OIL: Crude Range Trading, EIA US Stock Data & IEA Report Out Later

After falling around a percent on Tuesday, oil prices are little changed during APAC trading as the market waits for today’s IEA monthly report and US EIA inventory data, as well as the outcome of Friday’s Trump-Putin meeting. Ahead of this European and US leaders are holding a virtual meeting Wednesday to discuss Ukraine while President Zelenskyy has said they won’t cede the Donbas region. A truce is going to be difficult to reach thus making an easing of sanctions on Russia a distant prospect.

- WTI is slightly higher at around $63.23/bbl, close to the intraday high of $63.26. Brent is 0.2% higher at $66.23/bbl after rising to $66.24. Holiday-affected trading is resulting in lower volumes.

- The US EIA revised higher its global excess supply expectations for 2026 in its August report, while OPEC projected a tighter market (it tends to be the most optimistic of the three organisations). The IEA publishes later today and its output projections are likely to be monitored given ongoing excess supply concerns, which weigh on oil prices when geopolitical risks are in the background.

- Bloomberg reported that US oil inventories grew 1.5mn barrels last week, according to people familiar with the API data. In term of products, there was a gasoline drawdown of 1.8mn but distillate rose 300k. The official EIA data is out later Wednesday.

- Today the Fed’s Barkin, Goolsbee and Bostic speak. Apart from July updates for German & Spanish CPI, there are no data of note.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Closed Near Cheaps, Bear-Steepener

NZGBs closed near the session’s worst level, showing a modest bear-steepener. Benchmark yields were flat to 3bps higher. The NZ-US 10-year yield differential closed 2bps tighter at +14bps.

- The New Zealand performance of services index rebounded somewhat in June, rising to 47.3 from 44.1 (per BNZ and Business NZ). We are still sub the early 2025 highs for the index, which was just above the 50 expansion/contraction point.

- (Bloomberg) -- RBNZ balance sheet has shrunk further in June, according to data posted on the central bank website Monday in Wellington. Total assets declined to NZ$72.4b from NZ$77.3b at May 31, and from NZ$84.4b at June 20, 2024, the smallest since November 2020.

- Swap rates closed flat to 2bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed slightly softer across meetings. 19bps of easing is priced for August, with a cumulative 34bps by November 2025.

- Tomorrow, the local calendar will be empty.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 4.50% May-30 bond, NZ$200mn of the 4.25% May-36 bond and NZ$50mn of the 1.75% May-41 bond.

NZD: Asia Wrap NZD/USD - Challenging Support Just Below 0.6000

The NZD/USD had a range of 0.5981 - 0.6015 in the Asia-Pac session, going into the London open trading around 0.5985, -0.40%. Risk is opening on the backfoot this morning as the world has to again digest Trump's next round of tariffs this time on Europe and Mexico, E-Mini -0.40%, NQ -0.40%. NZD/USD needs to hold this support just below 0.6000 to build for another test higher, the risk is the USD taking a leg higher. A break below this support and the market would look back towards the 0.5850/0.5900 area.

- NZ Data - Services PMI Firmer In June, But Still Comfortably Sub 50.0 : The New Zealand performance of services index rebounded somewhat in June, rising to 47.3 from 44.1 (per BNZ and Business NZ). We are still sub the early 2025 highs for the index, which was just above the 50 expansion/contraction point.

- NZ Data - Mixed June Card Spending Trends, Down For Q2: June card spending figures were mixed, with total spending down 0.2% m/m, after a 0.3% May gain. Card spending for retail rose 0.5%m/m, after a revised 0.1% fall in May.

- (Bloomberg) -- RBNZ balance sheet has shrunk further in June, according to data posted on the central bank website Monday in Wellington. Total assets declined to NZ$72.4b from NZ$77.3b at May 31, and from NZ$84.4b at June 20, 2024, smallest since November 2020.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none.

