MNI EUROPEAN MARKETS ANALYSIS: Busy US Data Day Coming Up

- US equity futures have edged lower, while regional equity markets have mostly tracked weaker, as the global equity market rebound pauses. The USD has mostly tracked lower, with yen outperforming in the G10 space, while focus has been on KRW in the EM space. The won has risen but remains within recent ranges.

- US Tsy yields are little changed on the day. Oil is down weighed by earlier Iran headlines. Gold sentiment remains poor.

- Australian jobs growth was much stronger than forecast, but hasn't provided lasting benefit to the AUD, but local bond yields are higher.

- Later Fed Chair Powell speaks on the Framework Review and Barr also appears. In terms of data, US April retail sales, PPI, IP, May Philly Fed and jobless claims are released as well as Q1/March UK GDP, IP, trade, euro area Q1 preliminary GDP/employment and March IP. The ECB’s Cipollone, Elderson, de Guindos and BoE’s Dhingra also speak.

MARKETS

US TSYS: Asia Wrap - Quiet Session

TYM5 has traded slightly lower within a range of 109-18+ to 109-22 during the Asia-Pacific session. It last changed hands at 109-22, down 0-01 from the previous close

- The US 2-year yield has drifted lower, dealing around 4.049%, unchanged from its close.

- The US 10-year yield has drifted lower, dealing around 4.53%, down 0.01 from its close.

- (Bloomberg) -- “Taiwan’s Ministry of Finance said its reviews of US Treasury positions at state-backed banks and their internal risk-management measures have so far found no major issues.”

- “Fedspeak: Mary Daly said the economy’s strength allows policymakers to be patient. Philip Jefferson said tariffs and related uncertainty may slow growth and boost inflation but monetary policy is well positioned to respond.’(BBG)

- The 10-year Yield has broken above the 4.50% resistance. A sustained break above this level could see another round of selling targeting the 4.75% area. Support now seen back towards 4.35/40 where supply should now be seen.

- Data/Events : Retail Sales, PPI, Weekly Claims, Industrial Production and Capacity Utilization.

JGBS: Bear-Steepener, 30YY Hits 3.0%, Poor 5Y Auction, GDP Tomorrow

JGB futures are weaker, -31 compared to settlement levels, but sitting near of today’s Tokyo session range.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's heavy session. Today's US calendar will see a heavy round of economic data: Retail Sales, PPI, Weekly Claims, Industrial Production and Capacity Utilisation.

- Cash JGBs are flat to 9bps cheaper across benchmarks, but off the worst levels, with the steeper curve. The benchmark 5-year yield is 2.6bps higher at 1.003% after today's poorly received supply.

- Today’s 5-year JGB auction highlighted weak investor demand, with the auction price falling short of expectations at 100.07. The bid-to-cover ratio declined to 3.1894x from 3.8358x, while the tail widened slightly to 0.06 from 0.04—both pointing to a softer bid.

- Given the higher yield and steeper 2s/5s curve compared to last month, today’s outcome marks a notably weak signal.

- The cash 30-year yield is +4.8bps at 2.963% after setting a cycle high of 3.007%, the highest since late 2000.

- Swap rates are ~1bp lower out to the 20-year and flat beyond. Swap spreads are tighter.

- Tomorrow, the local calendar will see Q1 GDP (P) and IP data alongside a speech by BoJ Board Member Nakamura.

JAPAN DATA: Local Investors Buy Offshore Bonds & Equities

Japan outbound investment flows were positive in the week ending May 9, see the table below. The strongest flows were into offshore bonds, with just under ¥2trln of net purchases for this segment. This marks the third out of the last four weeks we have seen positive net flows to overseas bonds. Still, since the start of March, cumulative net flows are modestly negative. Global bond returns are down noticeably over the past week, with US Tsy yields firming and acting as a headwind to returns.

- Local investors also continued to buy overseas equities, marking the eighth straight week of net buying for this segment. Net buying was down from the prior week's heady pace.

- In terms of offshore inflows into Japan, trends were relatively muted last week. Japan markets were on holiday for the first two days of last week, which may have impacted such trends.

- Offshore inflows remained positive into local stocks for the fifth straight week.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending May 9 | Prior Week |

| Foreign Buying Japan Stocks | 439.0 | 968 |

| Foreign Buying Japan Bonds | -141.1 | -912.7 |

| Japan Buying Foreign Bonds | 1923.2 | -541.2 |

| Japan Buying Foreign Stocks | 250.8 | 2545.4 |

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Cheaper But Off Worst Levels Despite Jobs Beat

ACGBs (YM -6.0 & XM -5.5) are cheaper but notably better than Sydney session lows set following the release of stronger-than-expected employment data.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's heavy session. Today's US calendar will see a heavy round of economic data: Retail Sales, PPI, Weekly Claims, Industrial Production and Capacity Utilisation.

