MNI EUROPEAN MARKETS ANALYSIS: Aust Wages Close To Forecasts

- The risk on tone from US markets on Tuesday (as Fed easing expectations firmed post the CPI print) has carried over for most Asia Pac equities today. The USD and US Tsy yields have been steadier though, albeit with some USD weakness in parts of Asia FX.

- In Australia, the Q2 WPI rose 0.8% q/q leaving annual inflation at 3.4% y/y after a recent trough at 3.2% in Q4 2024 and 4.1% in Q2 2024. Japan's PPI was close to expectations and implies some softening in headline CPI y/y momentum.

- Today the Fed’s Barkin, Goolsbee and Bostic speak. Apart from July updates for German & Spanish CPI, there are no data of note.

MARKETS

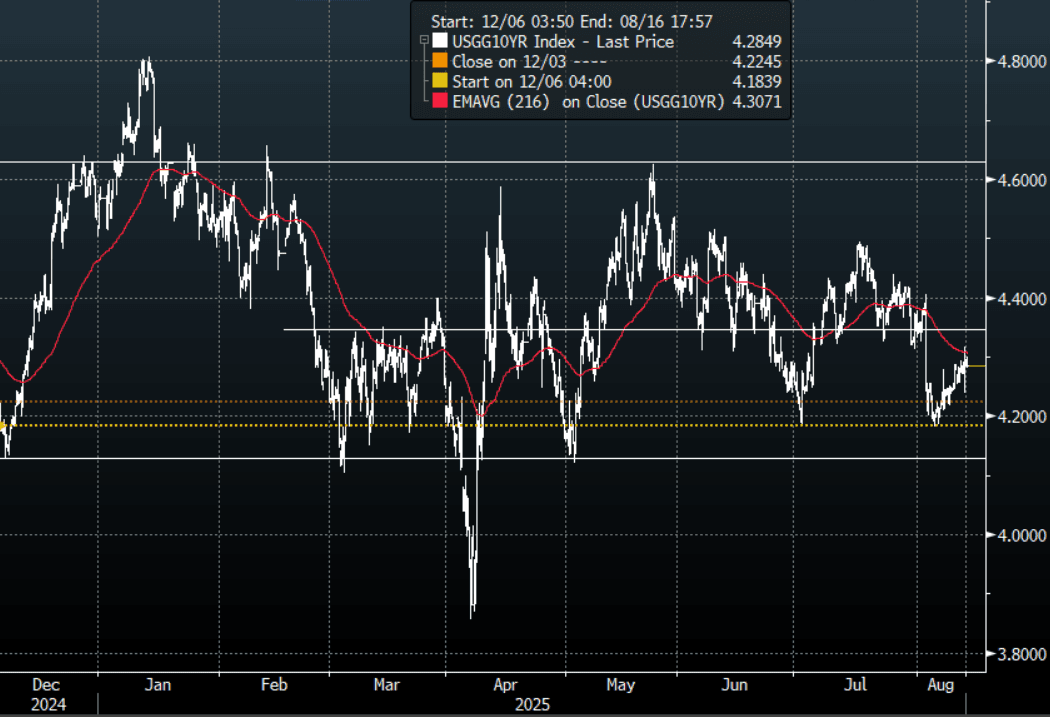

US TSYS: Yield Moves Muted In A Quiet Session

The TYU5 range has been 111-23 to 111-27 during the Asia-Pacific session. It last changed hands at 111-27, up 0-01 from the previous close.

- The US 2-year yield is trading around 3.73%, unchanged from its close.

- The US 10-year yield has edged slightly lower trading around 4.285%.

- Price action in the long-end is a little disconcerting for the bulls though the 10-Year yield still trades below its 4.30/35%% pivot within the wider range 4.10% - 4.65%. There should still be buyers of treasuries on bounces back towards 4.30/35%, looking to initially test the 4.10% area.

- Ben Hunt(Epsilon Theory) on X: “If we’re gonna cut in Sept (90% mkt odds as I write this) with core at 3.1% and rising, wages at 3.9% and rising, stocks and home prices at all-time highs … Can we at least stop talking about the Fed’s 2% inflation ‘target’? It’s just insulting to continue this charade.”

- Jim Bianco on X: “YoY Core CPI, 3.1%. Up 0.3% in the last 3-months. In the last 40 YEARS, only once has the Fed CUT rates when core was above 3% AND the 3m chg was >0.3%, Oct 1990 to Mar 1991. Agree with @EpsilonTheory, the 2% inflation target is dead. We are accepting a higher inflation world.”

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Cheaper After Poor 5Y Auction

JGB futures are weaker and at session lows, -26 compared to settlement levels, after today’s disappointing 5-year auction.

- Today’s 5-year JGB auction showed poor signals on demand. The low price came in line with expectations at 99.72, and the bid-to-cover ratio declined to 2.9616x from 3.5411x. Meanwhile the tail widened slightly to 0.03 from 0.02. The result aligns with the poor demand signals seen at this month’s 10-year auction. With yields higher and the 2s/5s curve steeper than last month, today’s outcome represents a deterioration in overall demand conditions.

- "JAPAN'S AKAZAWA: NOT BAD IF TRUMP EXEC ORDER COMES BY MID SEPT, US CAN'T GET INVESTMENT HELP IF PROMISES NOT KEPT. JAPAN COULD INCREASE ACTUAL US INVESTMENT PERCENTAGE, 1-2%, INVESTMENT FOLLOWS PAST CASES, COULD BE HIGHER" - BBG

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session after yesterday's twist-steepener.

- Cash JGBs are showing a twist-flattening, with benchmark yields 3bps higher to 2bps lower. The benchmark 5-year yield is 2.6bps higher at 1.069% versus the cycle high of 1.19%.

