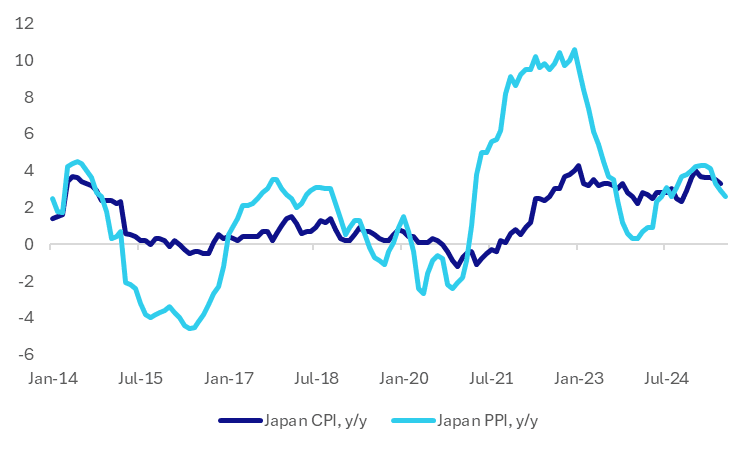

JAPAN DATA: July PPI In Line, Suggests Further Moderation In Headline Y/Y CPI

Japan's July PPI was close to expectations. The m/m outcome printed at +0.2%, in line with expectations, while the June outcome was revised to 0.1%m/m (originally reported as -0.2%). In y/y terms we printed at 2.6%, versus 2.5% forecast and 2.9% prior.

- The chart below plots the headline PPI y/y, versus the National CPI, also in y/y terms. At face value it implies some further softening in y/y CPI momentum for July. Note that this print comes out on August 22nd.

- In terms of the detail, manufacturing was up 0.2%, while some commodities, most notably petroleum, coal, rose for the first time in a number of months (+1.8%).

- The data is unlikely to shift near term BoJ thinking around wait and see mode from a policy standpoint.

Fig 1: Japan PPI & CPI, Y/Y

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

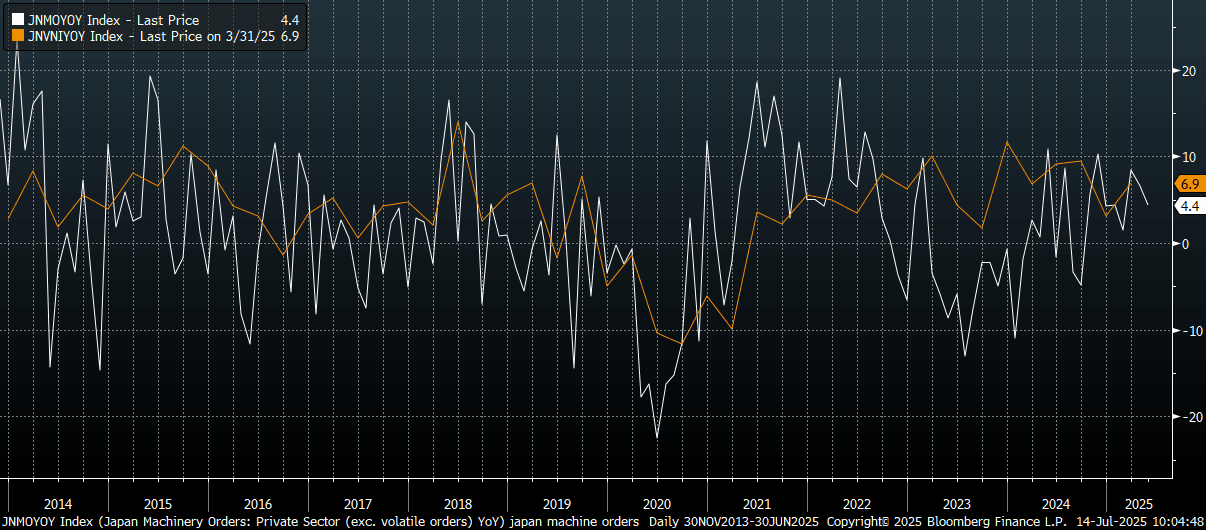

JAPAN DATA: Core Machine Orders Y/Y Slows, But Still Pointing To Resilient Capex

Japan May machine orders were slightly above market forecasts in m/m terms. We printed at -0.6%m/m, versus the -1.5% forecast. The April fall of -9.1% was unrevised. In y/y terms we were slightly below forecasts, printing 4.4%, versus 5.2% expected, while 6.6% was the May outcome.

- The chart below plots core machine orders, in y/y terms, against Japan quarterly capex (also in y/y terms). It implies some softer Capex momentum risks all else equal, but still positive growth.

- Looking at the detail, manufacturing orders fell by 1.8%m/m (after a 0.6% dip in April). Non-manufacturing surged by 30.4%m/m though, to provide some offset.

Fig 1: Japan Core Machine Orders & Capex (Y/Y)

Source: Bloomberg Finance L.P./MNI

US TSYS: Cash Open

TYU5 is trading 110-26, up 0-03 from its close.

- The US 2-year yield opens around 3.879%, down 0.01 from its close.

- The US 10-year yield opens around 4.42%, up 0.1 from its close.

- (Bloomberg) -- “Trump and his allies are scrutinizing renovations at the Fed’s headquarters as potential grounds to remove Jerome Powell. Deutsche Bank strategist George Saravelos said the central bank chair’s dismissal is a major and underpriced risk that may trigger a selloff in the dollar and Treasuries.”

- Nick Timiraos on X: “Penn’s Peter Conti-Brown: “We are in a high-stakes moment in the history of the Federal Reserve. It seems clear to me that the Trump administration, using various mechanisms, [has] now cooked up a post-hoc explanation for Powell’s removal.”

- MNI BRIEF: US Budget Surplus $27B In June; YTD Deficit $1.3T. The U.S. government posted a USD27 billion budget surplus for June, up USD98 billion from a year earlier, reflecting strong tax receipts and collections of import duties, the Treasury Department said Monday.

- The 10-year yield is again testing the 4.40/45% pivot with its wider 4.10% - 4.65% range. The market is clearly worried about inflation and the CPI this week will be a critical input into the market's thinking. A sustained close back above the 4.45% area could see more longs pared back, above here and the focus will turn back to the 4.60% area.

MNI: MNI JAPAN MAY CORE MACHINE ORDERS -0.6% M/M; APR -9.1%

- MNI JAPAN MAY CORE MACHINE ORDERS -0.6% M/M; APR -9.1%

- JAPAN MAY MACHINE ORDERS POSTS 2ND STRAIGHT M/M DROP