- Employment in April printed significantly higher than expected at +89k, but the unemployment rate remained at 4.1%.

- The April jobs data continue to show that Australia’s labour market remains tight with employment growth keeping up with the labour force over the last year. However, there are some early signs that workers would like more hours.

- Cash ACGBs are 6-7bps cheaper on the day with the AU-US 10-year yield differential at +1bps.

- The bills strip has retained its bear-steepener, with pricing -3 to -7.

- RBA-dated OIS pricing is 1-3bps firmer across meetings after the data. A 25bp rate cut in May is given an 89% probability (95% pre-data), with a cumulative 75bps (76bps pre-data) of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$800mn of the 2.50% 21 May 2030 bond.

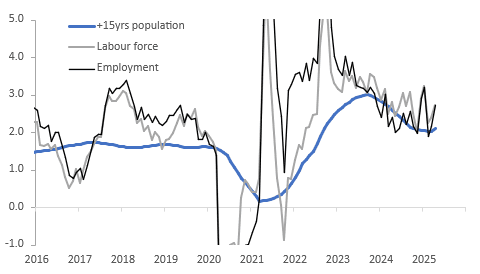

AUSTRALIA DATA: Tight Labour Market & Wages Growth To Keep RBA Tone Cautious

The April jobs data continue to show that Australia’s labour market remains tight with employment growth keeping up with the labour force over the last year and the unemployment rate remaining steady at 4.1%, only marginally higher than November’s recent low. However, there are some early signs that workers would like more hours. This week’s stronger-than-expected labour and wage data are unlikely to derail a May 20 rate cut but will probably keep the RBA cautious regarding future easing.

- Employment rose 89k in April, slightly below the 95k increase in the labour force which resulted in a 6k rise in the number of unemployed. Compared to last year jobs and the labour force both grew 2.7%, while working age population was up 2.1%. Unemployment is now 2.2% y/y higher, the slowest pace since November. The participation rate rose 0.3pp to 67.1%.

- Over the last 12 months 398.8k jobs were created averaging 32.5k/month compared to 335k and 27.9k over the previous year.

Employment vs labour force y/y%

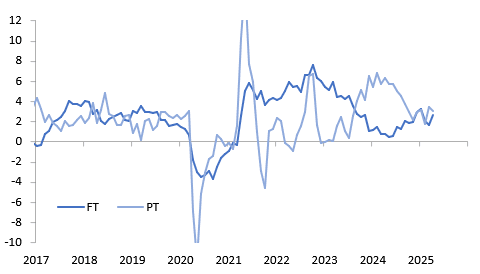

- Full-time (FT) employment recovered rising 59.5k in April, while part-time (PT) added 29.5k after 12.2k and 24.2k respectively. This saw the FT annual rate pickup to 2.6% from 1.6% while PT remained solid at 3.0% but down from March’s 3.4%.

Employment y/y%

Source: MNI - Market News/ABS

- The outperformance of the FT sector is also reflected in hours worked as they rose 0.1% m/m compared to PT falling 0.3% m/m leaving the total flat in April, despite strong jobs growth. 3-month momentum is weak though at -1.4% annualised after hours falling in both February and March and FT is down 2.2% while PT is up 2.4% but down significantly.

- Softening hours are reflected in April’s 0.15pp increase in the underemployment rate to 6.0%.

AUSTRALIA DATA: Inflation Expectations Remain Above 4% Despite Lower CPI Print

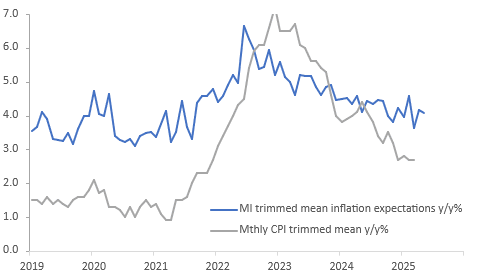

Melbourne Institute May consumer inflation expectations eased 0.1pp to 4.1%, unchanged from May 2024. It is worth noting that it didn’t fall further given the moderation in Q1 CPI released at the end of April and that petrol prices are significantly lower on a year ago and also in Q2 to date. But business price/cost components were generally higher in the April NAB business survey with retail prices jumping 1.4% 3m/3m which may be contributing to above 4% consumer inflation expectations. They have been oscillating around that level since October. Cost-of-living pressures remain households’ main concern. April CPI prints on May 28.