- Swaps rates flat to 1bp higher, with swap spreads tighter out to the 20-year.

- Tomorrow, the local calendar will be empty ahead of Q2 GDP on Friday.

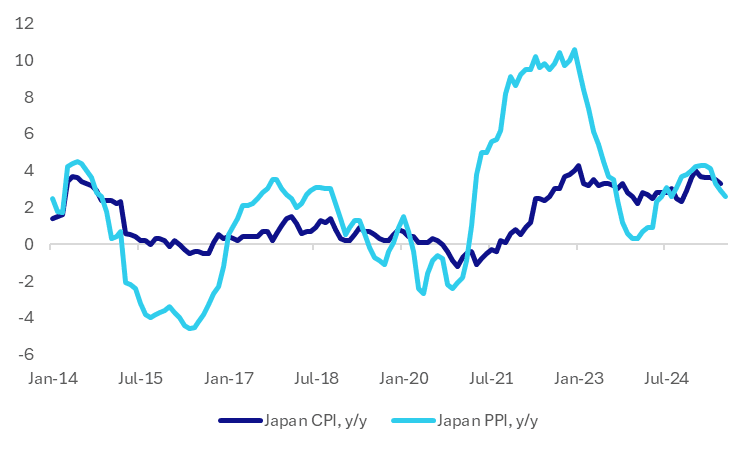

JAPAN DATA: July PPI In Line, Suggests Further Moderation In Headline Y/Y CPI

Japan's July PPI was close to expectations. The m/m outcome printed at +0.2%, in line with expectations, while the June outcome was revised to 0.1%m/m (originally reported as -0.2%). In y/y terms we printed at 2.6%, versus 2.5% forecast and 2.9% prior.

- The chart below plots the headline PPI y/y, versus the National CPI, also in y/y terms. At face value it implies some further softening in y/y CPI momentum for July. Note that this print comes out on August 22nd.

- In terms of the detail, manufacturing was up 0.2%, while some commodities, most notably petroleum, coal, rose for the first time in a number of months (+1.8%).

- The data is unlikely to shift near term BoJ thinking around wait and see mode from a policy standpoint.

Fig 1: Japan PPI & CPI, Y/Y

Source: Bloomberg Finance L.P./MNI

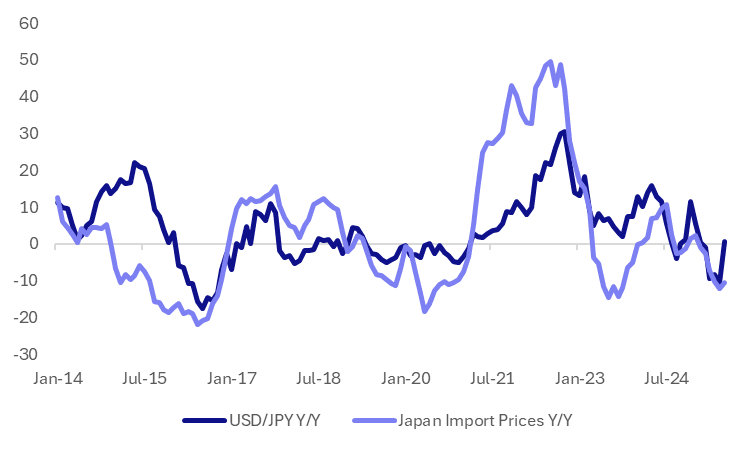

JAPAN DATA: Import Prices Up For First Month Since Jan, Y/Y Still Negative

For July, export and import prices both rose in m/m terms. Export prices were up 1.6%, while import prices were up 2.4%m/m. For import prices this was the first m/m rise since January of this year. In y/y terms, both export and import prices were still in negative territory, but up from the June levels. Export prices were -5.4%y/y, while imports were -10.4%.

- The chart below plots y/y changes in USD/JPY versus import prices y/y. To end July USD/JPY was up a touch in y/y terms. If current spot levels prevail, (currently around 147.80), USD/JPY will remain positive in y/y terms to end September (note USD/JPY was 152.03 end Oct last year).

- This implies some upside to import price y/y momentum in the near term, albeit fairly modestly. If USD/JPY holds around current level to end September, we would be up +2.9% in y/y terms.

Fig 1: Japan Import Prices & USD/JPY, Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Bull-Flattener Ahead Of Employment Data Tomorrow

ACGBs (YM +1.5 & XM flat) are slightly stronger after today’s wages data.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session after yesterday’s twist-steepener.

- With May and June employment gains disappointing, tomorrow’s July data will be monitored closely for signs that the labour market has turned. Q2 employment averaged 28.8k/month up from Q1’s 1.4k but slightly lower than Q2 2024’s 32.2k. Bloomberg consensus expects a 25k gain in July after June’s +2k, slightly below the Q2 average. The unemployment rate is forecast to decline 0.1pp to 4.2%, returning to the Q2 average.

- In its updated staff projections on Tuesday, the RBA continued to expect the Q4 2025 unemployment rate to be 4.3% and then stay there. Employment growth was revised up to 1.6% from 1.4% in Q4 2025 and it then slows to 1.4% and remains there over the rest of the forecast horizon.

- Cash ACGBs are flat to 2bps richer with a steeper 3/10 curve and the AU-US 10-year yield differential at -5bps.

- The bills strip is flat to +2.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 42% probability, with a cumulative 40bps of easing priced by year-end.

- The AOFM plans to sell A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.

RBA: MNI RBA Review-August 2025: Target Achieved With More Cuts

- Download Full Report Here

- The RBA made the unanimous decision to cut rates 25bp to 3.60%, as expected, with a larger move was not discussed.

