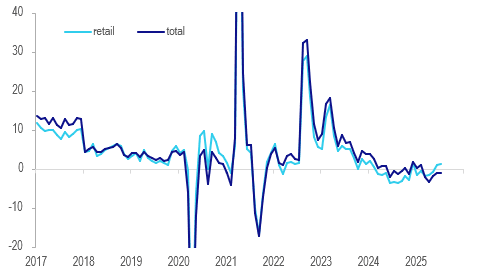

NEW ZEALAND: Gradual Recovery In Retail Card Spending

July NZ card transactions rose 0.6% m/m, the highest monthly increase this year, but the annual rate is still down 1.0%. Retail spending was up 0.2% m/m rising 1.2% y/y, signalling a gradual recovery in nominal consumption. It has been trending higher since the March trough at -1.8% y/y. The RBNZ is likely to cut rates on August 20 as inflation is in the band and the economic recovery remains subdued, and the July card data was consistent with this.

- While total retail spending rose slightly on the month, the core was close to flat. Statistics NZ noted that consumables transactions rose 0.5% m/m, while vehicles ex fuel jumped 5.2%. Apparel fell 1.9% and durables -0.8%.

- Non-retail ex services expenditure increased 1.6% m/m but services only 0.3%.

NZ card spending y/y%

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Modestly Cheaper After Friday's Heavy Close For US Tsys

ACGBs (YM -1.0 & XM -2.5) are modestly weaker after a heavy close for US tsys on Friday. US yields were 1-8bps higher, with a steeper curve.

- Tariff headlines buoyed US tsys briefly on Friday morning, but support gradually faded as exact tariff details were not announced.

- Chicago Fed President. Goolsbee tells the Wall Street Journal in an interview Friday that this week's latest round of tariff announcements could force him and the FOMC to wait for longer before having enough clarity to cut rates.

- June CPI is the highlight of next week's US data slate, with MNI's early roundup of analyst expectations showing an anticipated acceleration in the main measures of inflation.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -5bps.

- The bills strip little changed.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in August is given an 89% probability, with a cumulative 60bps of easing priced by year-end.

- Today, the local calendar will be empty.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$800mn of the 4.25% 21 March 2036 bond on Wednesday and A$1100mn of the 1.00% 21 November 2031 bond on Friday.

BONDS: Bear-Steeper In Line With US Tsys, Domestic Data Improves

In local morning trade, NZGBs are showing a modest bear-steepener after US tsys finished Friday cheaper. US yields were 1-8bps higher, with a steeper curve.

- Tariff headlines buoyed US tsys briefly on Friday morning -- gaining after Pres Trump announced a 35% tariff on Canada starting August 1, while considering 15%-20% tariffs on most other trading partners. However, support for US tsys gradually faded as exact tariff details were not announced.

- Rates ignored Trump to make a "major statement" on Russia Monday while stocks retreated.

- NZ Performance of Services Index rises to 47.3 in June from a revised 44.1 in May. The improvement in the services index mirrors, to some degree, the rebound in the manufacturing index from last Friday (48.8 from 47.4). “Every month it remains below 50 suggests service sector conditions are getting worse not better” and “The timeline for New Zealand’s long-awaited economic recovery just keeps getting pushed further and further out”: BNZ senior economist Doug Steel.

- NZ retail card spending rose 0.5% m/m in June versus a revised -0.1% in May.

- Swap rates are 2-4bps cheaper, with a steepener 2s10s curve

- RBNZ dated OIS pricing is little changed across meetings. 18bps of easing is priced for August, with a cumulative 33bps by November 2025.