Australia Melbourne Institute consumer inflation expectations vs core CPI y/y%

BONDS: NZGBS: Bull-Steepener, Food Prices Highest Since Jan-24

NZGBs closed showing a bull-steepener, with benchmark yields 1-5bps lower. NZGBs outperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 7-8bps tighter versus yesterday’s close.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's heavy session.

- Today’s NZGB auction showed strong demand, especially the 5-year supply, with cover ratios of 6.00x (May-30) to 3.42x (May-41) across the lines.

- Swap rates closed flat to 2bps lower, with implied swap spreads wider.

- NZ food prices rose 0.8% m/m to be up 3.7% y/y in April, the highest since January 2024, after 0.5% m/m and 3.5% y/y. The increase was driven by higher grocery and non-alcoholic beverage prices. Other categories were also released for April, including electricity for the first time, accounting for 46.5% of the CPI basket. Electricity and gas prices are now included in the monthly releases.

- While April prices were mixed, activity remains soft, and so another 25bp rate cut remains likely on May 28.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for May, with a cumulative 68bps by November 2025.

- Tomorrow, the local calendar will see BusinessNZ Manufacturing PMI, RBNZ Inflation Expectations and Non-Resident Bond Holdings.

NEW ZEALAND: Power Prices Added To Monthly Series, Mixed Components In April

NZ food prices rose 0.8% m/m to be up 3.7% y/y in April, the highest since January 2024, after 0.5% m/m and 3.5% y/y. The increase was driven by higher grocery and non-alcoholic beverage prices. Other categories were also released for April, including electricity for the first time, accounting for 46.5% of the CPI basket. While April prices were mixed, activity remains soft, and so another 25bp rate cut remains likely on May 28.

- Grocery prices rose 1.2% m/m and 5.2% y/y in April, while fruit & veg increased only 0.3% m/m & 0.2% y/y and meat fell 0.4% m/m to be up 3.6% y/y. Restaurant prices increased 0.5% m/m to be only 2.0% y/y higher.

- Existing rent increases were subdued rising 0.2% m/m to be up 3.0% y/y down from 3.3% y/y. This is a significant component of the CPI and the lowest annual rate in four years.

- Electricity and gas prices are now included in the monthly releases. Electricity rose 2.3% m/m & 6.2% y/y, down from 7.0% y/y, and gas 1.1% m/m & 15.8% y/y up from 14.6%, the highest since the series began in 2012.

- There was a sharp drop in alcohol prices of 1.5% m/m &-0.2% y/y, the lowest since April 2017. Petrol also fell 1.5% m/m to be down 9.2% y/y after 2.1% m/m & -6.2% y/y in March as global oil prices declined.

- Air travel rose sharply especially for overseas +24.7 m/m & +10.7% y/y while domestic was up 3.8% m/m & 10.6% y/y. Domestic and overseas accommodation fell on the month but the annual rates diverged with the former at -8.1% y/y but the latter +9.1% y/y.

NZ CPI y/y%

Source: MNI - Market News/Statistics NZ/LSEG

The BBDXY has had a range of 1229.14 - 1232.16 in the Asia-Pac session, it is currently trading around 1230. “Vladimir Putin appointed low-level officials for Ukraine talks in Turkey, dashing Volodymyr Zelenskiy’s hopes to speak to him directly. Donald Trump downplayed the chances of joining the gathering, but said Marco Rubio will go to Istanbul”(BBG).”Oil dropped after NBC reported Iran is willing to forgo nuclear weapons in exchange for relief from US sanctions”(BBG).”Foreign investment in Europe fell to a nine-year low in 2024, underscoring the region’s struggle to lure business even before Trump’s trade war darkened the outlook”(BBG).

- EUR/USD - Asian range 1.1173 - 1.1201, Asia is currently trading 1.1195. EUR/USD has had a quiet session as the market consolidates. The market is still expected to use dips as a buying opportunity, dips back towards 1.09/1.10 should be well supported.