- Around another 75bp of easing is assumed in the updated staff forecasts which results in underlying inflation at around the 2.5% band mid-point from H2 2025. Thus, more rate cuts are likely going forward dependent on the data developing broadly as the RBA expects

- Governor Bullock said that the Board continues to take things at a “measured pace”. While, she didn’t rule out “back-to-back cuts”, the next rate reduction is likely to again coincide with the Statement on Monetary Policy, which will be on November 4.

- RBA-dated OIS pricing has a 25bp rate cut in September is given a 37% probability, with a cumulative 52bps of easing priced by year-end.

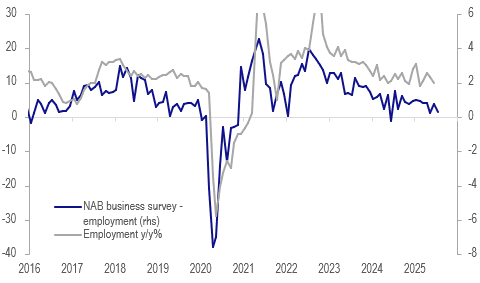

AUSTRALIA: Consensus Expects Some Normalisation In July Labour Data

With May and June employment gains disappointing, the July data will be monitored closely for signs that the labour market has turned. Q2 employment averaged 28.8k/month up from Q1’s 1.4k but slightly lower than Q2 2024’s 32.2k. Bloomberg consensus expects a 25k gain in July after June’s +2k, slightly below the Q2 average. The unemployment rate is forecast to decline 0.1pp to 4.2%, returning to the Q2 average.

- In its updated staff projections on Tuesday, the RBA continued to expect the Q4 2025 unemployment rate to be 4.3% and then stay there. Employment growth was revised up to 1.6% from 1.4% in Q4 2025 and it then slows to 1.4% and remains there over the rest of the forecast horizon.

- The employment component of the NAB business survey is signalling that labour demand growth is slowing and so we may see average job prints trending lower over coming months.

- Analysts’ projections for job gains in July range from +12k to +50k with most between +15k and +35k. The large local banks are clustered around consensus with ANZ and Westpac in line, but CBA and NAB slightly lower at 20k and 23k respectively.

- Unemployment rate expectations are between 4.2% and 4.4% with NAB and Westpac forecasting it to drop 0.1pp to 4.2%, but ANZ and CBA expecting it to stay at 4.3%.

- The participation rate is projected to be steady at 67.1%.

Australia NAB business survey employment vs employment y/y%

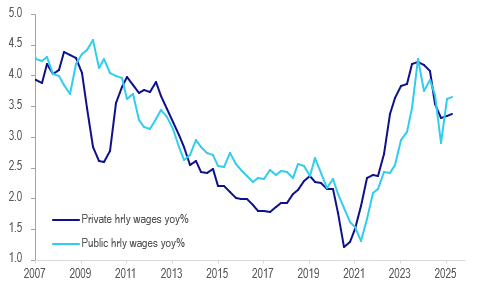

AUSTRALIA DATA: Public Pay Growth Outpacing Private Sector

The Q2 WPI rose 0.8% q/q leaving annual inflation at 3.4% y/y after a recent trough at 3.2% in Q4 2024 and 4.1% in Q2 2024. Public sector quarterly wage gains outpaced the private sector for the third consecutive quarter at 1.0% q/q compared with 0.8%. Public wage growth is now up 0.1pp to 3.7% y/y, while private was 3.4% y/y. The RBA had forecast 3.3% for Q2 and in its August projections is expecting the WPI to trend lower to around 3% by Q2 2026. 2025 to date is showing some stabilisation in wage inflation.

Australia private vs public wages ex bonuses y/y%

- The share of large pay rises, above 4%, has declined substantially over the last year at 25% after 46% in Q2 2024.

- Private sector average wage rises in Q2 were 3.9% down from 4.2% a year ago. The share of employees receiving an increase was little changed at 12% compared to 11%.

- In the public sector, the share was 20% after 19% in Q2 last year with the average rise 3.5% down from 3.8%.

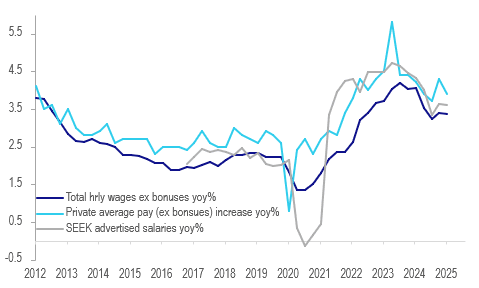

- SEEK advertised salaries rose 0.8% q/q in Q2, in line with the WPI result. Annual growth has trended lower since peaking at 4.9% y/y in September 2023 and was 3.5% in June this year.

- 55% of pay increases were covered by individual agreements. Awards tend to see changes scheduled for July 1, which will impact the Q3 data. The minimum wage rose 3.5% on July 1.

Australia wages ex bonuses y/y%

NEW ZEALAND: Gradual Recovery In Retail Card Spending

July NZ card transactions rose 0.6% m/m, the highest monthly increase this year, but the annual rate is still down 1.0%. Retail spending was up 0.2% m/m rising 1.2% y/y, signalling a gradual recovery in nominal consumption. It has been trending higher since the March trough at -1.8% y/y. The RBNZ is likely to cut rates on August 20 as inflation is in the band and the economic recovery remains subdued, and the July card data was consistent with this.

- While total retail spending rose slightly on the month, the core was close to flat. Statistics NZ noted that consumables transactions rose 0.5% m/m, while vehicles ex fuel jumped 5.2%. Apparel fell 1.9% and durables -0.8%.

- Non-retail ex services expenditure increased 1.6% m/m but services only 0.3%.

