AUSSIE BONDS: Subdued Session, Market Scales Back Chances Of A Nov Cut

Oct-22 04:05

ACGBs (YM -0.5 & XM +1.0) are slightly mixed.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +15bps.

- The bills strip is -1 to -2 across contracts.

- A 25bp rate cut in November is assigned a 64% probability, with a cumulative 23bps of easing priced by year-end.

- Compared with previous instances in this easing cycle, the market appears less confident than usual about a November 4 cut.

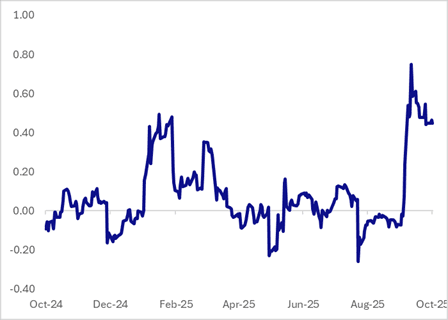

- This caution aligns with the RBA’s pattern over the past year of easing less than what six-month forward expectations had implied. Those expectations currently sit around 3.20%, compared with the cash rate of 3.60%. (see chart)

- The local data calendar remains fairly quiet throughout the week.

- Today’s auction of the Jun-35 showed solid pricing for ACGBs, with the weighted average yield coming in 0.43bps below prevailing mid-yield. However, the cover ratio nudged lower to 2.9056x from 3.2958x at the previous auction.

- The AOFM plans to sell A$800mn of the 2.75% 21 November 2029 bond on Friday.

- QTC has priced a A$2 billion increase to its 4.50% August 22, 2035 A$ fixed rate benchmark bond, according to BofA Securities. - BBG

Figure 1: RBA Cash Rate Vs. OIS 6M1M (6M Ago)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Futures Rally in Morning Trade

Sep-22 04:00

- Following the daily 7-day OMO, a CNY300bn 140-day reverse repo was issued this morning.

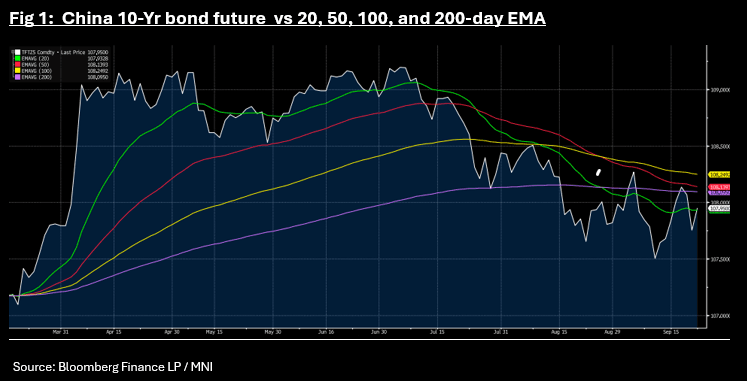

- The 10-Yr bond future is up +0.195 at 107.95, its biggest jump since August whilst the 10-Yr CGB is down at 1.79%.

- The gains push the 10-Yr above the 20-day EMA of 107.93.

JGBS: Futures At Lows At Lunch

Sep-22 03:09

At the Tokyo lunch break, JGB futures are weaker and at session lows, -12 compared to the settlement levels.

- See the full MNI BoJ Review here.

- The BOJ kept rates at 0.5%, but two members dissented in favour of a 25bp hike, arguing the price target is “more or less achieved” and rates should move “closer to neutral,” highlighting stronger hawkish voices within the board.

- Ueda remained balanced, noting “underlying inflation is approaching 2%, but the 2% level has not yet been reached” and that there is “little sign of tariff having impact on Japan’s economy,” while emphasising ongoing global uncertainty and data dependency.

- Views diverge—some expect a hike in October following the Tankan Survey and LDP leadership election, while others see January 2026 as the base case. Political risks (e.g., dovish LDP candidates) and Fed-driven yen appreciation could delay tightening.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after Friday’s modest sell-off.

- Cash JGBs are slightly weaker across benchmarks, led by the futures-linked 7-year (+2.3bps). The benchmark 10-year yield is 0.6bp higher at 1.651% versus the cycle high of 1.653% set on Friday.

- Swap rates are 1-2bps higher. Swap spreads are mostly wider.

STIR: BOJ-Dated OIS Firmer Than Pre-MPM Levels

Sep-22 02:59

Markets had been positioned for a cautious, wait-and-see approach from the BoJ at this meeting.

- Nevertheless, at the time of writing, BOJ-dated OIS pricing was ~5bps firmer across meetings versus Friday’s pre-MPM levels.

- Moreover, post-MPM moves leave 2026 meetings 4-15bps firmer than early August levels.

- Current OIS pricing implies just a 50% probability of a 25bp hike in October, rising to 62% by November and 86% by December.

Figure 1: BOJ-Dated OIS – Today Vs. August 1, 2025

Source: Bloomberg Finance LP / MNI