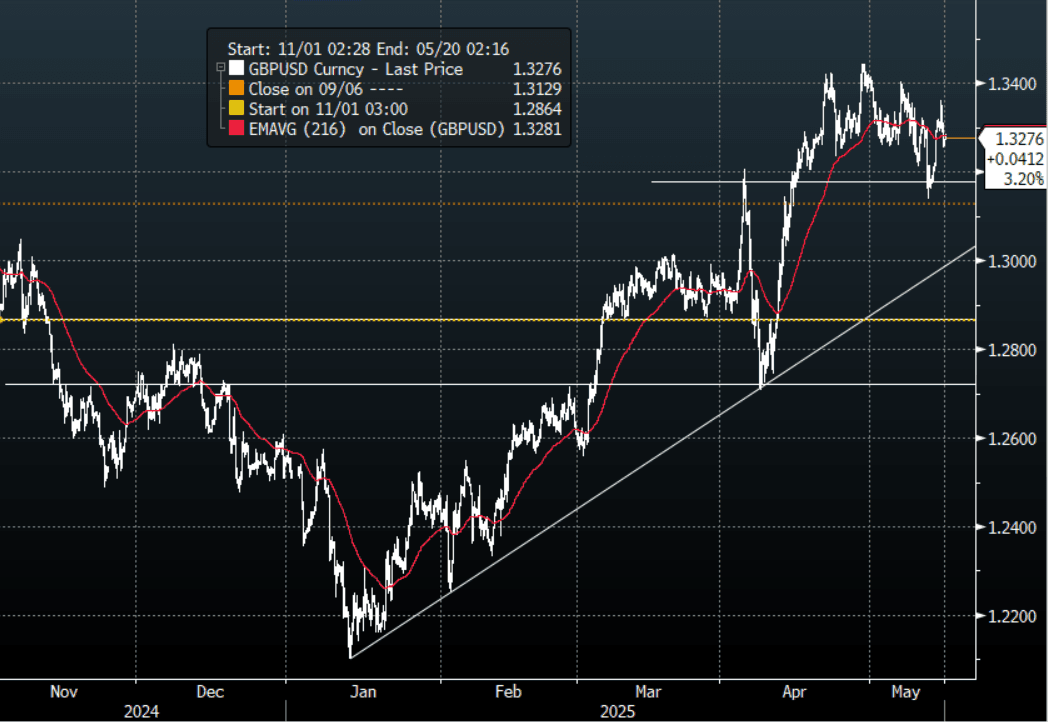

- GBP/USD - Asian range 1.3259 - 1.3287, Asia is currently dealing around 1.3280. Decent demand for GBP emerged sub 1.3200 , it has since bounced back to the middle of its recent range of 1.3150 - 1.3450.

- USD/CNH - Asian range 7.2056 - 7.2157, the USD/CNY fix printed 7.1963. Asia is currently dealing around 7.2095. Sellers should be found on a bounce back towards 7.24/25 again.

- Cross asset : SPX -0.19%, Gold $3150, US 10-Year 4.53%, BBDXY 1230, Crude oil $61.75

Data/Events : Retail Sales, PPI, Weekly Claims, Industrial Production and Capacity Utilization

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

JPY: USD/JPY Asian Wrap - Drifts Lower

The Asia- Pac range has been 145.96 - 146.75, Asia is currently trading around 146.05. USD/JPY has drifted lower for most of our session as the move higher in risk continues to run out of steam.

- Today’s 5-year JGB auction highlighted weak investor demand, with the auction price falling short of expectations at 100.07. The bid-to-cover ratio declined to 3.1894x from 3.8358x, while the tail widened slightly to 0.06 from 0.04—both pointing to a softer bid.

- “It looks as though investors are holding back for a 1% yield, which wasn’t reached today even though secondary yields did touch that level earlier this week. All of which show the upcoming 20- and 40-year auctions this month will be tough to complete.”(BBG)

- USD/JPY is consolidating after a powerful break higher, support is now back towards 145.00. With the move higher in risk stalling the impetus has been taken out of the move higher for now.

- MNI FX OPTIONS: Expiries for May15 NY cut 1000ET (Source DTCC)USD/JPY: Y140.00($3.4bln), Y145.00($2.1bln), Y146.95-05($1.3bln)