NZ card spending y/y%

Source: MNI - Market News/LSEG

BONDS: NZGBS: Closed With A Modest Bull-Steepener

NZGBs closed showing a bull-steepener, with benchmark yields 2bps lower to 1bp higher.

- The NZ-US and NZ-AU 10-year yield differentials closed flat and 2bps wider, respectively.

- July NZ card transactions rose 0.6% m/m, the highest monthly increase this year, but the annual rate is still down 1.0%. Retail spending was up 0.2% m/m rising 1.2% y/y, signalling a gradual recovery in nominal consumption. It has been trending higher since the March trough at -1.8% y/y. The RBNZ is likely to cut rates on August 20 as inflation is in the band and the economic recovery remains subdued, and the July card data was consistent with this.

- Swap rates closed 1-2bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed slightly softer across meetings. 23bps of easing is priced for August, with a cumulative 41bps by November 2025.

- Tomorrow, the local calendar will be empty ahead of the July BNZ manufacturing PMI Index and July monthly price series on Friday.

- Tomorrow, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 2.75% Apr-37 bond.

FOREX: Asia Wrap - USD Bears Back In Charge ?

The BBDXY has had a range of 1202.63 - 1204.07 in the Asia-Pac session, it is currently trading around 1203, -0.02%. The USD collapsed in the N/Y Session as the market rushed to re-enter or add to USD shorts. This is clearly the side the market is more comfortable trading and a sustained break below 1197 could see the move lower regain momentum and a retest of the year's lows.

- EUR/USD - Asian range 1.1670 - 1.1688, Asia is currently trading 1.1685. The market moved very quickly back to 1.1700 where it stalled on its first attempt to challenge this area. Will this second attempt have the impetus to break through.

- GBP/USD - Asian range 1.3493 - 1.3508, Asia is currently dealing around 1.3505. The pair bounced nicely off the 1.3100/1.3200 support area. Like a few other G10 currencies the reasons to fade this initial impulse higher don’t look as strong, as the USD begins to look vulnerable again.

- USD/CNH - Asian range 7.1817 - 7.1883, the USD/CNY fix printed 7.1350, Asia is currently dealing around 7.1830. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.05%, Gold $3350, US 10-Year 4.287%, BBDXY 1203, Crude Oil $63.23

- Data/Events : Germany Wholesale Price Index/CPI, Spain CPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

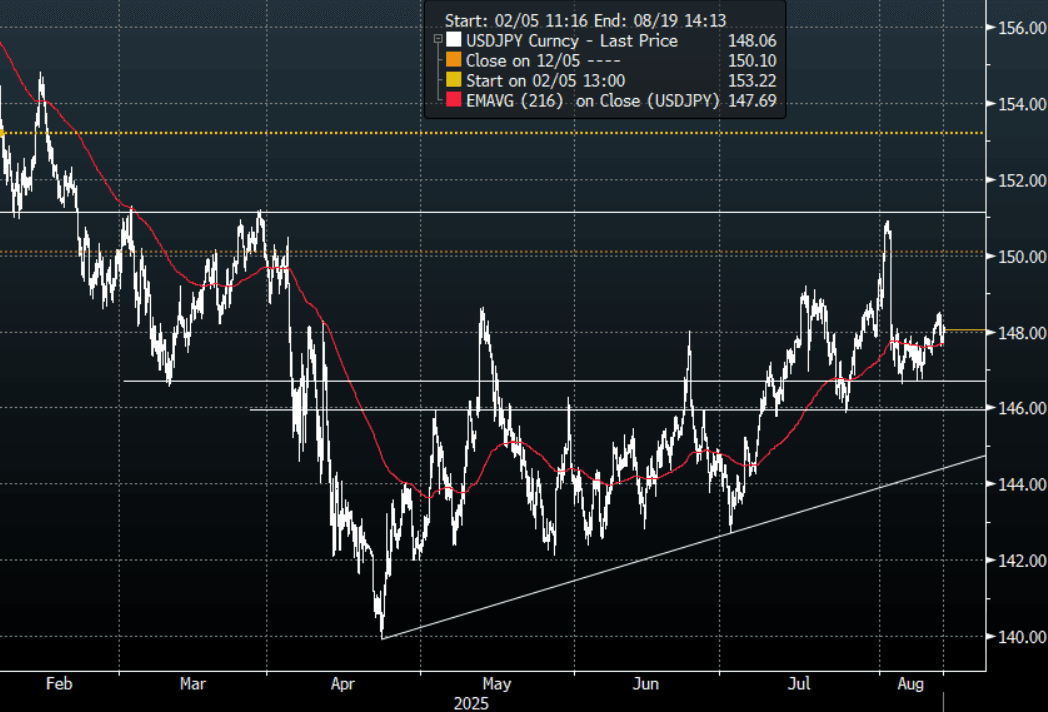

JPY: Asia Wrap - USD/JPY Finds Demand Sub 148.00

The Asia-Pac USD/JPY range has been 147.70 - 148.17, Asia is currently trading around 148.05, +0.15%. USD/JPY’s gains going into the US CPI were quickly reversed after the print. Price is currently still holding above the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again. Until then, the recent range of 146.50-148.50 will continue to dominate. Decent demand seen below 148.00 in our session.

- JAPAN DATA July PPI In Line, Suggests Further Moderation In Headline Y/Y CPI: Japan's July PPI was close to expectations. The m/m outcome printed at +0.2%, in line with expectations, while the June outcome was revised to 0.1%m/m (originally reported as -0.2%). In y/y terms we printed at 2.6%, versus 2.5% forecast and 2.9% prior.

