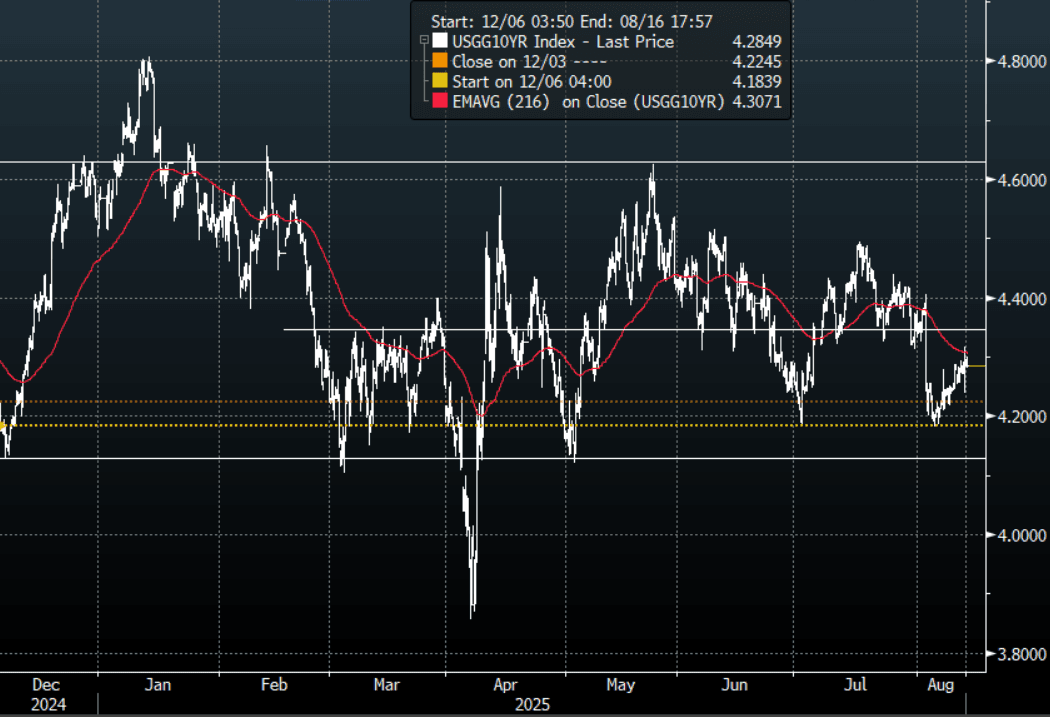

US TSYS: Yield Moves Muted In A Quiet Session

The TYU5 range has been 111-23 to 111-27 during the Asia-Pacific session. It last changed hands at 111-27, up 0-01 from the previous close.

- The US 2-year yield is trading around 3.73%, unchanged from its close.

- The US 10-year yield has edged slightly lower trading around 4.285%.

- Price action in the long-end is a little disconcerting for the bulls though the 10-Year yield still trades below its 4.30/35%% pivot within the wider range 4.10% - 4.65%. There should still be buyers of treasuries on bounces back towards 4.30/35%, looking to initially test the 4.10% area.

- Ben Hunt(Epsilon Theory) on X: “If we’re gonna cut in Sept (90% mkt odds as I write this) with core at 3.1% and rising, wages at 3.9% and rising, stocks and home prices at all-time highs … Can we at least stop talking about the Fed’s 2% inflation ‘target’? It’s just insulting to continue this charade.”

- Jim Bianco on X: “YoY Core CPI, 3.1%. Up 0.3% in the last 3-months. In the last 40 YEARS, only once has the Fed CUT rates when core was above 3% AND the 3m chg was >0.3%, Oct 1990 to Mar 1991. Agree with @EpsilonTheory, the 2% inflation target is dead. We are accepting a higher inflation world.”