JPY: USD/JPY - Continues To Challenge Conviction Of JPY Bulls

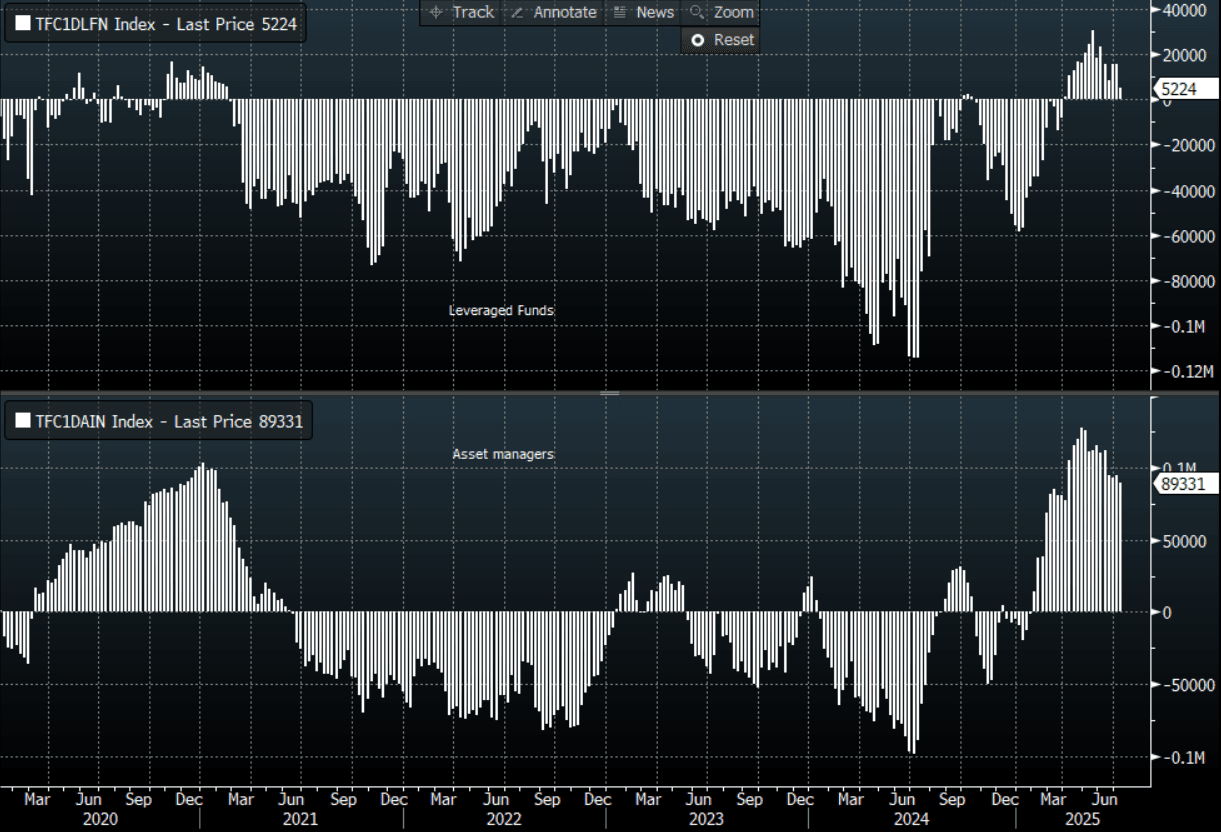

The Friday night range was 146.72 - 147.52, Asia is currently trading around 147.40. USD/JPY kept the pressure on JPY longs pushing above 147.00. The USD/JPY relentless march higher has been pretty telling, challenging a market positioned the wrong way. Price is now consolidating some of those recent gains, dips back towards 145.00 should now find support first up. CFTC Data shows leveraged funds have pared back their JPY longs almost back to flat, Asset managers have pared back some of their position but still continue to run a decent sized long JPY position.

- (Bloomberg) - “The US government is pressing Japan and Australia to clarify their roles in the event of a US-China war over Taiwan, a move that upsets America’s two key allies in the region, the FT reported.”

- “US trading partners trying to navigate the final weeks of negotiations before President Trump’s so-called reciprocal tariffs hit are facing a leader who has made clear he’s lost patience with talks.” - BBG

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to continue to correct higher the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.10($514m).Upcoming Close Strikes : 146.50($1.25b July 16).

- CFTC data shows Asset managers reduced their JPY longs slightly +89331, while leveraged funds have almost squared their newly built JPY longs +5224.

- Data/Event : Core Machine Orders, Industrial Production, Capacity Utilization

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P