- JAPAN DATA Import Prices Up For First Month Since Jan, Y/Y Still Negative : For July, export and import prices both rose in m/m terms. Export prices were up 1.6%, while import prices were up 2.4%m/m. For import prices this was the first m/m rise since January of this year. In y/y terms, both export and import prices were still in negative territory, but up from the June levels. Export prices were -5.4%y/y, while imports were -10.4%.

- "JAPAN'S AKAZAWA: NOT BAD IF TRUMP EXEC ORDER COMES BY MID SEPT, US CAN'T GET INVESTMENT HELP IF PROMISES NOT KEPT. JAPAN COULD INCREASE ACTUAL US INVESTMENT PERCENTAGE, 1-2%, INVESTMENT FOLLOWS PAST CASES, COULD BE HIGHER" - BBG

- "AKAZAWA: WILL SUPPORT ISHIBA IF HE RUNS AGAIN FOR LDP HEAD" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($1.06b), 146.85($751m).Upcoming Close Strikes : 149.00($1.15b Aug 14) - BBG.

- CFTC data shows asset managers reduced their JPY longs +60532( Last +75119), leveraged funds slightly reduced their newly built short JPY position -29308(Last -31280).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

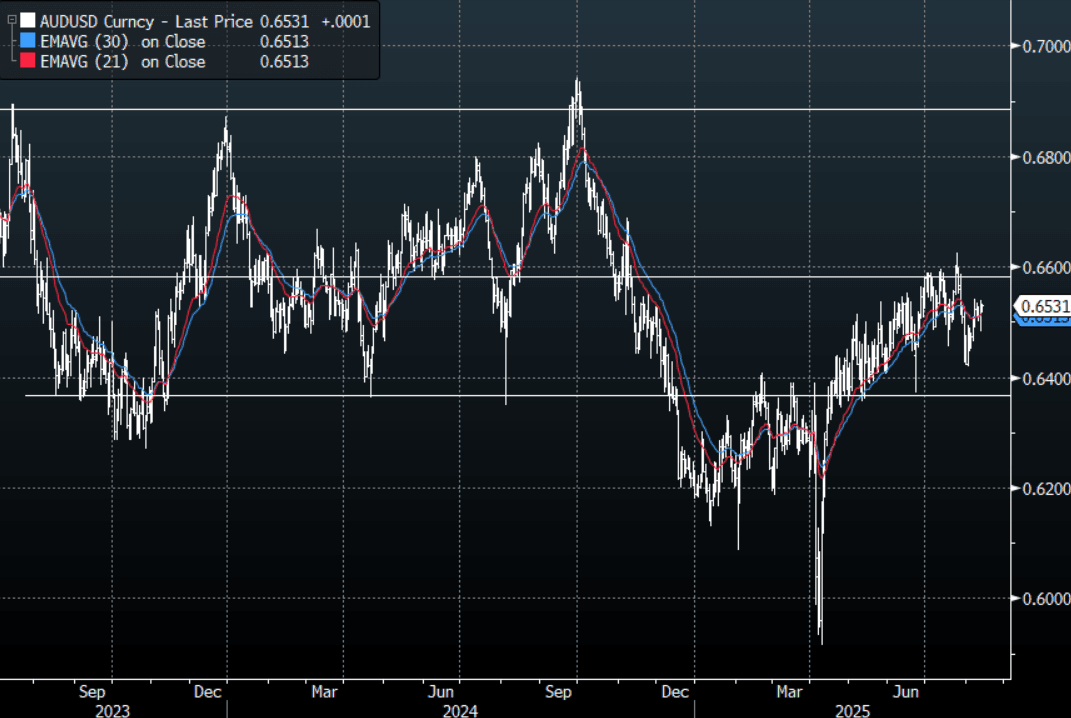

AUD: Asia Wrap - AUD/USD Consolidates Back Above 0.6500

The AUD/USD has had a range of 0.6517 - 0.6532 in the Asia- Pac session, it is currently trading around 0.6530, +0.02%. US equities roared higher as the market gets ready for more rate cuts, the slight reprieve for the USD going into the print was quickly reversed. The more cuts being priced in increases the pressure on an already bearish USD market. I felt the bounce back towards 0.6550 offered a good risk/reward to fade initially but if the US starts pricing in more aggressive cuts can the AUD ignore it? The Price remains firmly in the 0.6350-0.6650 range, if the USD extends lower can it test the top end?

- MNI AUSTRALIA: Consensus Expects Some Normalisation In July Labour Data. With May and June employment gains disappointing, the July data will be monitored closely for signs that the labour market has turned. Q2 employment averaged 28.8k/month up from Q1’s 1.4k but slightly lower than Q2 2024’s 32.2k. Bloomberg consensus expects a 25k gain in July after June’s +2k, slightly below the Q2 average. The unemployment rate is forecast to decline 0.1pp to 4.2%, returning to the Q2 average.

- MNI AU DATA: Public Pay Growth Outpacing Private Sector. The Q2 WPI rose 0.8% q/q leaving annual inflation at 3.4% y/y after a recent trough at 3.2% in Q4 2024 and 4.1% in Q2 2024. Public sector quarterly wage gains outpaced the private sector for the third consecutive quarter at 1.0% q/q compared with 0.8%. Public wage growth is now up 0.1pp to 3.7% y/y, while private was 3.4% y/y. The RBA had forecast 3.3% for Q2 and in its August projections is expecting the WPI to trend lower to around 3% by Q2 2026. 2025 to date is showing some stabilisation in wage inflation.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6575(AUD746m), 0.6550(AUD597m). Upcoming Close Strikes : 0.6600(AUD1.25b Aug 14), 0.6690(AUD583m Aug 14), 0.6523(AUD562m Aug15) - BBG

