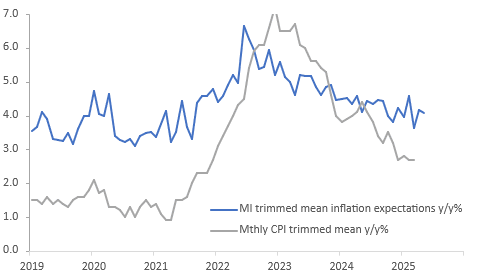

AUSTRALIA DATA: Inflation Expectations Remain Above 4% Despite Lower CPI Print

Melbourne Institute May consumer inflation expectations eased 0.1pp to 4.1%, unchanged from May 2024. It is worth noting that it didn’t fall further given the moderation in Q1 CPI released at the end of April and that petrol prices are significantly lower on a year ago and also in Q2 to date. But business price/cost components were generally higher in the April NAB business survey with retail prices jumping 1.4% 3m/3m which may be contributing to above 4% consumer inflation expectations. They have been oscillating around that level since October. Cost-of-living pressures remain households’ main concern. April CPI prints on May 28.

Australia Melbourne Institute consumer inflation expectations vs core CPI y/y%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: NZD and AUD Outperforming, Kiwi Above 200-day MA

NZD and AUD both outperforming in the G10 space, led by the Kiwi. Both currencies are through their respective highs from Monday, albeit the NZD more convincingly. NZD/USD was last near 0.5900, above its simple 200-day MA, see the chart below. AUD/USD was above 0.6340, with headlines from the RBA Minutes crossing. The RBA is maintaining a cautious tone around the timing further rate cuts.

- Generally green Asia Pac equity trends are helping the Kiwi and AUD, with the MSCI Asia Pac index up 1%, while US equity futures are back close to flat. We were down close to 0.50% at one stage in the first part of trade.

Fig 1: NZD/USD Testing Above Simple 200-day MA

Source: MNI - Market News/Bloomberg

CHINA: Central Bank Drains Liquidity during OMO

- The PBOC issued CNY164.5bn of 7-day reverse repo at 1.5% during this morning’s operation.

- Today’s maturities CNY167.4bn

- Net liquidity withdrawal CNY2.9bn.

- The PBOC monitors and maintains liquidity through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted Average is at 1.51%, from 1.70% yesterday.

- The China Overnight interbank repo rate is at 1.65%, from 1.50% yesterday.

- The China 7-day interbank repo rate is at 1.72%, from 1.70% yesterday.

STIR: RBA Dated OIS Pricing Softer Ahead Of RBA Minutes (April)

RBA-dated OIS pricing is flat to 4bps softer across meetings today.

- A 50bp rate cut in May is given a 39% probability, with a cumulative 121bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Today Vs. Yesterday

Source: MNI – Market News / Bloomberg