curb Russian oil imports. The NIFTY 50 has reached a new high of 25,866, up +0.10% in morning trade.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

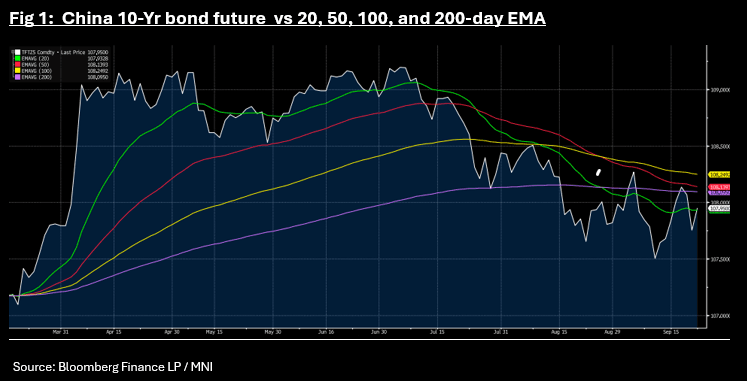

CHINA: Bond Futures Rally in Morning Trade

- Following the daily 7-day OMO, a CNY300bn 140-day reverse repo was issued this morning.

- The 10-Yr bond future is up +0.195 at 107.95, its biggest jump since August whilst the 10-Yr CGB is down at 1.79%.

- The gains push the 10-Yr above the 20-day EMA of 107.93.

JGBS: Futures At Lows At Lunch

At the Tokyo lunch break, JGB futures are weaker and at session lows, -12 compared to the settlement levels.

- See the full MNI BoJ Review here.

- The BOJ kept rates at 0.5%, but two members dissented in favour of a 25bp hike, arguing the price target is “more or less achieved” and rates should move “closer to neutral,” highlighting stronger hawkish voices within the board.

- Ueda remained balanced, noting “underlying inflation is approaching 2%, but the 2% level has not yet been reached” and that there is “little sign of tariff having impact on Japan’s economy,” while emphasising ongoing global uncertainty and data dependency.

- Views diverge—some expect a hike in October following the Tankan Survey and LDP leadership election, while others see January 2026 as the base case. Political risks (e.g., dovish LDP candidates) and Fed-driven yen appreciation could delay tightening.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after Friday’s modest sell-off.

- Cash JGBs are slightly weaker across benchmarks, led by the futures-linked 7-year (+2.3bps). The benchmark 10-year yield is 0.6bp higher at 1.651% versus the cycle high of 1.653% set on Friday.

- Swap rates are 1-2bps higher. Swap spreads are mostly wider.

STIR: BOJ-Dated OIS Firmer Than Pre-MPM Levels

Markets had been positioned for a cautious, wait-and-see approach from the BoJ at this meeting.

- Nevertheless, at the time of writing, BOJ-dated OIS pricing was ~5bps firmer across meetings versus Friday’s pre-MPM levels.

- Moreover, post-MPM moves leave 2026 meetings 4-15bps firmer than early August levels.

- Current OIS pricing implies just a 50% probability of a 25bp hike in October, rising to 62% by November and 86% by December.

Figure 1: BOJ-Dated OIS – Today Vs. August 1, 2025

Source: Bloomberg Finance LP / MNI