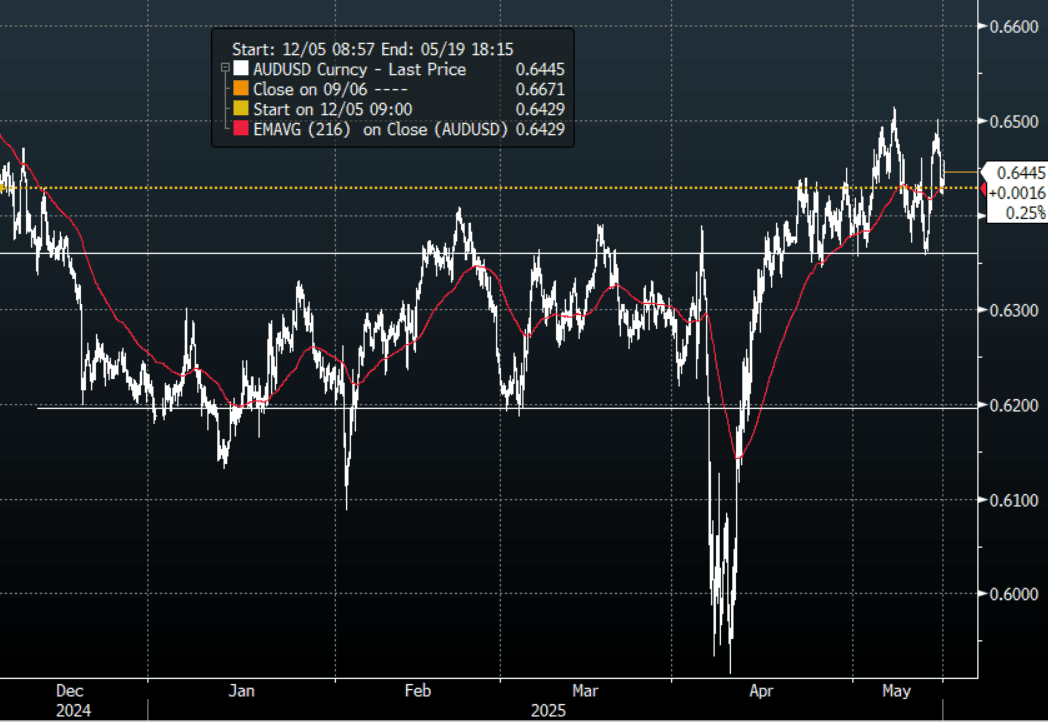

AUD/USD Wrap - Bounces On Higher April Employment

MNI AU - Employment in April printed significantly higher than expected at +89k but the unemployment rate remained at 4.1% as the participation rate rose to 67.1%. The strength was in both full-time and part-time jobs.

- The AUD jumped 15/20 points on the better employment data to print a high of 0.6458 on the day.

- It then drifted off from those levels for the balance of our session, we now head into the London session trading around 0.6440.

- The AUD/USD has found decent supply back towards 0.6500 and is looking to consolidate its gains on a 0.6400 handle.

- Key Support in the AUD is back towards 0.6350 a close back below here would start to challenge the newly formed uptrend. While this holds the market should find demand on dips.

MNI FX OPTIONS: Expiries for May15 NY cut 1000ET (Source DTCC) : AUD/USD: $0.6475(A$1.3bln)