- AUD/JPY - Asia-Pac range 96.40 - 96.70, Asia is trading around 96.70. The pair has bounced and is testing its first resistance around the 96.50/97.00 area. There should be sellers around here initially, but a break above 97.50 though would negate this and reinstate the momentum higher.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

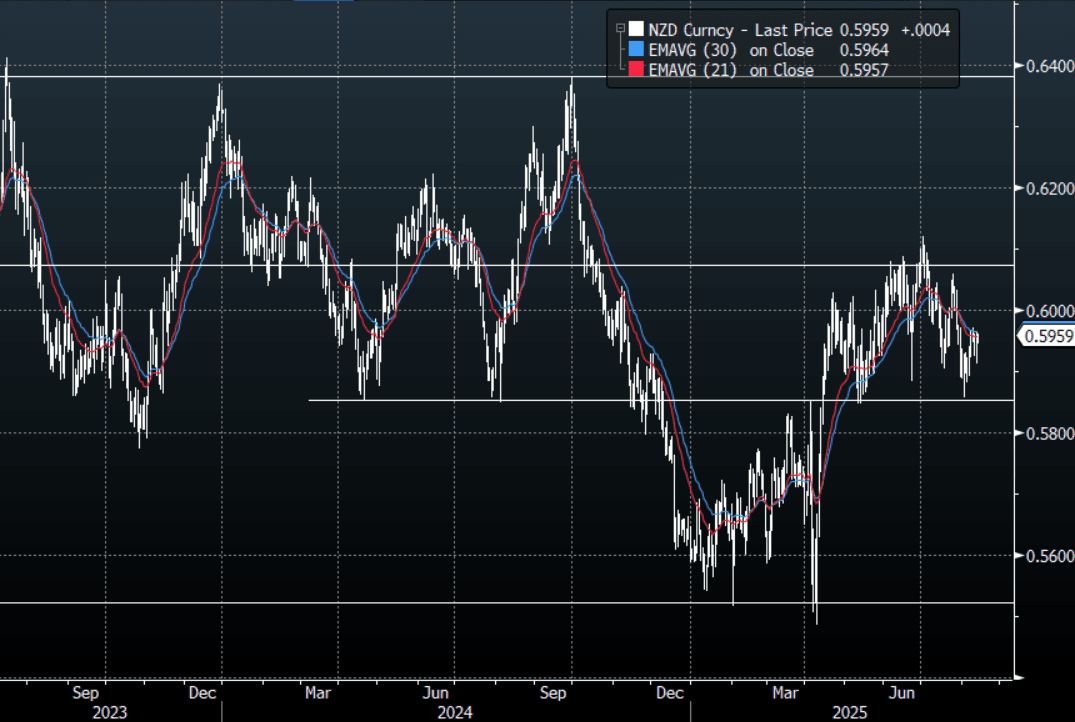

NZD: Asia Wrap - NZD/USD Slightly Higher As USD Bears Wrestle Back Control

The NZD/USD had a range of 0.5945 - 0.5961 in the Asia-Pac session, going into the London open trading around 0.5960, +0.08%. US equities roared higher as the market got ready for more rate cuts, the slight reprieve for the USD going into the print was quickly reversed and more cuts being priced in will increase the pressure on an already bearish USD market. Risk has ben pretty mute today, E-minis +0.05%, NQU5 +0.09%. The NZD/USD is still firmly within its 0.5850-0.6150 range, the CPI print last night will probably give pause to those wanting to fade the bounce, can it give it the boost it needs to regain upward momentum though, time will tell.

- MNI NZ: Gradual Recovery In Retail Card Spending. July NZ card transactions rose 0.6% m/m, the highest monthly increase this year, but the annual rate is still down 1.0%. Retail spending was up 0.2% m/m rising 1.2% y/y, signalling a gradual recovery in nominal consumption. It has been trending higher since the March trough at -1.8% y/y. The RBNZ is likely to cut rates on August 20 as inflation is in the band and the economic recovery remains subdued, and the July card data was consistent with this.

- (Bloomberg) - "China Consumer Loan Subsidy Expected to Drive Lending Recovery. China’s consumer loan interest subsidy program is expected to support a recovery in lending, especially for operating loans in the consumer services sector, while benefiting major banks and enhancing their market share, according to analysts from brokerages including China Merchants Securities." BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD300m Aug 14). - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short in the NZD -1811(Last +3903), the Leveraged community added to their shorts slightly -6778(Last -6250).

- AUD/NZD range for the session has been 1.0955 - 1.0969, currently trading 1.0960. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Mostly A Sea Of Green Following US Lead, Aust Lags

Asian stocks markets are nearly higher across the board (with the ASX 200 and Philippines bourse the main outliers at this stage). After very strong gains in cash Tuesday trade, as speculation grew for Fed easing after the US CPI print), US futures are close to unchanged so far in Wednesday trade. Nevertheless, the positive spillover is evident for most parts of the region.

- Japan markets continue to rally, the NKY 225, up around +1.4% and above 43300, which is a fresh record high. The Topix is up +0.90%, while a poor 5yr debt auction has impacted sentiment at this stage. Positive spill over from US moves have been cited as a major driver so far today.

- In US trade on Tuesday, the SOX index rose nearly 3.0%. The Taiex, in Taiwan, was up in the first part of trade, tracking to a fresh record high, but is now back around flat. South Korea's Kospi is up 0.65%, back above the 3200 level. Foreign investors have been net buyers so far today (per NBUY on BBG), while onshore institutional and retail investors have been net sellers.

- China and Hong Kong markets are also higher. The CSI 300 last around +0.90%. Earlier we heard from the authorities who outlined plans on consumption subsidies (via subsidizing personal loans) to boost consumption. The HSI is up around +1.90%, with the tech sub index +2.35%.

