US TSYS: Modest Declines in Yields Again Today

Oct-22 04:15

Bond futures finished -01 lower today for TYZ5 on low volumes, looking for a catalyst for the next move .

- The US 2-Yr did very little all morning before rising modestly to 3.465 in the afternoon trading session.

- The US 5-Yr ground was flat at 3.56%

- The 10-Yr has consolidated below 4.00%, rallying again modestly by -0.5bps to reach 3.96% in line with October 24 yield levels.

- The 30-Yr continues to outperform rallying -0.5bps overnight to reach 4.53%. Likely next inflection point could be the April lows of 4.40%.

- Yield moves are appearing disjointed relative to current interest rate pricing as the government shutdown continues as bond traders agonize over the potential impact on the economy. New ranges are being defined and as markets await the release of the September CPI, markets appeared skewed towards lower yields for now.

- There is limited Tier 1 data releases for markets to follow tonight, only MBG mortgage applications. Equity weakness in Asia will be watched for any follow through particularly as many bourses reach new highs.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Yields Continue To Retrace Higher

Sep-22 04:12

The TYZ5 range has been 112-22 to 112-27+ during the Asia-Pacific session. It last changed hands at 112-23, down 0-01 from the previous close.

- The US 2-year yield has edged higher trading 3.578%, up 0.01 from its close.

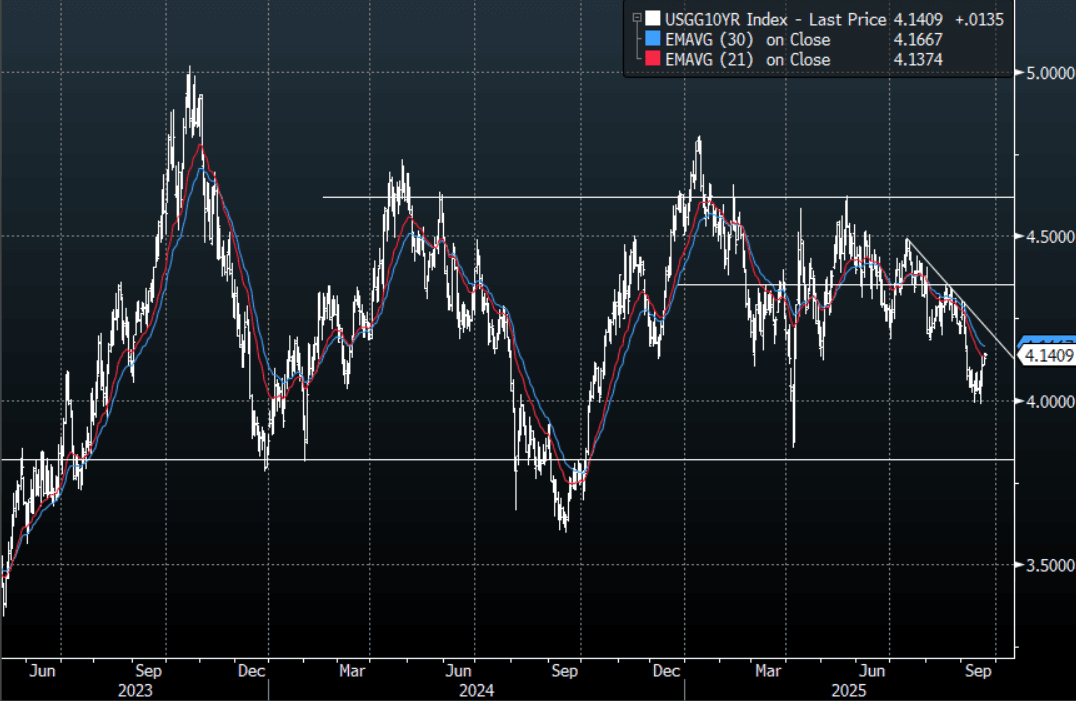

- The US 10-year yield is trading around 4.141%, up 0.01 from its close.

- 10-Year Yields could not extend below 4.00% and have bounced as the Fed could not meet the markets very dovish expectations. The first buy-zone is now back towards the 4.20% area where I suspect demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- Robin Brooks on X: “Germany's real 10-year yield crossed above 1% this month, the first time it's been here since 2011. This is a destabilizing force for the Euro zone, because it pushes up yields everywhere else, including for highly indebted countries. It's already impacting Spain and France...”

- ISABELNET on X: “LEI - A 0.5% decline in the US Leading Economic Index (LEI) in August 2025 indicates an ongoing slowdown in US economic activity.”

- (Bloomberg) -- Asset-manager net long position in long-bond futures was unwound at a rapid pace in the week to Sept. 16., CFTC data shows. Other bigger positioning shifts saw hedge funds cover shorts in 5-year note futures while asset managers extended net long in ultra-long bond futures.

- Data/Events: Chicago Fed Nat Activity Index

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

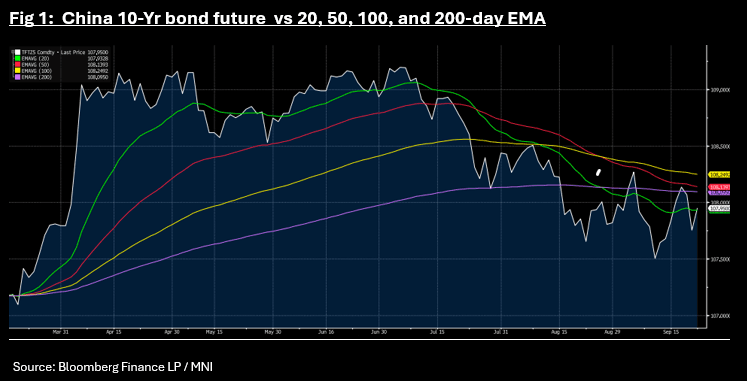

CHINA: Bond Futures Rally in Morning Trade

Sep-22 04:00

- Following the daily 7-day OMO, a CNY300bn 140-day reverse repo was issued this morning.

- The 10-Yr bond future is up +0.195 at 107.95, its biggest jump since August whilst the 10-Yr CGB is down at 1.79%.

- The gains push the 10-Yr above the 20-day EMA of 107.93.

JGBS: Futures At Lows At Lunch

Sep-22 03:09

At the Tokyo lunch break, JGB futures are weaker and at session lows, -12 compared to the settlement levels.

- See the full MNI BoJ Review here.

- The BOJ kept rates at 0.5%, but two members dissented in favour of a 25bp hike, arguing the price target is “more or less achieved” and rates should move “closer to neutral,” highlighting stronger hawkish voices within the board.

- Ueda remained balanced, noting “underlying inflation is approaching 2%, but the 2% level has not yet been reached” and that there is “little sign of tariff having impact on Japan’s economy,” while emphasising ongoing global uncertainty and data dependency.

- Views diverge—some expect a hike in October following the Tankan Survey and LDP leadership election, while others see January 2026 as the base case. Political risks (e.g., dovish LDP candidates) and Fed-driven yen appreciation could delay tightening.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after Friday’s modest sell-off.

- Cash JGBs are slightly weaker across benchmarks, led by the futures-linked 7-year (+2.3bps). The benchmark 10-year yield is 0.6bp higher at 1.651% versus the cycle high of 1.653% set on Friday.

- Swap rates are 1-2bps higher. Swap spreads are mostly wider.

Trending Top

Apr-03 08:04

Apr-02 19:04