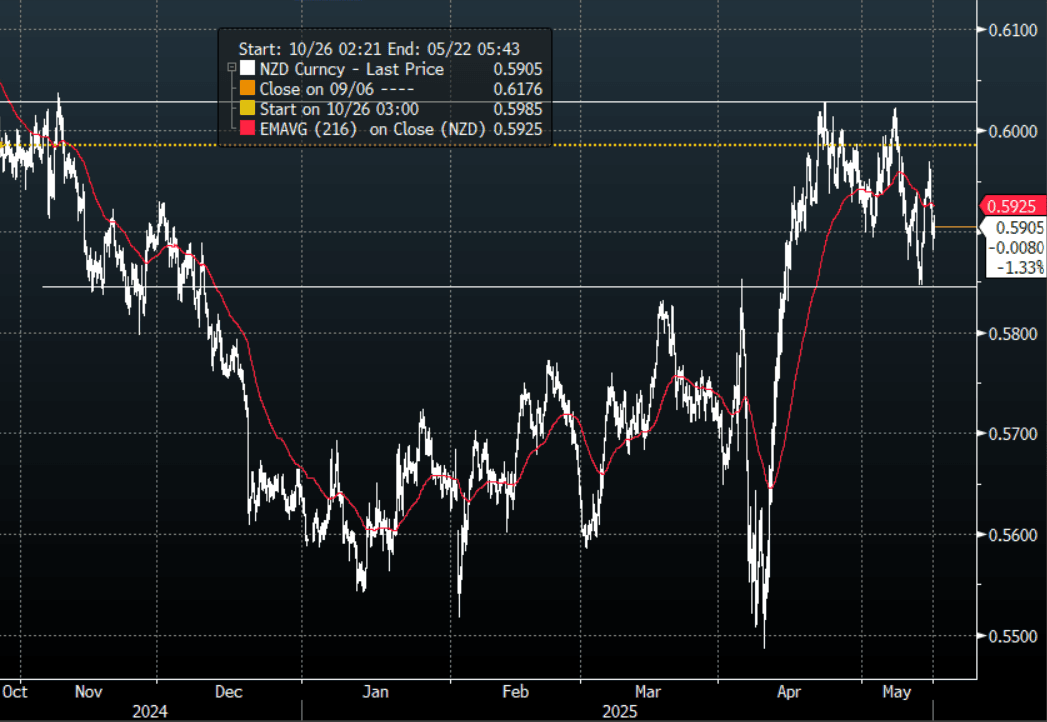

NZD: NZD/USD Wrap - Consolidating

The NZD had a range in our session of 0.5881 - 0.5916, going into the London session around 0.5905. A very quiet session for risk today with the NZD trading sideways.

- The NZD up moved in sympathy with the AUD as it popped higher on a better employment print.

- AUD/NZD continues to grind higher, attempting to get a foothold above 1.0900, the better AUD data gave it a lift printing a high of 1.0922 in our session. Support is seen back towards 1.0800 and a sustained break above 1.0900 would turn the focus higher once again.

- "APEC SEES REGIONAL GDP GROWTH FOR 2025 AT 2.6% DOWN FROM 3.3% EARLIER, APEC SEES EXPORT GROWTH FOR 2025 AT 0.4% VERSUS 5.7% IN 2024” - RTRS

- The NZD now seems to be comfortable in a 0.5800/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 held very well, and while this continues to hold expect buyers to return on dips. The first target is the highs just above 0.6000, a break above here is needed to regain momentum higher.

MNI FX OPTIONS: Expiries for May15 NY cut 1000ET (Source DTCC): NZD/USD: $0.5880(N$1.0bln)

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Yields Drift Lower in Today's Asia-Pac Session

TYM5 has traded in a tight 110-19/110-27+ range so far in today's Asia-Pac session. Going into the London open, it is dealing near its highs around 110-26,+0.02 from its close.

- The US 10-year yield has continued to drift lower in a tight range of 4.3408 - 4.3856 in Asia. Going into the London open dealing around 4.3485%.

- The market is starting to realise the FED will not be stepping in to rescue it by cutting rates, as long as it expects inflation to track higher on the back of Trump’s policies.

- The Fed’s Waller said yesterday the impacts of the tariffs on inflation would be temporary. He also described the new policy as “ one of the biggest shocks” on the US economy in decades, the effects of which are highly uncertain.

- Bostic spoke after the US market close: ”Right now range of possible outcomes has multiplied. Inflation still much higher than target. Not in position to boldly move in any direction, need more clarity.”

- Bessent says the Treasury has a big toolkit if needed for Bonds.

- Dips in the 10-year yield back towards 4.25/30% should now find supply, any move back to 5% and above would become problematic for equities.

- Upcoming Data/Events: Retail Sales and Fedspeak from Powell on Wednesday.

JGBS AUCTION: Poor Demand Metrics For 20Y Auction

The 20-year JGB auction delivered poor results across key metrics. The low price underperformed dealer forecasts, which were set at 100.40 according to a Bloomberg poll. Moreover, the cover ratio decreased to 2.9639x from 3.4594x in the previous auction and the auction tail lengthened dramatically to 0.34 from 0.20.

- As noted in the auction preview, today’s offering featured an outright yield at a cycle high, 15bps higher than last month’s auction.

- Moreover, the 10/20 yield curve was at its steepest since 1999 and the 20-year JGB was at its cheapest valuation within the 10/20/30 butterfly since early 2023.

- As a consequence, this result is likely to be seen as significantly worse than the mixed performance observed in the 30-year JGB auction earlier this month.

- Post-auction, the 20-year JGB is little changed.

JGBS AUCTION: 20-Year JGB Auction Results

The Japanese Ministry of Finance (MOF) sells Y750.9bn 20-Year JGBs:

- Average Yield: 2.349% (prev. 2.278%)

- Average Price: 100.69 (prev. 96.20)

- High Yield: 2.374% (prev. 2.294%)

- Low price: 100.35 (prev. 96.00)

- % Allotted At High Yield: 40.8163% (prev. 44.1031%)

- Bid/Cover: 2.9639x (prev. 3.4594x)