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg

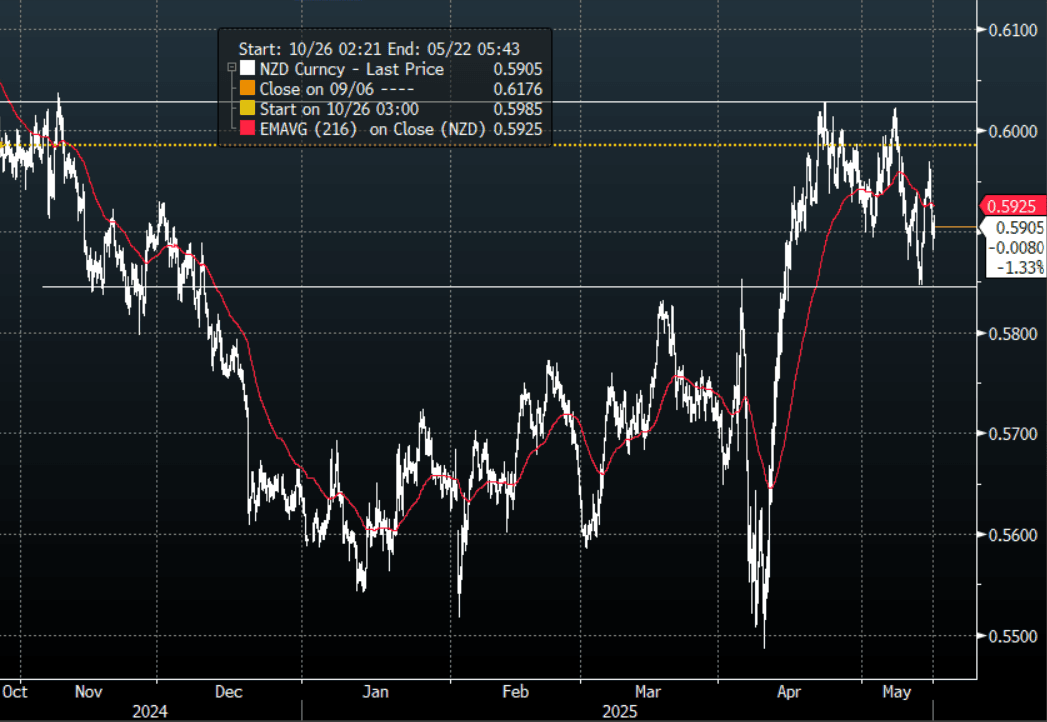

The NZD had a range in our session of 0.5881 - 0.5916, going into the London session around 0.5905. A very quiet session for risk today with the NZD trading sideways.

- The NZD up moved in sympathy with the AUD as it popped higher on a better employment print.

- AUD/NZD continues to grind higher, attempting to get a foothold above 1.0900, the better AUD data gave it a lift printing a high of 1.0922 in our session. Support is seen back towards 1.0800 and a sustained break above 1.0900 would turn the focus higher once again.

- "APEC SEES REGIONAL GDP GROWTH FOR 2025 AT 2.6% DOWN FROM 3.3% EARLIER, APEC SEES EXPORT GROWTH FOR 2025 AT 0.4% VERSUS 5.7% IN 2024” - RTRS

- The NZD now seems to be comfortable in a 0.5800/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 held very well, and while this continues to hold expect buyers to return on dips. The first target is the highs just above 0.6000, a break above here is needed to regain momentum higher.

MNI FX OPTIONS: Expiries for May15 NY cut 1000ET (Source DTCC): NZD/USD: $0.5880(N$1.0bln)

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Most Major Bourses Lower Today

Despite solid earnings from Tencent (revenue up 13% in the March quarter) China's major bourses fell today. Next to report will be Alibaba which reports after Hong Kong close today with investors looking for an update on the launch of its new video generating model.

In what felt like a day of consolidation where the trade truce euphoria ran out of steam, most major bourses across the region fell today.

- China's Hang Seng is down -0.25% today following yesterday's strong gains. The CSI 300 is down -0.60%, Shanghai down -0.40% and Shenzhen down -0.94%.

- The KOSPI is down today by -0.55% following yesterday's gains of +1.2%.

- The FTSE Bursa Malaysia KLCI Index is down -0.54% but remains higher for the week.

- The Jakarta Composite continues to rally, up +1.1% today and from the April lows is better by more than 18%.

- The FSE Straits Times in Singapore is an outlier, gaining +0.41% whilst the PSEi in the Philippines is one of the worst performers down -1.33%.

- The NIFTY 50 has given back yesterday's gains and is lower by -0.43%

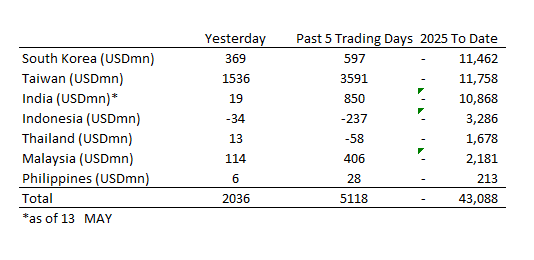

ASIA STOCKS: Outsized Inflow into Taiwan Yesterday

Taiwan has now enjoyed US$6.7bn of inflows in the last nine trading days as the TWD rallies over 5% and the TAIEX up almost 5%.

- South Korea: Recorded inflows of +$369m as of yesterday, bringing the 5-day total to +$597m. 2025 to date flows are -$11,462m. The 5-day average is +$119m, the 20-day average is +$1m and the 100-day average of -$130m.

- Taiwan: Had inflows of +$1,536m as of yesterday, with total inflows of +$3,591m over the past 5 days. YTD flows are negative at -$11,758. The 5-day average is +$718m, the 20-day average of +$330m and the 100-day average of -$138m.

- India: Had inflows of +$19m as of the 13th, with total inflows of +$850m over the past 5 days. YTD flows are negative -$10,868m. The 5-day average is +$170m, the 20-day average of +$254m and the 100-day average of -$125m.

- Indonesia: Had outflows of -$34m as of yesterday, with total outflows of -$237m over the prior five days. YTD flows are negative -$3,286m. The 5-day average is -$47m, the 20-day average -$56m and the 100-day average -$36m

- Thailand: Recorded inflows of +$13m as of yesterday, outflows totaling -$58m over the past 5 days. YTD flows are negative at -$1,678m. The 5-day average is -$12m, the 20-day average of -$14m the 100-day average of -$18m.