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

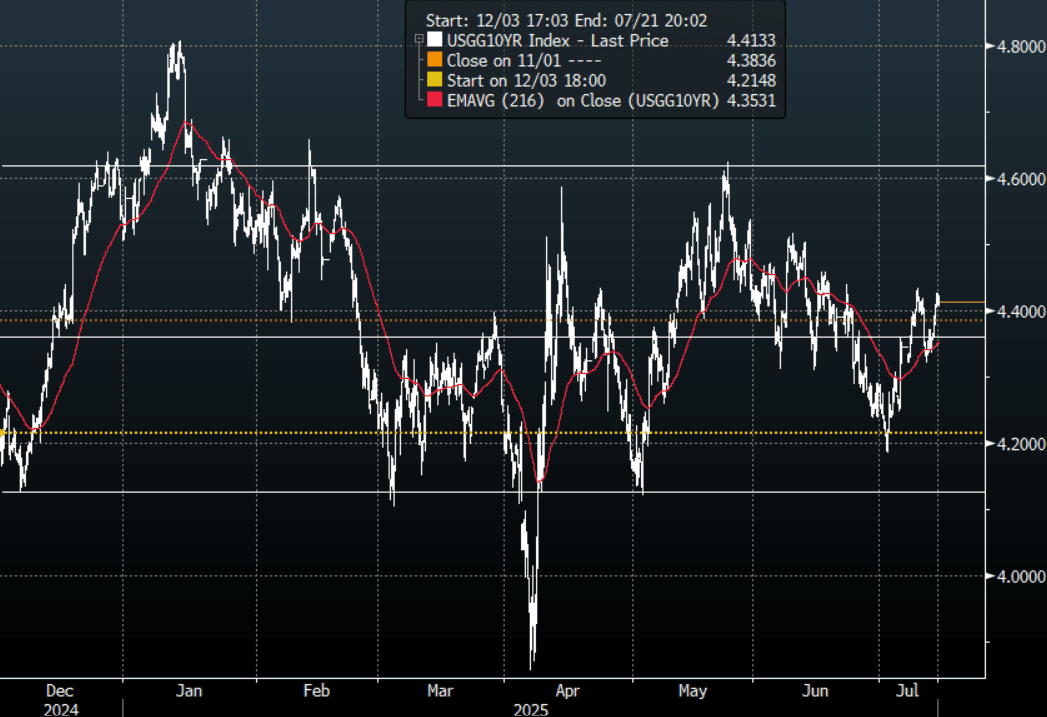

US TSYS: Asia Wrap - Quiet Session For US Bonds

The TYU5 range has been 110-24+ to 110-28 during the Asia-Pacific session. It last changed hands at 110-27, up 0-04 from the previous close.

- The US 2-year yield has edged lower trading around 3.88%

- The US 10-year yield has edged higher trading around 4.413%.

- The 10-year yield is again testing the 4.40/45% pivot within its wider 4.10% - 4.65% range. The market is clearly worried about inflation and the CPI this week will be a critical input into the market's thinking. A sustained close back above the 4.45% area could see more longs pared back, above here and the focus will turn back to the 4.60% area.

- Nick Timiraos on X: “Penn’s Peter Conti-Brown: “We are in a high-stakes moment in the history of the Federal Reserve. It seems clear to me that the Trump administration, using various mechanisms, [has] now cooked up a post-hoc explanation for Powell’s removal.”

- "TRUMP: IF POWELL TO STEP DOWN WOULD BE A GOOD THING" - BBG

- MNI BRIEF: US Budget Surplus $27B In June; YTD Deficit $1.3T. The U.S. government posted a USD27 billion budget surplus for June, up USD98 billion from a year earlier, reflecting strong tax receipts and collections of import duties, the Treasury Department said Monday.

Fig 1: 10-Year US Yield Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Steady Today After Friday Strong Gain

Gold is little changed in today’s Asia-Pac session, after closing ~1% higher at $3355.59 on Friday.

- This came despite US tsys finishing Friday’s session with a bear-steepener. Higher rates are typically negative for gold, which doesn’t pay interest. Cash US tsys are slightly mixed in today's Asia-Pac session, with yields 1bp lower to 1bp higher.

- (Bloomberg) – “Gold has a raft of supportive drivers, from central-bank buying and investor inflows into exchange-traded funds to concerns about the trade war and, separately, the US fiscal outlook.”

- “Central banks and other institutions accumulated about 77 tons of gold on average each month from January through to May, according to Goldman Sachs Group Inc., which maintained forecasts for bullion to rally to fresh records in the coming quarters.”

- Mounting pressure on Federal Reserve Chair Jerome Powell continues, with President Donald Trump criticising his monetary policy approach as overly restrictive.

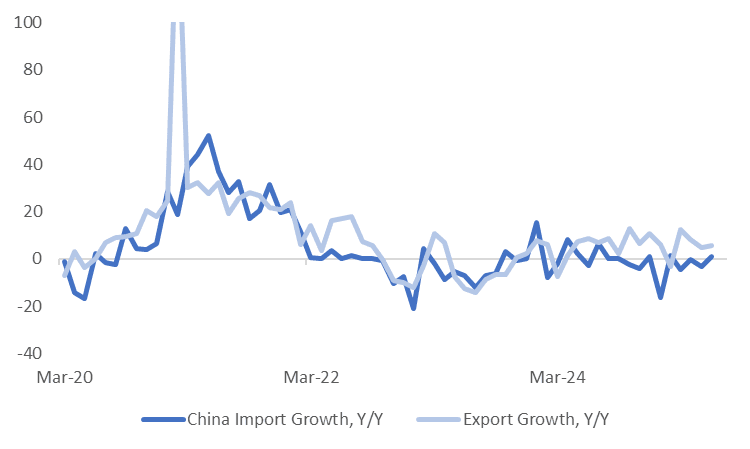

CHINA DATA: Export & Import Trends Improve, Rare Earth Exports Rebound

China June trade figures were slightly better than forecast. Exports rose 5.8%y/y, against a 5.0% forecast (4.8% was the May outcome). Imports rose 1.1%y/y, versus 0.3% forecast and -3.4% for May. The trade surplus pushed higher to $114.8bn, slightly above forecasts (near $112bn), while the May print was $103.22bn.

- In terms of commodity import volumes, we had coal down slightly to 33.04mln tonnes (36.04 was the May outcome). Crude oil rose though as did iron ore (to 105.95mln tonnes). Copper and natural gas rose, while soybeans fell slightly.

- Our China policy team noted that H1 imports were impacted by lower commodity prices: "Bulk commodities accounted for about 30% of China's total import value, Wang said, noting the average price of crude oil, iron ore and soybeans dropped more than 10% y/y in H1, dragging down the overall growth rate by 2.7 percentage points."

- Rare earth export volumes rose 32% in m/m terms and were +11.9%y/y. This was a sticking point from the US side around recent trade negotiations. China promised to accelerate export licenses in this space.

- Still, overall exports to the US were still down 16.1%y/y (per BBG). The trade surplus with the US rose to $26.57bn, the first rise since March of this year.

- The trade surplus with the EU eased to $25.94bn from $26.62bn. the surplus with Hong Kong rose to $26.15bn from $22.97bn.

- China also saw lower trade deficits with both Taiwan and Australia.

Fig 1: China Export & Import Trends Y/Y

Source: Bloomberg Finance L.P./MNI