- In South East Asia, Thailand markets have returned from a two-day break and are higher by 0.75%. We have the BoT later, which is expected to cut, albeit as a close call. Malaysia and Indonesia are both up over 1%, but the Philippines is lagging.

- In Australia, the ASX 200 is struggling, last down around 0.50%. Reported profit taking on CBA (after it posted results) is weighing on financial related stocks.

ASIA STOCKS: Indonesia Sees Best Inflow Day Since April, Some Outflows Elsewhere

Yesterday saw modest outflows from both South Korean and Taiwan stocks. Both markets still remain positive from a net inflow standpoint over the past 5 trading days, but we are off recent highs for this metric. We did see tech equity outperformance through Tuesday US trade, with the SOX surging 3%, as Fed easing expectations firmed in the aftermath of the CPI print. South Korean equities are tracking modestly higher in the first part of Wednesday trade. Focus will remain on global trends, along with the South Korean government's policy outlook.

- In South East Asia, Indonesia was the standout in terms of positive inflow momentum. Yesterday's +$136mn in net inflows was the best inflow day since mid April of this year. The JCI rallied strongly yesterday, +2.44%, which pushed the index back Oct 2024 levels. There didn't appear a fresh catalyst for this move, but offshore participation in the July rally in the JCI was fairly muted, so some catch up may in play.

- Elsewhere, outflows continued from Malaysia, while Indian outflows were recorded at the start of this year.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -49 | 217 | -4908 |

| Taiwan (USDmn) | -134 | 822 | 4285 |

| India (USDmn)* | -110 | -851 | -12138 |

| Indonesia (USDmn) | 136 | 224 | -3557 |

| Thailand (USDmn)** | 3 | 122 | -1696 |

| Malaysia (USDmn) | -24 | -192 | -3267 |

| Philippines (USDmn) | 4 | 19 | -613 |

| Total (USDmn) | -173 | 361 | -21895 |

| * Data Up To Aug 11 | |||

| ** Data Up To Aug 8 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Range Trading, EIA US Stock Data & IEA Report Out Later

After falling around a percent on Tuesday, oil prices are little changed during APAC trading as the market waits for today’s IEA monthly report and US EIA inventory data, as well as the outcome of Friday’s Trump-Putin meeting. Ahead of this European and US leaders are holding a virtual meeting Wednesday to discuss Ukraine while President Zelenskyy has said they won’t cede the Donbas region. A truce is going to be difficult to reach thus making an easing of sanctions on Russia a distant prospect.

- WTI is slightly higher at around $63.23/bbl, close to the intraday high of $63.26. Brent is 0.2% higher at $66.23/bbl after rising to $66.24. Holiday-affected trading is resulting in lower volumes.

- The US EIA revised higher its global excess supply expectations for 2026 in its August report, while OPEC projected a tighter market (it tends to be the most optimistic of the three organisations). The IEA publishes later today and its output projections are likely to be monitored given ongoing excess supply concerns, which weigh on oil prices when geopolitical risks are in the background.

- Bloomberg reported that US oil inventories grew 1.5mn barrels last week, according to people familiar with the API data. In term of products, there was a gasoline drawdown of 1.8mn but distillate rose 300k. The official EIA data is out later Wednesday.

- Today the Fed’s Barkin, Goolsbee and Bostic speak. Apart from July updates for German & Spanish CPI, there are no data of note.

Gold Range Trading Post-US CPI Data, Fed Speakers Later

Gold prices have been moving in a narrow range during today’s APAC session with few drivers after rising 0.2% to $3348.26/oz on Tuesday as the market priced in a higher probability of a Fed rate cut in September, now around 95%, following July US CPI data showing subdued goods inflation despite higher import duties.

- Bullion fell to a low of $3342.78 before rising to $3354.35 to be 0.1% higher today at $3351.1. It is trading between initial resistance at $3409.2, 8 August high, and support at $3268.2, 30 July low. The US dollar and yields are also steady.

- Silver has outperformed today rising 0.7% to $38.193, close to the intraday high. It fell to $37.85 early in the session. The technical trend remains bullish with initial resistance at $39.655. Initial support is at $36.216, 31 July low.

- Equities are generally stronger with the Hang Seng up 1.9% and Nikkei +1.6% but S&P e-mini flat and ASX down 0.5%. Oil prices are flat with WTI around $63.18/bbl. Copper is down 0.3%.

- Later the Fed’s Barkin, Goolsbee and Bostic speak. Apart from July updates for German & Spanish CPI, there are no data of note.

CHINA: Country Wrap: Plans Afoot to Subsidize Consumer Loans

- China plans to subsidize interest payments on eligible personal consumer loans from Sept. 2025 to Aug. 2026, according to a statement from the Ministry of Finance. Subsidy applies to loans under 50,000 yuan for consumption, and designated big-ticket items over 50,000 yuan — including autos, education, and healthcare. China’s consumer loan interest subsidy program is expected to support a recovery in lending, especially for operating loans in the consumer services sector, while benefiting major banks and enhancing their market share, according to analysts from brokerages including China Merchants Securities. (source BBG)

- resident Xi Jinping and Brazilian President Luiz Inacio Lula da Silva have expressed their opposition to unilateralism and protectionism, and pledged to promote the greater development of bilateral ties. In a phone conversation between the two heads of state on Tuesday, Xi told Lula that China is ready to work with Brazil to set an example of unity and self-reliance among major countries of the Global South, and to jointly build a more just world and a more sustainable planet. (source China Daily)

- China and Hong Kong markets are also higher. The CSI 300 last around +0.90%. The HSI is up around +1.90%, with the tech sub index +2.35%.