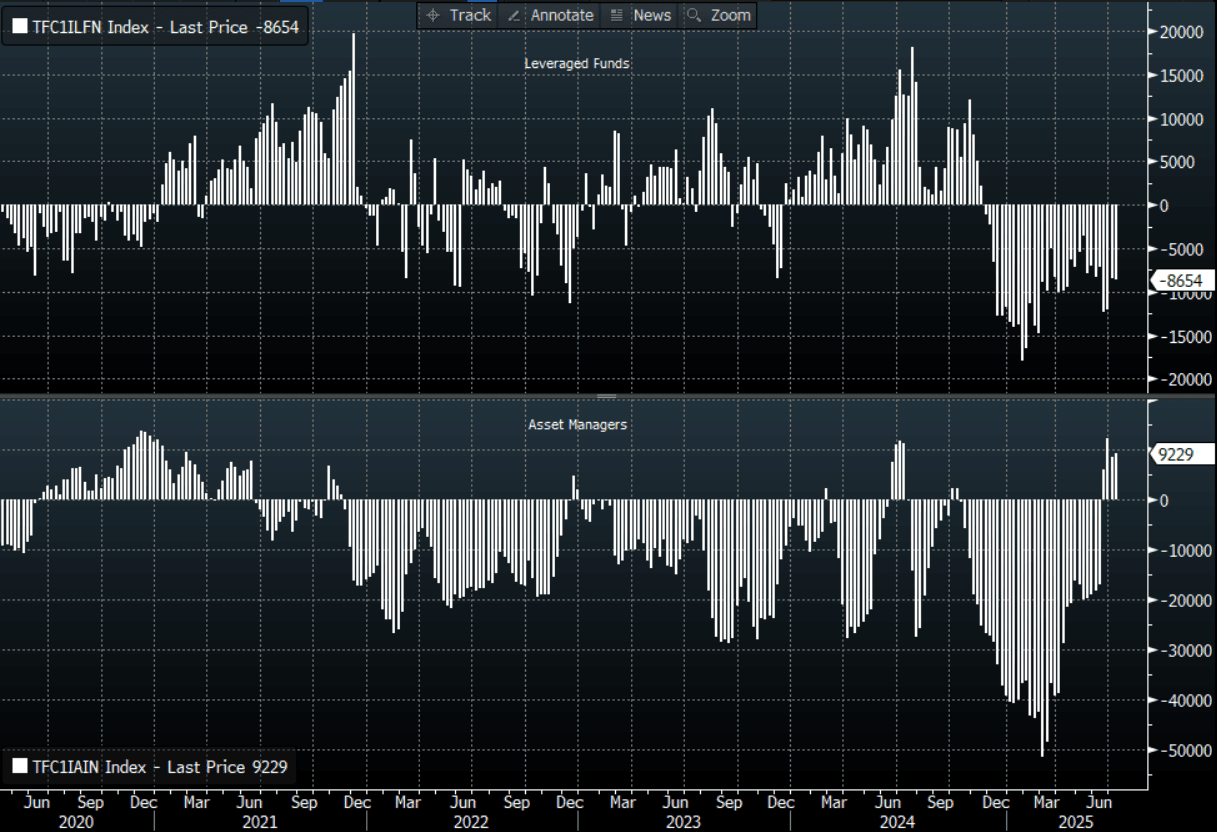

- CFTC Data shows Asset Managers added slightly to their newly built longs in NZD +9229, the Leveraged community added slightly to their shorts last week -8654.

- AUD/NZD range for the session has been 1.0927 - 1.0972, currently trading 1.0970. TThe cross has broken out of its recent range and is now trying to push through the more pivotal 1.0950 area. Dips back to 1.0850/1.0900 should now be supported as the pair tries to build momentum to move higher.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Modest Gains Evident For Most Markets, Despite Negative US Futures

Asian stock markets have had a fairly indifferent start to the trading week, albeit with a positive bias for most markets. At this stage, aggregate moves are not much beyond 0.50% for the major regional bourses. US equity futures are down close to 0.40% at this stage. Weekend threats from US President Trump on a 30% tariff for the EU (as well as Mexico) has weighed on sentiment. EU futures are down around 0.60% at this stage. There appears to be room for negotiations but concrete deals might be difficult to achieve ahead of the August 1 deadline.

- China and Hong Kong markets are marginally higher in the first part of Monday trade. The CSI 300 holding above 4000 at this stage, while the HSI is above 24000. Earlier we have China June trade data, where export and import growth marginally surprised on the upside. These trends don't look spectacular but are holding up well considering tariff levels.

- Japan markets are marginally higher in the first part of Monday trade. We continue to sell upward pressure on longer dated JGB yields. We have upper house elections later this week. Local news wires noted that the ruling bloc may struggle to keep its majority (FNN ANALYSIS via BBG).

- South Korea's Kospi is showing modest outperformance, up +0.40%, near 3190 in index terms. The sell-side consensus remains for higher Kospi levels, with Goldman's upgrading its target, while J.P. Morgan stated the index could get to 5000 within the next few years.

- Taiwan markets are struggling for further upside, with the Taiex down around 0.70% at this stage.

- The ASX 200 is around flat. In SEA, aggregate moves aren't large at this stage. Thailand, Indonesia and Philippines markets are all in the green.