- Malaysia: Recorded inflows of +$114m as of yesterday, totaling +$406m over the past 5 days. YTD flows are negative at -$2,181m. The 5-day average is +$81m, the 20-day average of +$31m and the 100-day average of -$25m.

- Philippines: Saw inflows of $6m as of yesterday, with net inflows of +$28m over the past 5 days. YTD flows are negative at -$213m. The 5-day average is +$6m, the 20-day average of +$4m the 100-day average of -$3m.

OIL: Crude Down Through Today, IEA Forecasts Out Later

Oil prices took a step down at the start of today’s APAC trading after NBC reported that a top Iranian official said that the country would “commit to never making nuclear weapons” and “getting rid of its stockpiles of highly-enriched Uranium” in exchange for reduced sanctions. It has continued trending down through the session to be over 2% lower on the day.

- WTI is down 2.3% to $61.68/bbl off the intraday low of $61.36 but remains around 6% higher in May helped by hopes of a US-China trade deal which would improve the demand outlook. Brent is 2.3% lower at $64.60/bbl after falling to $64.32. Both benchmarks remain in a downtrend but well off initial support. The USD index is down 0.2% but unable to provide assistance to crude.

- CCIC Singapore has been sanctioned for inspecting Iranian crude shipments destined for China but not reporting them, as reported by Bloomberg. It signals that sanction-breaking shipments are being increasingly scrutinised as US President Trump has sounded tougher on Iran.

- The IEA’s April report is published later today. Its forecasts for the market tend to be less optimistic than OPEC’s and so it is likely to be watched closely.

- Later Fed Chair Powell speaks on the Framework Review and Barr also appears. In terms of data, US April retail sales, PPI, IP, May Philly Fed and jobless claims are released as well as Q1/March UK GDP, IP, trade, euro area Q1 preliminary GDP/employment and March IP. The ECB’s Cipollone, Elderson, de Guindos and BoE’s Dhingra also speak.

- Gold's safe haven status is unwinding at present, falling for fifth day out of seven.

- Gold is equally losing ground as bond market signals point to a declining probability of rate cuts.

- Losing ground by -0.98% to US$3,146.25 today takes gold below the 50-day EMA of $3,164.22

- Gold is up 21% year to date yet since the early May high of US$3,431.77 is down over 8%.

CHINA: Country Wrap: RRR Cut Comes into Effect

- A 0.5-percentage points reduction in the reserve requirement ratio (RRR) for eligible financial institutions takes effect Thursday, with the move expected to inject roughly 1 trillion yuan (about 139 billion U.S. dollars) of long-term liquidity into the financial market. The RRR cut, the first such move since the start of this year, was announced last week by the People's Bank of China, China's central bank. (source Xinhua)

- China on Wednesday suspended its unreliable entity list and export control measures on multiple U.S. entities, the Ministry of Commerce has said. When answering media inquiries, a ministry spokesperson said that a measure which added 11 U.S. firms to China's unreliable entity list, which was announced on April 4, has been suspended for 90 days. An April 9 measure that added six U.S. firms to China's unreliable entity list has also been paused, the spokesperson said, adding that domestic enterprises are now permitted to apply to conduct transactions with these entities. China has also suspended export control measures that added 28 U.S. entities to its export control list in announcements on April 4 and April 9 for 90 days, the spokesperson said. (source Xinhua)

- Despite solid earnings from Tencent (revenue up 13% in the March quarter) China's major bourses fell today. Next to report will be Alibaba which reports after Hong Kong close today with investors looking for an update on the launch of its new video generating model. China's Hang Seng is down -0.25% today following yesterday's strong gains. The CSI 300 is down -0.60%, Shanghai down -0.40% and Shenzhen down -0.94%.

- Yuan Reference Rate at 7.1963 Per USD; Estimate 7.2169

- CGBs remain very quiet with the 10YR trading in a tight range all week at 1.67%

INDIA: Country Wrap: Outward FDI Doubles

- India and the US are working out a fresh customs audit process to minimize the rejection of consignments, lessen the number of certification and expedite movement of goods amid ongoing trade negotiation between the two nations.