- Yuan Reference Rate at 7.1350 Per USD; Estimate 7.1768

- Ten year government bond yields are modestly lower with the 10-year at 1.72%

SOUTH KOREA: Country Wrap: Unemployment Down in July

- South Korea’s adjusted unemployment rate fell to 2.5% in July, compared to 2.6% last month, according to Statistics Korea statement. Estimate at 2.6% (range 2.5% to 2.8%, 10 economists). 171,000 jobs were added in July from a year earlier. Labor force participation rate at 65% in July. Population over 15 years old increased 0.4% from a year ago (source BBG)

- President Lee Jae Myung on Wednesday raised the possibility of supporting an expansionary fiscal policy, calling for measures to improve the efficiency in government spending to boost economic growth. Lee voiced concerns over limited financial resources to push forward government initiatives during a meeting with financial officials and economic experts to discuss ways to improve efficiency in budget spending. "Although fiscal policy should serve as a catalyst for growth, tax revenues are decreasing. The slowdown in economic growth has reduced revenue, making national finances vulnerable," Lee said. (source Korea Times)

- After three consecutive days of losses, the KOSPI bounced today with gains of +0.79%

- The Won didn't participate in the regional rally today, left hovering around 1,383.45

- Bonds are seeing steeper curves with the 10yr at 2.82% (from yesterday's close of 2.80%)

INDONESIA: Country Wrap: FTA Focus Continues for Indonesia

- The Ministry of Trade has announced that 90.68 percent, or around 7,257 categories of Indonesian goods, can now enter Peru tariff-free under the Indonesia-Peru Comprehensive Economic Partnership Agreement (CEPA). The products benefiting from the import tariff exemption include motor vehicles, footwear, textiles, palm oil and its derivatives, manufactured goods, and household appliances. (source Antara)

- Indonesia is hoping to ink a trade pact with Canada later this year, although the two governments have yet to set a date, according to a senior officials. Both countries had substantially concluded the negotiations for their bilateral comprehensive economic partnership agreement (CEPA) last December. Under this deal, Canada agrees to drop a significant chunk of tariffs on Indonesian goods. Jakarta will also enjoy a similar treatment for its Canada-bound exports. (source Jakarta Globe)

- The Jakarta Composite has had an impressive day again up +1.3% following on from yesterday's +2.44% rise.

- The Rupiah has had a strong day also with gains of +0.33% to 16,235.

- Bonds have had a decent rally with he 5YR continuing to perform, down -3bps. The 10yr is at 6.42%

ASIA FX: SEA FX Higher, USD/IDR At 200-day EMA Support, BoT Later

In South East Asia FX, there is a more clear bias of a softer USD trend, although part of this is catch to USD losses post onshore markets closing yesterday. IDR is up around 0.30%, likewise for PHP, while MYR is up close to 0.25%. Regional equities are mostly up firmly, following the strong lead from US markets on Tuesday (as Fed easing expectations build post the CPI print).

- Spot USD/IDR is testing under 16240 at the time of writing. This is around the 200-day EMA support zone. Recent breaks sub this support level haven't been sustained. We have to go back to 2024 for a meaningful period where we were under this support level. Cross asset signals are in favor of IDR, with global and local equities rallying. Better offshore inflows are also evident into local stocks and bonds.

- USD/PHP has found support just under the 50 and 100-day support points, getting to lows of 56.83, but we sit back above 56.90 in latest dealings. Philippines equities have been laggards of late, which may be reducing PHP impetus at the margins.

- USD/MYR is back around 4.2200, +0.25% in MYR terms. This is fresh lows back to late July. Downside focus in the pair will be on a re-test of the 4.2000 region.

- USD/THB was higher in the first part of trade, getting to 32.41, after onshore markets were out for the first two days this week. We sit back at 32.33 now though, unchanged from end Friday levels last week. The main focus today will be on the BoT decision later. As per our preview: Given that inflation is below the Bank of Thailand's (BoT) 1-3% target band and growth is lacklustre and lending continues to contract, 14/23 analysts surveyed by Bloomberg are forecasting a 25bp rate cut to 1.5% on August 13. However, there are also numerous reasons for it to be on hold, thus it is a close call. A new governor takes over from October 1, Vitai, and he is considered to be dovish. If rates are left at 1.75%, it will be a dovish hold and there is likely to be at least one 25bp cut in one of the two BoT meetings left in 2025.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 13/08/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 13/08/2025 | 0700/0900 | *** | HICP (f) | |

| 13/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 13/08/2025 | - | *** | Money Supply | |

| 13/08/2025 | - | *** | New Loans | |

| 13/08/2025 | - | *** | Social Financing | |

| 13/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 13/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 13/08/2025 | 1700/1300 | Chicago Fed's Austan Goolsbee | ||

| 13/08/2025 | 1730/1330 | Atlanta Fed's Raphael Bostic | ||

| 14/08/2025 | - | NorgesBank Meeting | ||

| 14/08/2025 | 0130/1130 | *** | Labor Force Survey | |

| 14/08/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0600/0700 | ** | Trade Balance | |

| 14/08/2025 | 0600/0700 | ** | Index of Services | |

| 14/08/2025 | 0600/0700 | ** | Index of Production | |

| 14/08/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 14/08/2025 | 0600/0700 | *** | GDP First Estimate | |

| 14/08/2025 | 0645/0845 | *** | HICP (f) | |

| 14/08/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 14/08/2025 | 0900/1100 | ** | Industrial Production | |

| 14/08/2025 | 0900/1100 | *** | GDP (p) | |

| 14/08/2025 | 0900/1100 | * | Employment | |

| 14/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 14/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1230/0830 | *** | PPI |