The customs representative from both sides met last week to introduce clearer protocols and auditing mechanisms in compliance with international trade standards, and at the same time to reduce certification requirements for seafood, and genetically modified agricultural goodse, and processed food, according to the Economic Times (source BBG) - India’s outward foreign direct investment (FDI) commitments almost doubled to $6.8 billion in April 2025, up from $3.58 billion in the same month last year. Sequentially, they rose from $5.9 billion in March 2025, according to data from the Reserve Bank of India (RBI). (source BBG)

- The NIFTY 50 has given back yesterday's gains and is lower by -0.43%

- The Rupee is the worst performer of its regional peers today down -0.45% at 85.66 whilst most others rallied.

- Bonds are given back some of the gains from earlier in the week with the IGB 10YR 6.31% (+3bps today)

ASIA FX: KRW & TWD Rally, But Recent Ranges Holding, CNH Steady

In North East Asia FX, the focus has been on KRW and to a lesser extent TWD, with both currencies rising against the USD, while CNH has remained on the sidelines. Equity markets have paused in terms of the recent rebound, although this hasn't impacted FX sentiment significantly today. The trend amongst the majors has mostly been for a softer USD, led by JPY.

- For USD/KRW spot we opened high and pushed to 1412, before quickly turning lower. Session lows rest at 1391.60, just above intra-session lows from Wednesday. We were last near 1396.5, still up around 0.50% in won terms for the session. Despite reported denials from US officials, markets may continue to speculate around FX policy forming part of broader trade discussions, particularly until firmer details emerge. US Trade Representative is visiting South Korea at the moment and will speak with South Korea shipping companies.

- Spot USD/TWD sits back under 30.15 in latest dealings around 0.40% stronger in TWD terms. Downside focus in this pair will rest with a re-test of 30.00. Outside of FX policy speculation, continued strong equity inflows from offshore investors, now at $6.7bn this month, continue to provide a tailwind for TWD.

- USD/CNH has been relatively quiet in comparison. We were last near 7.2100, little changed from end Wednesday levels in the US. The USD/CNY fixing nudged higher, while the error term went back to negative. Local equities and Hong Kong equities are down modestly for the first part of Thursday trade.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 15/05/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 15/05/2025 | 0600/0700 | ** | Index of Services | |

| 15/05/2025 | 0600/0700 | *** | Index of Production | |

| 15/05/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 15/05/2025 | 0600/0700 | *** | GDP First Estimate | |

| 15/05/2025 | 0600/0800 | ** | Norway GDP | |

| 15/05/2025 | 0600/0700 | ** | Trade Balance | |

| 15/05/2025 | 0645/0845 | *** | HICP (f) | |

| 15/05/2025 | 0700/0900 | Flash GDP | ||

| 15/05/2025 | 0700/0900 | ECB's Cipollone at Payments Forum | ||

| 15/05/2025 | 0750/0950 | ECB's Elderson At Green Finance Conference | ||

| 15/05/2025 | 0900/1100 | ** | Industrial Production | |

| 15/05/2025 | 0900/1100 | *** | GDP (p) | |

| 15/05/2025 | 1015/1215 | ECB's De Guindos At ISDA Meeting | ||

| 15/05/2025 | 1130/1330 | ECB's Cipollone In Digital Currency Fireside Chat | ||

| 15/05/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 15/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 15/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 15/05/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/05/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/05/2025 | 1230/0830 | *** | Retail Sales | |

| 15/05/2025 | 1230/0830 | *** | PPI | |

| 15/05/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/05/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 15/05/2025 | 1230/0830 | *** | Retail Sales | |

| 15/05/2025 | 1240/0840 | Fed Chair Jerome Powell | ||

| 15/05/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/05/2025 | 1315/0915 | *** | Industrial Production | |

| 15/05/2025 | 1400/1000 | * | Business Inventories | |

| 15/05/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 15/05/2025 | 1400/1500 | BOE Dhingra At New Economics Foundation conference | ||

| 15/05/2025 | 1400/1000 | * | Business Inventories | |

| 15/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 15/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 15/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 15/05/2025 | 1800/1400 | *** | Mexico Interest Rate | |

| 15/05/2025 | 1805/1405 | Fed Governor Michael Barr | ||

| 16/05/2025 | 2350/0850 | *** | GDP | |

| 16/05/2025 | 0430/1330 | ** | Industrial Production | |

| 16/05/2025 | 0730/0930 | ECB's Cipollone At EU Cyber Resilience Board Meeting | ||

| 16/05/2025 | 0800/1000 | *** | HICP (f) | |

| 16/05/2025 | 0900/1100 | * | Trade Balance | |

| 16/05/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/05/2025 | 1230/0830 | New York Fed's Roberto Perli | ||

| 16/05/2025 | 1230/0830 | *** | Housing Starts |